Early look at 2026 carry candidates

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

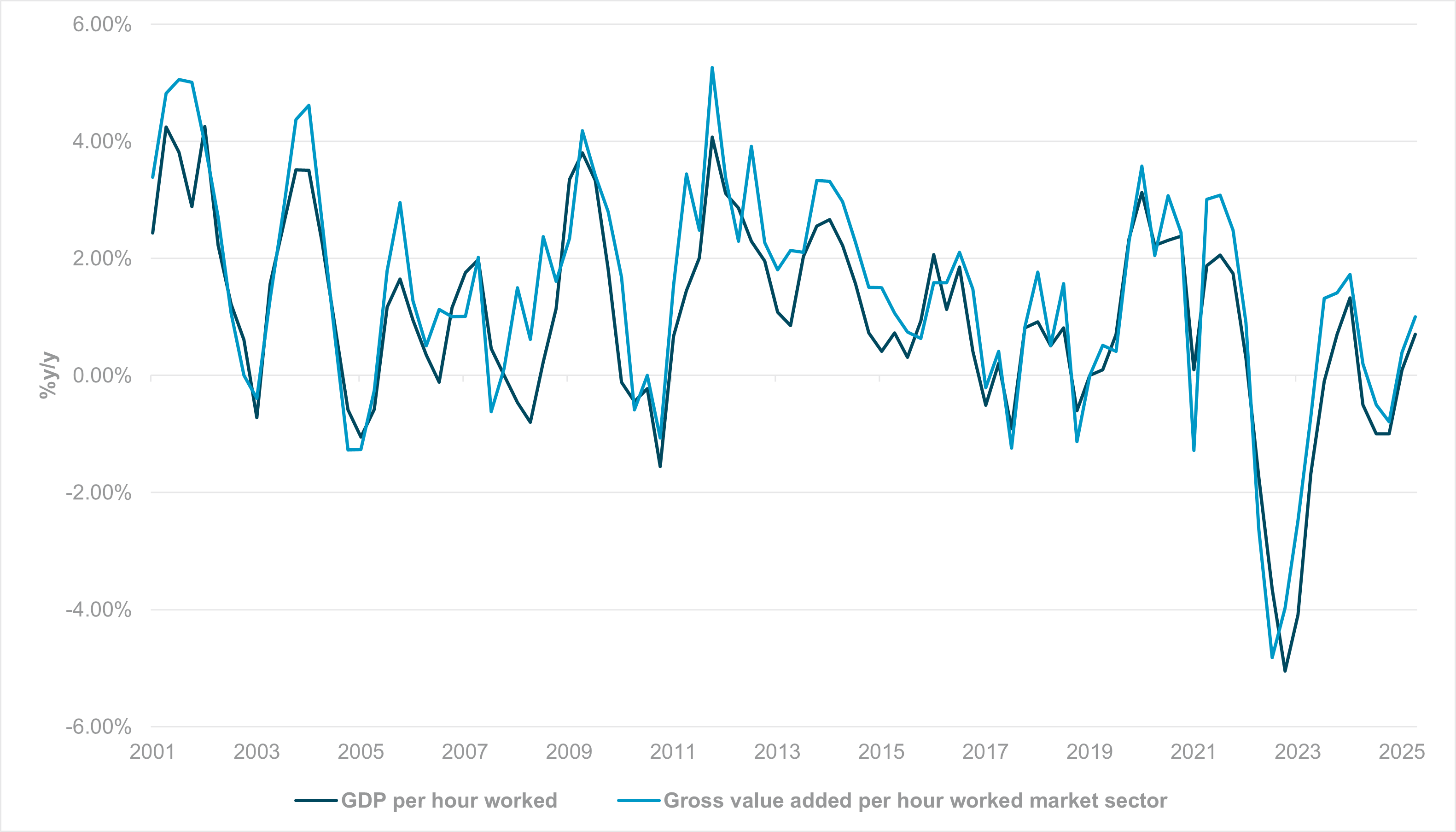

EXHIBIT #1: GDP AND GVA PER WORKER GROWTH (SEASONALLY ADJUSTED), 2001 TO PRESENT

Source: BNY

Our take

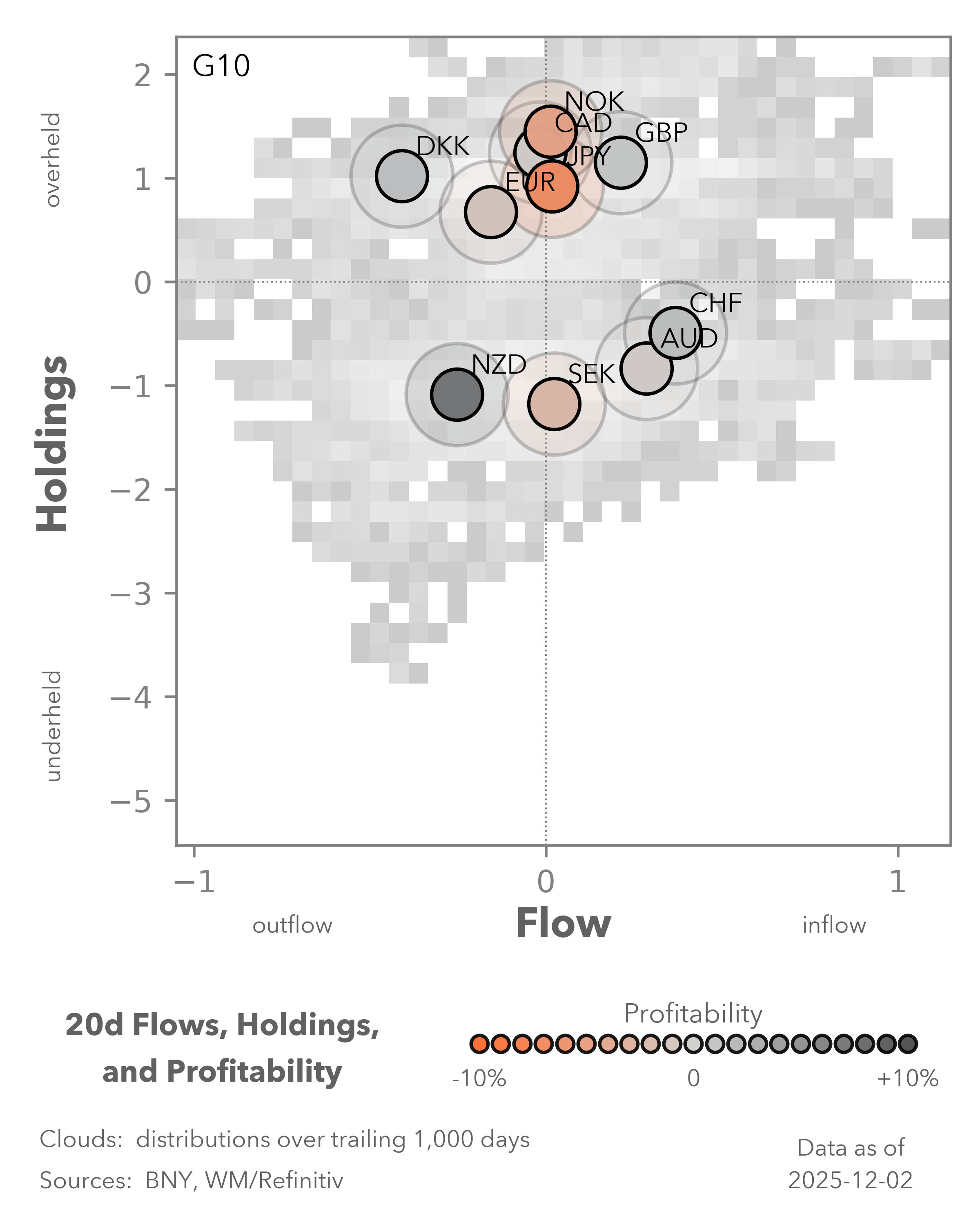

Based on current pricing, the Reserve Bank of Australia (RBA) is currently one of the top G10 candidates (other than the Bank of Japan, which has always been in a different cycle) to start an easing cycle early next year. We support this view, and the RBA’s decision next week could lay the groundwork for fresh guidance in a tightening direction. Whether this translates into a stronger Australian dollar (AUD) is a different proposition.

We continue to see the currency performing well on a variety of factors, both internal and external, while positioning is also favorable based on iFlow’s current reading. However, before initiating fresh AUD long positions against the USD or on a relative value basis, we believe there remains a risk of disappointment in the nominal exchange rate. In real terms, AUD strength is already evident through wage growth and inflation differentials.

However, it has proven difficult to shift the adjustment burden onto the nominal exchange rate, mostly due to weak productivity growth. In absolute terms, Australian productivity has all but stalled over the past five years. The stagflationary implications have been difficult to manage, with the AUD weakening as domestic savings are recycled overseas in search of stronger real returns.

Forward Look

When productivity is strong enough to drive real income growth, rather than relying on nominal gains, the real effective exchange rate (REER) can begin to rise and serve as the main tightening channel, rather than interest rates. Recently, RBA Deputy Governor Andrew Hauser warned that the Australian economy may be “boxed in” by low productivity. This is bound to have an impact on external flows.

Rate hikes in such an environment are merely in place to ensure real rates are sufficient to avoid overheating in an economy with very limited spare capacity. We believe the country’s rare earths prowess and ability to realize strategic autonomy represent a new and discrete source of potential investment growth from multiple external channels. However, domestic policy shifts are needed to take full advantage of such flow demand and generate sufficient productivity growth, to ensure the country’s non-inflationary growth rate can move above, in Hauser’s words, “far from spectacular performance by historical standards.”

Without such changes, the AUD’s performance may well remain “far from spectacular.”

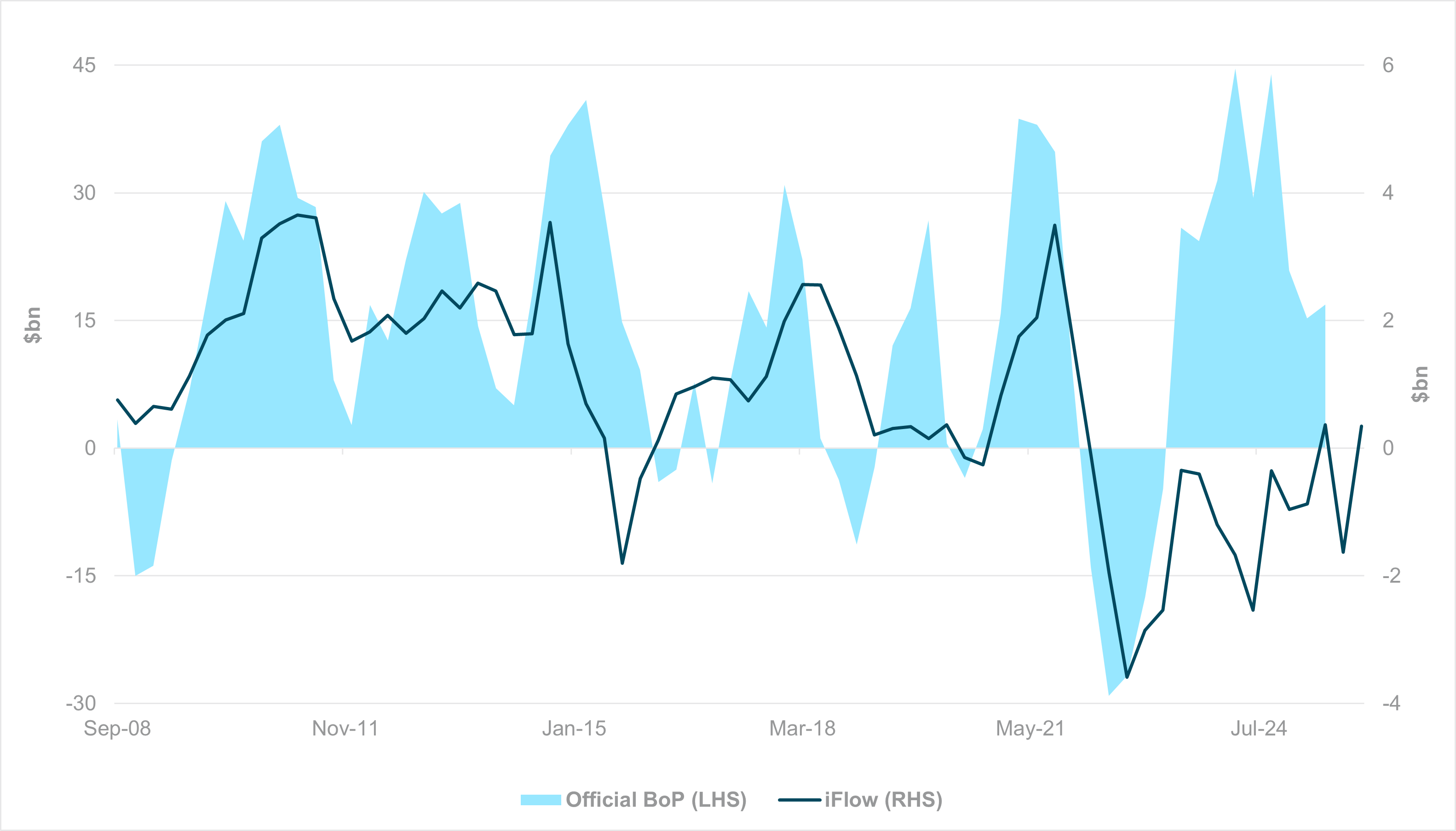

EXHIBIT #2: INDIA ROLLING FOUR-QUARTER INCURRENCE OF EXTERNAL PORTFOLIO LIABILITIES, OFFICIAL DATA AND IFLOW

Source: BNY, Bloomberg

Our take

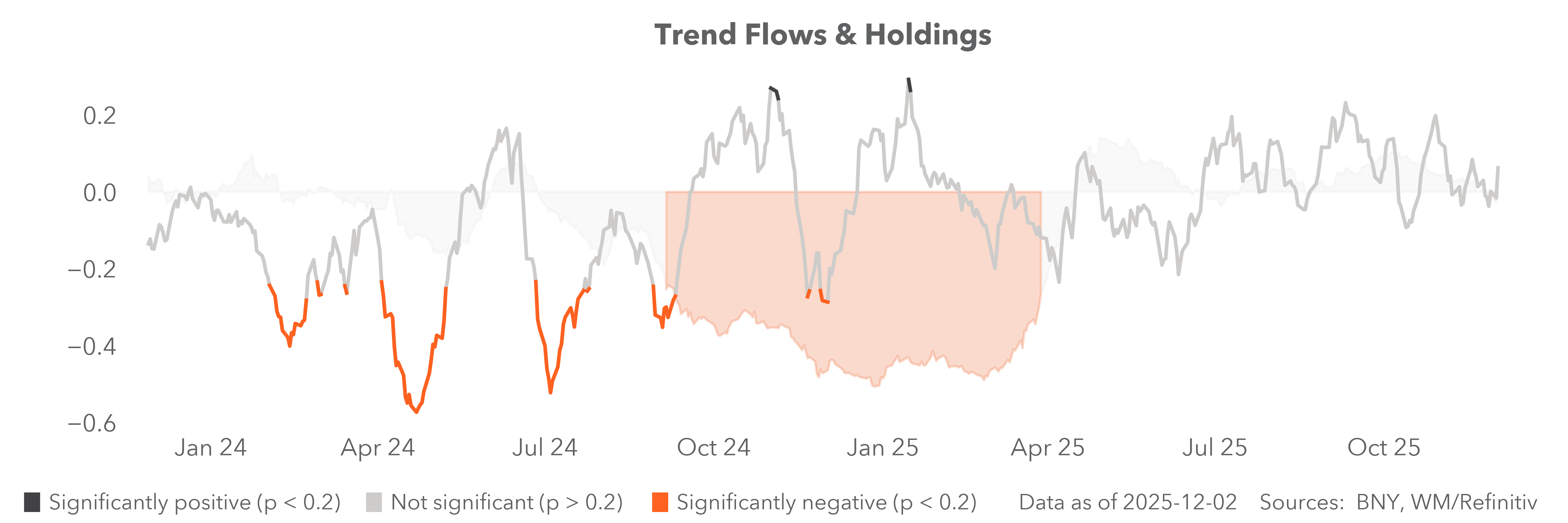

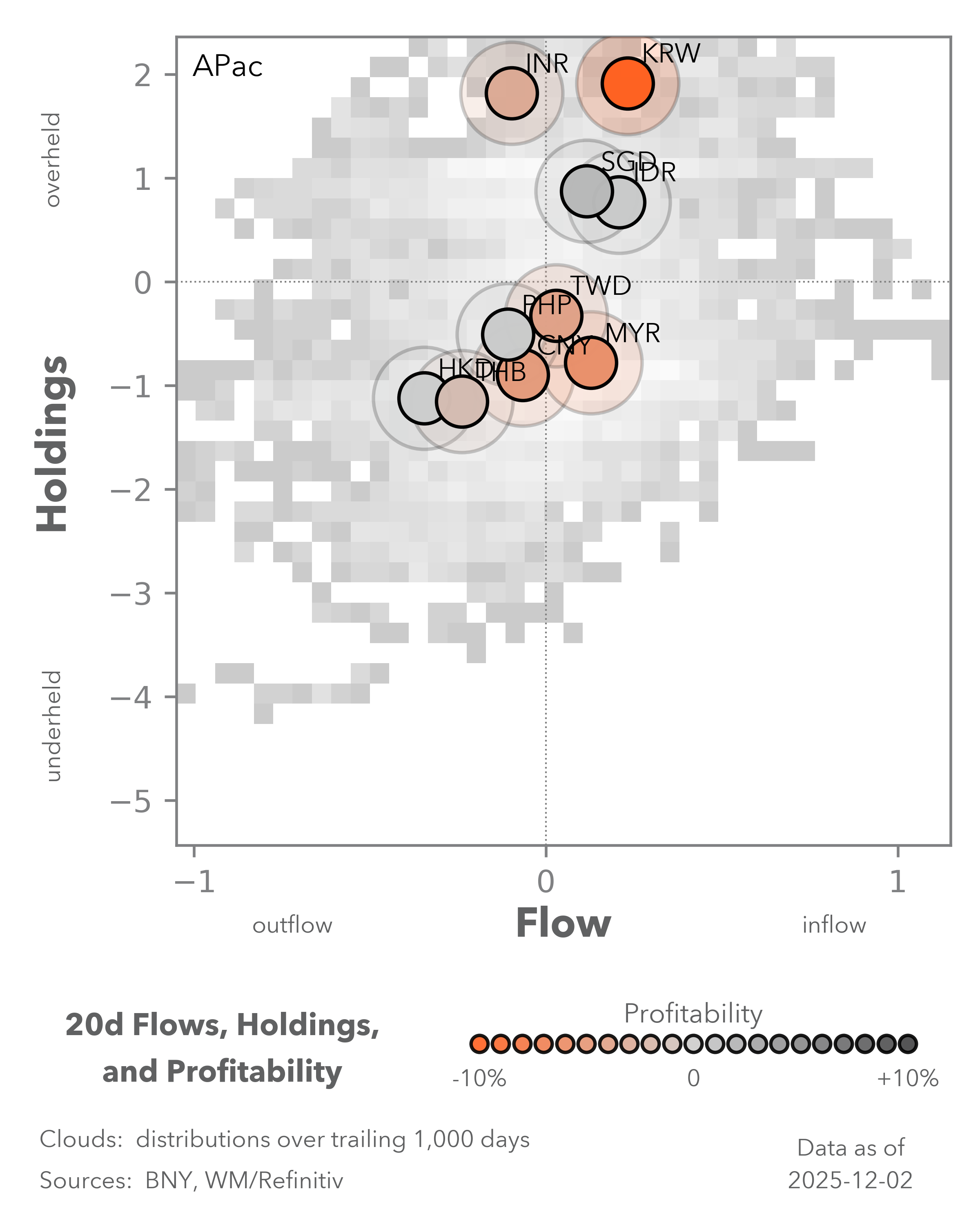

The Indian rupee’s (INR) ongoing decline this week is a major flashpoint in EM FX. The currency has been one of the anchors for carry trade holdings globally, and, along with the Indonesian rupiah (IDR), one of the only APAC currencies to sustain overheld status throughout recent rate cycles.

The macro drivers behind INR flows are well documented, and current reports point to foreign institutional investors (FIIs) as the main drivers of weak performance, along with strong FX demand from domestic financial institutions. The INR has been a sui generis case in APAC, and we don’t see a material impact on broader EM FX performance – other Asian currencies, for example, are in a different savings and flow position.

In this light, we would also be cautious in calling for extreme moves ahead of the Reserve Bank of India’s (RBI) decision next week. We broadly agree with the market’s view that the RBI has capacity to deliver another 25bp cut to 5.25% as it seeks to boost the economy.

Forward look

After USDINR moved past 90.0 on Wednesday, India’s Chief Economic Advisor V. Anantha Nageswaran said that he was “not losing sleep” over the currency’s decline and that movements were “not troubling” the administration.

Although we believe the RBI will need to maintain vigilance and support efforts to stabilize exchange rates, INR weakness that helps close large current account gaps should be seen as welcome in the near term. We don’t see material outflows on a structural basis either, as most FIIs are seeking India allocations as part of a longer-term asset allocation view.

Our leading iFlow EM index (Exhibit #2) shows a daily rolling 12-month incurrence of external portfolio liabilities and compares it to lower-frequency official data. The trend over the past 12 months remains positive, and as of December 2, the rolling 12-month sum is also positive for the Indian economy. Strong levels of accumulation since 2022 have established a solid net positioning buffer, echoing consistent holdings in the RBI. The RBI may soon be able to signal terminal levels, with real rates at a sufficient level to support the INR.

Foreign investors keen on EM allocations next year may even see current INR levels as offering value for underlying assets, and any progress toward a trade deal with the U.S. and better insulation from geopolitical factors will provide renewed support.

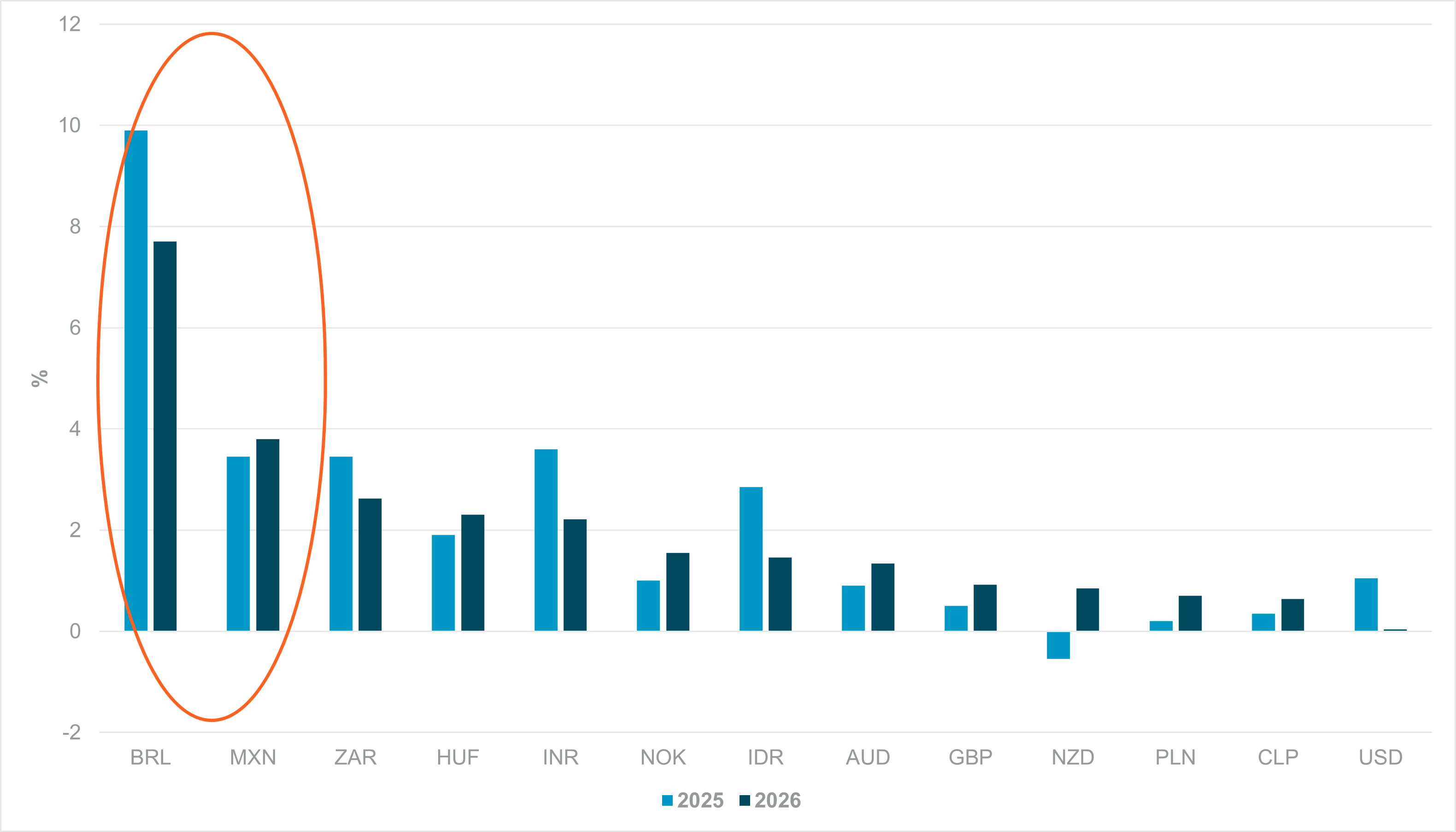

EXHIBIT #3: CURRENT AND 2026 REAL RATES, KEY “CARRY” ECONOMIES

Source: BNY, OECD

Our take

Based on the Organisation for Economic Co-operation and Development’s (OECD) latest forecast and current market pricing, the INR will continue to have the highest real rates in APAC and rank among the top five major markets globally by the same measure. As the December round of G10 policy decisions loom, we expect more central banks to signal that resuming tightening cycles is possible. However, the OECD’s own CPI forecasts do not suggest a strong risk of overshooting inflation.

We identified 12 currencies across G10 and EM where current rates are relatively high – around 4% or higher – or where the one-year to one-year-forward rate can point to better carry prospects. This list also includes the USD, which will remain the main benchmark (Exhibit #3).

For 2026, no currency on this list is expected to have meaningfully low real rates, which is largely by design. Only New Zealand is expected to end 2025 with negative real rates, which may explain its recent decision to signal an end to the easing cycle, even though data warranted additional support.

Forward look

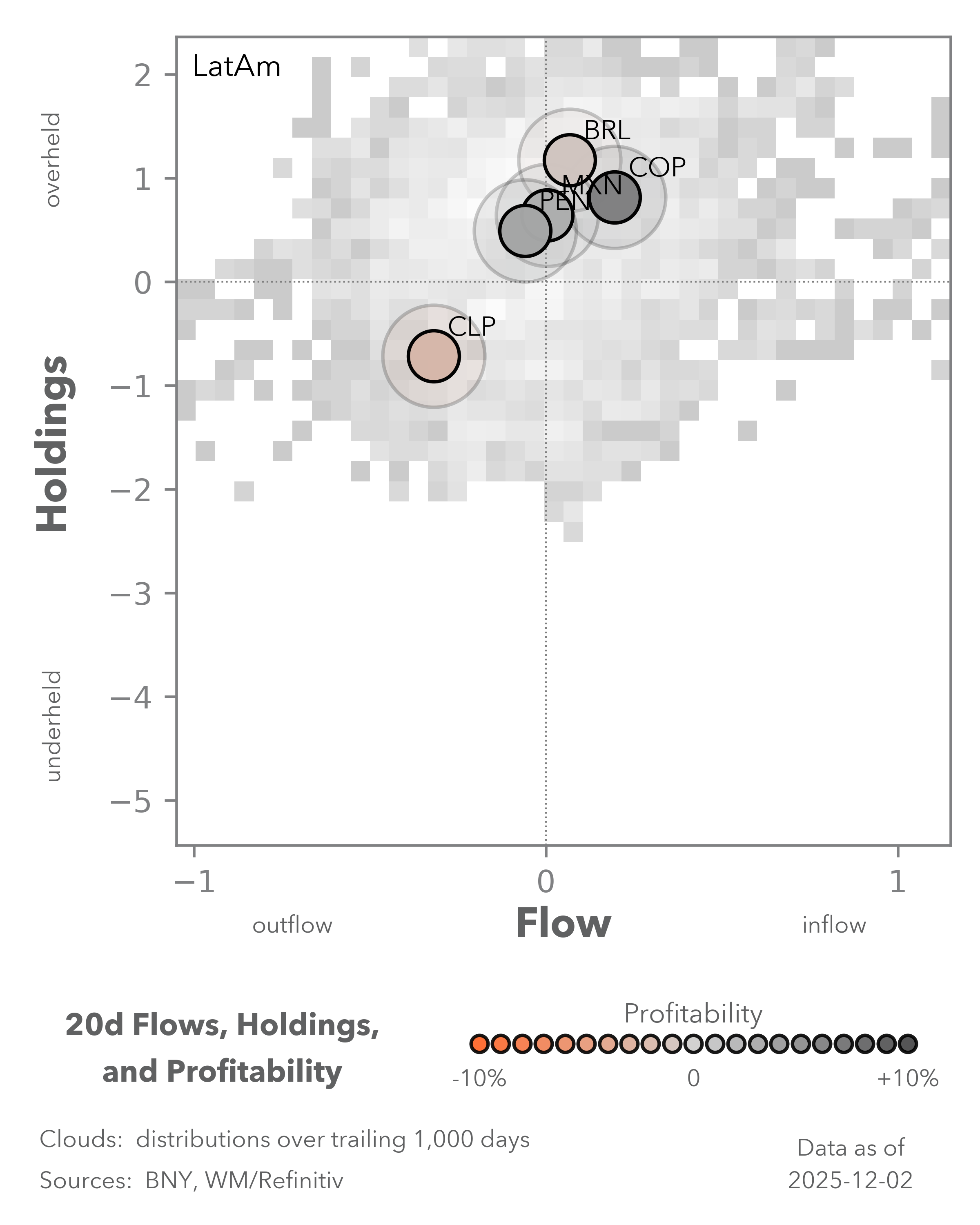

Within this group, Latin America is maintaining a material advantage. Brazilian real rates are expected to remain in the high single digits next year, much to the disappointment of fiscal authorities. Forward rates also point to a strong Banxico rate anchor, which is unlikely to change even if a more permanent trade arrangement with the U.S. is realized

The biggest risk for all these economies is a lack of fiscal consolidation. This is viewed as a more significant risk in Central and Eastern Europe than in Latin America. In all cases, the erosion of real rates through higher-than-expected inflation is likely to occur via the fiscal channel.

A structural challenge, however, is the poor outlook for emerging markets to raise real rates – and their currencies – through productivity gains, as China’s industrial prowess has cast doubt on their ability to move up the value chain through manufacturing alone.

Fiscal consolidation aside, policy adjustments focused on economic diversification and value-added services growth should move up the agenda, especially if the external trade outlook is now permanently affected by U.S. tariffs and Chinese capacity issues.

In this context, currency strength purely for external competitiveness is far less relevant to growth and industrial policy. We expect central banks to remain broadly supportive of sustained nominal appreciation.