Europe’s price path remains driven by services and wages

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

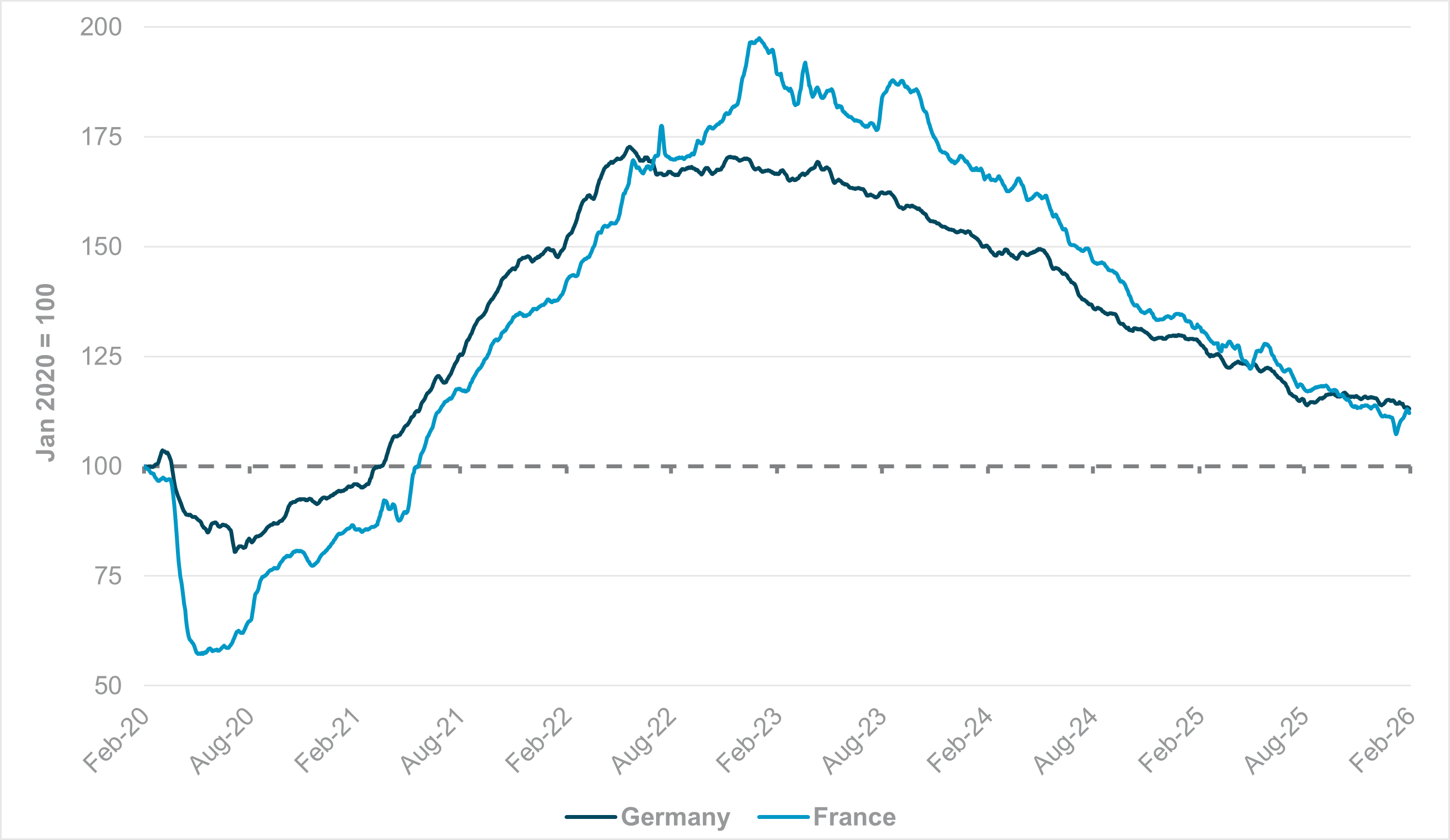

EXHIBIT #1: TOTAL JOB OPENINGS, GERMANY AND FRANCE

Source: European Central Bank, BNY

Our take

The downside surprises in French and Dutch January preliminary inflation prints will likely raise more questions for the European Central Bank (ECB) Governing Council regarding its policy assessment. On current evidence, monetary policy is no longer “in a good place,” nor are conditions weak enough to merit an additional pivot.

There are also clear distinctions between French and Dutch inflation, with the former falling dangerously close to no price growth. Dutch inflation may even welcome more significant declines, as prior levels overshot the ECB’s own inflation target.

Given the risk of periodic bouts of volatility in U.S. trade relations, some structural weakness in Eurozone growth expectations will likely persist. But this is already consistent with developments in the manufacturing sector, which continues to contract in terms of output and labor.

Wage and labor market expansion continues apace in services, as confirmed by the latest PMIs, and declines in the sector appear to have stabilized in both Germany and France (Exhibit #1).

Forward Look

Challenges for the export sector are already present in the policy assessment. Risks to the downside in prices arising from the exchange rate have increased – as flagged in recent commentary – but services demand is far less sensitive to exchange rates. One factor that does impact services, and where the ECB may have less visibility, is fiscal impulse. With the passage of the French budget, marginal contraction is expected, and there is still the risk of Germany’s spending plans disappointing expectations. Recent steepening in Eurozone yield curves – some in sympathy with the situation in Japan – may act as a constraint on government spending for the rest of the year.

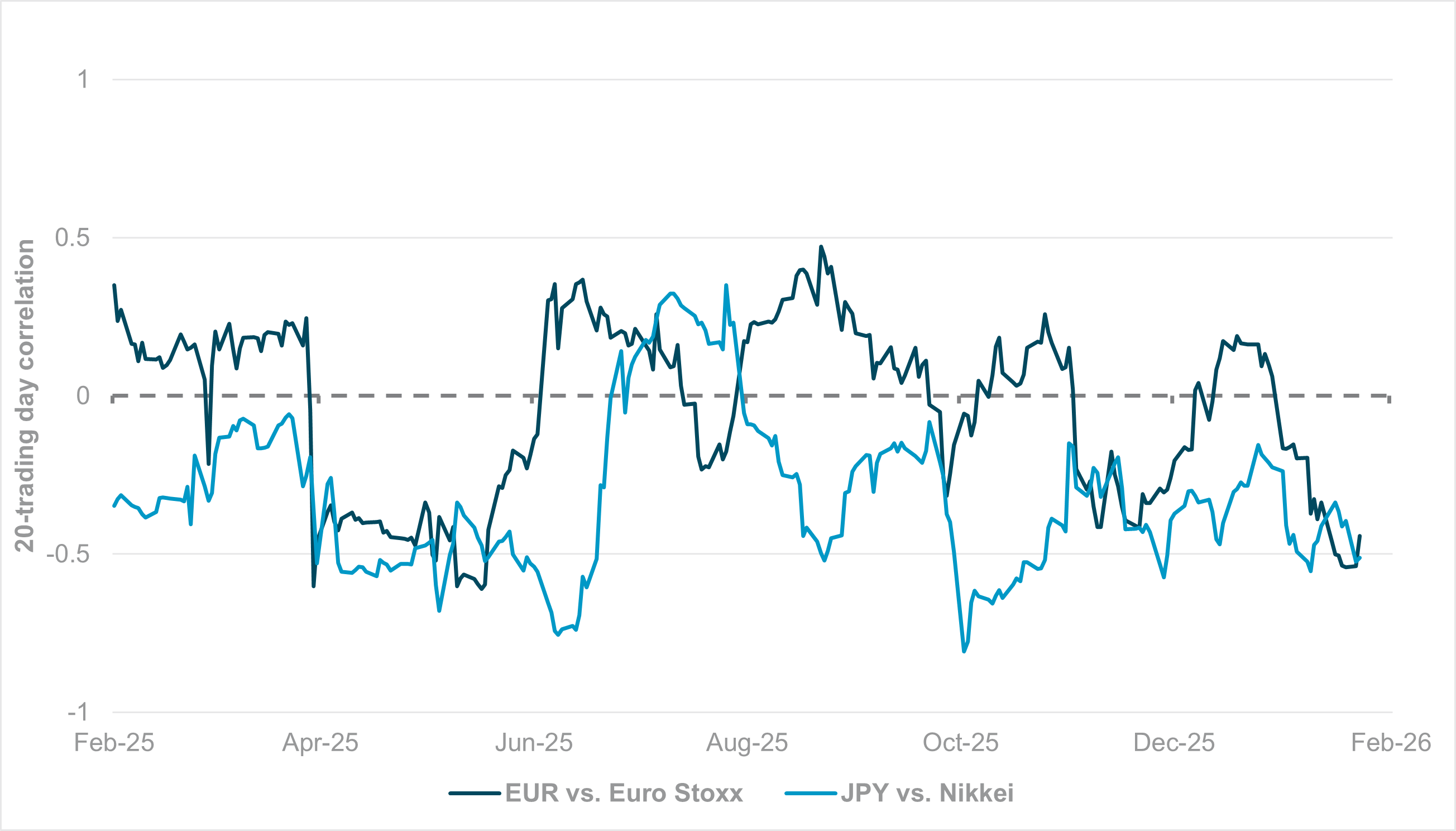

EXHIBIT #2: CORRELATION BETWEEN STOCK MARKETS AND LOCAL NOMINAL EFFECTIVE EXCHANGE RATES (NEER)

Source: Swiss National Bank, BNY

Our take

In addition to the ECB’s Governing Council, policymakers in Sweden have started to signal that additional cuts may be needed despite guidance that terminal rates have been reached for now. The Riksbank’s shift in tone on the SEK – from undervaluation to disinflation driver – is likely to be repeated across all export-based economies.

The disinflationary impact of Chinese exports is already a concern for competitiveness, while other competitors in highly value-added goods across the Asia Pacific region also have currency valuation advantages.

While near-term challenges with the U.S. over Greenland have been averted, tariffs have been imposed, and this represents forced real effective exchange rate (REER) appreciation on the exporter. All of this points to increased earnings translation risk for European corporates, which could ultimately translate into labor market challenges beyond what is currently reflected in survey data.

If export-based job losses reaccelerate, the demand impact could start to affect the services sector as well, even with stable fiscal impulse.

Forward look

Due to high levels of overseas sales, equity markets in exporting nations traditionally have a strong negative sensitivity to the exchange rate, though this can vary.

For example, the Nikkei’s correlation to JPY NEER is rarely positive, but Euro Stoxx 50 performance can sometimes withstand EUR NEER strength, particularly if domestic demand in the Eurozone holds up better than in Japan. More recently, however, the correlation between Euro Stoxx 50 returns and the EUR has fallen to its most negative level since Q2 last year (Exhibit #2).

A stronger currency on its own is manageable, and policymakers will lean on corporates to react through hedging and cost adjustments. However, combined with volatility in equity markets, a steeper yield curve and geopolitical uncertainty, the tightening in financial conditions is material and requires additional vigilance. Peers in Switzerland and Sweden will likely need to make similar adjustments.

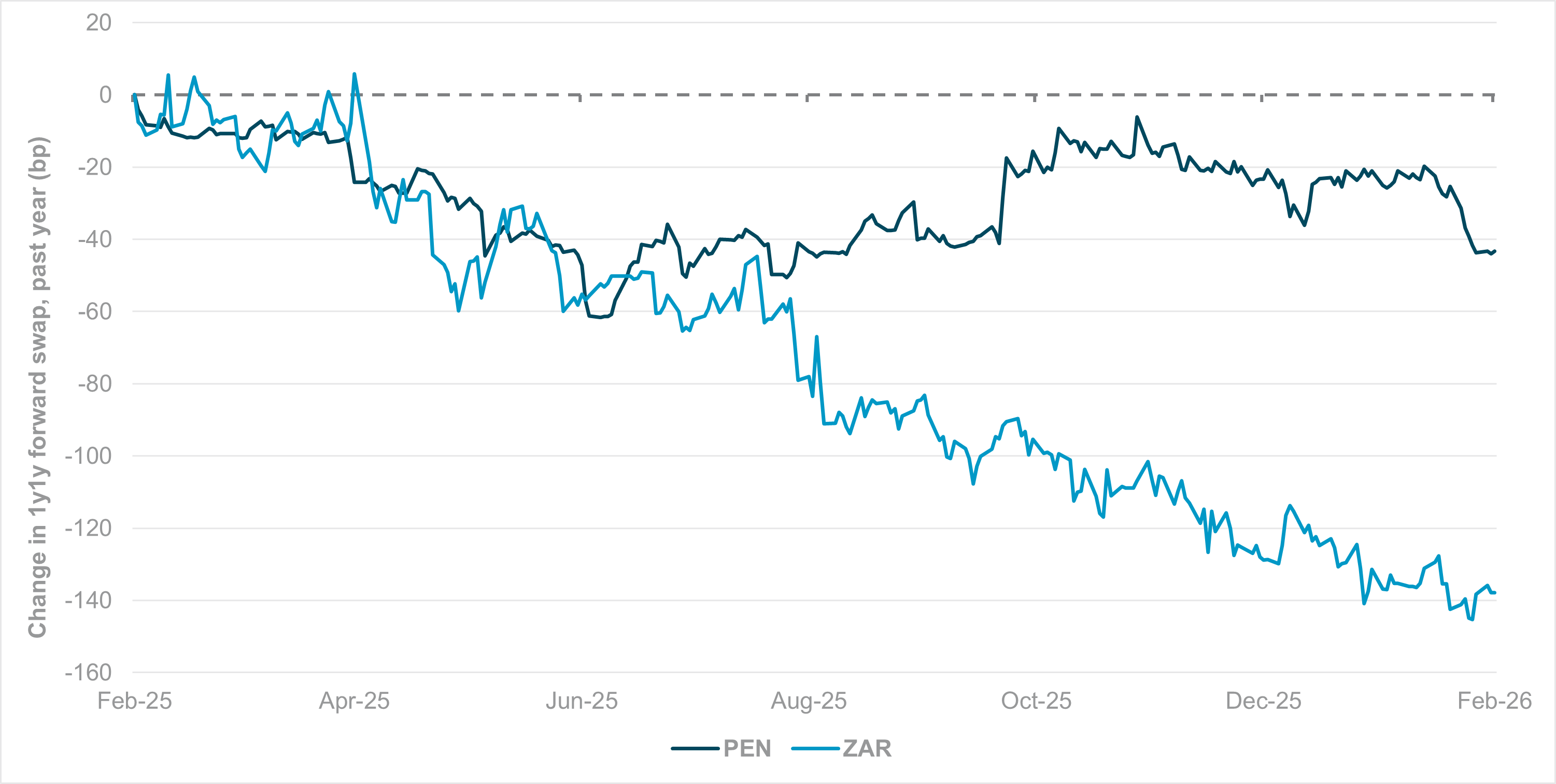

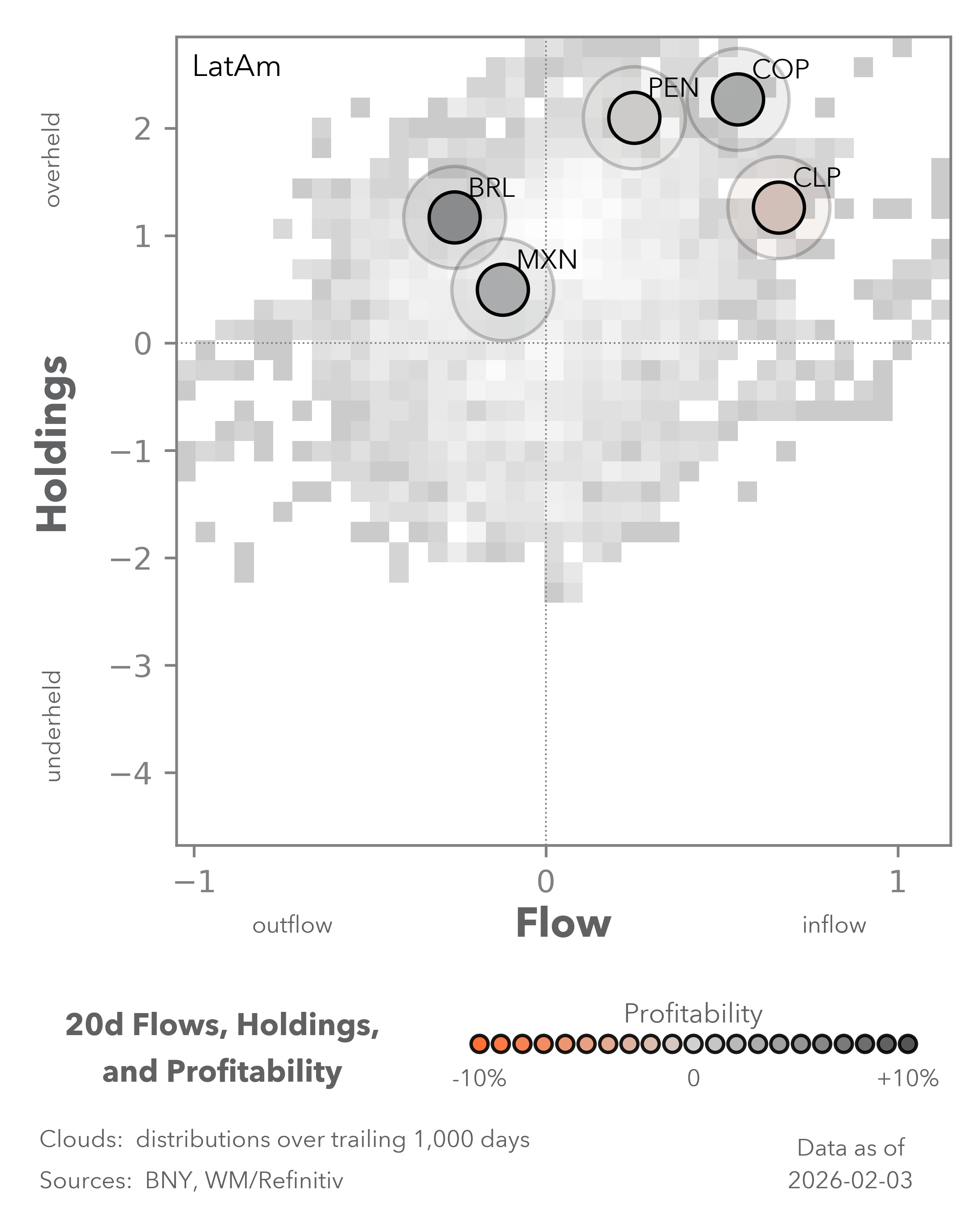

EXHIBIT #3: DIVERGENT PATHS FOR PEN AND ZAR DESPITE TERMS-OF-TRADE BOOST

Source: BIS, BNY

Our take

Central banks and governments in metals-producing countries will be relieved that the extreme price action seen last Friday and early Monday was not more disruptive.

While prices have not recovered to pre-volatility highs, associated assets such as currencies and equity indices have stabilized. With the bulk of the price gains (in dollar terms) over the past 12 months still intact, these economies can look forward to more sustained terms-of-trade improvement, improved government revenue and some associated disinflation risk.

However, we would be cautious about expecting structural changes in underlying economies from the rally in metals pricing.

First, the world is not entering a new commodity super-cycle, and one of the core drivers of metals prices – fears of fiat currency debasement – has very little to do with physical demand. Second, and perhaps more importantly, any commodity windfall is not sufficient to generate a structural re-rating of the economy.

Forward look

Throughout history, far too many emerging and even developed markets have succumbed to “Dutch Disease,” as overinvestment in the resource sector, profligate fiscal spending and currency overvaluation generate prolonged stagflation.

The initial currency and royalties windfall represent a loosening in financial conditions, which should make structural reforms far less painful. For example, energy subsidies are commonplace across emerging markets and lower fuel import costs can help reduce fiscal burdens. Importing capital goods for public investment and infrastructure should also be cheaper.

In reality, such measures are rarely adopted, and structural reforms only take place when the situation approaches crisis levels and entails a political cost.

South Africa began changes after the formation of the Government of National Unity (GNU) in 2024, and the market has been rewarding local assets ever since. These efforts culminated in the lowering of the inflation target, which accelerated inflows. 1y1y forward rates have fallen by 140bp year to date in a sign of confidence. By all accounts, the metals rally, which helped boost terms of trade, was a bonus that helped strengthen momentum in reforms.

In contrast, the market does not appear as optimistic about Peru (Exhibit #3), which is currently benefiting from the surge in silver prices. Admittedly, the economy is smaller and the starting point for policy rates and inflation is lower, but there appears to be a high degree of skepticism about the windfall’s ability to be transformative, at least until confidence in political stability improves.