GPIF the lead ship in APAC pension super tankers

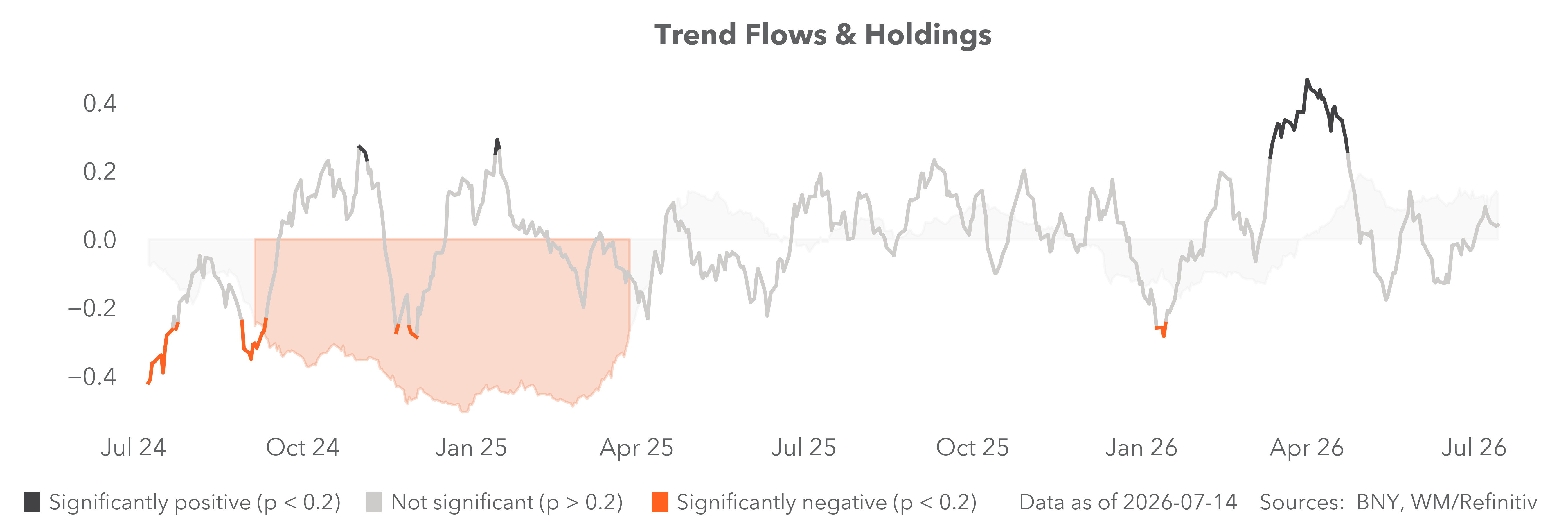

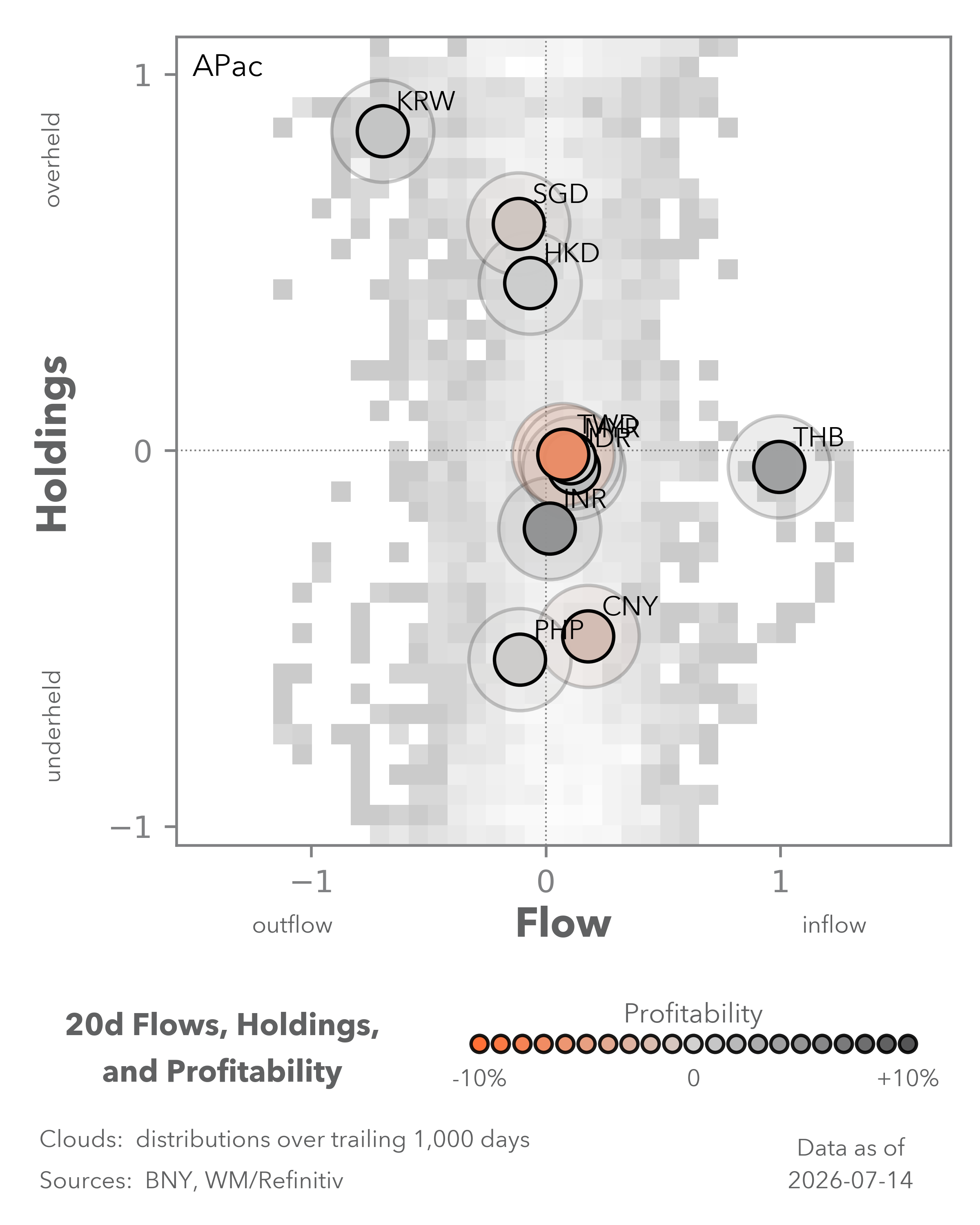

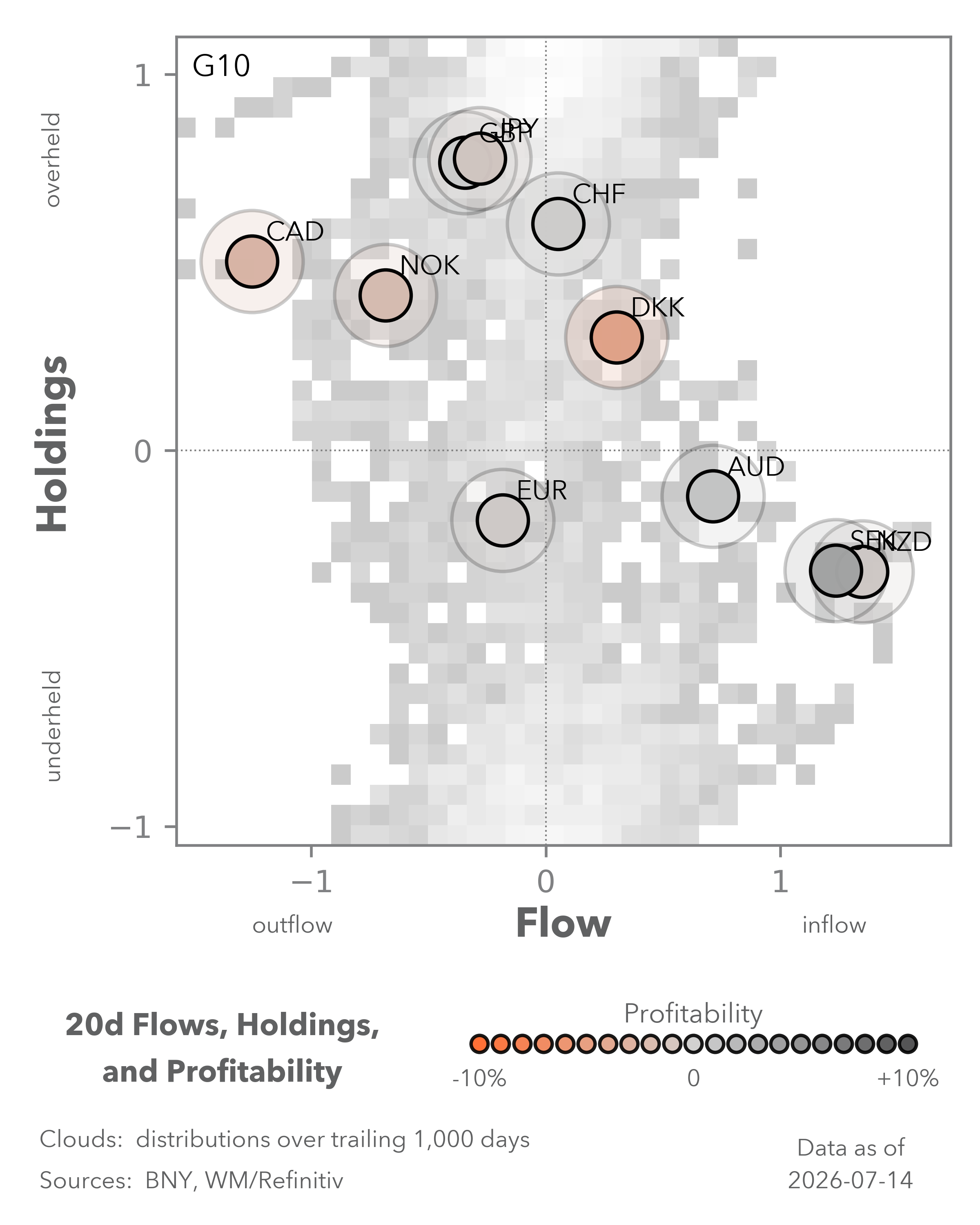

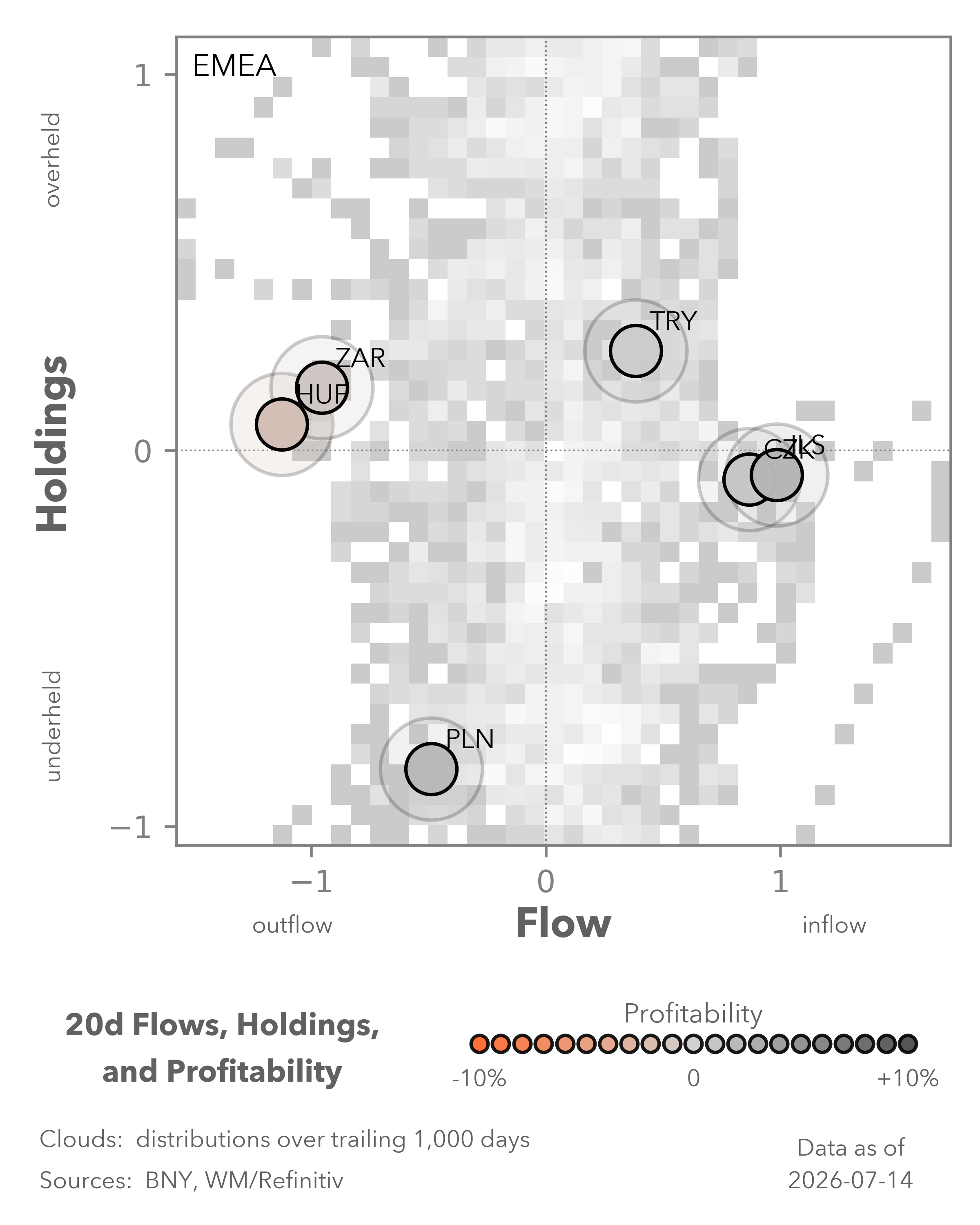

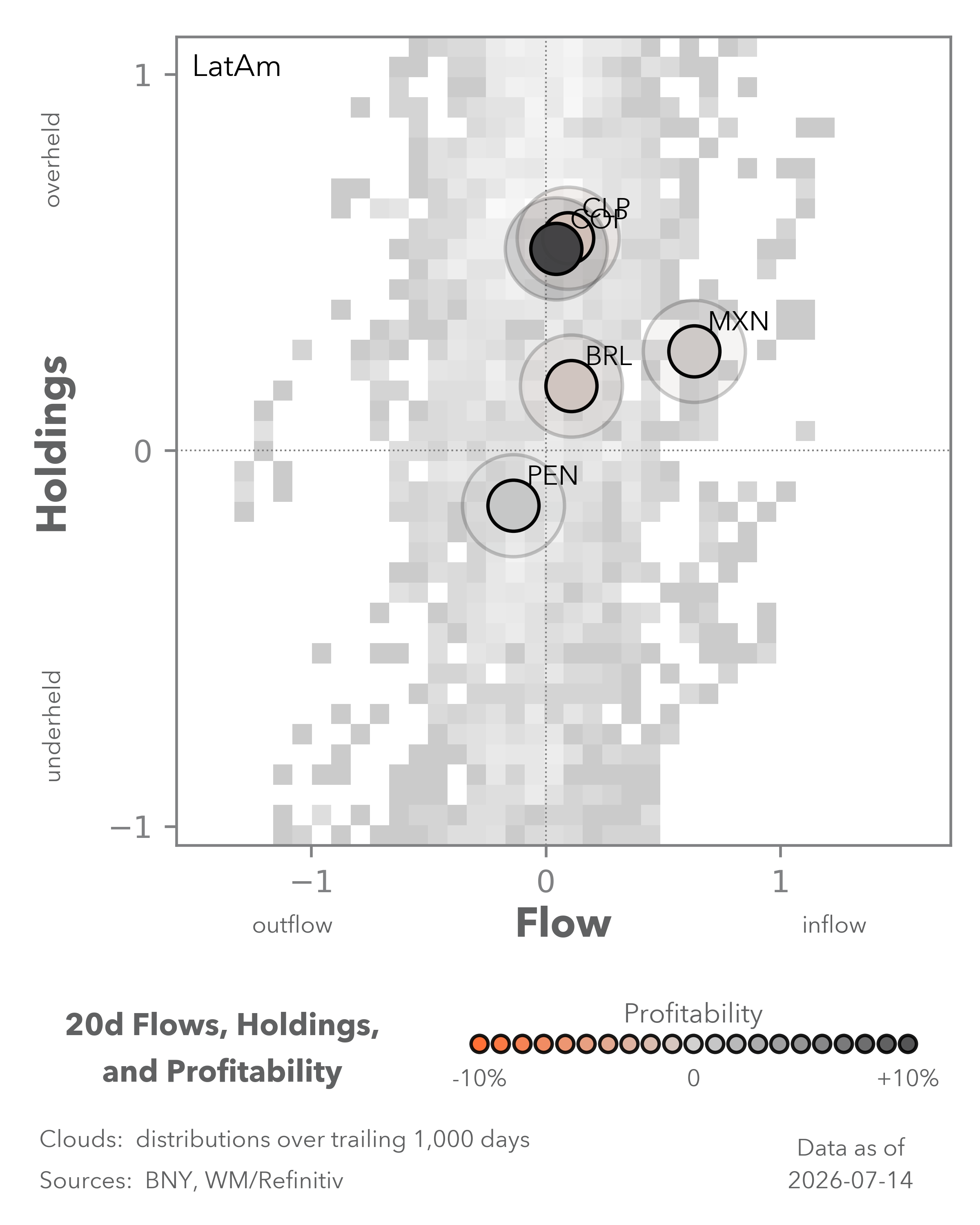

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

The Government Pension Investment Fund (GPIF) discussion is only the beginning of a broader debate on official-sector pension allocations across Asia. The largest public pension funds in Japan, South Korea and Taiwan together manage more assets than the three economies’ combined FX reserves, with almost half invested overseas. A gradual shift toward greater domestic allocation would provide an important structural tailwind for regional currencies. Reallocating existing portfolios, however, is only part of the adjustment. Sustained currency appreciation ultimately requires a larger share of newly generated domestic savings to remain invested onshore.

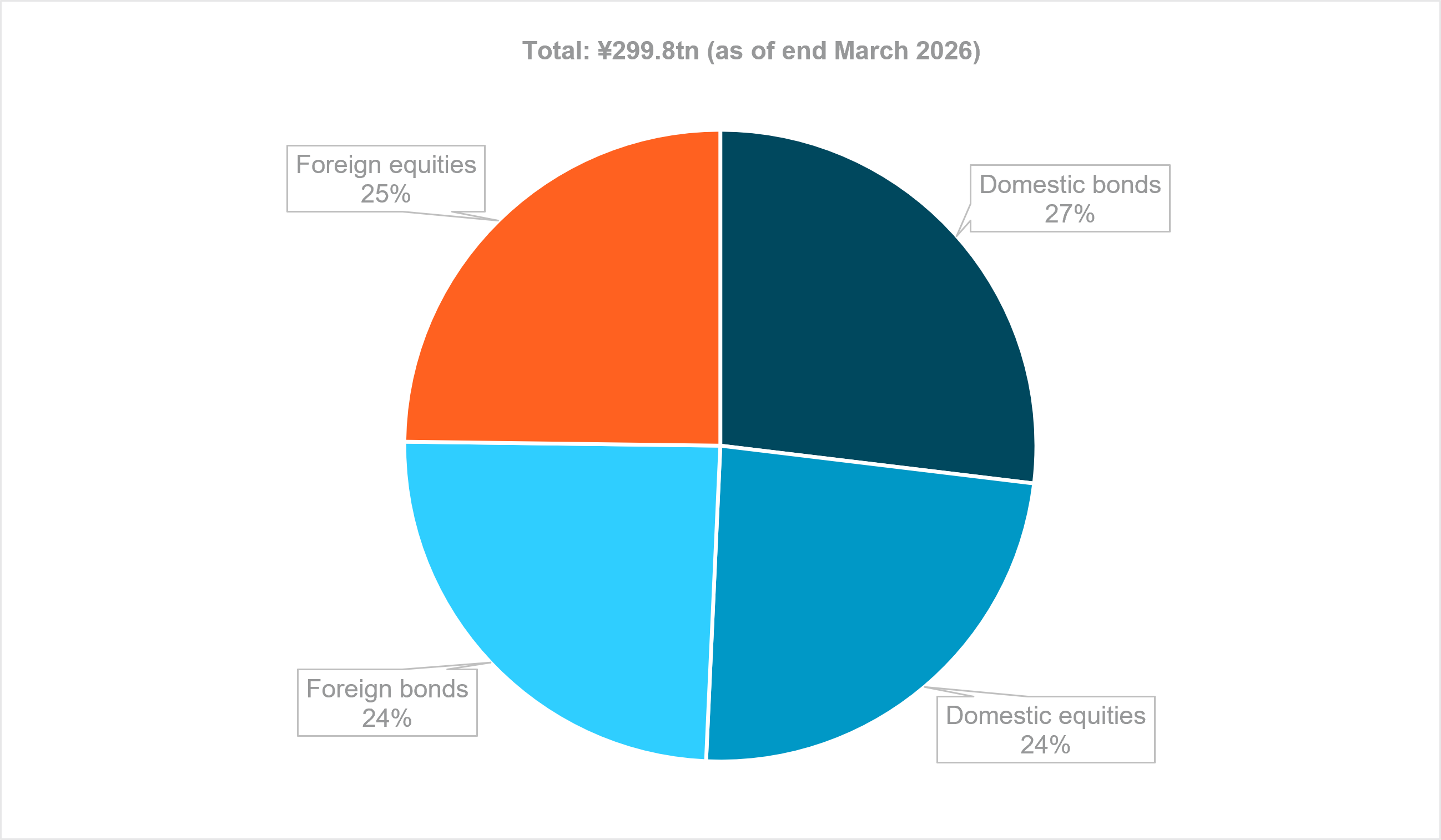

EXHIBIT #1: CURRENT GPIF ASSET ALLOCATION

Source: BNY, Bloomberg

Our take

The GPIF manages ¥299.8tn (approximately $1.9tn) as of March 31, 2026, making it the world’s largest public pension fund. The current policy asset mix became effective on April 1, 2025, as part of GPIF’s Fifth Medium-Term Plan (FY2025–FY2029) approved on March 31, 2025. It allocates 25% to domestic bonds, 25% to foreign bonds, 25% to domestic equities and 25% to foreign equities. The permitted deviation bands are ±6% for domestic bonds, domestic equities and foreign equities, and ±5% for foreign bonds. Aggregate bond and equity allocations each have ±9% deviation bands. Alternative assets are not established as a separate asset class. Investments in private equity, infrastructure and real estate are managed within the four core asset classes, with a maximum allocation of 5% of total assets.

As of March 31, the actual portfolio comprised 26.9% domestic bonds (¥80.7tn), 24.5% foreign bonds (¥73.4tn), 23.8% domestic equities (¥71.4tn) and 24.8% foreign equities (¥74.4tn). Alternative assets represented 1.7% of total assets.

Forward Look

Regardless of how GPIF ultimately executes, the policy discussion has clearly shifted toward greater domestic allocation. Pressure in the JGB market highlights the need for a broader domestic investor base, as fiscal financing requirements increase. Similar demographic and fiscal trends are emerging across North Asia. Even so, GPIF alone is unlikely to materially alter Japan’s external position. A ten-percentage-point portfolio reallocation equates to approximately $186bn, roughly equivalent to just over two months of the Ministry of Finance’s intervention during May 2024. Japan’s ¥562tn net international investment position remains substantially larger. More importantly, a lasting adjustment requires newly generated balance-of-payments surpluses to remain invested domestically rather than continuing to be recycled overseas.

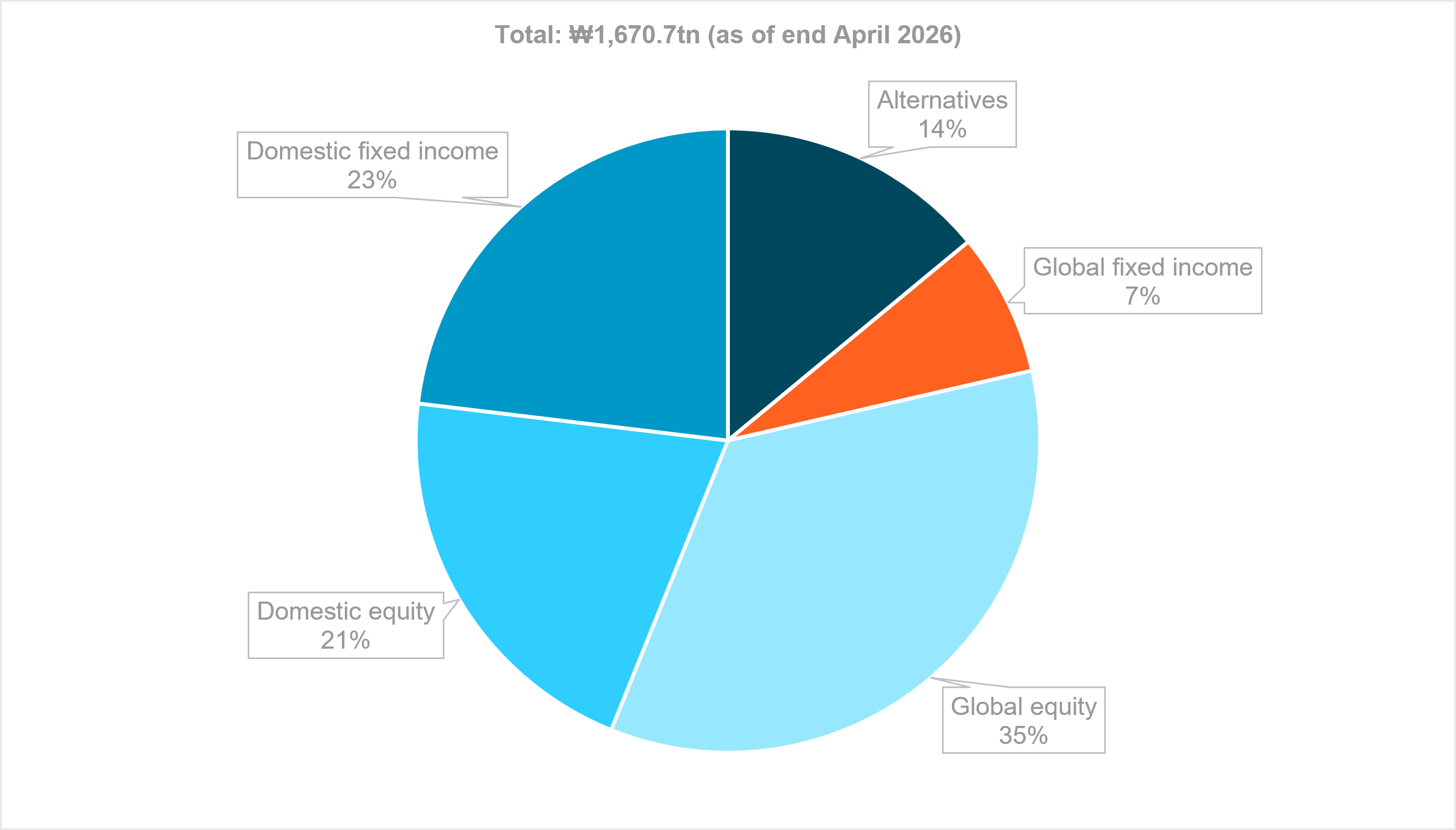

EXHIBIT #2: CURRENT NPS ASSET ALLOCATION

Source: BNY; HS 85 represents Electrical Machinery, Equipment and Parts, etc.

Our take

The National Pension Service (NPS) manages approximately ₩1,671tn (approximately $1.2tn). Under its 2026 Annual Fund Management Plan, the strategic asset allocation targets are 20.8% domestic equities, 34.7% foreign equities, 23.1% domestic fixed income, 7.4% foreign fixed income and 14.0% alternative investments. Alternative investments comprise private equity, infrastructure, real estate and private debt.

The NPS investment framework consists of a five-year mid-term asset allocation plan and an annual fund management plan, both approved by the National Pension Fund Management Committee. The NPS publishes both strategic asset allocation targets and actual portfolio allocations. The 2026 strategic asset allocation targets comprise 55.5% equities, 30.5% fixed income and 14.0% alternative investments.

Forward Look

South Korea has been identified repeatedly by U.S. Treasury Secretary Scott Bessent as not reflective of fundamentals, but domestic policymakers have become increasingly focused on retaining domestic savings. The announced semiconductor investment programs exceeding $500bn will require substantial domestic financing over time, increasing the incentive for export earnings and institutional savings to remain onshore. Relative to regional peers, however, NPS already maintains a lower overseas allocation, with foreign equities and bonds accounting for 42.1% of its strategic asset allocation. This suggests the scope for portfolio reallocation alone is more limited than in Japan.

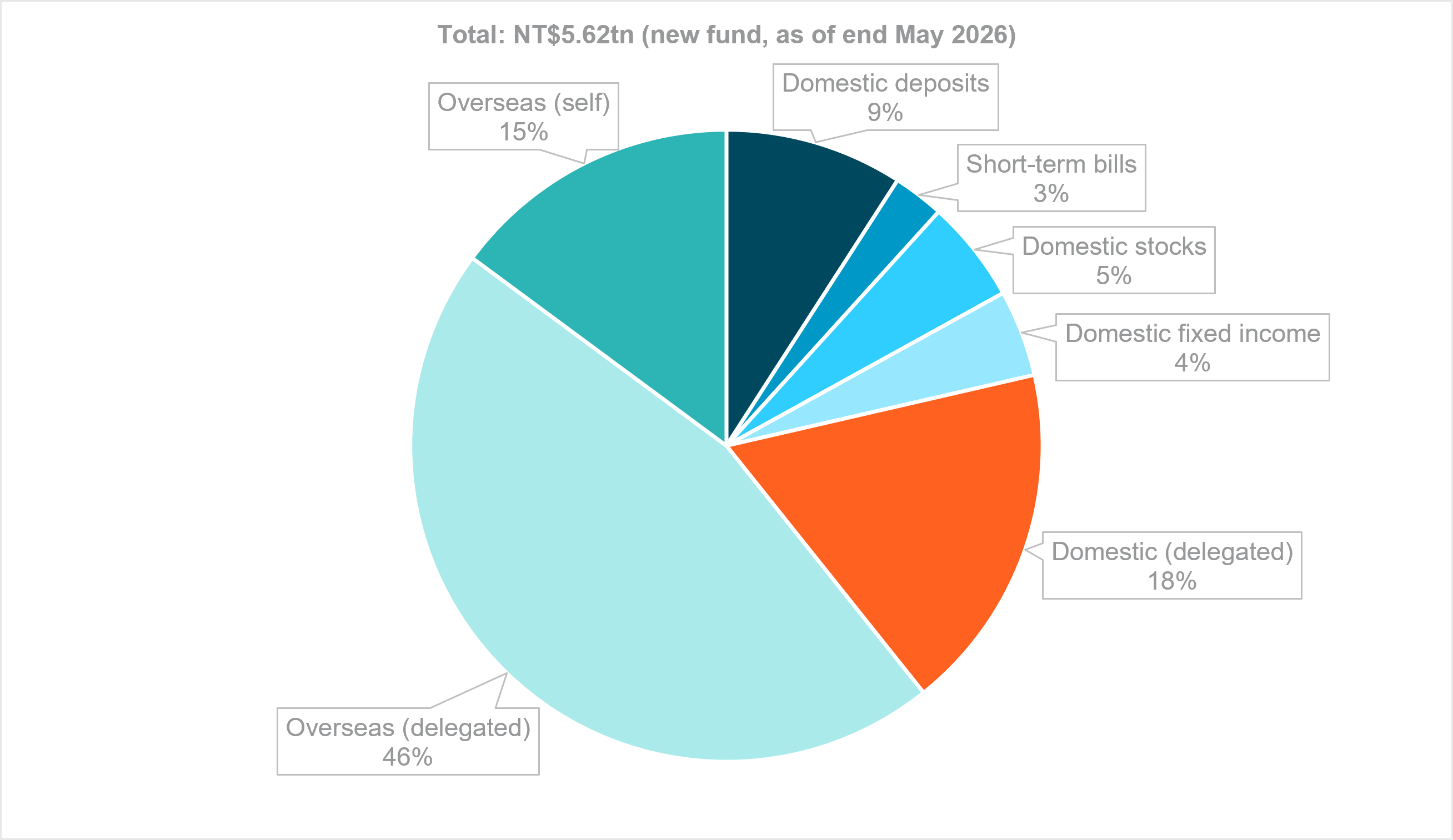

EXHIBIT #3: LPF (NEW FUND) ASSET ALLOCATION

Source: BNY, 8542 represents Electronic Integrated Circuits

Our take

Taiwan’s Labor Pension Fund (LPF) is managed by the Bureau of Labor Funds (BLF) under the Ministry of Labor and manages approximately NT$5.62tn (approximately $177bn) as of May 31, 2026. The BLF manages multiple government-sponsored funds. At end 2025, aggregate Labor Funds totaled approximately NT$7.79tn. Including entrusted management of the National Pension Insurance Fund and the Farmers’ Pension Fund, total assets under management exceeded NT$9.5tn.

Taiwan’s BLF doesn’t publish a fixed strategic asset allocation for the LPF. Instead, it publishes the fund’s portfolio composition each month. As of May 31, the portfolio comprised 9.11% deposits in financial institutions, 2.61% short-term bills, 5.25% domestic stocks and beneficiary certificates, 4.43% government, financial and corporate bonds, 14.87% overseas investments managed internally, 17.88% domestic delegated mandates and 45.85% overseas delegated mandates.

Forward look

Taiwan differs from Japan and South Korea in both fund size and domestic market depth. Overseas mandates account for 60.7% of the LPF portfolio, the highest among the three funds discussed. This leaves comparatively less scope for a material reduction in overseas allocations through portfolio rotation alone. As in South Korea, policies that encourage a greater share of newly generated domestic savings to remain invested locally are likely to have a more durable effect than reallocating existing portfolios.

The debate will inevitably move from theory to implementation. GPIF’s discussion signals that official-sector capital allocation is becoming an active policy tool rather than a long-term aspiration. Investors should treat this as the start of a multi-year structural theme, extending well beyond Japan. The opportunity is not simply to anticipate portfolio rotation, but to identify where governments are creating the conditions for new domestic savings to remain onshore. That is where the largest and most durable currency adjustments are likely to emerge.