Emerging market FX narratives diverge

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

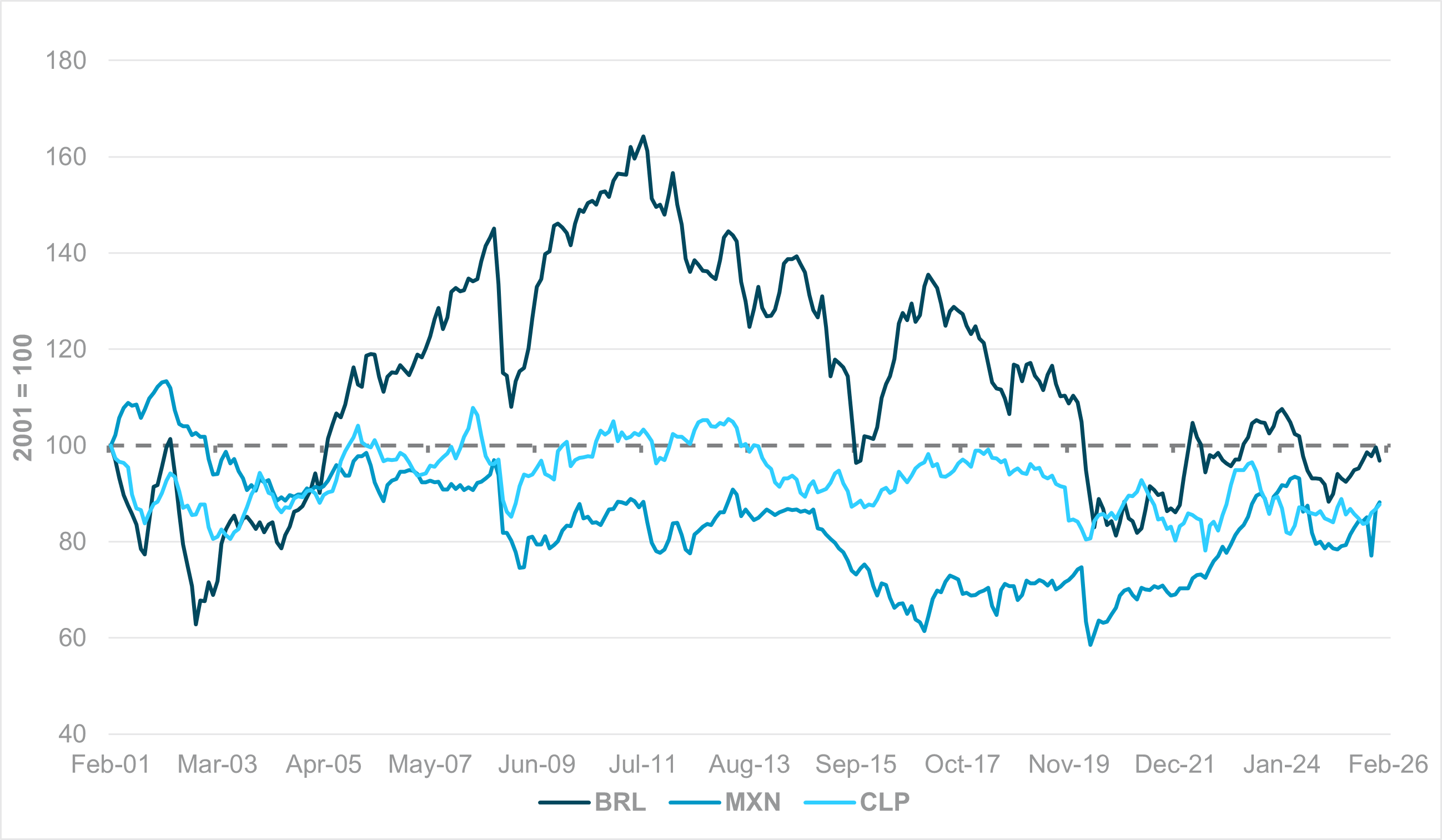

EXHIBIT #1: BIS REER INDICES: BRL, MXN AND CLP

Source: Bank for International Settlements (BIS), BNY

Our take

Latin American (LatAm) currencies continue to drive flow and holdings in carry trade themes. The region is now significantly outperforming the rest of emerging markets in both FX and fixed income, which is likely to raise valuation concerns. In the near term, we acknowledge that any pricing adjustment in metals will impact terms of trade. News this week of a very large output cut at the largest nickel mine in Indonesia, the world’s dominant producer, underscores the price risk facing mining- and commodity-based economies: underlying industrial and consumption demand is simply not there.

However, even taking into account short-term valuations risks, we stress that core LatAm currencies are not excessively valued. Based on the BIS real effective exchange rate (REER) indices, as of January 2026, BRL, MXN and CLP remain below their levels at the beginning of the century – crucially, before China’s accession to the World Trade Organization and the subsequent rotation in trade exposure away from the U.S. and toward China.

Forward Look

If commodity terms of trade are the only benchmark, then LatAm will not revisit the highs seen during the commodity supercycle. Downside risk from U.S. trade tensions could also impact productivity and trend growth, both of which are essential to long-term currency valuations. On the other hand, we note that this is also a good opportunity for LatAm to continue diversifying its growth exposures, as concentrated risk to one large economy or one particular export group will tend to generate highly cyclical growth.

LatAm has attained unique credibility in an era of fiscal dominance, which helped lift positioning in their currencies and fixed income well before the recent run in commodity prices. Given the favorable demographics and a low productivity base, there is significant upside for REER, especially through the nominal channel if inflation remains well-anchored by central bank rates. Short-term asset holding extremes point to the need for a significant correction, but this should not detract from a far more positive long-term valuation framework.

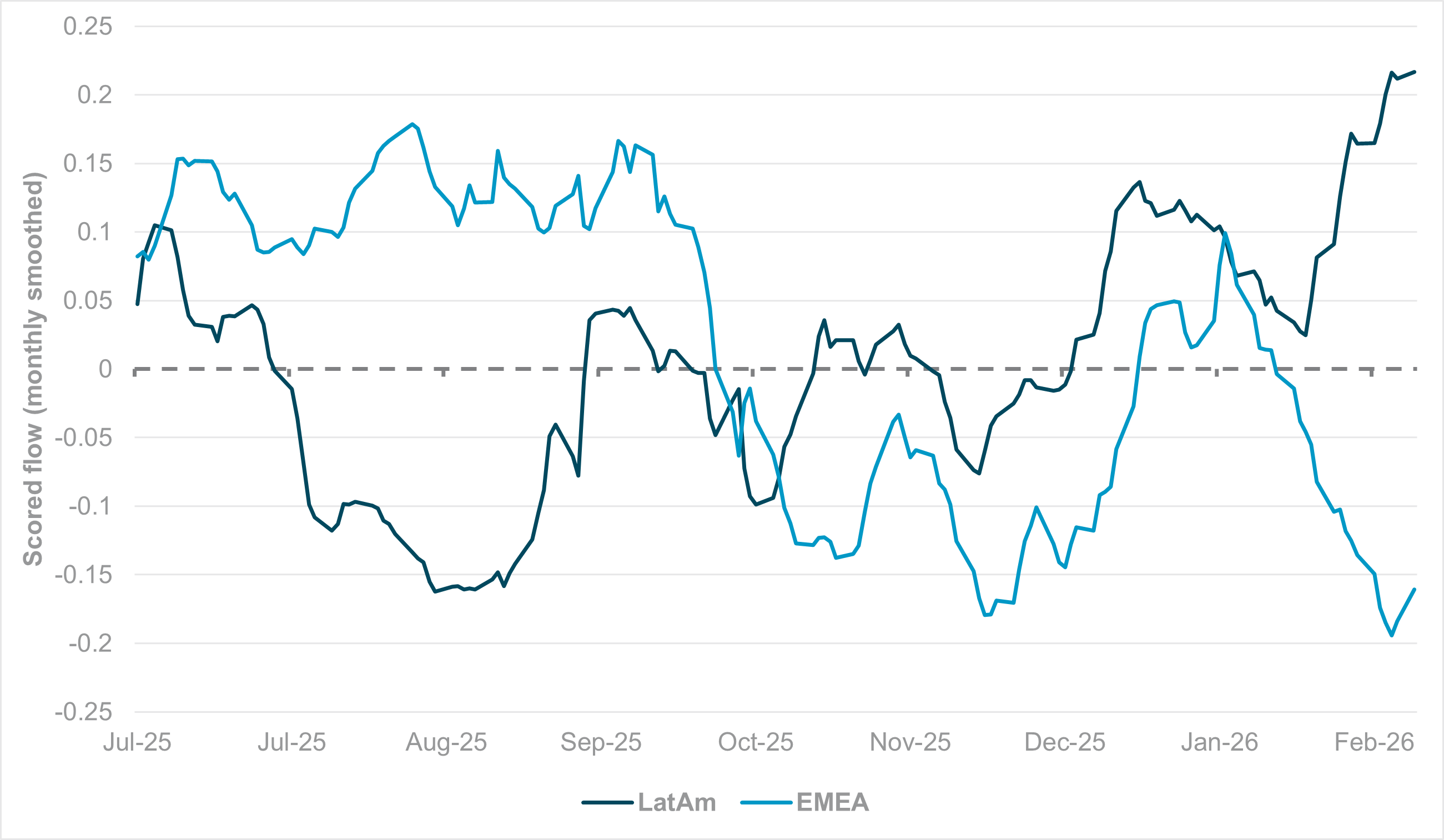

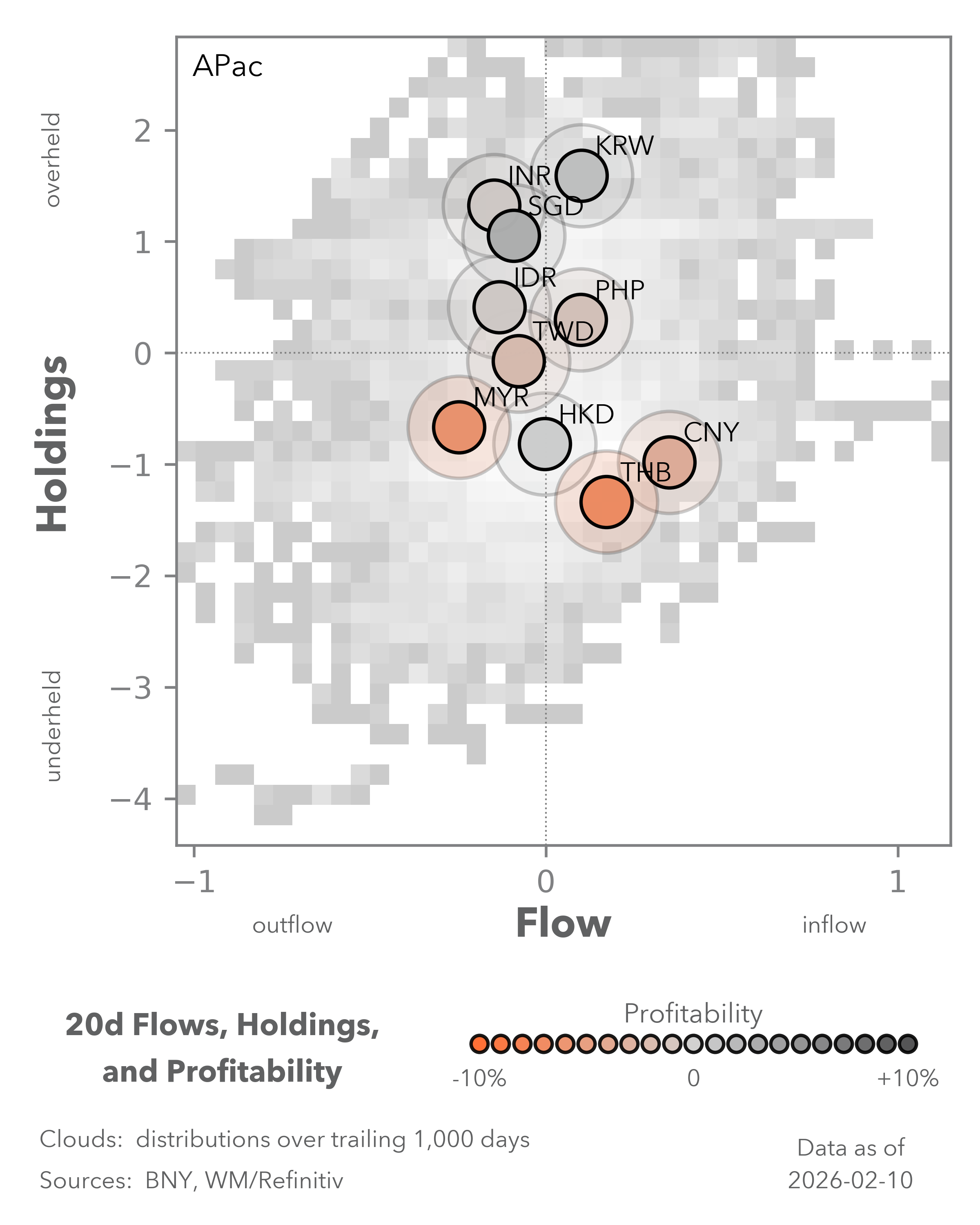

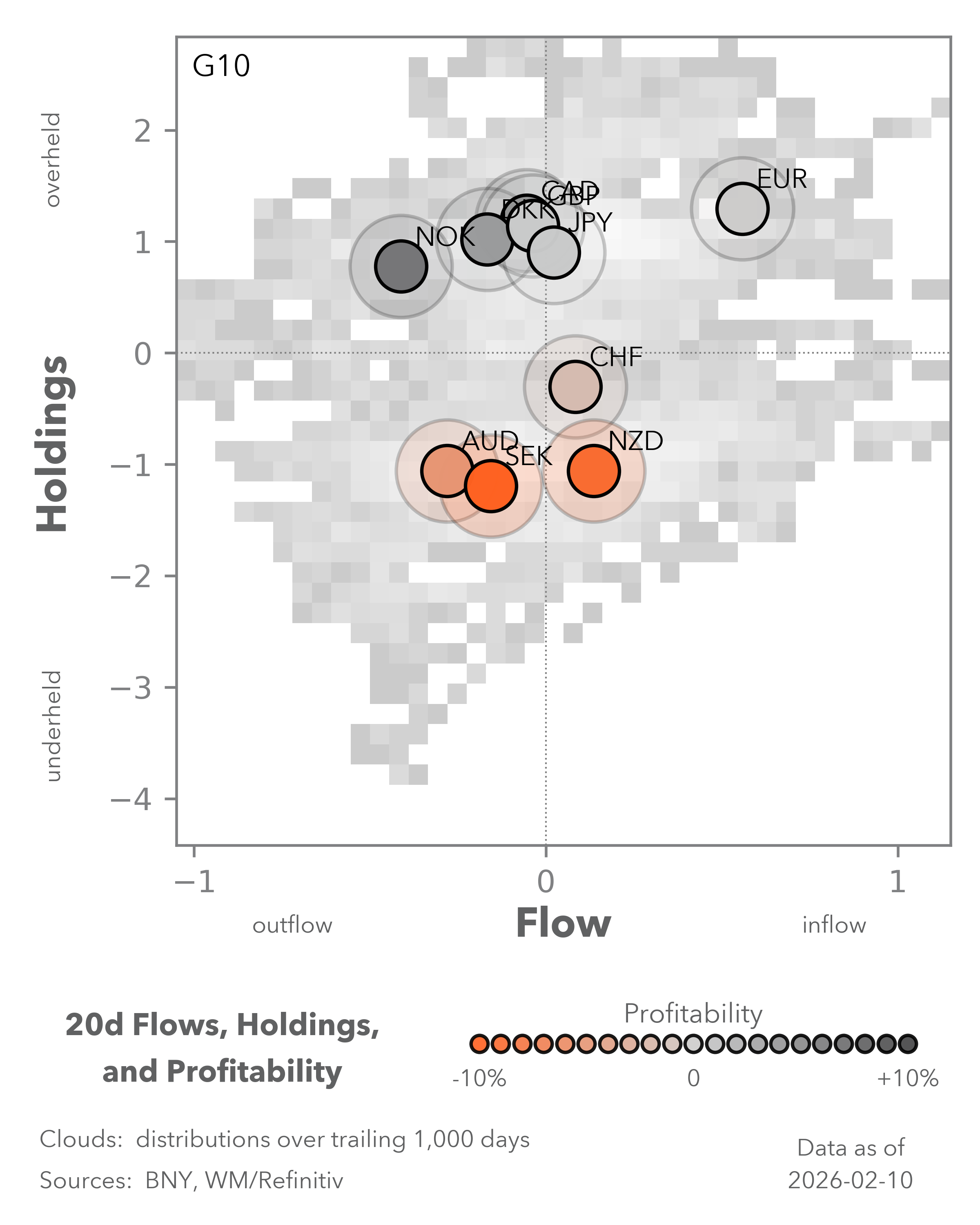

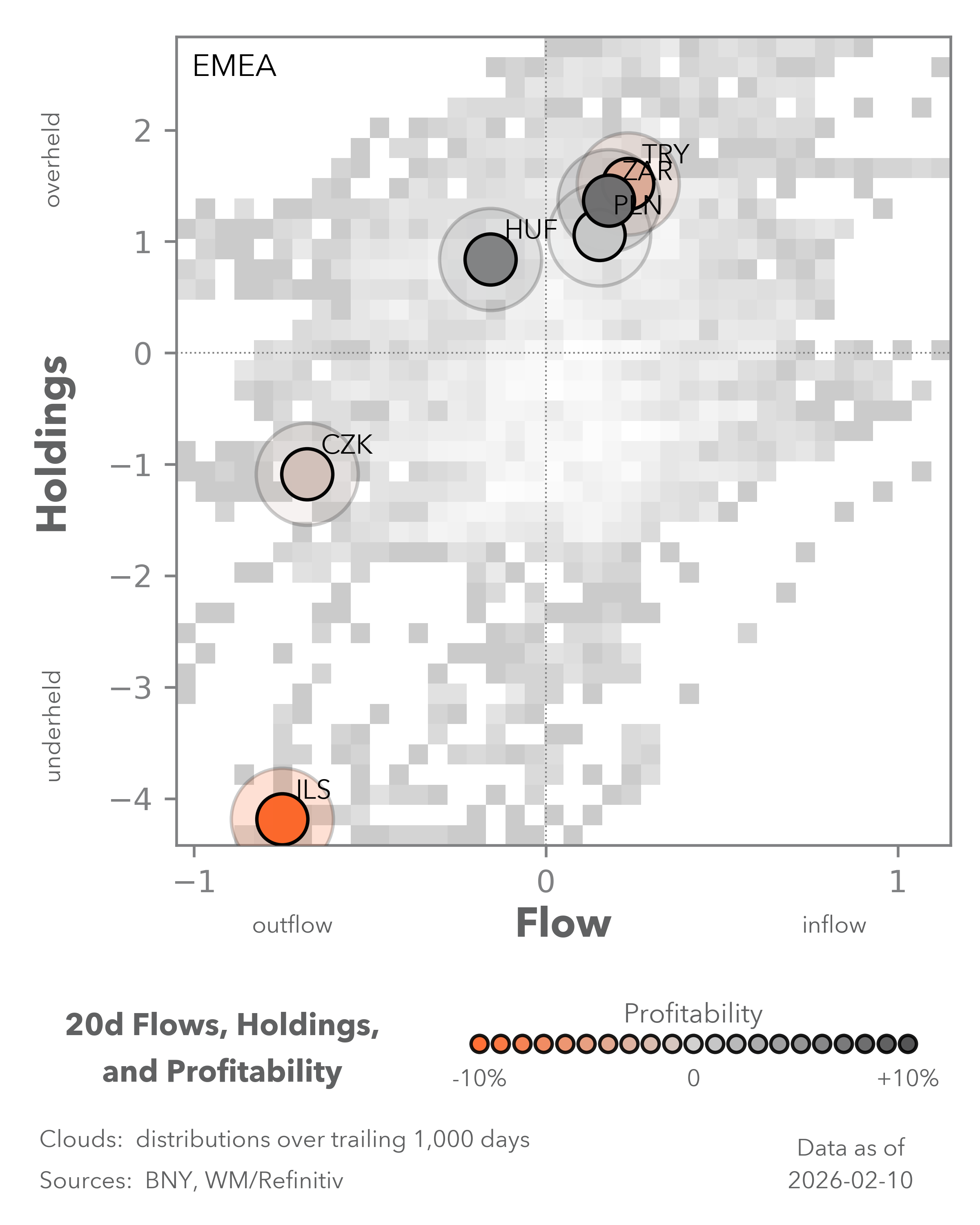

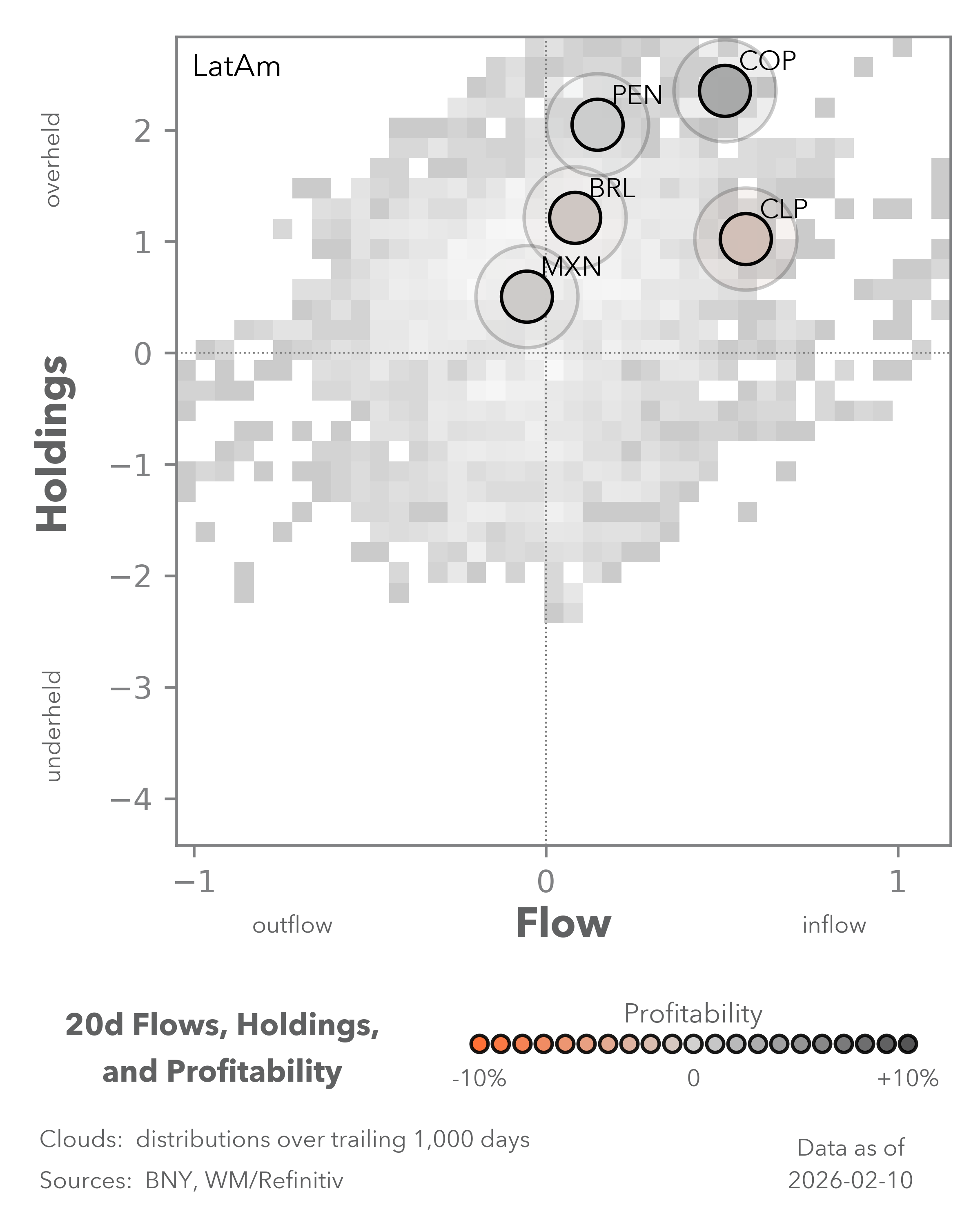

EXHIBIT #2: SMOOTHED MONTHLY FLOWS, LATAM VS. EMEA FX AGGREGATES

Source: BNY

Our take

Our iFlow Carry index shows that high-yielding currencies are slowly seeing reductions in holdings, but we stress that there are major differences developing in the underlying drivers. On the one hand, low-yielding APAC currencies and even the EUR are driving the reversal, but on the carry-reduction side, the pressure is almost exclusively on currencies in Central and Eastern Europe (CEE) and Africa, even though these two clusters still have relatively strong holdings.

LatAm currencies are now enjoying their strongest flow surge in six months and are significantly better held compared to other emerging markets currencies. In contrast, the EMEA region is now facing its strongest period of selling over the past six months, and CEE is looking particularly exposed.

Forward look

As FX valuations and holdings levels hit extremes, the bar is relatively low for profit-taking. We have been highlighting for some time that fiscal dominance risk is very high in CEE, and markets are now starting to pay closer attention to political developments. Significant policy pivots have taken place in both developed and emerging market economies with respect to inflation risk. But if there are institutional factors behind the inability of CEE central banks to do the same, then the divergence is understandable, especially compared with LatAm (e.g., Colombia has resumed its tightening cycle, and COP is the strongest-performing currency in iFlow over the past month).

The bottom line is that the market needs to trim its FX carry holdings while volatility conditions allow, recognizing that flows in CEE represent the path of least resistance.

EXHIBIT #3: DECEMBER-2026 FUTURES RATES, NEW ZEALAND AND AUSTRALIA

Source: BIS, BNY

Our take

The Reserve Bank of Australia (RBA) rate hike last week has rekindled expectations for divergence within the G10, particularly between commodity-linked central banks and the rest. With Norwegian inflation registering a sharp upside surprise, Norges Bank easing – which remains in its guidance – is being steadily priced out. For the Bank of Canada, interest rate futures point to a greater probability of higher policy rates by year end.

For now, the Reserve Bank of New Zealand (RBNZ) is expected to be the next mover, with full hikes priced in for the second half of the year. However, FX markets should be careful in viewing NZD as an ersatz AUD and anticipate stronger valuations. Although the December 2026 futures contract is anticipating 3% rates, the trajectory versus Australia is very different: pricing for end-2026 remains well below levels seen last year and has barely moved since December (Exhibit #3). The trajectory for New Zealand interest rate futures suggests that markets had to revise their growth expectations for New Zealand materially lower last year and remain cautious on the medium-term outlook.

Forward look

RBA Deputy Governor Andrew Hauser’s comments this week highlighted the factors that have impacted the bank’s policy outlook, but crucially the data has justified such a step. New Zealand inflation is also quite elevated, which supports the pivot toward tightening. However, through the latter end of the forecast horizon, New Zealand’s inflation path is expected to converge back to target sooner, and there are questions over steady-state levels for growth and price levels. Hauser’s comments that Australia is being “more inflation prone,” citing comparisons to New Zealand, have merit.

Some light fiscal tightening and weaker external demand have opened up a large output gap in New Zealand, requiring a stronger monetary offset. On a forward-looking basis, as its economy is smaller and prone to greater volatility in output gaps, pre-emptive and aggressive tightening may not be the optimal approach. From liquidity to volatility-adjusted returns, NZD is unlikely to see a valuation lift equivalent to the AUD.