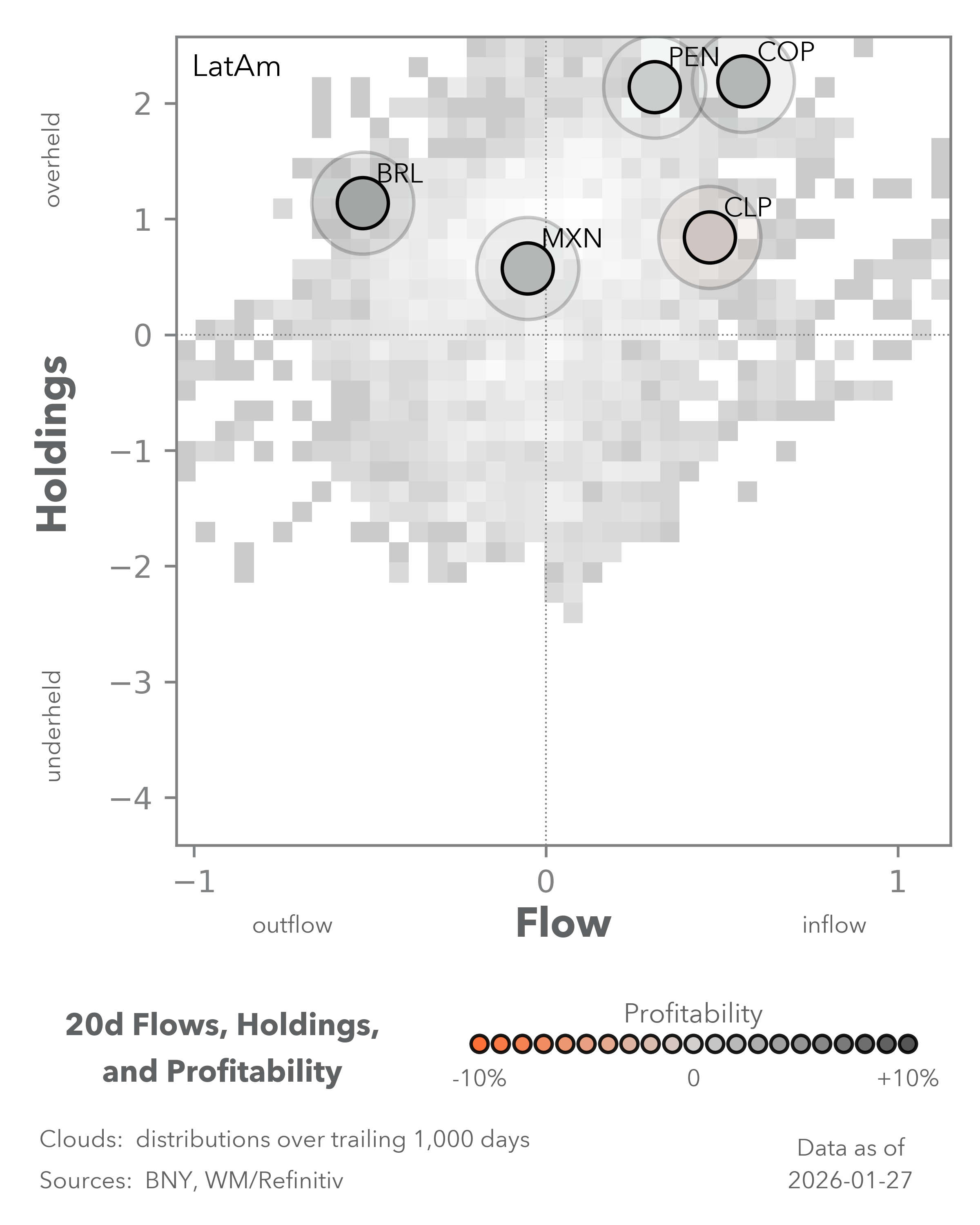

FX tolerance tested as key thresholds breached

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

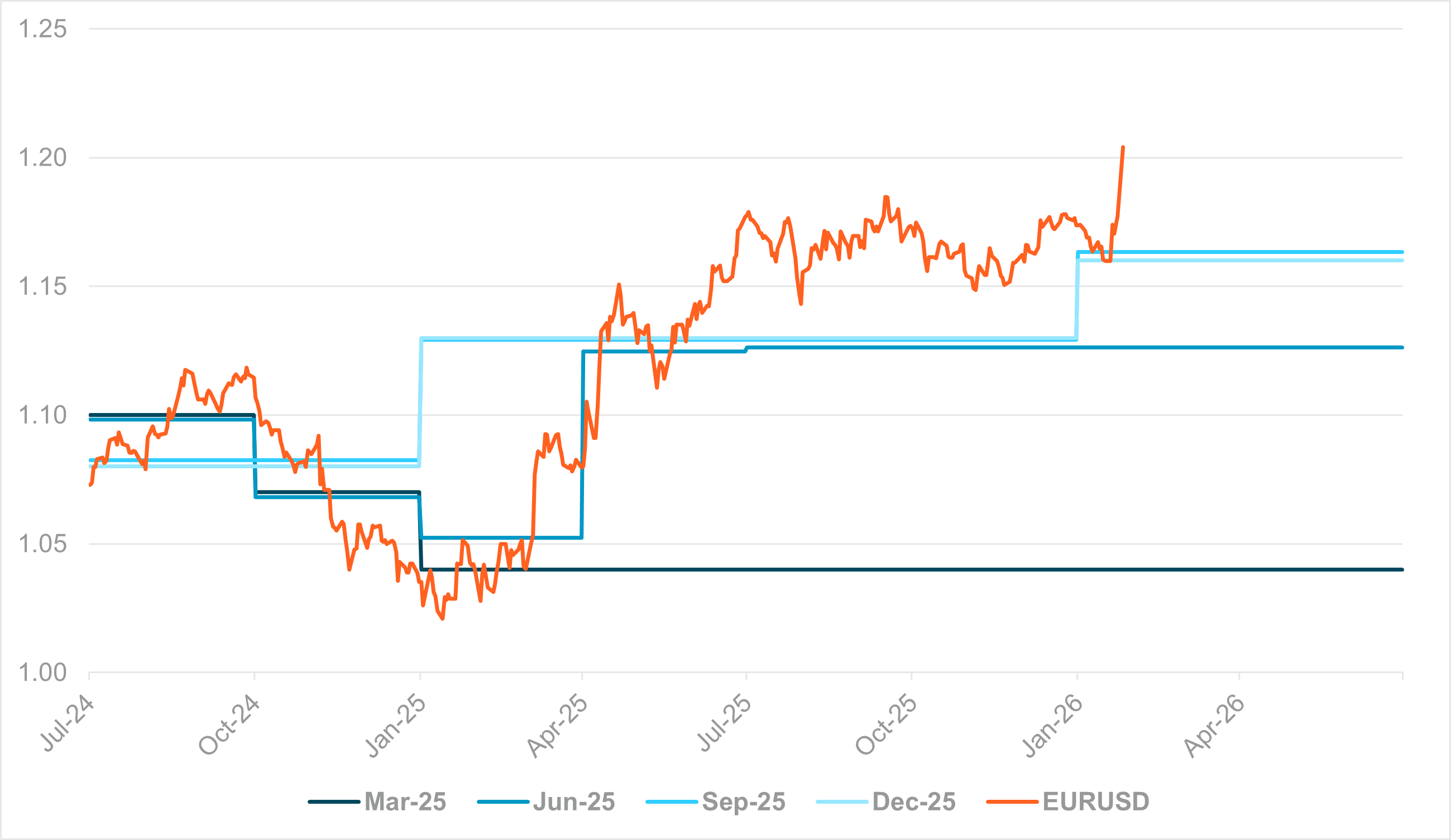

EXHIBIT #1: EURUSD VS. ECB QUARTERLY PROJECTIONS FOR 2025

Source: European Central Bank (ECB), BNY

Our take

Whether the U.S. is still exercising a traditional “benign neglect” policy toward the dollar remains to be seen. But the EURUSD’s return to 1.20 for the first time since mid-2021 has finally led to some Governing Council members breaking ranks, explicitly linking the value of the EUR to monetary policy. The central bank governors of France and Austria were the first to highlight vigilance, though other Governing Council members also stressed that there was no need for alarm. Either way, the current exchange rate volatility and tariff uncertainty point to a more cautious approach by the European Central Bank (ECB), and we suspect monetary policy can no longer be characterized as being in “a good place.” We have long held the view that Europe’s structural issues with exports already required some degree of support through limiting currency strength. However, the speed at which the dollar has fallen across the board means pass-through risk is now front-loaded.

Forward Look

Although EURUSD stayed well above the ECB’s base scenario last year without triggering strong disinflation risk (Exhibit #1), trade uncertainty persists, and there is no clear path toward a global cycle recovery that would mitigate inflation risk. Based on the ECB’s December projections, an average 1.21 represents the 75th percentile of the exchange rate’s interquartile range of option-implied density over the relevant forecast period and a deviation of 4.3% from baseline. The expected deviation is only 0.1% in HICP, which is not enough to trigger a strong response.

Consequently, we acknowledge that the 1.20 to 1.21 range is effectively the threshold at which the exchange rate can initiate a conversation about negative pass-through risk and monetary policy implications. This is precisely what is taking place with a range of opinions already being aired. Although forecasts may change, the December staff projections indicate that EURUSD at 1.25 would clearly breach the option-implied density range – that is, a full overshoot and potentially enough to trigger a change in guidance.

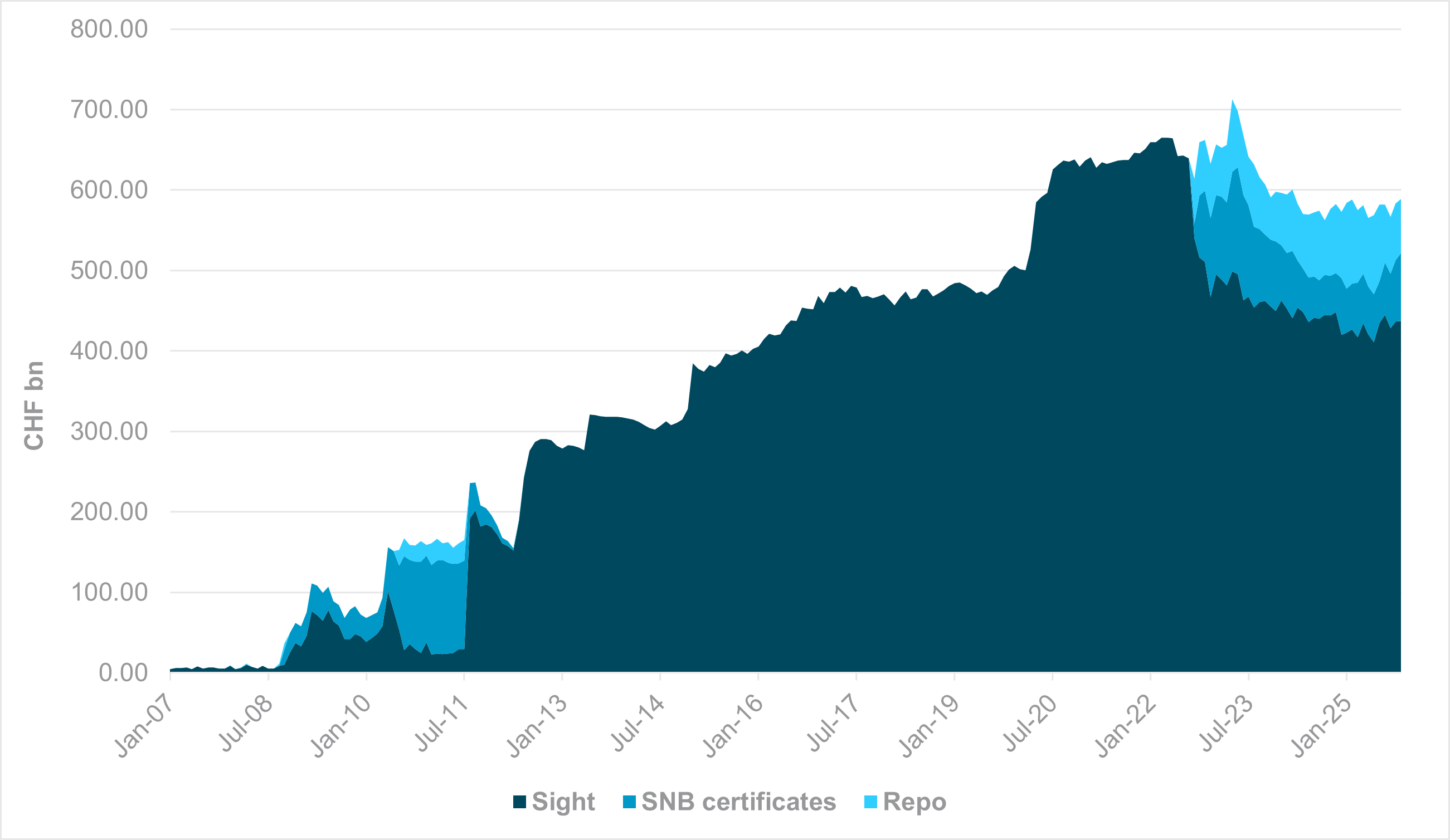

EXHIBIT #2: SNB LIABILITIES

Source: Swiss National Bank (SNB), BNY

Our take

The CHF has once again distinguished itself as the core G10 safe-haven currency – and even globally – while interest in holding high-yielding currencies remains elevated. Inevitably, as key levels are breached in USDCHF and even EURCHF, questions are being raised over a policy reaction by the Swiss National Bank (SNB), especially amid challenging data and inflation struggling to register clear positive momentum. In our view, the SNB will not overreact and will wait for its March conditional inflation forecast, given that current demand for the franc is not driven by Eurozone- or EUR-based factors, and the ECB is not considering a significant easing in financial conditions. Aside from minimal smoothing operations, the bar remains high for any active open market adjustments.

Forward look

Our base case is that negative rates will not be adopted at all for the current policy cycle, though it will remain an option if there is clear deterioration in inflation and inflation expectations. Intervention to weaken the CHF is even more remote, and unlike 15 years ago, could lead to greater difficulties in trade relations with the U.S. Before cutting benchmark rates into negative territory, however, we believe the SNB has ample room to utilize its balance efficiently to engineer far lower money market rates. These are already negative – the SARON® (Swiss Average Rate Overnight) fix has recently drifted higher, from nearly –8bp at the beginning of the year to –4.3bp at the end of last week.

Through early redemption of SNB certificates and the rolling off of repurchase agreements with banks, the SNB can actively “unlock” an additional CHF 150bn of sight deposits without any balance sheet adjustments, and push money market rates further negative. As we doubt any G10 peer will move toward zero – let alone negative rates – this cycle, that leaves ample room for CHF to realize funding currency status.

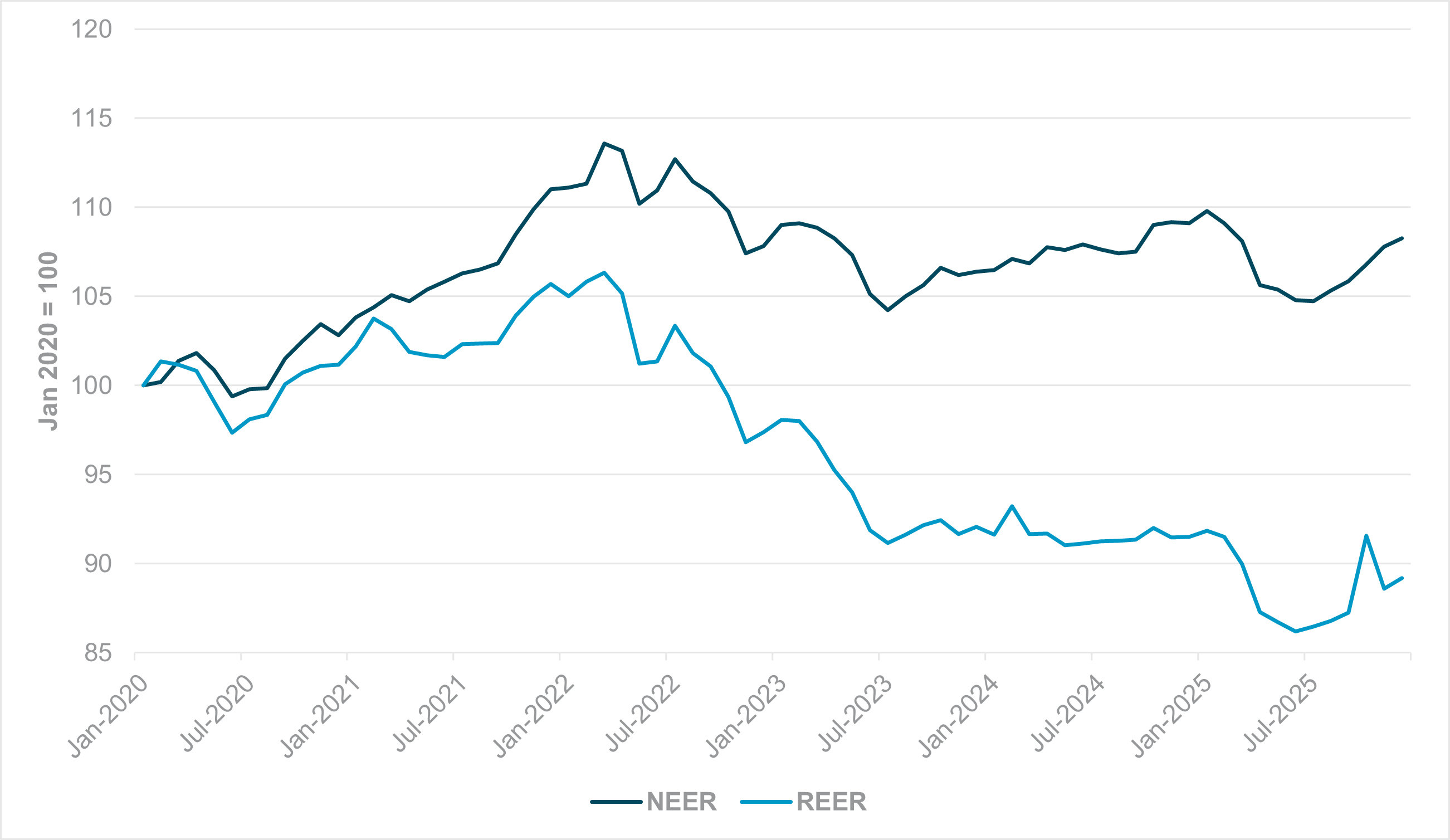

EXHIBIT #3: CNY BIS EFFECTIVE EXCHANGE RATE INDICES – REAL VS. NOMINAL

Source:Bank for International Settlements (BIS), BNY

Our take

We believe the more sustainable declines in the dollar will be against funding APAC currencies, and this is also in line with U.S. objectives. KRW and JPY are under pressure at present, and the push for gradual CNY appreciation has been on the agenda of every U.S. Treasury Secretary over the last two decades. On this note, we believe that Beijing and Washington, D.C. are largely in alignment. The USDCNY fixing has broken decisively through 7.00 in recent sessions, and we expect the nominal effective exchange rate (NEER) to easily move through the highs seen in early 2025. Furthermore, recent comments from the People’s Bank of China (PBoC) suggest no conflict between allowing CNY strength and loosening monetary conditions through the credit channel.

Forward look

However, the process will be carefully managed. The PBoC’s global peers should recognize that appreciation in the real effective exchange rate (REER) is far more valuable for optimal global economic rebalancing, especially in trade. Between October and December 2025, China’s PPI registered three straight months of sequential growth for the first time since Q1 2022, and there hasn’t been any monthly contraction since August. However, producer prices are still down by 2% on an annualized basis, and the cumulative drag on the CNY REER from price differences has become extreme.

Price growth remains fragile and excessive NEER gains could become disinflationary. This could trigger a disproportionately “involuted” response onshore, with wage restraint and other cost-cutting measures further suppressing input and output prices. As with the ECB and SNB, a clearer policy assessment will likely follow the March National People’s Congress, when the year’s fiscal outlook is announced.

All else being equal, CNY appreciation will accelerate only once authorities are confident that price momentum – through the domestic demand channel – is strong enough to offset pass-through risk.