Conviction lacking amid consensus views

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

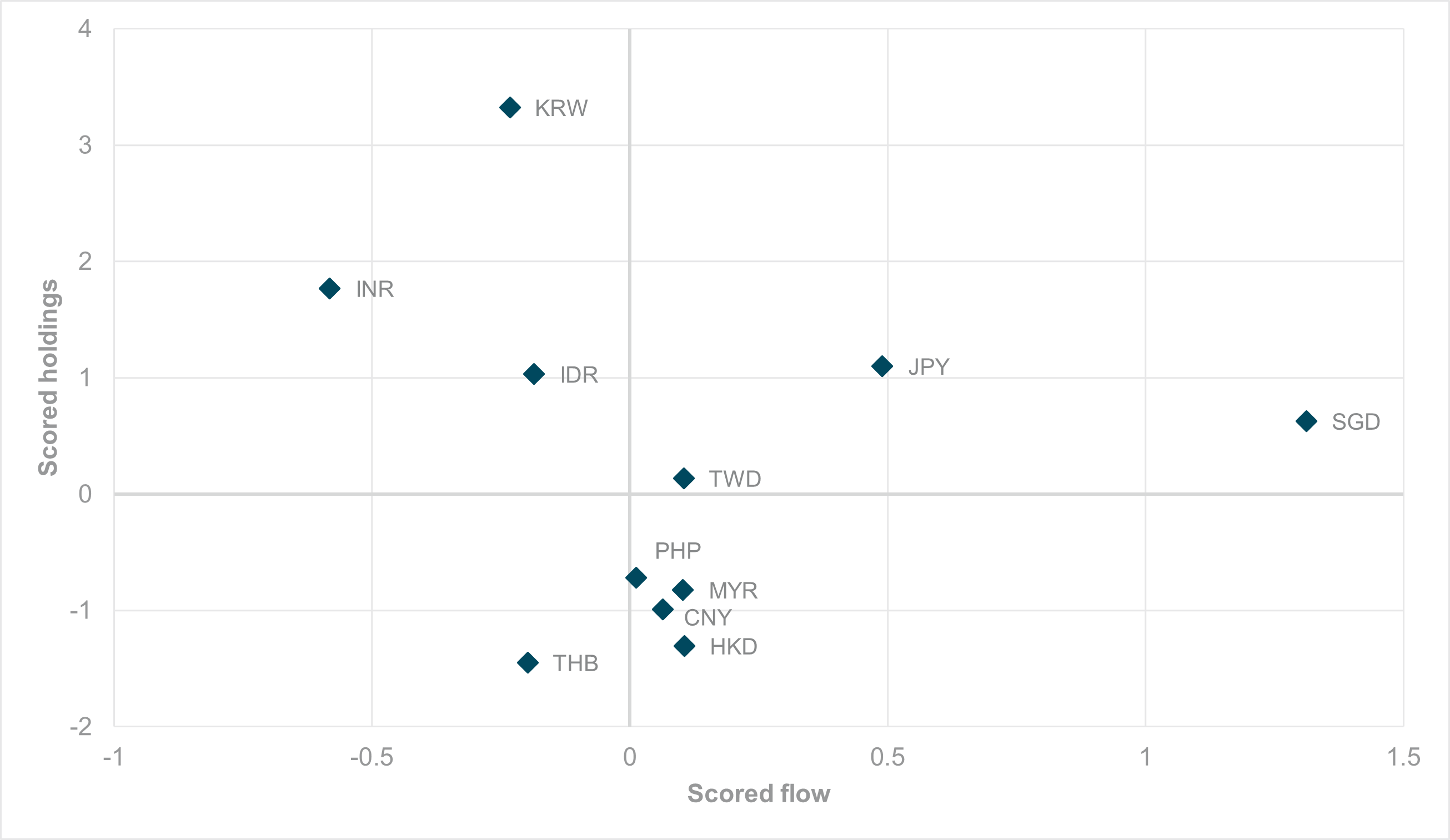

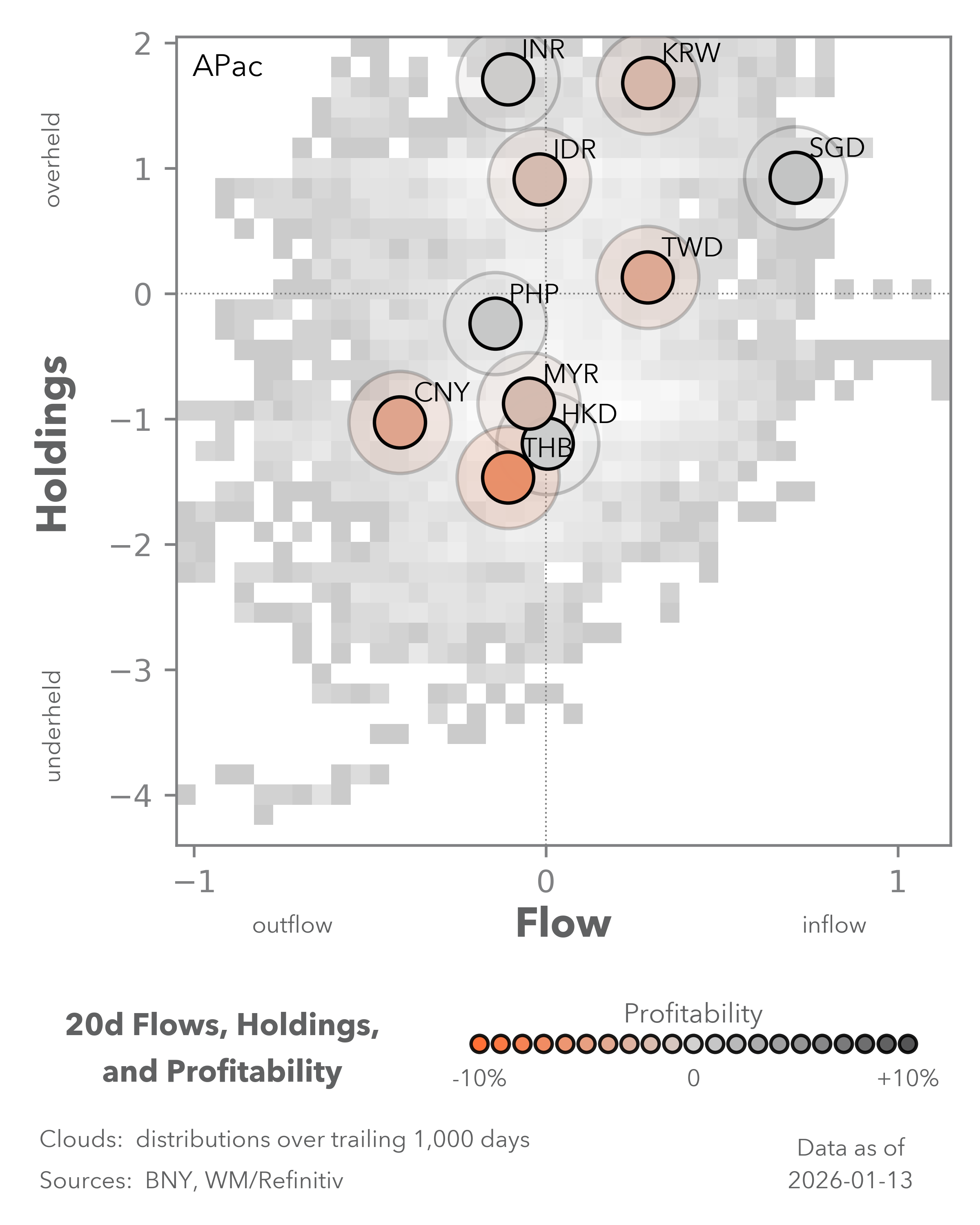

EXHIBIT #1: WEEKLY SCORED HOLDINGS VS. FLOW – EM APAC CURRENCIES AND JPY

Source: BNY, Macrobond

Our take

APAC currency valuations are back on the agenda as official discomfort with current exchange rates is rising. Multiple Japanese officials have called the JPY level inconsistent with fundamentals, while U.S. Treasury Secretary Scott Bessent warned on Wednesday that the depreciation of the KRW was also “not in line with [South] Korea’s strong fundamentals.” Similar grievances surrounding CNY valuations have been standard from U.S. Treasury Secretaries for at least two decades, while the TWD and CHF could face similar scrutiny given their large total and U.S.-specific trade surpluses.

The need for APAC currency appreciation is a well-established view for 2026, and iFlow indicates that asset allocators are now largely positioned for strength. Throughout 2025, we observed how JPY stayed in overheld territory for cross-border investors. Even now, it is largely on par with NOK as the best-held currency in G10. Despite progressive weakness against the dollar, valuations pointed to secular improvement. The Bank of Japan (BoJ) also pushed for gradual tightening, only for government and policy changes to generate some uncertainty regarding their policy path.

Forward Look

Toward the end of 2025 and more recently, KRW and TWD both moved toward overheld territory (Exhibit #1), after struggling through a period of strong underheld positioning due to carry loss versus the dollar and others. SGD – perhaps the only clear safe-haven in the region, backed by strong credit ratings – have also seen holdings remain static in overheld territory. The only other overheld APAC currencies are INR and IDR, both core carry names.

It is clear that broad-based appreciation among APAC is now the base case, but flows over the past week suggest that aside from the uniquely positioned SGD, underlying flow magnitudes remain light. The view is clear, but conviction is lacking. Even with rhetoric on the side of APAC FX longs, such as KRW and JPY, official action is not seen as effective. Efforts to stabilize the KRW did not generate sustained strength. TWD has given up most of its Q2 2025 gains, and questions remain over Japan’s fiscal credibility. Crucially, there are no clear signs of more assertive Fed easing to mitigate carry interest.

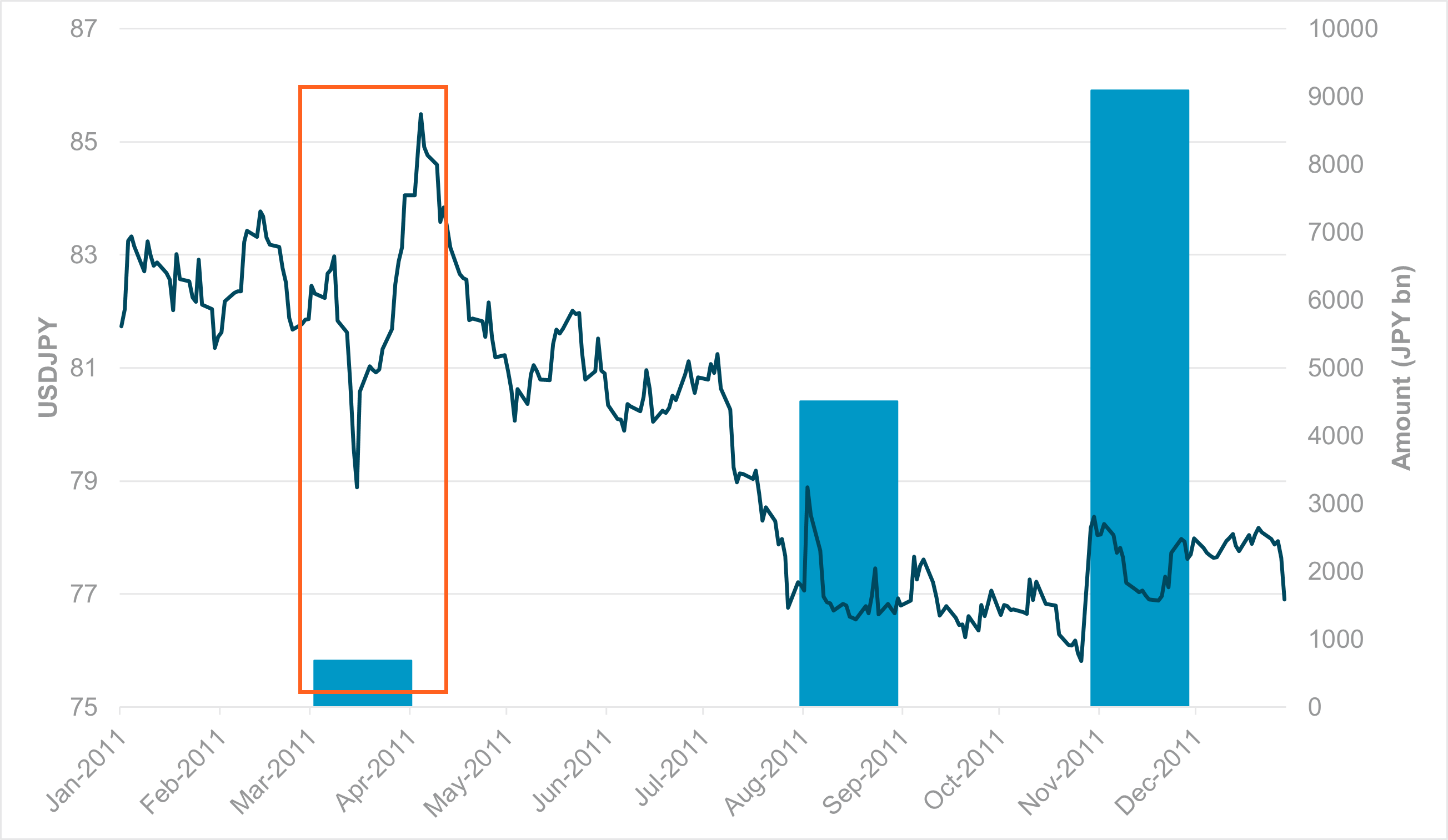

EXHIBIT #2: USDJPY VS. JAPAN INTERVENTION OPERATIONS, 2011

Source: BNY

Our take

For now, Japanese and U.S. monetary policy are insufficient to move the needle on currency weakness, while administrative efforts to influence long-term hedging behavior by local asset managers are unlikely to have near-term impact. If patience begins to run thin in the U.S. Treasury Department, extraordinary measures may be considered – one of which is U.S.-led joint intervention. Given currency valuations are viewed as a critical factor in trade talks and part of the U.S. Treasury’s toolkit, we see little scope for Japanese, South Korean and Taiwanese authorities to push back. (China and the CNY remain a separate case.)

The last time global fiscal and monetary authorities participated in joint intervention with Asia at the core was in March 2011. Following the Great Tohoku Earthquake, the JPY appreciated sharply due to risk-aversion flows in Japan. On March 18, the Federal Reserve, European Central Bank, Bank of England, and Bank of Canada coordinated with the BoJ – acting on behalf of the Ministry of Finance – to engineer a weaker JPY. The U.S. intervened with $1bn – split between the Federal Reserve System’s Open Market Account and the U.S. Treasury’s Exchange Stabilization Fund – while total Japanese sales of JPY were close to $8.5bn. The effect was immediate and forceful, with USDJPY rallying over 6% in just three weeks. The one-off episode was far more effective than the much larger interventions later in the year, including a mammoth $120bn round in October, which was almost fully reversed by year end.

Forward look

We stress that for surplus APAC economies, limiting currency weaknesses is very different from future strength. By and large, it would require a change in behavior in local savings pools, coupled with much higher local yields that governments may not be willing to tolerate. However, the U.S. holds a strong advantage in this respect. Political tools such as tariffs and trade barriers aside, engineering dollar weakness is far more straightforward for U.S. authorities.

To be clear, as the experience of 2011 shows, intervention itself is not sufficient to correct misalignments. APAC surplus economies must change their behavior through credible, large-scale fiscal stimulus to raise domestic demand. Steeper local curves would also help keep more funds onshore, while greater cross-border investment – supported by high levels of dollar hedges – could help loosen financial conditions through financing channels.

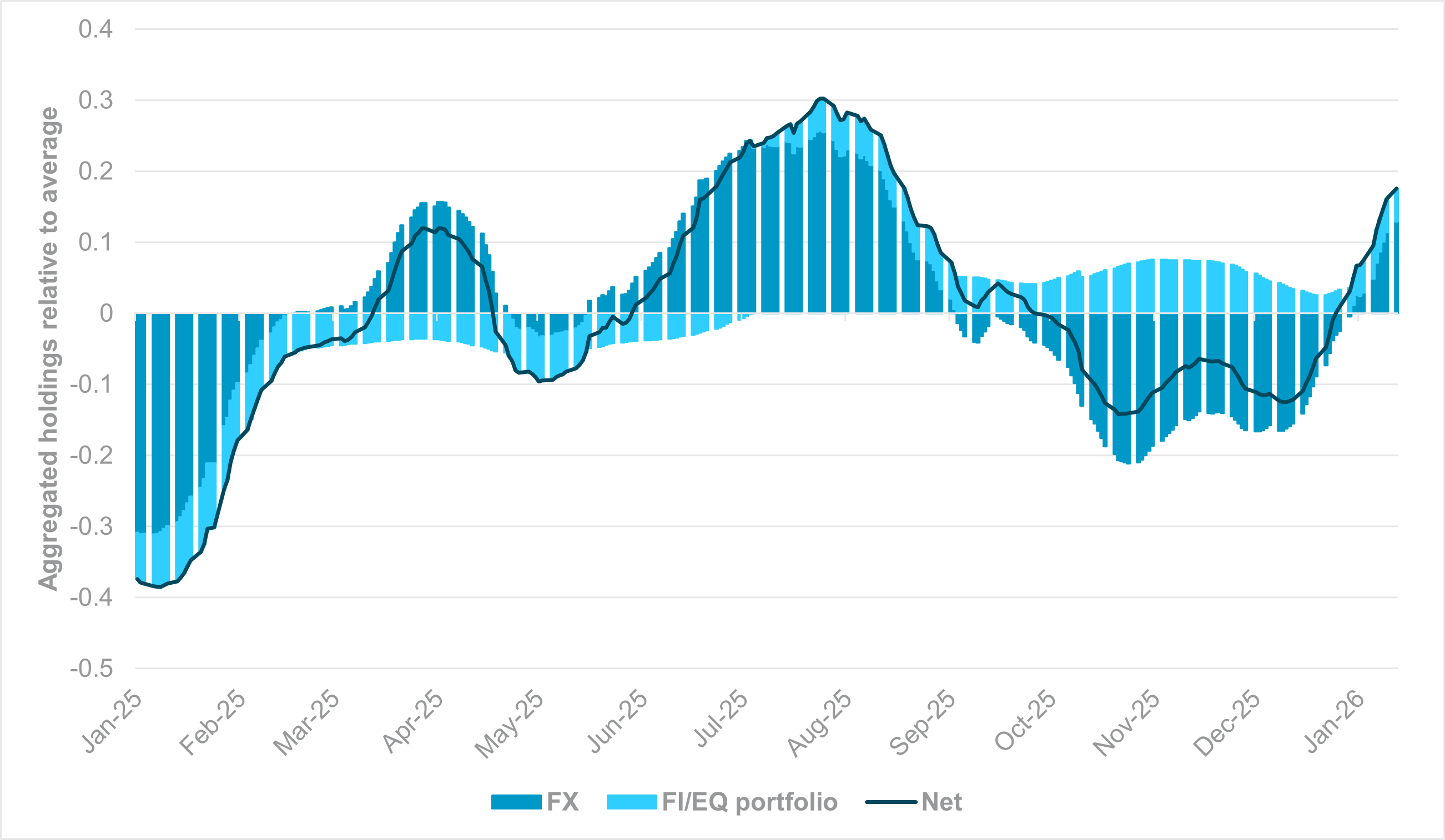

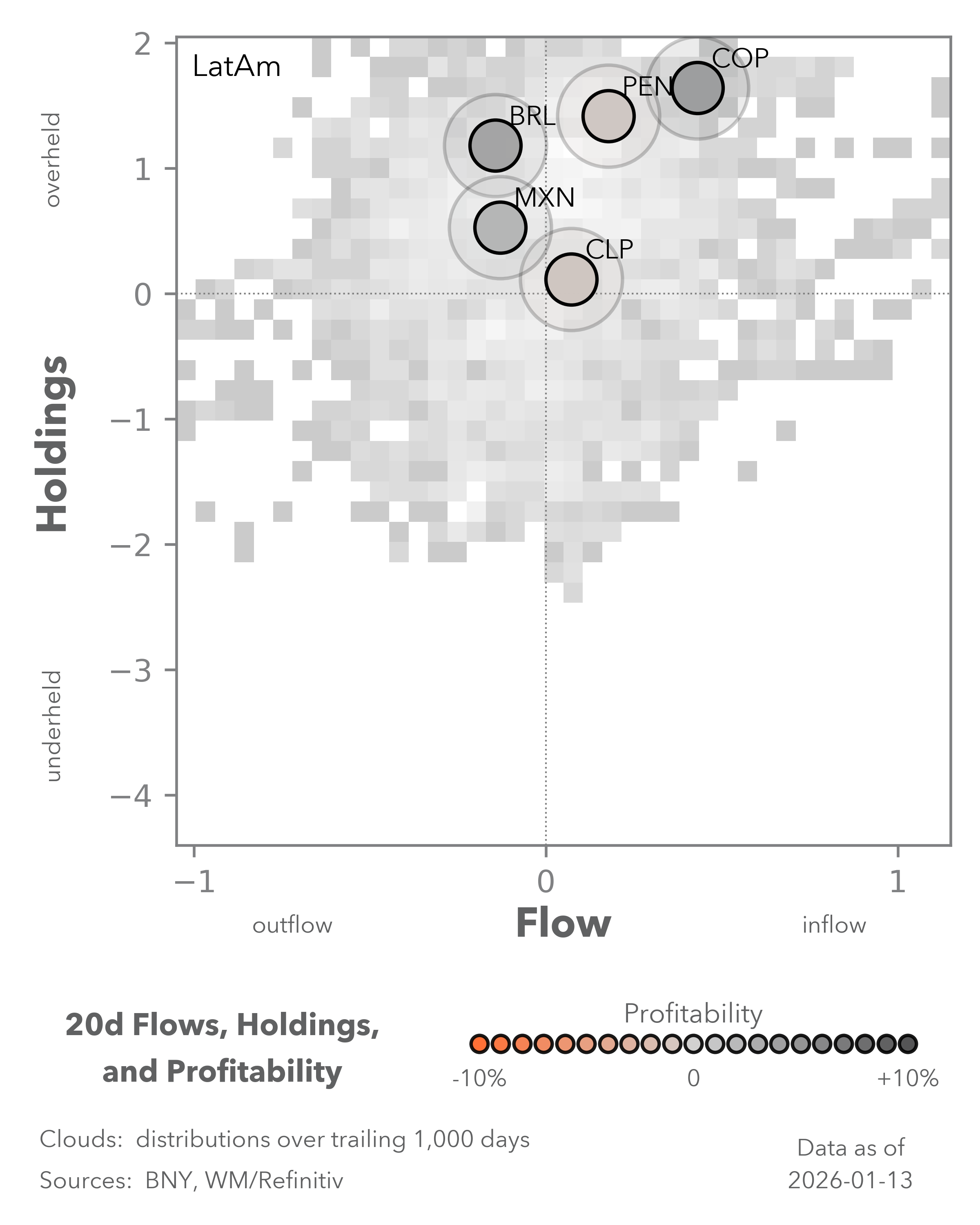

EXHIBIT #3: CUMULATIVE HOLDINGS VS. 1Y AVERAGE, FX AND LATAM FI/EQ PORTFOLIO

Source: BNY

Our take

In terms of FX valuations, one region where U.S. Treasury Secretary Bessent need not be too concerned is in Latin America (LatAm). Although FX flows into high-carry regions have moderated, holdings levels remain near 18-month highs, with no signs of an impending correction. Geopolitical risks will continue to factor into the equation, but the combination of high real yields and an ongoing commodity rally is helping the region hold its own.

Although the Fed is not dovish enough to fully boost the carry trade, current conditions still support maintaining large FX positions alongside moderate asset holdings. We highlight that relative to the 1y average, total exposure is now steadily approaching the highs seen around mid-2025. Assuming an 80:20 fixed income to equity split, combined FX and portfolio holdings in LatAm show FX once again driving the contribution (Exhibit #3).

Forward look

EM asset allocation in general is still recovering from several years of U.S. exceptionalism. The base for positioning in both fixed income and equities is so low that significant improvement need not come at the expense of U.S. or broader developed market performance. However, the right balance between FX and asset exposures is necessary.

For now, we see a greater risk of FX holdings declining due to stretched positioning, meaning further asset inflows will likely face a higher hedge ratio. This means that LatAm central banks may utilize the current phase of currency strength to accelerate easing or at least guide toward lower terminal rates.