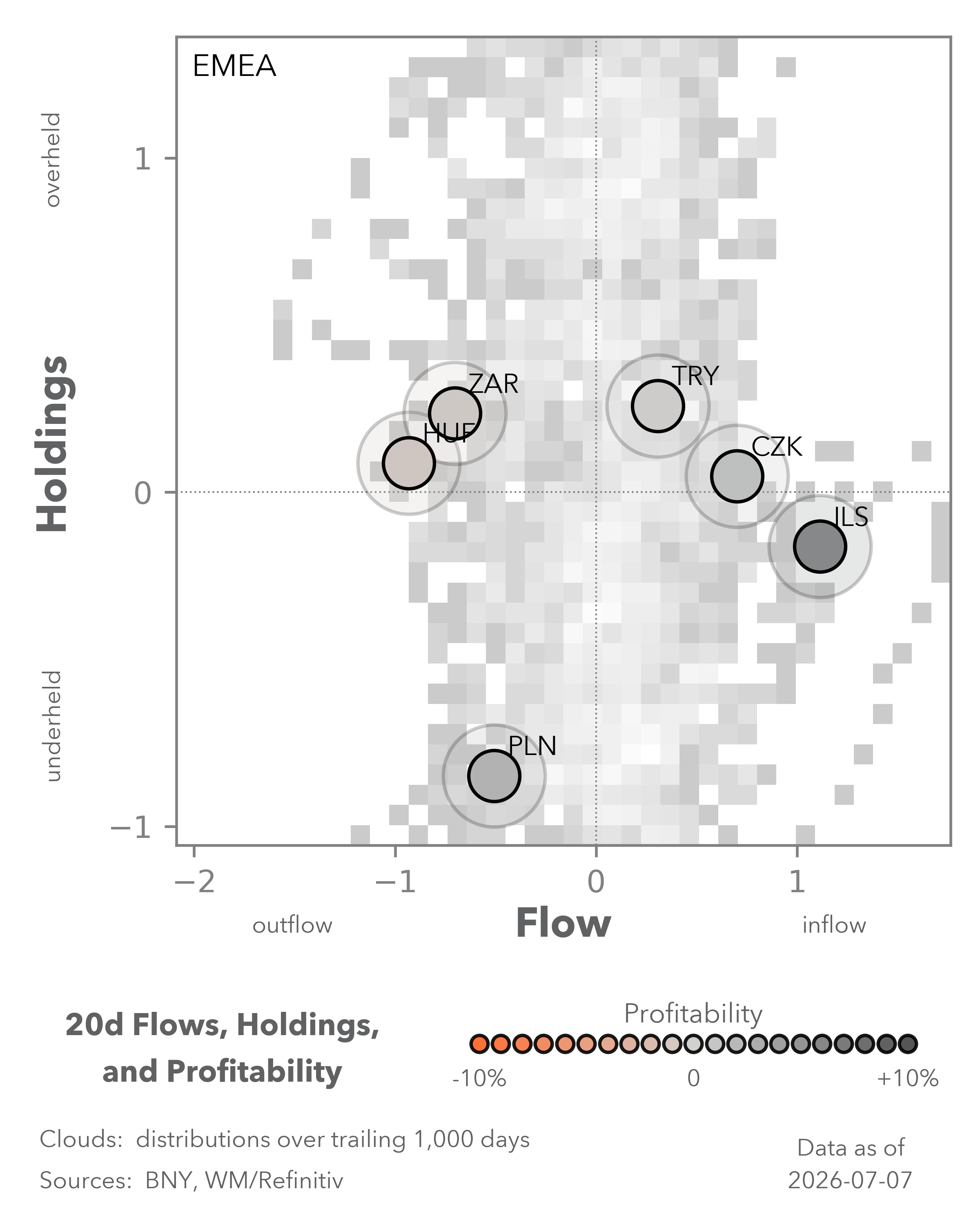

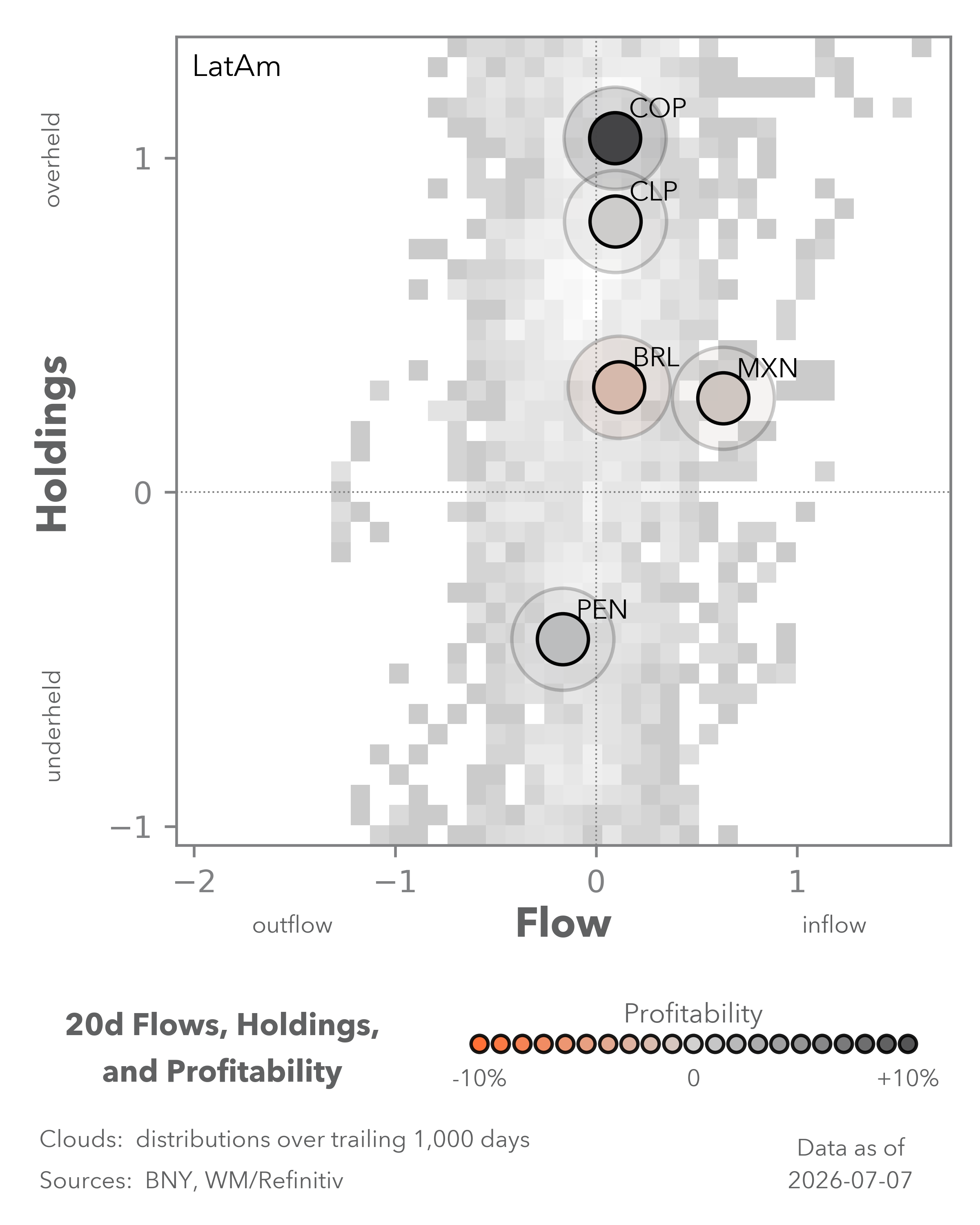

Bad hikes, good cuts

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

Currencies are taking their cues from growth, not just rates. Select carry trades are still performing, and hedging costs remain important for asset allocation. But if monetary policy is seen as suboptimal for the economy’s needs, asset inflows are likely to be weak in the first place. Conventional relationships between monetary policy and currency performance are breaking down, especially in Europe. Policy U-turns are hard to sell but we can’t rule them out.

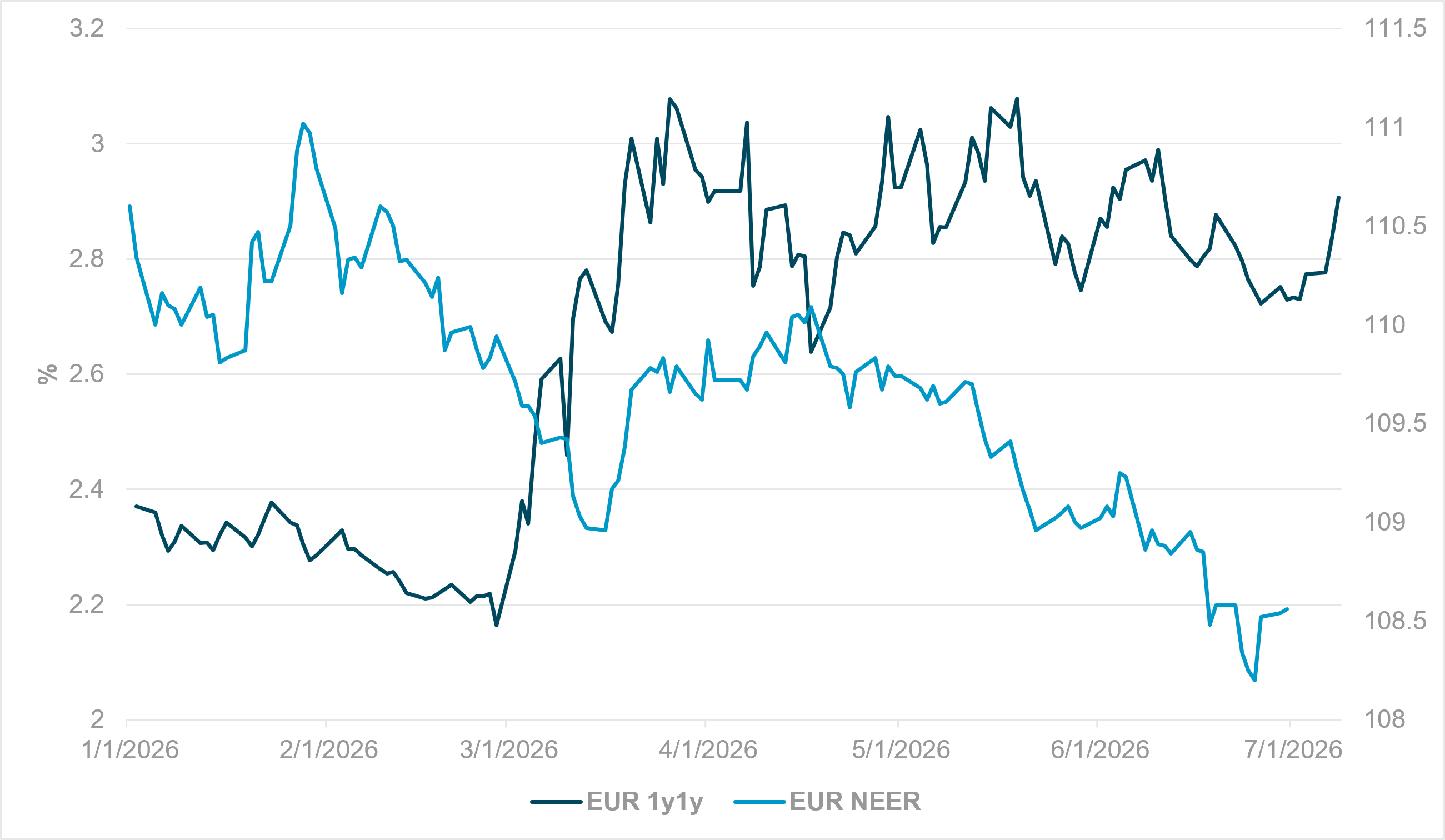

EXHIBIT #1: EUR 1Y1Y VS. EUR NOMINAL EFFECTIVE EXCHANGE RATE (NEER)

Source: BNY, Bloomberg, BIS

Our take

Right on cue, hawkish European Central Bank (ECB) members are sending clear policy warnings around the fragility of the U.S.–Iran ceasefire and supply risks through the Strait of Hormuz. Even though energy markets remain well below the highs seen in March and April, Bundesbank President Joachim Nagel warned that, after the latest news, the ECB was “back where we began.” The market is back to pricing in two 25bp hikes by year end. However, there’s little evidence from the move in inflation breakevens to justify that equivalence. If the ECB hikes further, real rates may rise, but we believe this would only further damage the EUR’s growth case.

Forward Look

The more the ECB leans into bad hikes, the more EUR risks becoming the funding leg for better growth stories elsewhere. The EUR has performed very poorly since the beginning of the ceasefire because there’s no growth-based justification for asset allocation. Europe can benefit from global rotation away from concentrated AI themes, but this will be hard to sustain without stronger domestic demand, especially given the structural downturn in European industrial performance. Higher rates would restrain demand further, particularly through the critical fiscal channel.

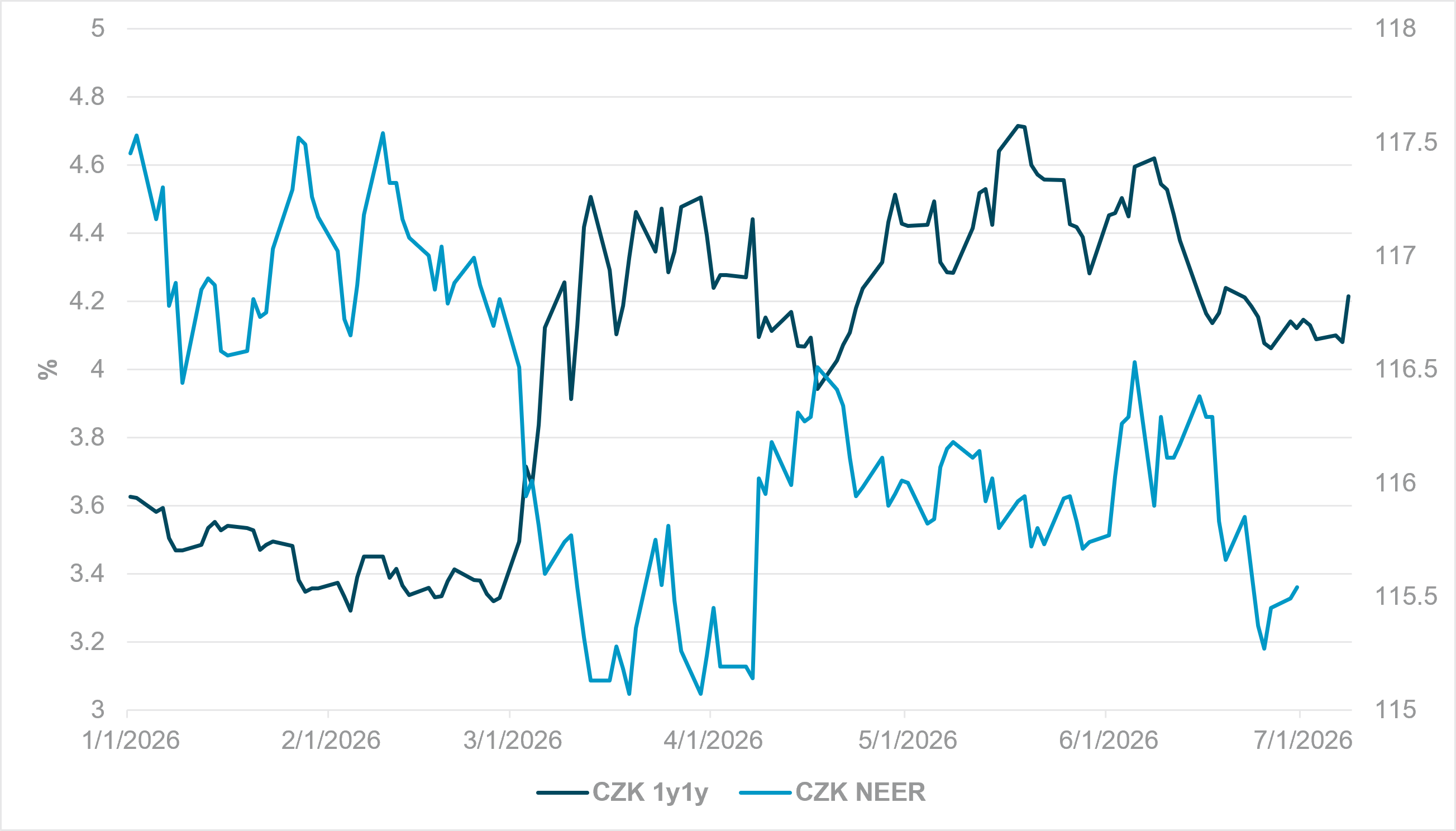

EXHIBIT #2: CZK 1Y1Y VS. CZK NEER

Source: BNY, Bloomberg, BIS

Our take

Smaller European economies integrated into the Eurozone supply chain often must move in line with the ECB. But aligning the domestic economy with sub-optimal policy, with or without a currency board, is also risky. The market has pushed up the Czech National Bank’s expected policy path as well, yet on a nominal effective exchange rate (NEER) basis, CZK is drifting back toward the lows of the year. While it’s easy to blame the recent fall in inflation for turning policy expectations around, the sharp rise in policy pricing in May did not help the currency either.

Forward Look

The CNB may need a clean break with the ECB. The industrial links between Czechia and the Eurozone mean that if current ECB policy is hurting growth, the Czech economy is unlikely to perform well. Matching the ECB may even amplify the adverse effect. If the export channel is structurally weaker, domestic stimulus should be considered. Czechia has rightly prided itself on avoiding some of the fiscal excesses seen elsewhere in Central and Eastern Europe. In a growth-focused market, credible stimulus may now be rewarded, as much as German assets repriced materially in 2025, with a meaningful benefit for the EUR.

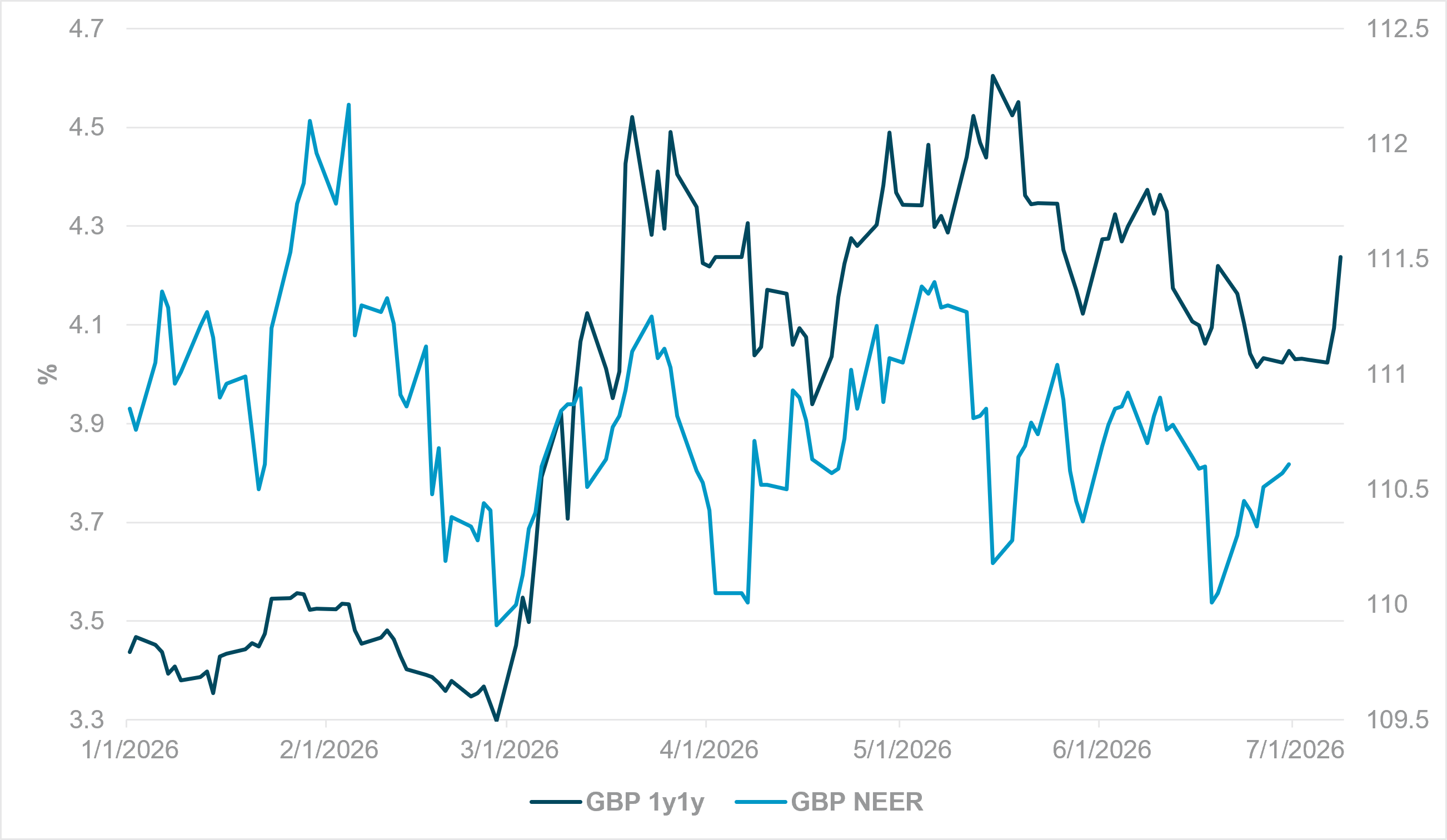

EXHIBIT #3: GBP 1Y1Y VS. GBP NEER

Source: BNY, Bloomberg, BIS

Our take

In the U.K. and GBP’s case, whether rates are the dominant driver is questionable, given the volume of political noise still weighing on the economy. Bank of England (BOE) Governor Andrew Bailey has credited market rate moves with “doing the tightening for the BOE” and appears clearly skeptical of using further hikes to address a supply shock. Compared with the ECB, we believe the BOE’s flexibility around its price stability mandate is a deliberate choice that isn’t currently damaging the currency.

Forward look

The Monetary Policy Committee can’t fix the U.K.’s structural issues, but it can avoid making them worse. Asset allocation to the U.K.’s equity market differs greatly from the Eurozone due to global exposures. Energy-driven supply shocks could even prove beneficial to GBP on the margins. Gilt yields also matter, but our flow data show that domestic purchases have been highly consistent due to positive real rates. It’s the international component that’s currently limiting GBP’s potential, mostly due to concerns over potential growth and politics.

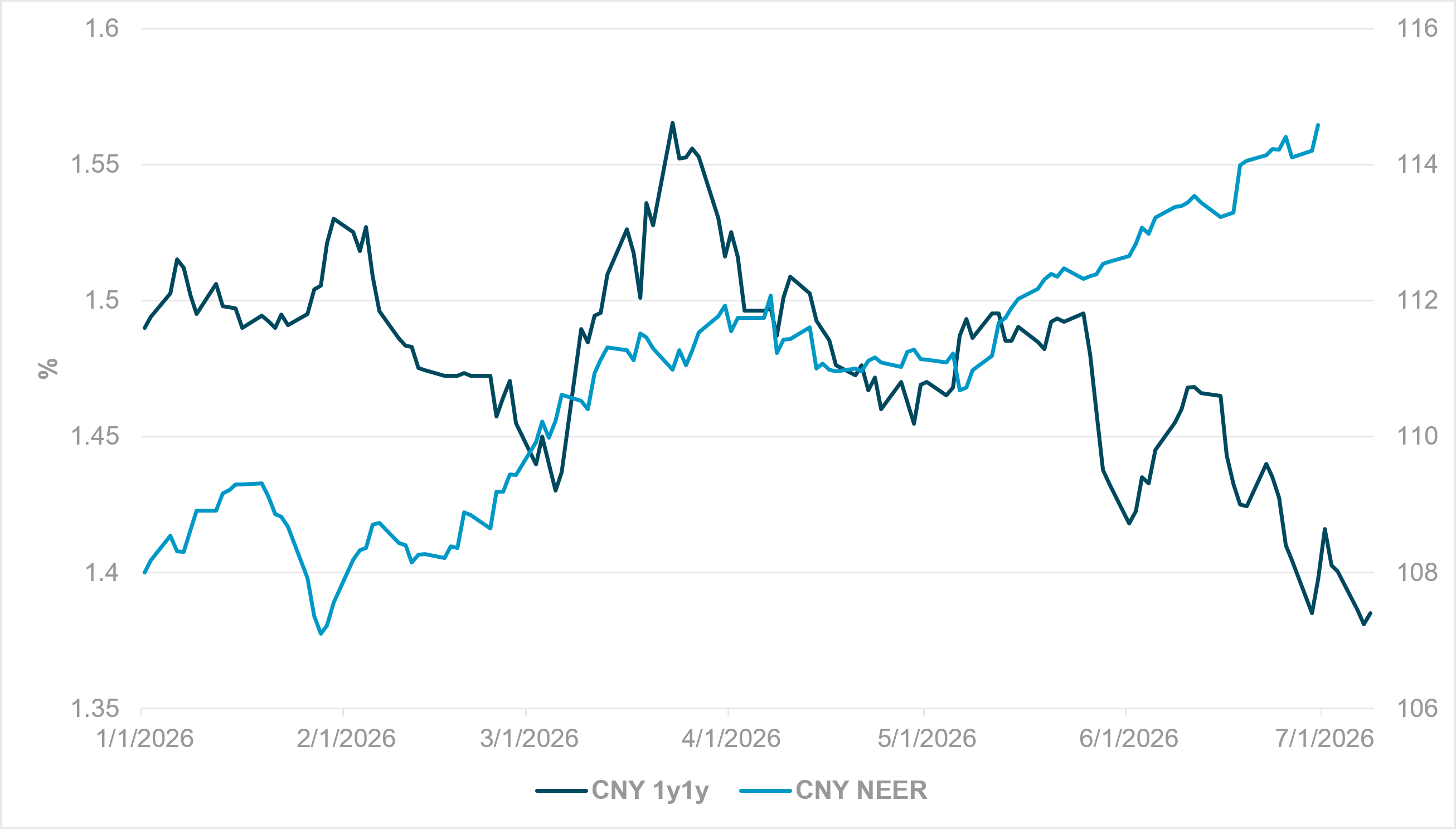

EXHIBIT #4: CNY 1Y1Y VS. CNY NEER

Source: BNY, Bloomberg, BIS

Our take

The People’s Bank of China’s (PBOC) introduction of a new benchmark overnight rate marks a further step toward international monetary policy standards and makes comparisons with G10 peers easier. CNY’s inverse relationship with the current rate path is perhaps the strongest among the world’s major economies. The conflict has not generated an inflation impulse; consensus still expects another poor year of price growth, and therefore weak corporate profitability, without clearer policy action. Yesterday’s PBOC Monetary Policy Report explicitly pledged “accommodative and flexible” policy ahead.

Forward look

If good cuts become credible reflation, CNY can strengthen further. Given China’s FX framework, allowing CNY to appreciate is also a policy choice, even if it may run counter to price objectives. But this week’s rotational flows into China point to an undervalued and under-owned growth narrative. Investors have little doubt that China can engineer stronger growth and reflation through stimulus and administrative measures if policymakers choose to do so. Equity rotation is already reflecting these upside risks.

If the supply shock is deemed transitory, add exposure to economies where monetary policy is improving the structural case for allocation. Bad hikes are failing to save EUR and CZK, GBP is showing greater indifference to rates, and good cuts are helping CNY. Outside very high-yielding names with commodity or inflation premia, the FX winner is not who pays the most; it’s where policy fits the economy.