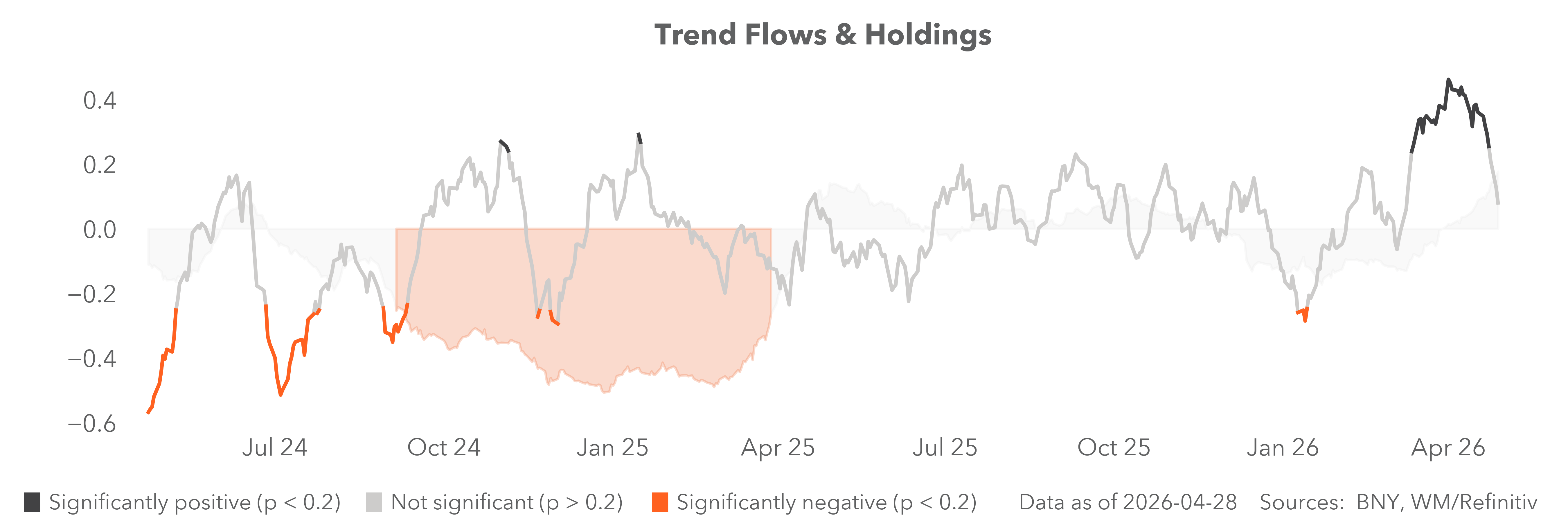

Breathing space for idiosyncratic drivers

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

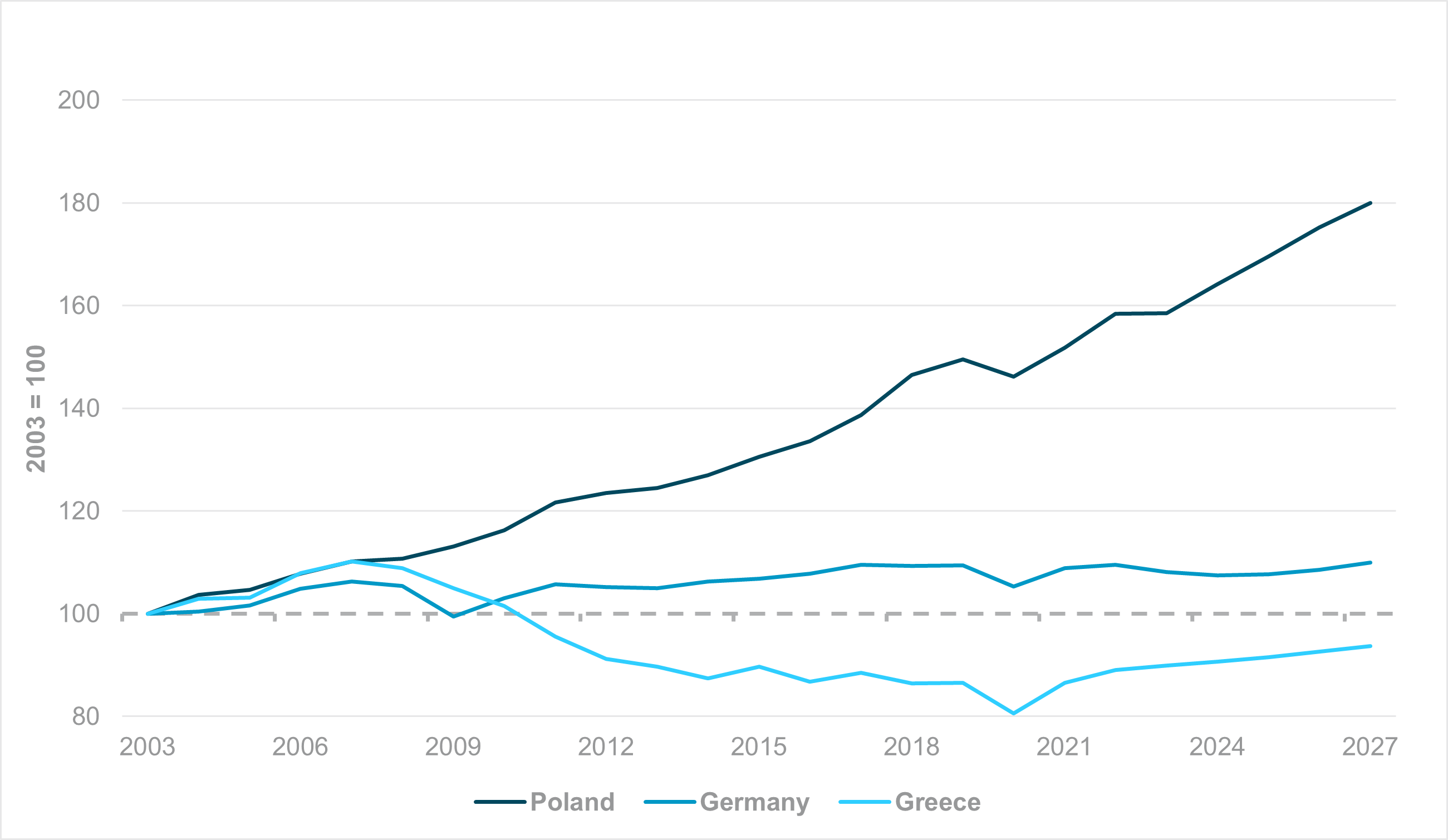

EXHIBIT #1: OECD LABOUR PRODUCTIVITY, 2003 = 100

Source: BNY, Bloomberg, OECD

Our take

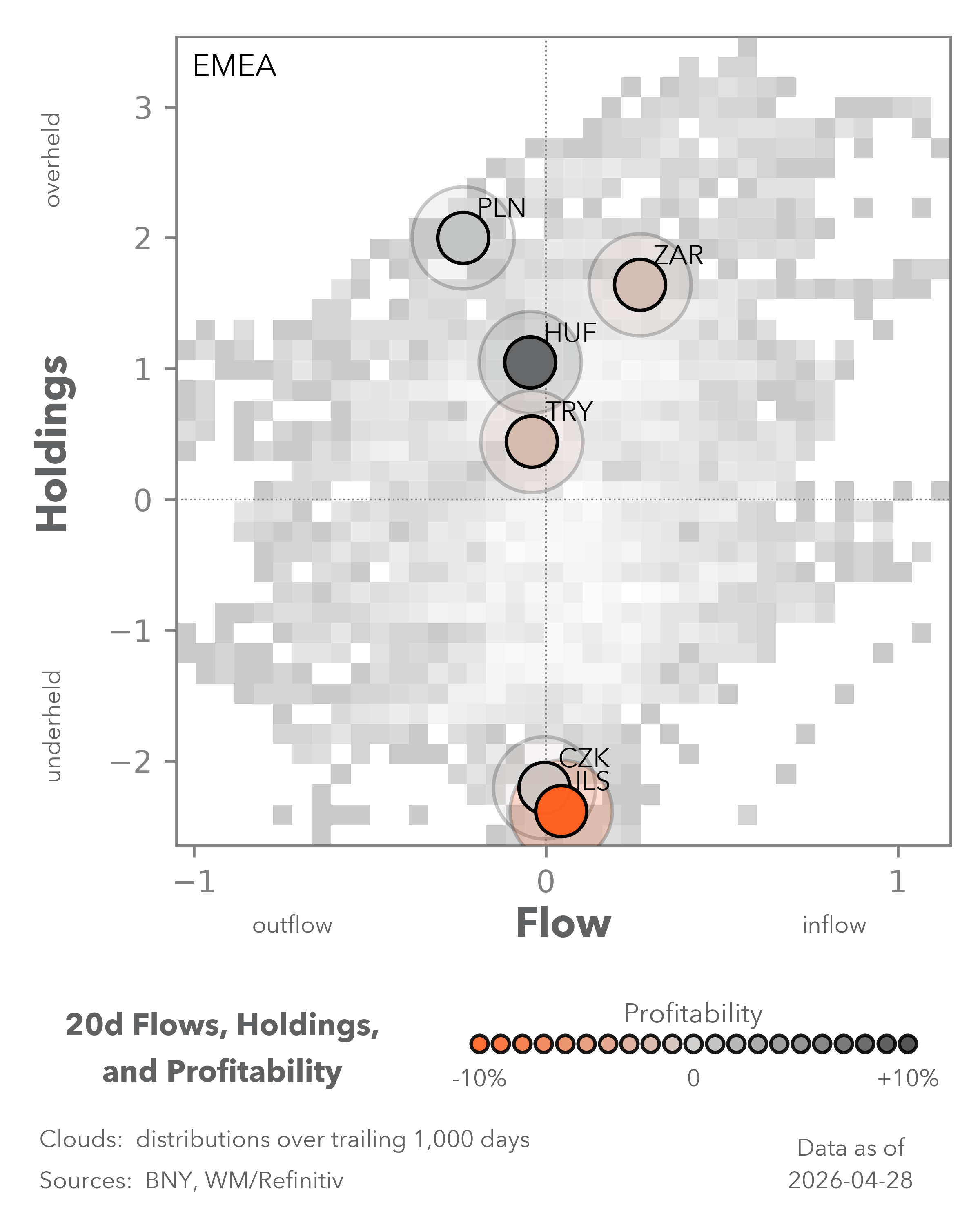

The National Bank of Poland decision next week is not expected to generate any surprises, and the market is currently more focused on the fiscal trajectory, especially if adverse developments will pose a threat to positioning. The government has raised its full-year deficit forecast to 6.8% of GDP from an already high 6.5%, and the risk is clearly to the upside if energy subsidies are extended. The EU will likely allow for national budgetary flexibility in the current environment, and normally the currency would need to weaken to offer investors a risk premium. For now, however, real rates are sufficiently high to act as a restraining factor on other facets of the economy. If wage growth overshoots, the market may want to push for a more hawkish path – average wage growth remains above 6% y/y, and vigilance is warranted.

Forward Look

With respect to the deficit, Finance Minister Andrzej Domanski stated this week that “Poland is not threatened by a second Greece.” Notwithstanding that Greece’s fiscal performance has been exceptional in recent years (something Domanski himself stressed), there are crucial differences between the Poland of the mid-2020s and Greece during its sovereign debt crisis. A flexible exchange rate and monetary policy independence is the first factor. Data quality of public finances matters here as well.

Finance ministers typically point to their countries’ ability to grow out of debt – and in this respect, Poland has one of the strongest possible cases in Europe, due to strong productivity growth. Greek productivity was already on the decline by the mid-2000s (Exhibit #1), and this exacerbated fiscal stress during the crisis. In contrast, Polish productivity growth has outperformed Germany’s ever since it joined the EU, and there is no sign of a slowdown, with the latest push helped by defense spending, both domestically and on a multilateral basis. PLN has stress factors, mostly in valuations and holdings, but fiscal factors are manageable. The country’s focus on industry rather than excessive financialization can also help it avoid imbalances, but supervisory vigilance will be crucial.

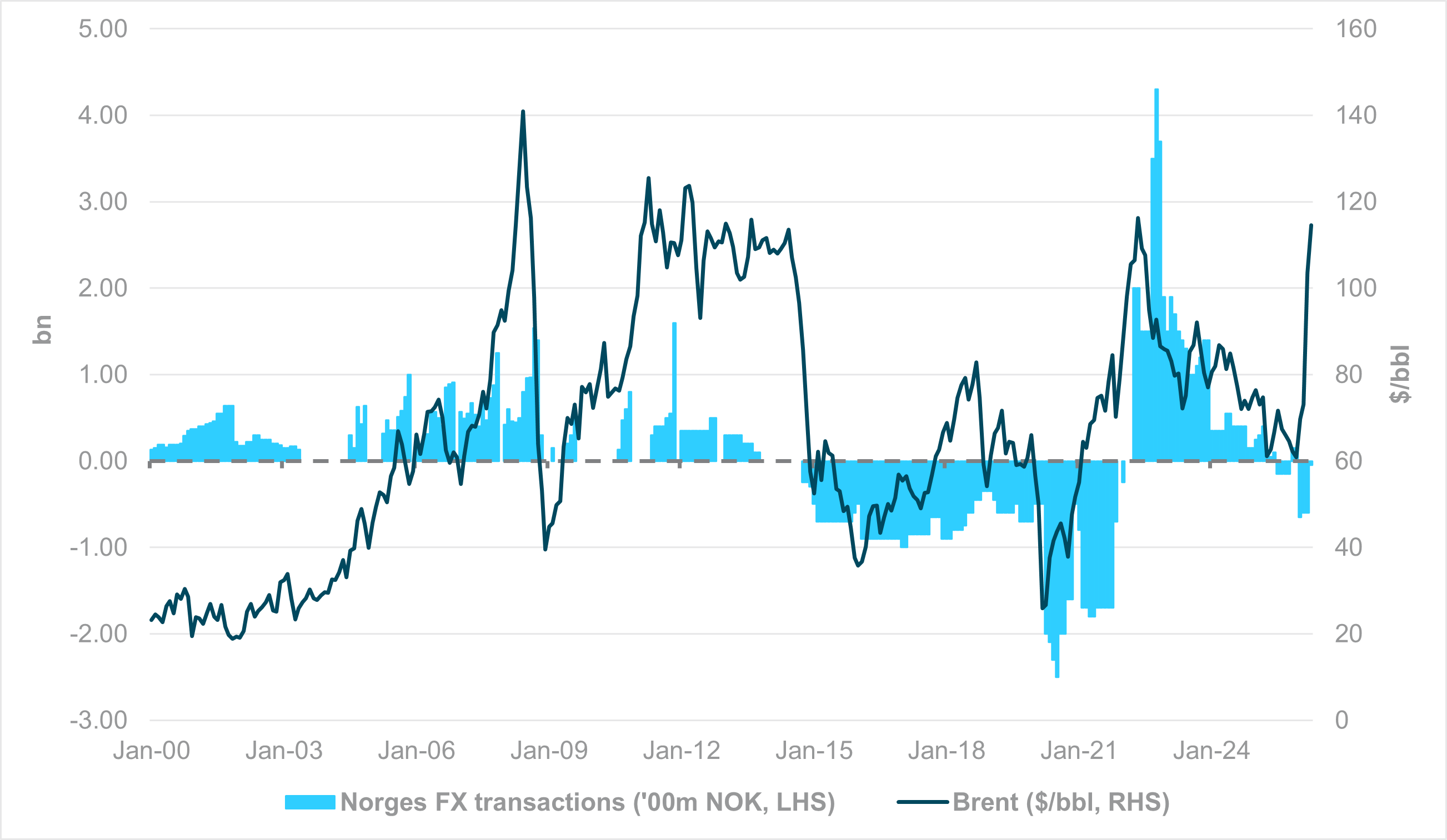

EXHIBIT #2: NORGES BANK DAILY FX TRANSACTIONS VS. BRENT CRUDE

Source: BNY, Macrobond, Norges Bank

Our take

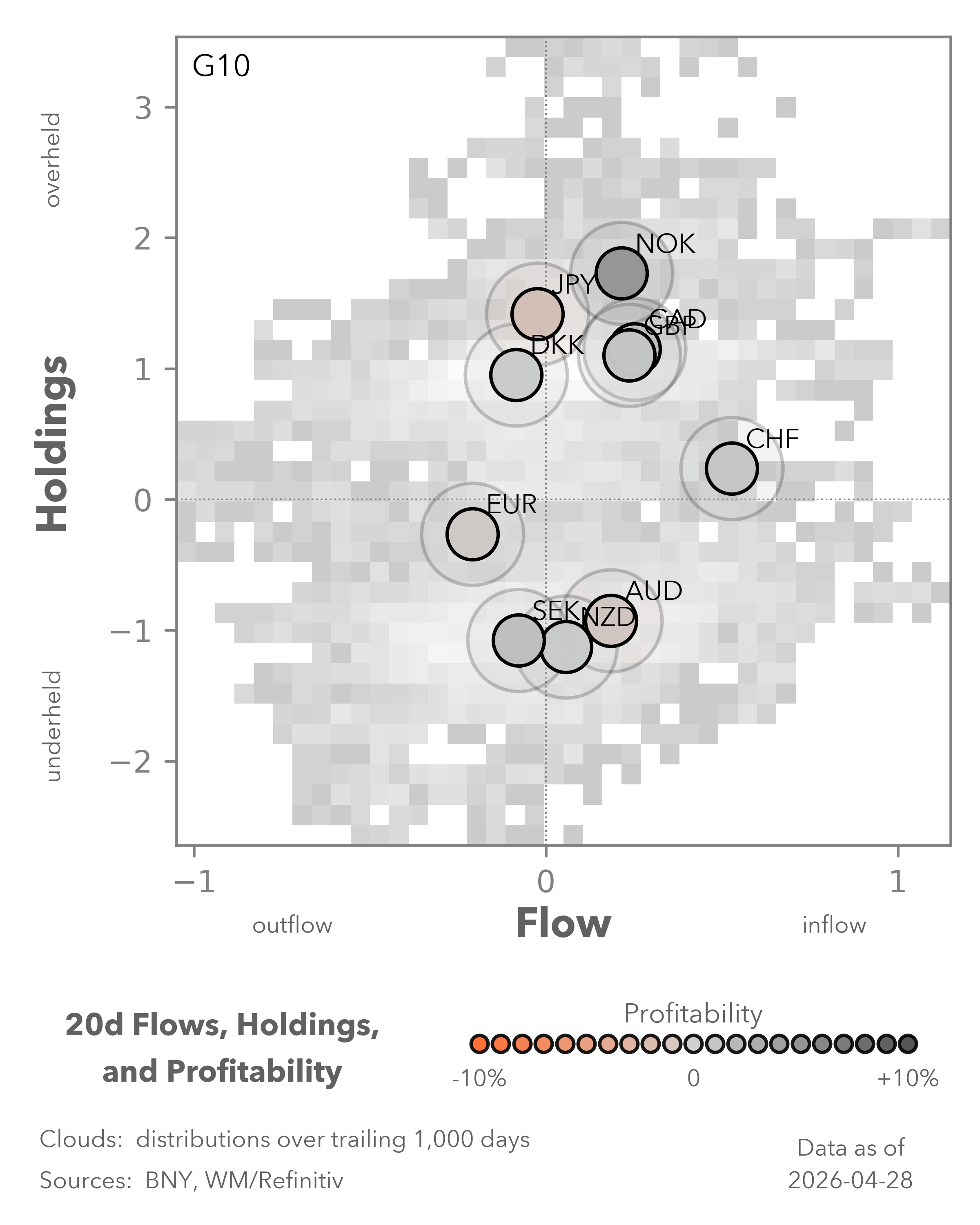

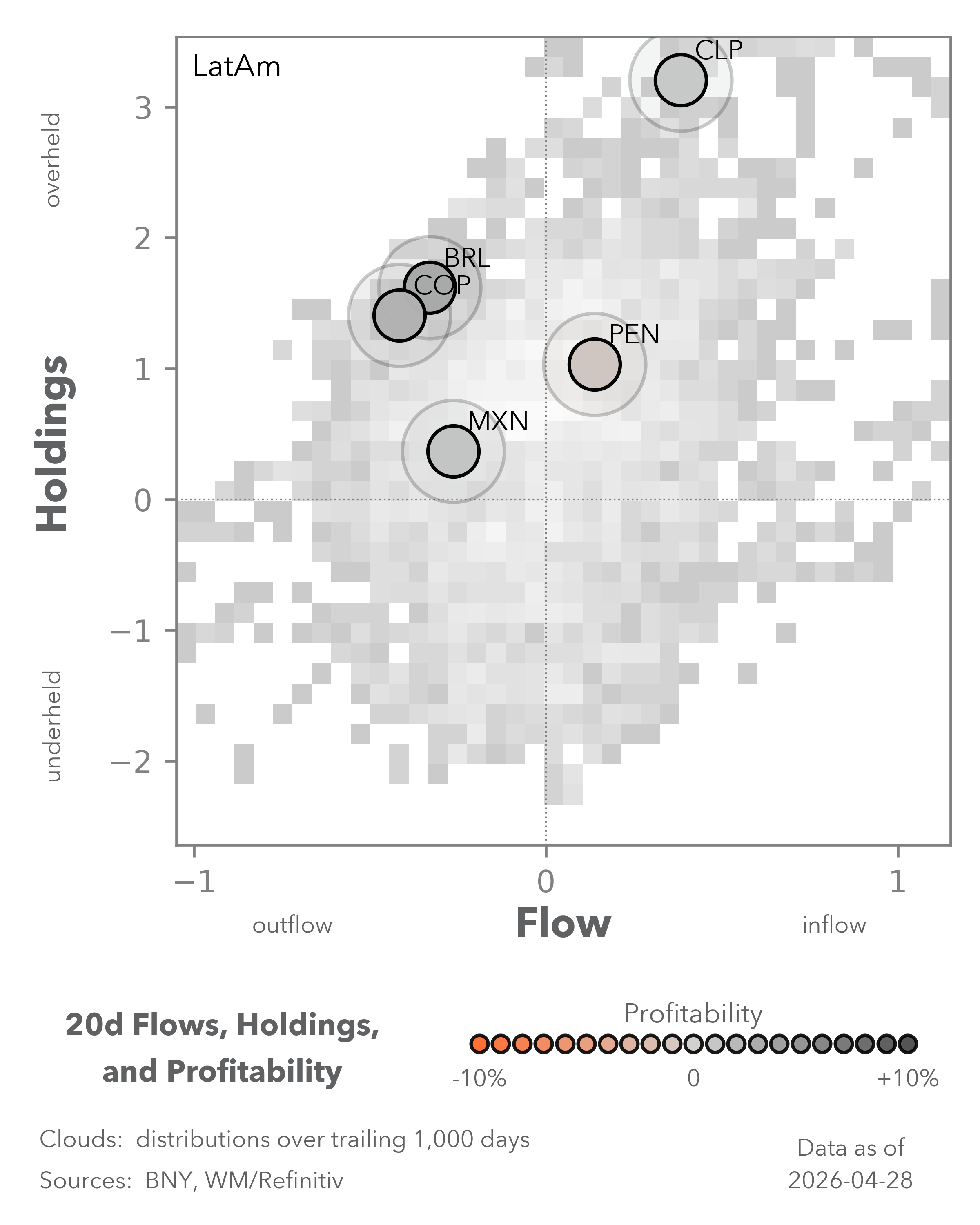

A key theme for end-April rebalancing flows is some softening in commodity-linked currencies in G10 and EM. This is not a call against fundamentals in any way, and we expect balance of payments to remain strong in Norway, Australia and much of Latin America. However, with the ceasefire still in place and domestic economies adjusting rapidly, there is now a window to take stock of idiosyncratic factors. For example, the rate decisions in Scandinavia next week may all have a hawkish lean in line with peers in Europe, but we expect the near-term outlook to be relatively challenging for both SEK and NOK. The Riksbank is expected to stay on hold, and full-year pricing is well below the ECB. Meanwhile, Norges Bank has already flagged a potential hike, but further changes will heavily depend on wage developments. Furthermore, even if Norges leads tightening, we believe the balance of flow is on the verge of shifting as Norges Bank is able to start selling NOK again.

Forward Look

Irrespective of the war’s outcome, energy prices will likely remain elevated and well above budget assumptions established before conflict levels. Norway has already downgraded non-oil sector growth to 1.8% from 2.1%, but the deficit hit will be manageable as domestic demand remains robust. We believe a repeat of the 2022 situation will likely repeat, whereby a geopolitical shock suddenly boosts oil revenues well above expectations, resulting in a 38-month run of net FX purchase and NOK sales. There will be a transition period, as there was in 2022: Norges Bank moved from net buying of NOK 250mn per day that January to flat for two months, before sharply raising FX purchases to NOK2bn per day in April 2022. April transactions were already close to flat, and the market should brace for a shift in the balance within the next quarter. Barring extremely aggressive Norges hikes, it is hard to see other factors supporting further re-rating in the currency.

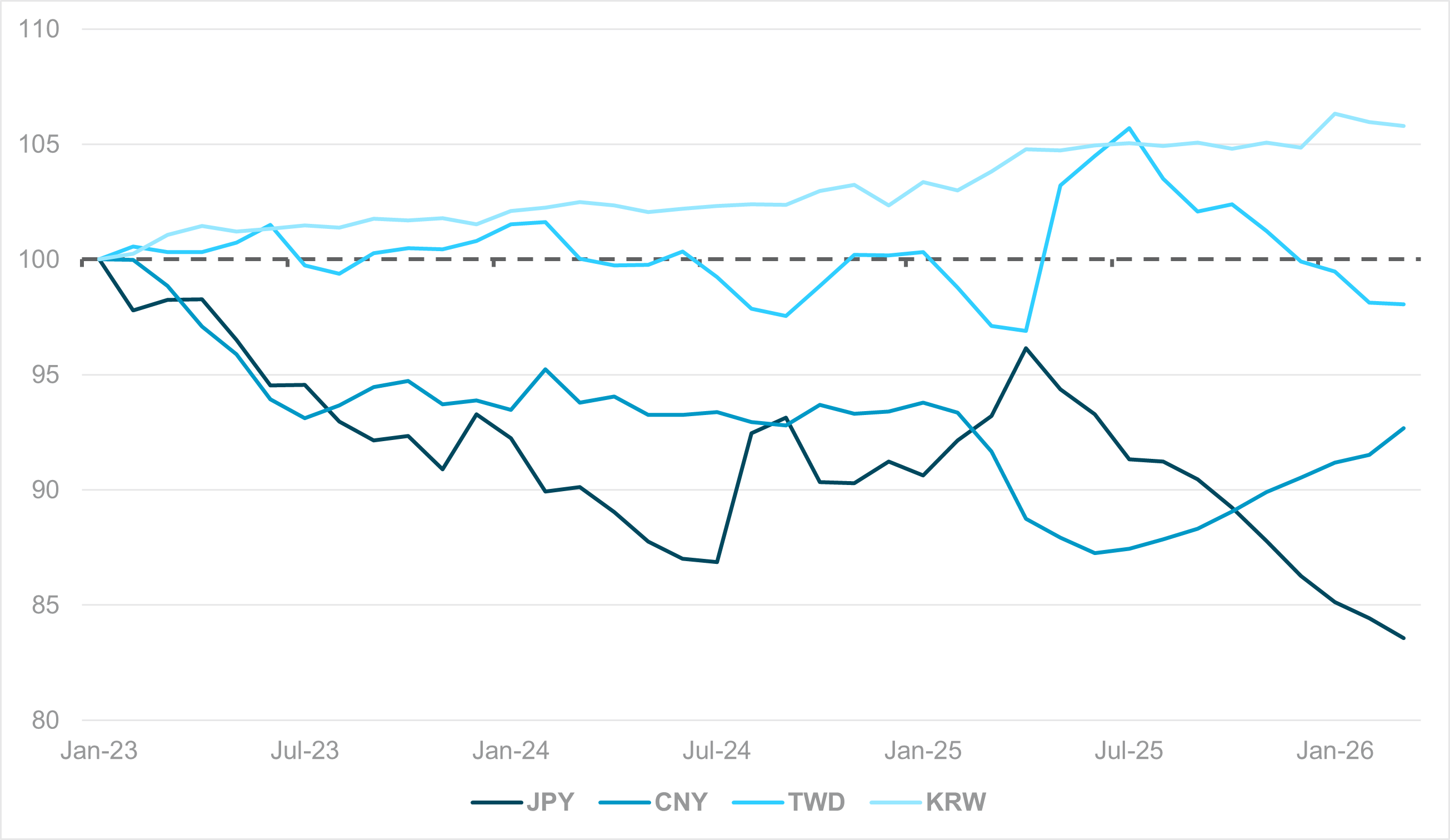

EXHIBIT #3: BIS REER EVOLUTION SINCE 2023, REBASED

Source: BNY, Bloomberg LP

Our take

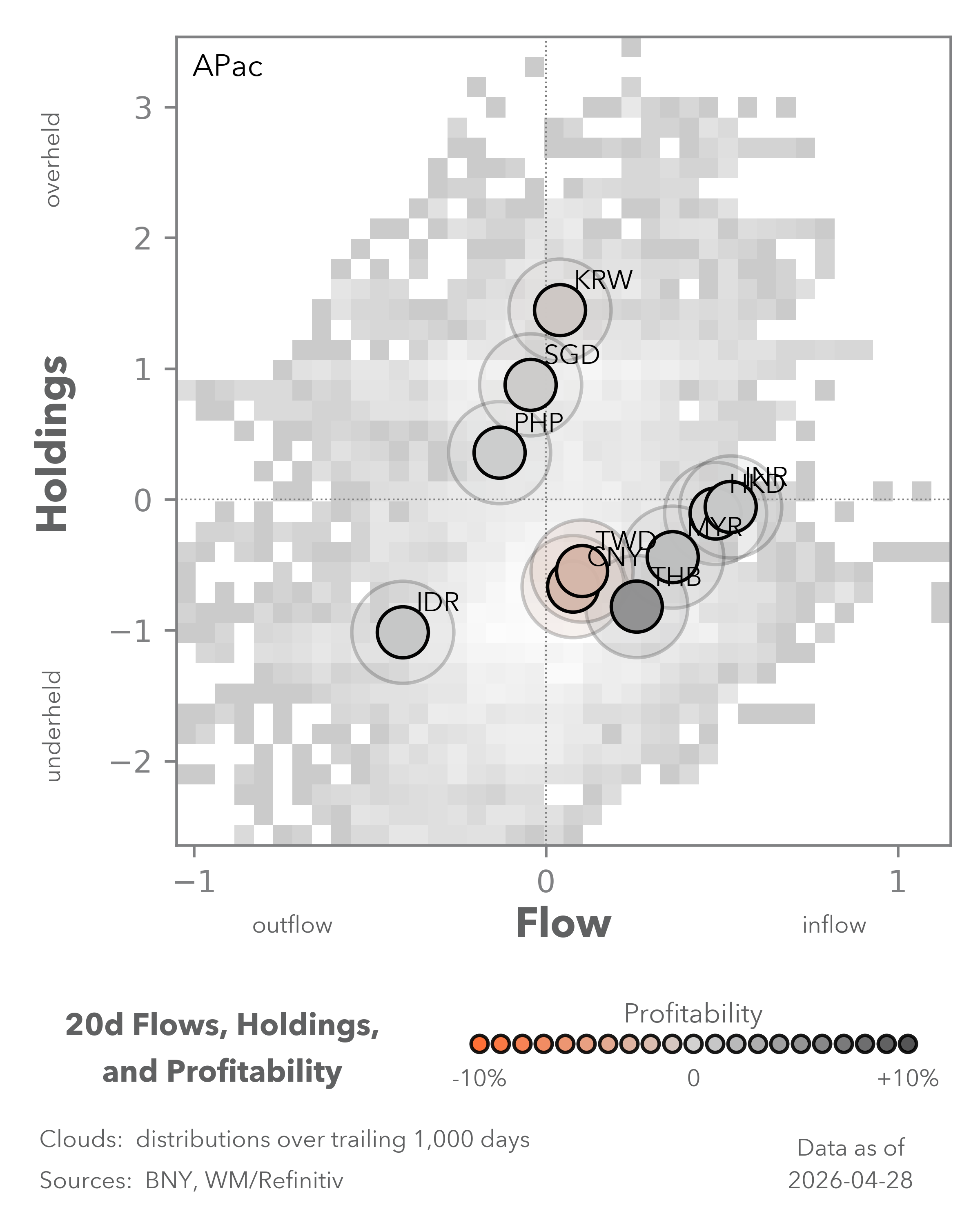

Upside inflation surprises in China, especially in PPI, have injected a new dynamic into APAC FX and the wider global economy. This is clearly a double-edged sword. On the one hand, for years the market and global policymakers called for China to engage in fiscal policies to support inflation expectations. This will drive a higher CNY real effective exchange rate (REER) through inflation differentials, boost China’s purchasing power and stimulate the region. Now that this is taking place, however, there is no sign of China ceding market share across manufactured goods to the extent that the currency’s strength could even drive inflation globally, amid acute supply chain shocks. The prospect of China leaving behind certain lower value-add parts of the global manufacturing sector is remote, and captive shares may even help boost corporate margins to serve domestic purposes.

Forward look

Based on the performance level and breadth of Chinese equities, the market is certainly not anticipating any sudden margin lift, and CNY strength will not help that cause in the near term. We continue to see managed nominal appreciation, and even with higher PPI, the global lift in inflation may also limit the extent of REER gains. Furthermore, based on trend performance since 2023 when China exited pandemic restrictions, the currency’s valuations remain relatively attractive and are well below TWD and KRW equivalents, even after the March supply shock hurt all export-based economies in APAC. The regional outlier remains JPY, and its weakness is now at a point where pass-through will become increasingly prominent, even if there are minimal changes elsewhere. Governor Kazuo Ueda’s comments and the vote split at the April Bank of Japan meeting suggest that unease is growing, but the gap between JPY’s REER and the rest of the region is already too wide. CNY’s performance will add to global inflation, but it will be felt unevenly.