Flying blind vs. benign neglect

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

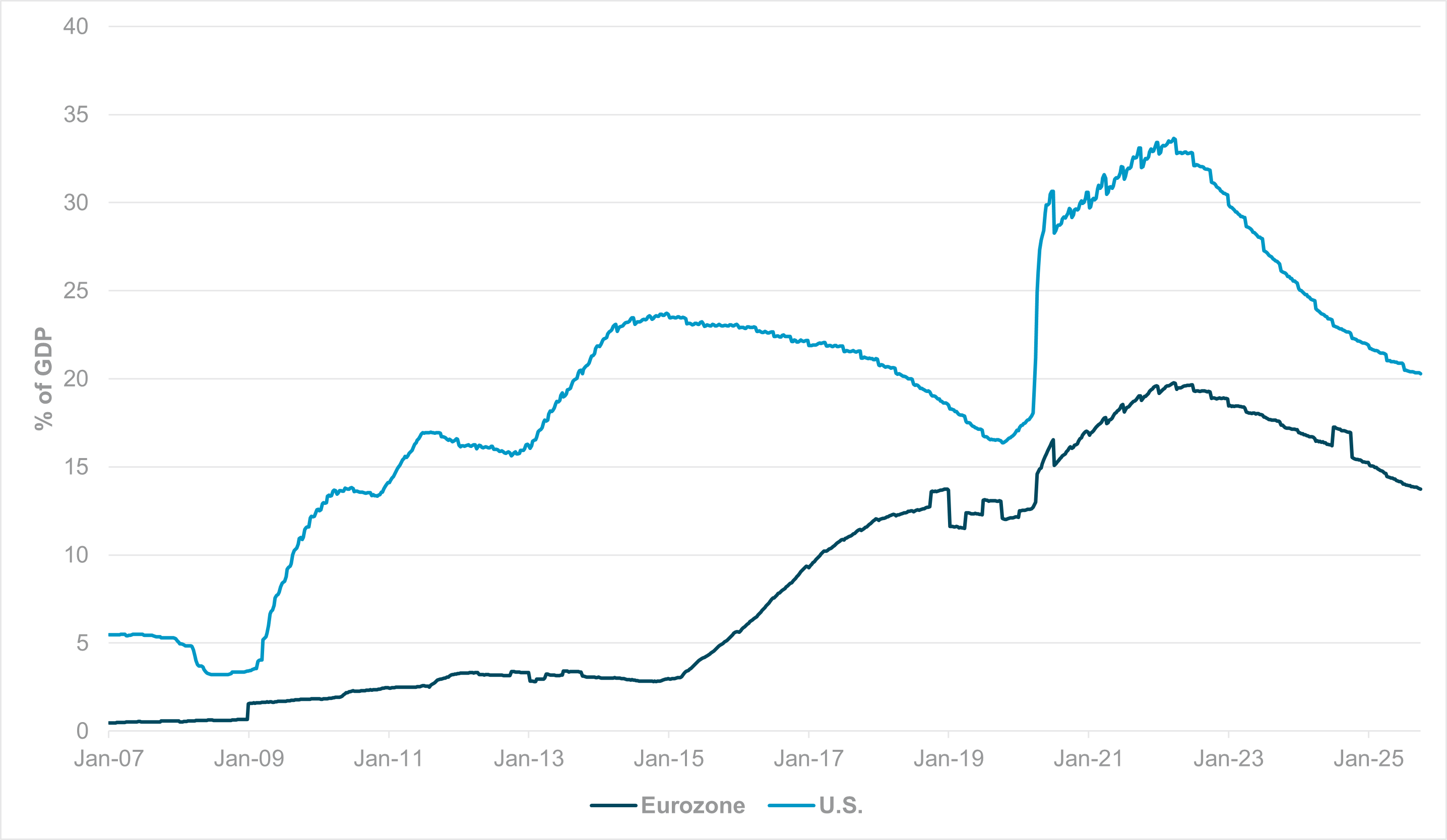

EXHIBIT #1: BALANCE SHEET SIZE TO GDP RATIOS, U.S. VS. EUROZONE

Source: BNY

Our take

In our Short Thoughts report this week, we highlighted that Fed Chair Powell’s recent comments supports our long-held belief that the Fed’s balance sheet shrinkage is due to end, possibly as soon as the upcoming FOMC meeting, or at their December gathering. Given the Fed’s lack of data inputs at present, erring on the side of caution across all financial conditions inputs is likely the safest course, and this includes quantitative measures because funding costs need to remain in an acceptable range. Among the world’s major economies, central banks have seen the value of pushing for more ample liquidity stock while managing the flow, but the ECB is the major exception. In contrast to the Fed, the upcoming ECB decision is not live and even the prospect of a December cut is only a tail risk for now. The divergence in rate paths between the ECB and its peers is already wide enough, but we believe liquidity differentials is one area where adjustments aren’t even under consideration by the Governing Council. The Eurozone’s central bank balance sheet-to-GDP ratio is now below 15%, and the gap looks set to widen again if the Fed ends QT soon (Exhibit #1). There are technical factors which make the ECB’s liquidity management differ from its peers but simply based on quantitative differentials the ECB’s current balance sheet remains small relative to the size of the economy. Assuming the Fed stops QT – and the pace of tightening is already slowing in the U.K. and Japan – global liquidity conditions will be another area where the ECB’s stance looks restrictive.

Forward Look

Major differences in debt issuance outstanding mean that the ECB’s debt portfolio is not consistent with GDP contributions to the Eurozone economy, and there are underlying political factors which continue to incentivize balance sheet roll-off. The ECB can, with some justification, point to low nominal rate levels helping anchor reserve borrowing costs, but we have in the past seen how credit stress can create major gaps in Eurozone funding conditions. Such concerns are now moving back to the fore of the global economy, which warrants a more cautious response. The current risk is that the ECB has the tightest financial conditions on the rate path, exchange rate and quantitative channel just as the world economy faces greater turbulence up ahead. Its remaining firepower could quickly be exhausted in the event of adverse scenarios.

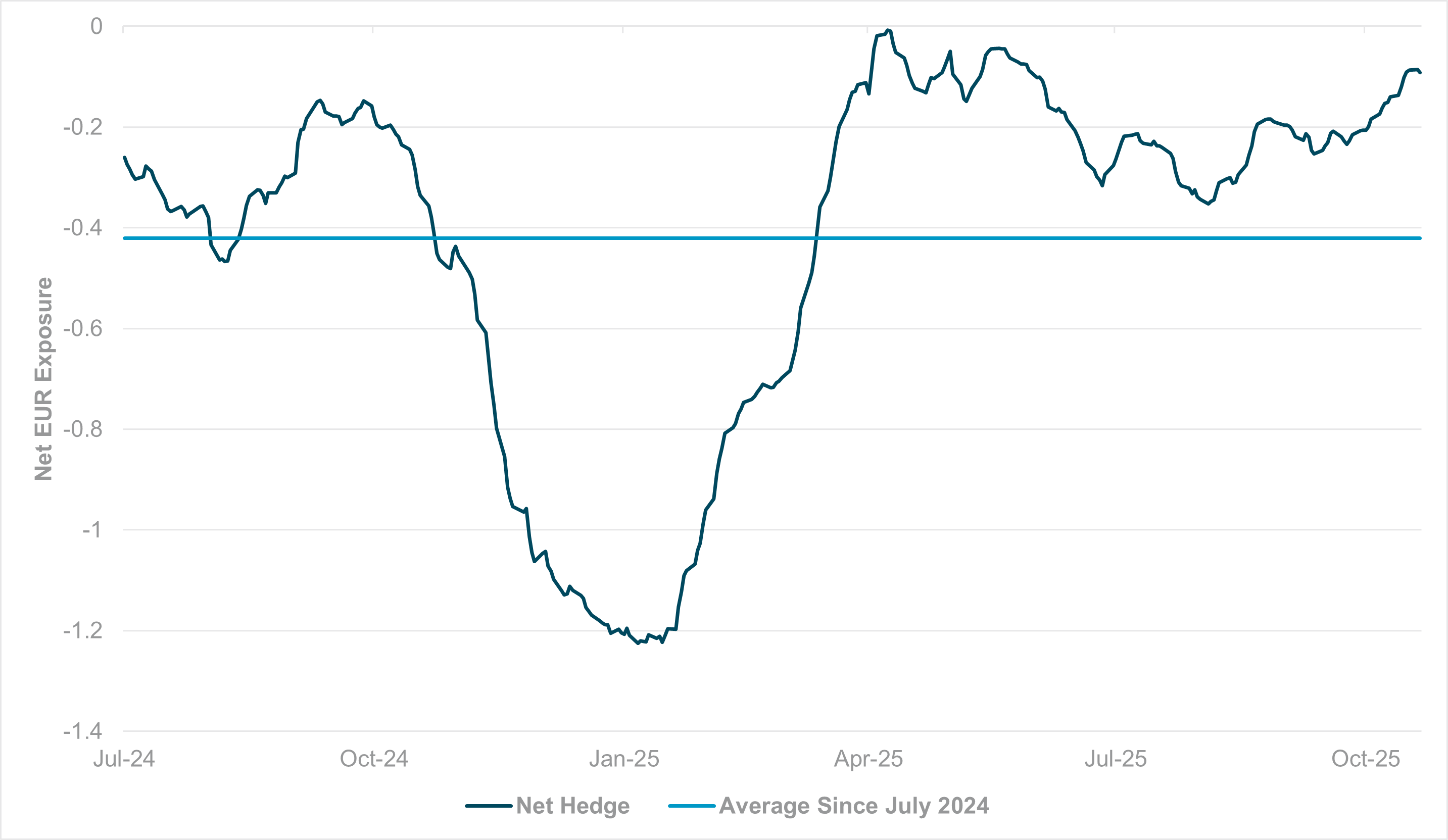

EXHIBIT #2: NET HEDGE IN EUR FOR CROSS-BORDER INVESTORS

Source: BNY

Our take

Even with a more favorable policy stance, cross-border investors have not shown any preference for a stronger EUR. Using our “net-hedge” indicator, where we aggregate cross-border EUR holdings against a weighted (30 to 70) basket of equity and fixed income holdings in the Eurozone, the current exposure is close to flat. In theory, this indicates that FX exposure is fully neutral, but unlike the dollar, “neutral” FX exposure is not the default position for the EUR, especially considering the developments in EUR holdings last year, during which the “excess” level of EUR underheld positions moved toward extreme levels for policy and political reasons. Throughout the summer, renewed stress over the French political situation has contributed to renewed deterioration but nowhere near the scale of last year (Exhibit #2).

Forward look

We doubt there will be much interest in pushing EUR holdings through these levels. The currency has historically been underheld on a structural basis due to lower equilibrium yields, which in turn reflects fundamentals such as weaker trend growth and policy expectations. Current pricing simply indicates that rates or general growth will not be as weak as expected, but we remain of the view that financial conditions are far too tight and only targeting a very specific aspect of the economy. If anything, current supply chain issues could impede productivity even further but at the cost of manufacturing output, and it would be negligent for the ECB to not react if inflation remains the narrow focus.

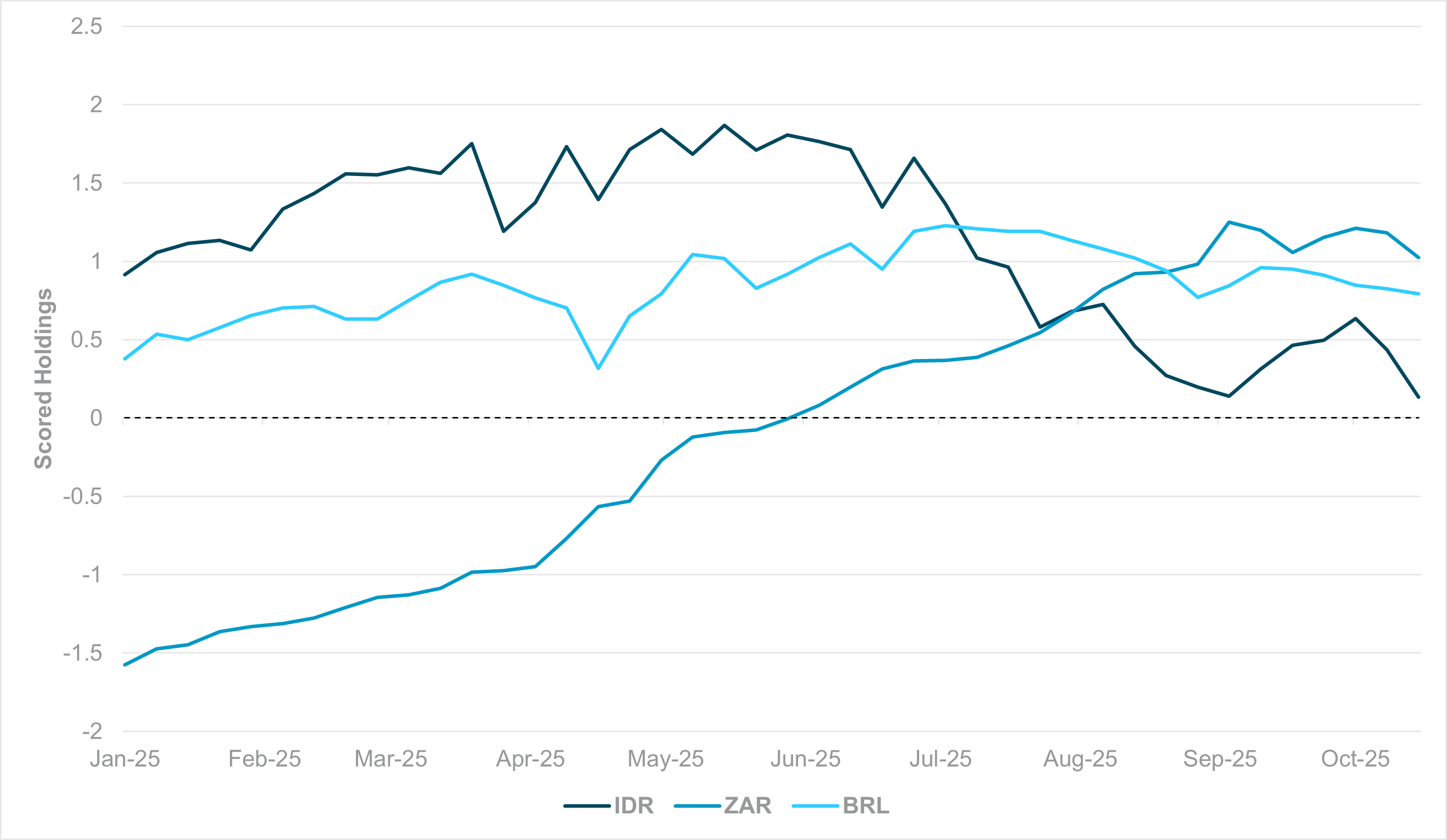

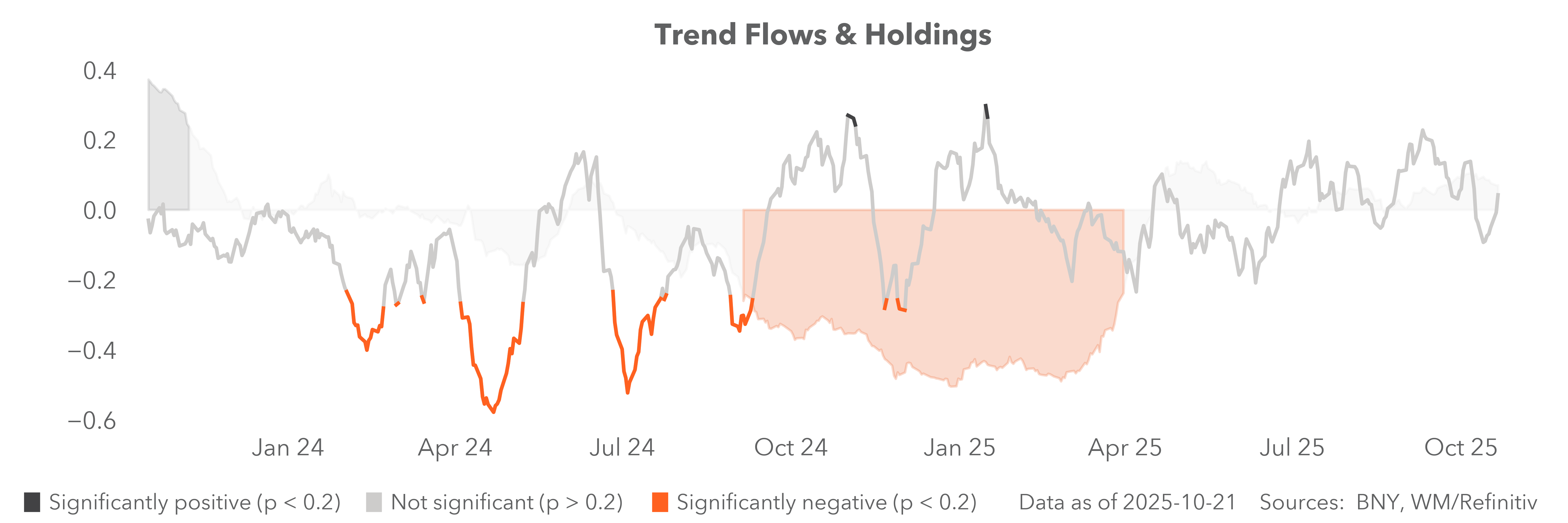

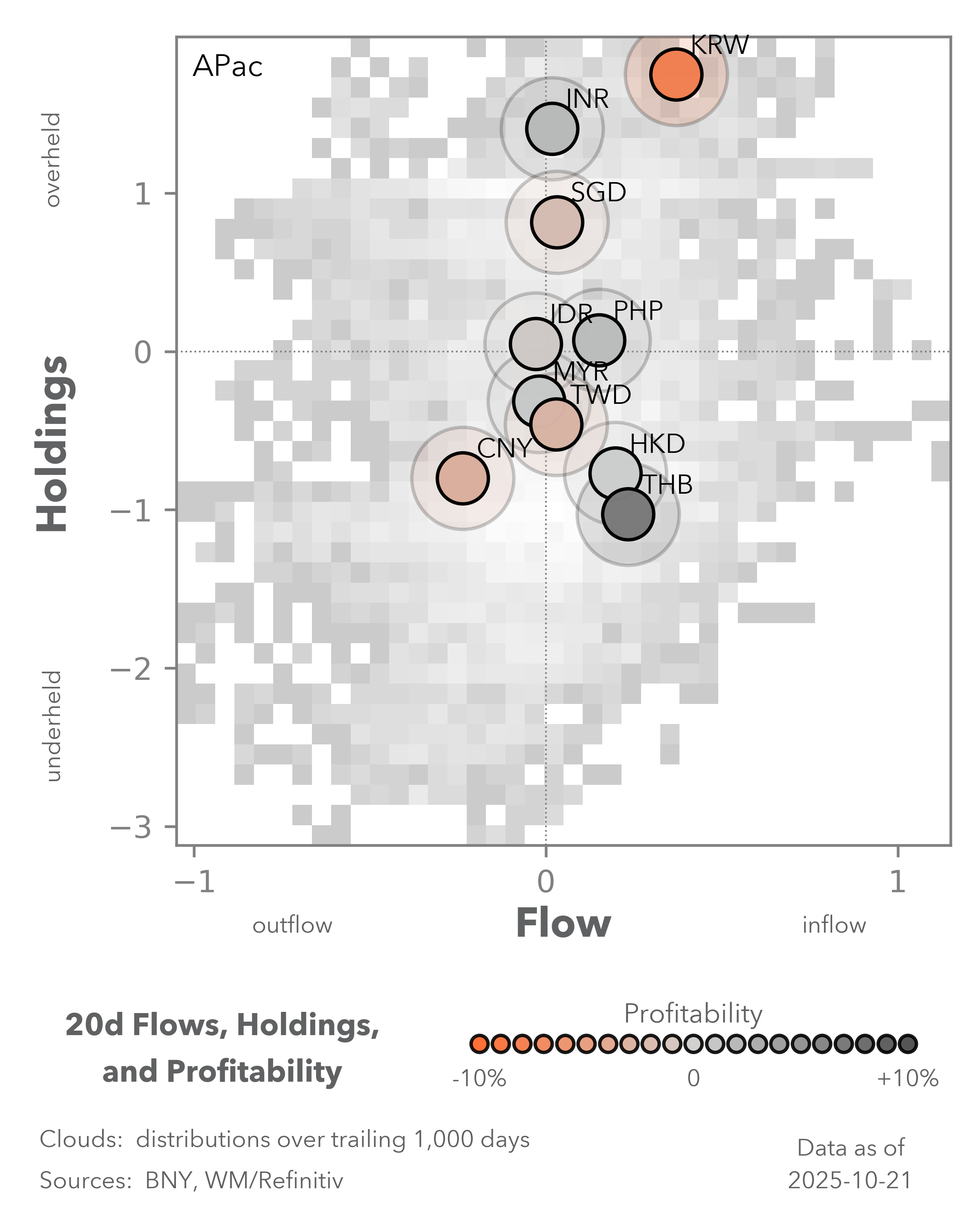

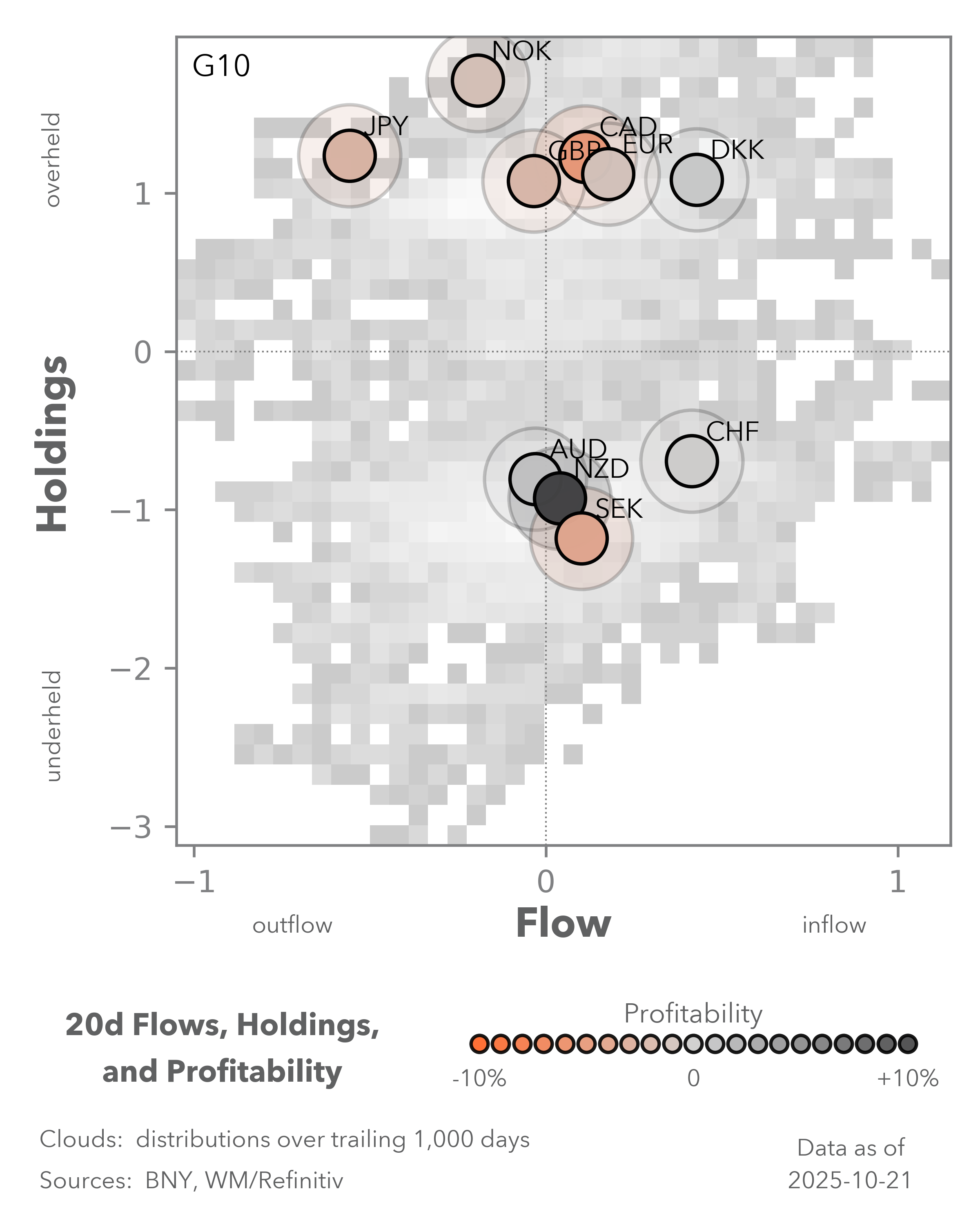

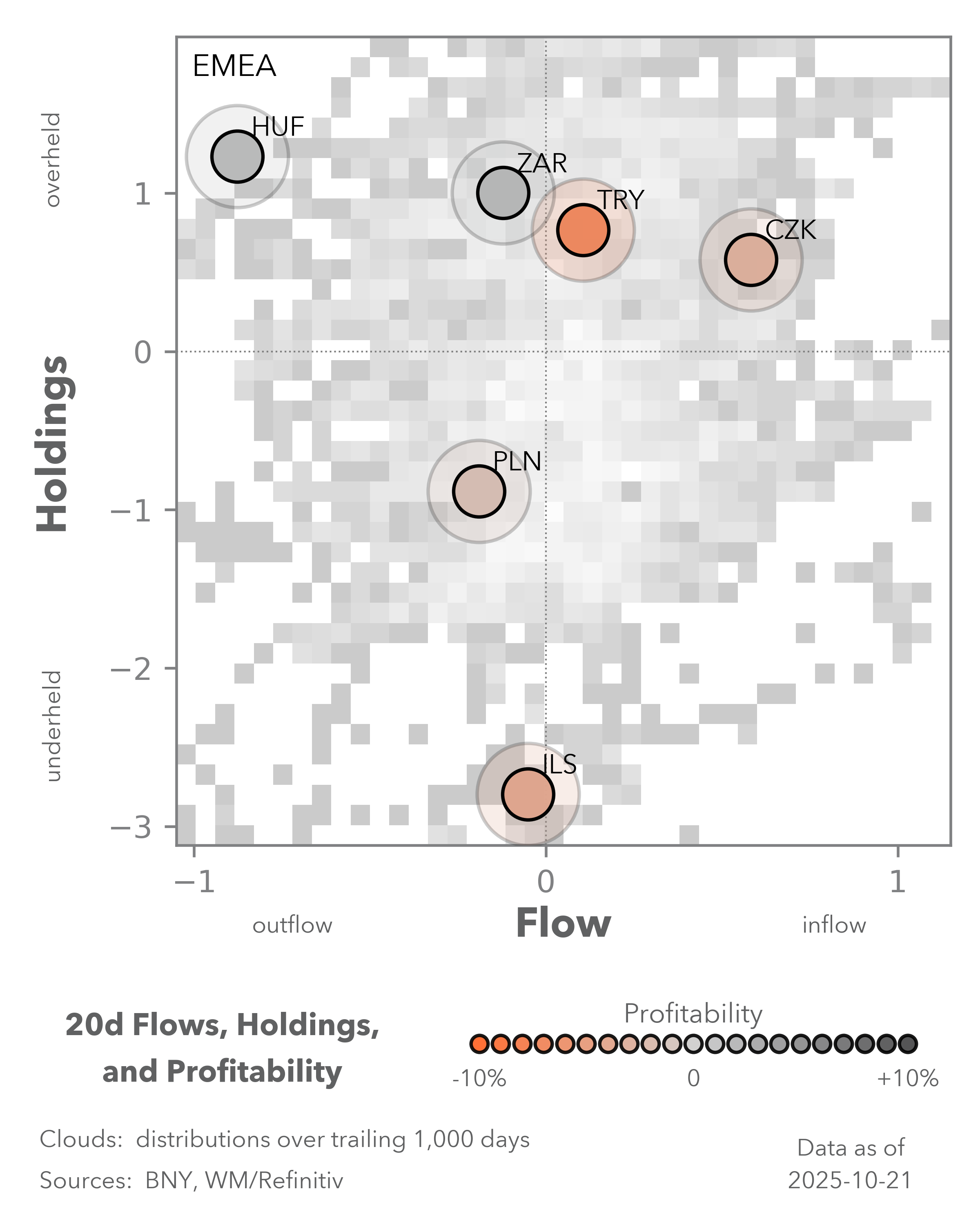

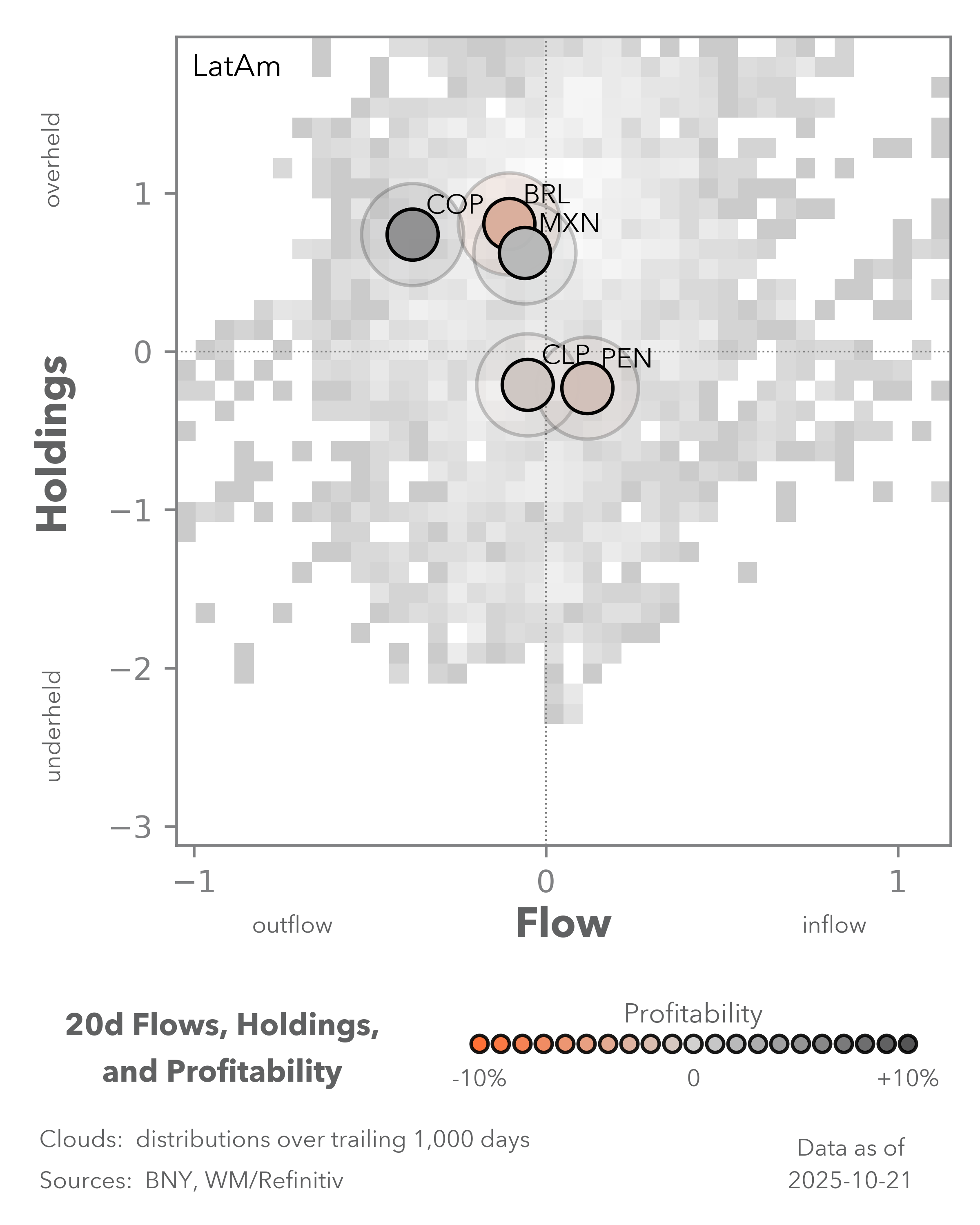

EXHIBIT #3: CORE COMMODITY CURRENCY HOLDINGS IN EM, BY REGION

Source: BNY

Our take

Outside of G10, we continue to monitor the carry unwind process and the prospect of iFlow Carry holdings also turning toward neutral. Like the difficulty in shifting low-yielding currencies to outright long (KRW has been the only large mover for cross-border investors), the high cost of carry also limits the prospect of a sharp reduction in high-yielder holdings. The surprise BI decision to hold yesterday underscores the fact that continuing to push for carry unwind is not a straightforward process, and BI’s intent to deliver currency stability has been clear. However, with the recent volatility arising in gold prices, there is a case to assess vulnerabilities in commodity-exposed currencies which remain overheld. In APAC, we still see IDR as the main commodity currency due to its nickel prowess, whereas ZAR and BRL are the key names in EMEA and Latin America. All three have been anchoring positive statistical significance in iFlow Carry holdings, but flow activity looks to be peaking (Exhibit #3).

Forward look

ZAR’s prior status as an underheld currency shows that it is possible for a high nominal- and real-yielding name to move into underheld, but idiosyncratic factors will likely play the most important role. All three currencies are facing such challenges up ahead, but central bank credibility is not in doubt and more assertive easing will only take place if there is a material downturn in growth. Consequently, hedging flow will remain a function of underlying asset exposures and this is where the commodity aspect comes through. Gold prices will directly affect the current outperformance in South African equities, while Indonesia and Brazil retain heavy bond exposures which will be exposed to any pick-up in global credit volatility. A comprehensive round of liquidation and hedging flow is not on the cards yet, but current holdings in EM commodity FX remain too high relative to risks. IDR is already approaching flat, and we see BRL and ZAR holdings as most vulnerable to the current environment.