Idiosyncratic FX drivers becoming apparent

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

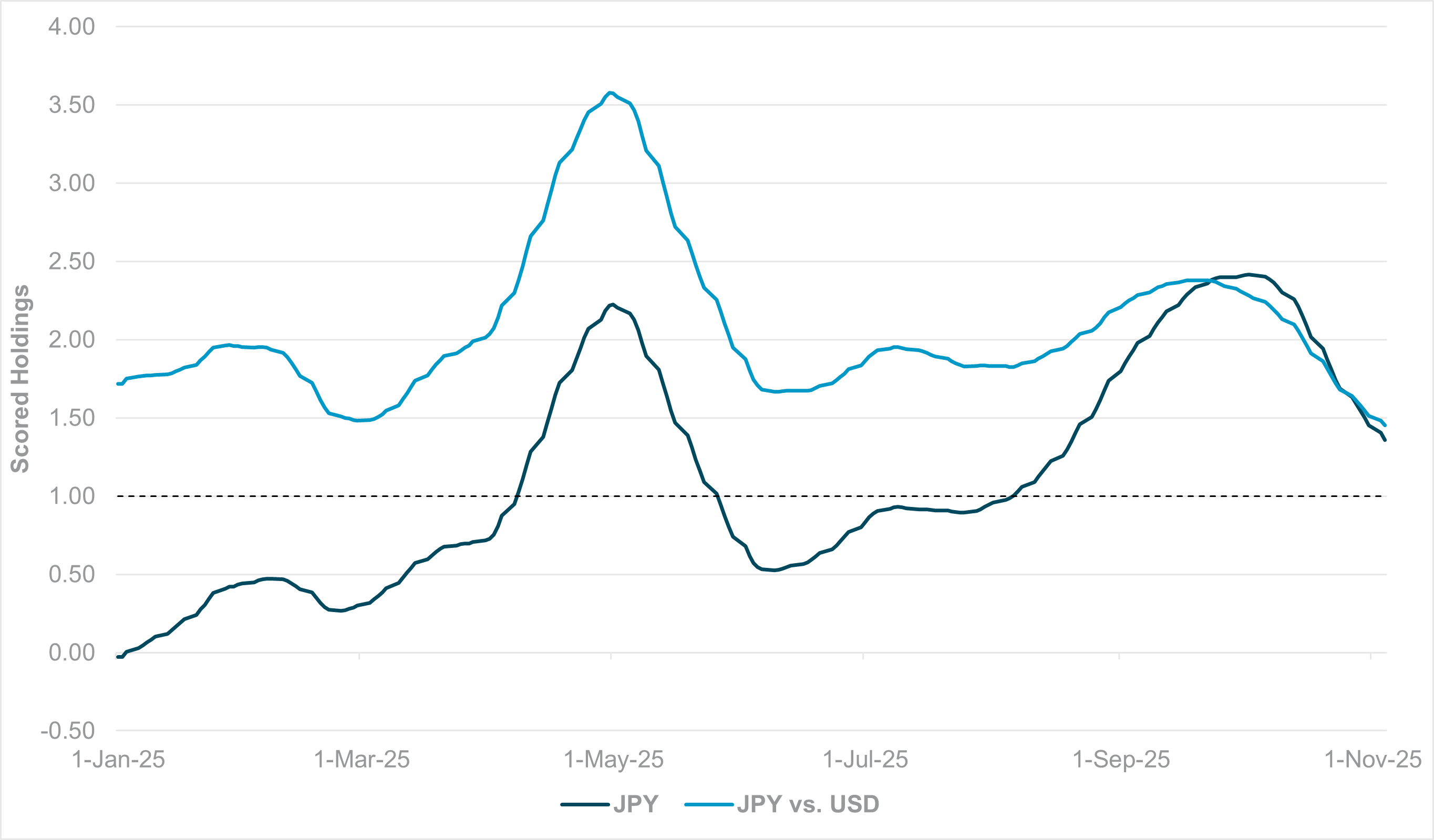

EXHIBIT #1: JPY AGGREGATE HOLDINGS AND USDJPY HOLDINGS (INVERTED)

Source: BNY

Our take

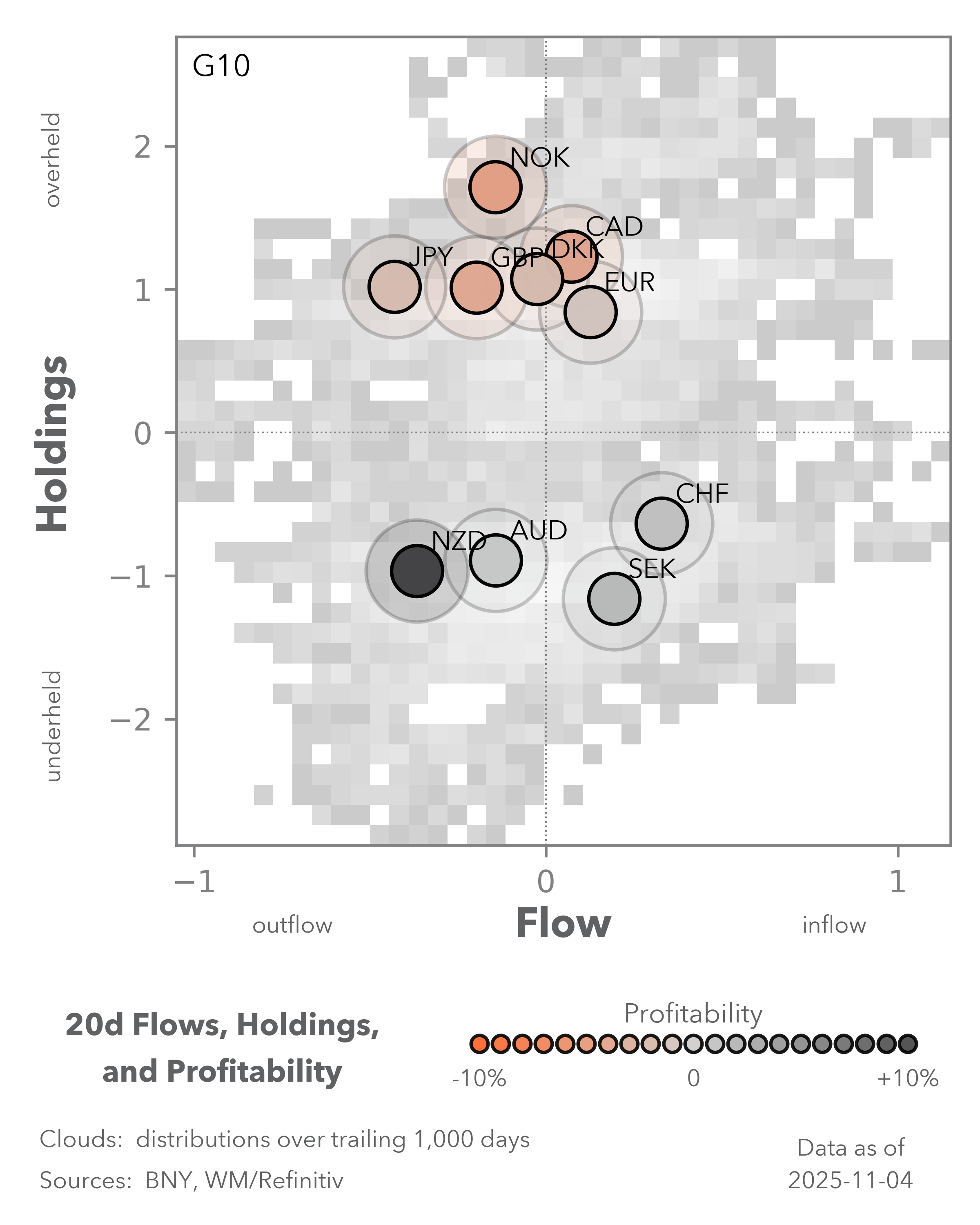

Japanese officials’ warnings about the yen (JPY) have increased recently, as reflected in our holdings figures. The JPY remains overheld both in aggregate and in the U.S. dollar-to-yen (USDJPY) exchange rate specifically (Exhibit #1), as positions were established around expectations that the Bank of Japan (BoJ) would hike rates and boost JPY valuations. However, after the Liberal Democratic Party’s election, aggregate JPY holdings have halved and appear set to return to the rolling 12-month average. Furthermore, some interesting structural changes are taking place within JPY holdings. USDJPY remains the dominant vehicle for JPY positioning and has been positively skewed (i.e., long JPY and short USD) for much of the year on expectations of JPY appreciation. However, a large body of JPY-funded (i.e., short JPY) positions continued to weigh on the overall aggregate figure. In other words, USDJPY was a proxy for a hawkish BoJ or broader domestic conditions, without disrupting the JPY-funded carry trades against other high-yielders in a general risk-on environment.

April’s risk-off environment triggered sharp unwinding of cross-JPY positions, though normal service resumed over the summer. The past quarter has seen a structural change, however, as JPY-funded positions were reduced amid rate cuts by more high-yielding central banks. By the end of September, JPY and USDJPY holdings had converged for the first time this year, and they remain well-aligned. As a result, there is no longer a material cross-JPY carry trade offsetting USDJPY flow in either direction.

Forward Look

Assuming markets continue to trade in a risk-off tone for the remainder of the year, residual cross-JPY carry trades may have helped provide JPY bids to offset USDJPY buying amid ongoing concerns about Japan’s monetary and fiscal outlook. Yet they are no longer in place. iFlow Carry indicates neutral interest in carry trades for now. Consequently, USDJPY purchases are now driving overall changes in JPY holdings. If policy consistency is established, we expect JPY holdings to stabilize. Time is of the essence, however, especially as the USD is gaining renewed support from shifts in the Fed’s stance and its role as a safe-haven asset.

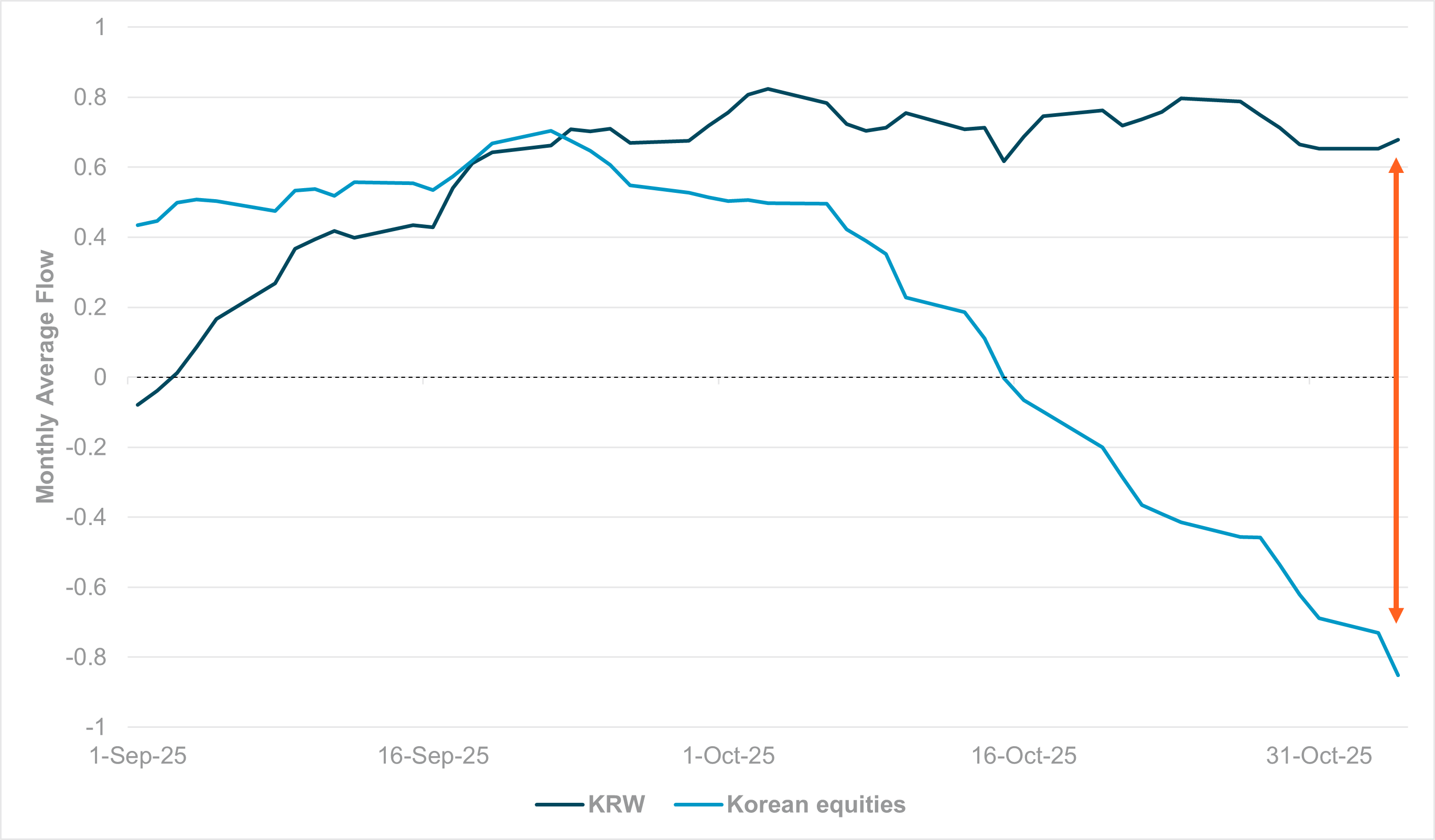

EXHIBIT #2: KRW VS. SOUTH KOREAN EQUITY MONTHLY SMOOTHED FLOW

Source: BNY

Our take

As equity holdings in the Asia-Pacific (APAC) region remain under pressure due to concerns over broader valuations in the semiconductor industry, currencies that benefited strongly, such as the South Korean won (KRW) and Taiwan dollar (TWD), will be of particular focus. For now, KRW continues to find good bids based on iFlow, and these purchases have been consistent since early September. Initially, we believed that they reflected the market’s view that currencies such as KRW, TWD, Chinese yuan (CNY) and Singapore dollar (SGD) were undervalued, despite lower yields, given their export prowess. This view also assumed that policymakers would tolerate currency appreciation as a form of tightening, particularly in South Korea and Taiwan, due to certain aspects of credit growth and the housing market.

However, since mid-October, equity flows have shifted sharply, and South Korea is now facing its strongest equity outflows since mid-June and the second-strongest YTD. As a result, some of the current stability in FX flows and holdings is likely due to the unwinding of hedges (Exhibit #2). In hindsight, this shift also offers insight into the extent of hedging on prior equity purchases, which appears to be high.

Forward look

Given recent spot performance in KRW and TWD, some capital outflows are likely occurring as equities continue to struggle. We will continue to monitor the changes in FX holdings. But if the current inverse relationship between FX and equity flows breaks, it may signal that the hedging component has run its course. In that case, any additional liquidation by cross-border investors will have a more meaningful FX impact. On the other hand, if both flows begin to stabilize, it could pave the way for fundamentals to reassert themselves. Without taking an outright view on AI, valuations remain compelling across APAC funders, and conditions may support new long positions.

EXHIBIT #3: OFFICIAL BRAZILIAN BALANCE OF PAYMENTS DATA VS. IFLOW EM LEADING INDICATOR

Source: BNY, Office for Budget Responsibility

Our take

We highlighted in Investor Trends that Brazilian equities are leading global equity inflows, despite some degree of concentration risk in the mining sector. Despite the Monetary Policy Committee’s (COPOM) outlook yesterday and ongoing pressure from the Finance Ministry on yield levels, Brazil’s overall balance of payments remains strong. This is holding even amid recent volatility in risk appetite.

Our iFlow EM framework aggregates daily cross-border inflows into emerging market equity and bond markets. It serves as a leading indicator of the portfolio account, gauging the strength of external inflows ahead of official data and assessing whether these flows can continue to support the currency. iFlow EM data for Brazil broadly matches trends on a rolling 12-month basis. As of August, combined equity and fixed income flows have turned positive again (Exhibit #3), showing renewed momentum.

Forward look

The current inflow environment is very different from 2021, when emerging market (EM) central banks were ahead of developed market (DM) peers in rate hikes, and global liquidity was abundant. If anything, at 15% nominal yields, Brazil could be seen as an outlier, maintaining excessively tight financial conditions despite weaker global growth and trade. These are the arguments being made by the Ministry of Finance. However, among peers, it is rare for our iFlow EM leading indicator to break decisively into positive territory. The current trend indicates official data will point to even stronger gains. If confirmed, these flows would continue to underpin the Brazilian real’s (BRL) status as the best-held EM currency, even though holdings are currently running at a slight loss.