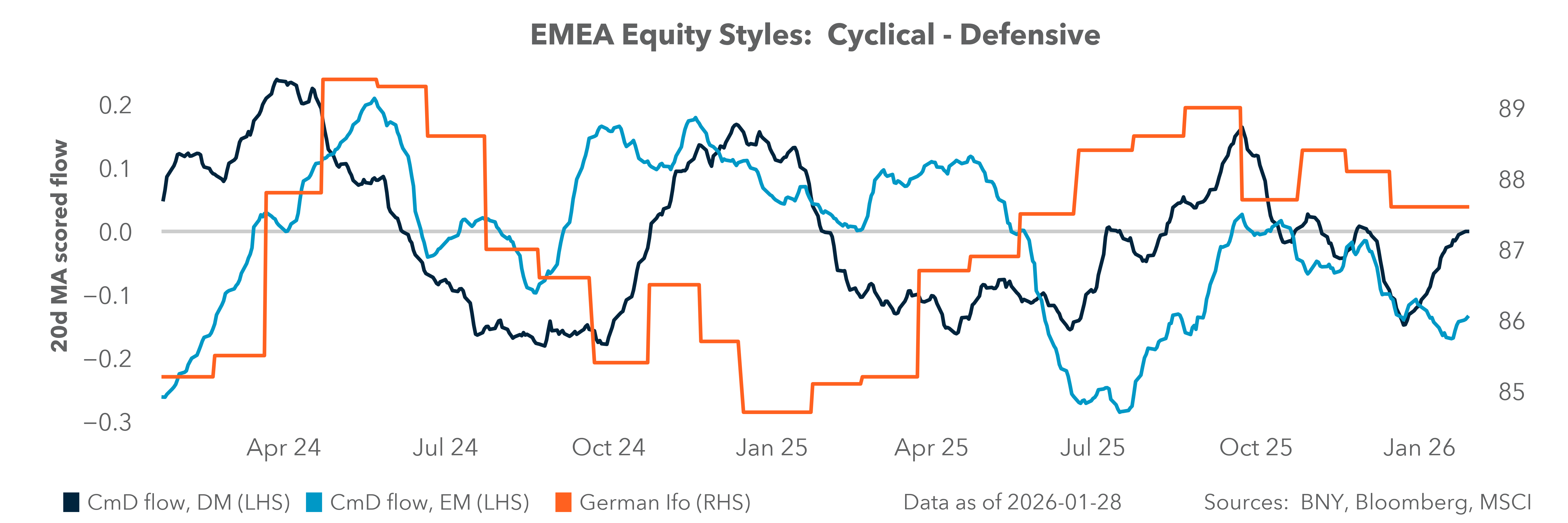

What if the USD adds to volatility?

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

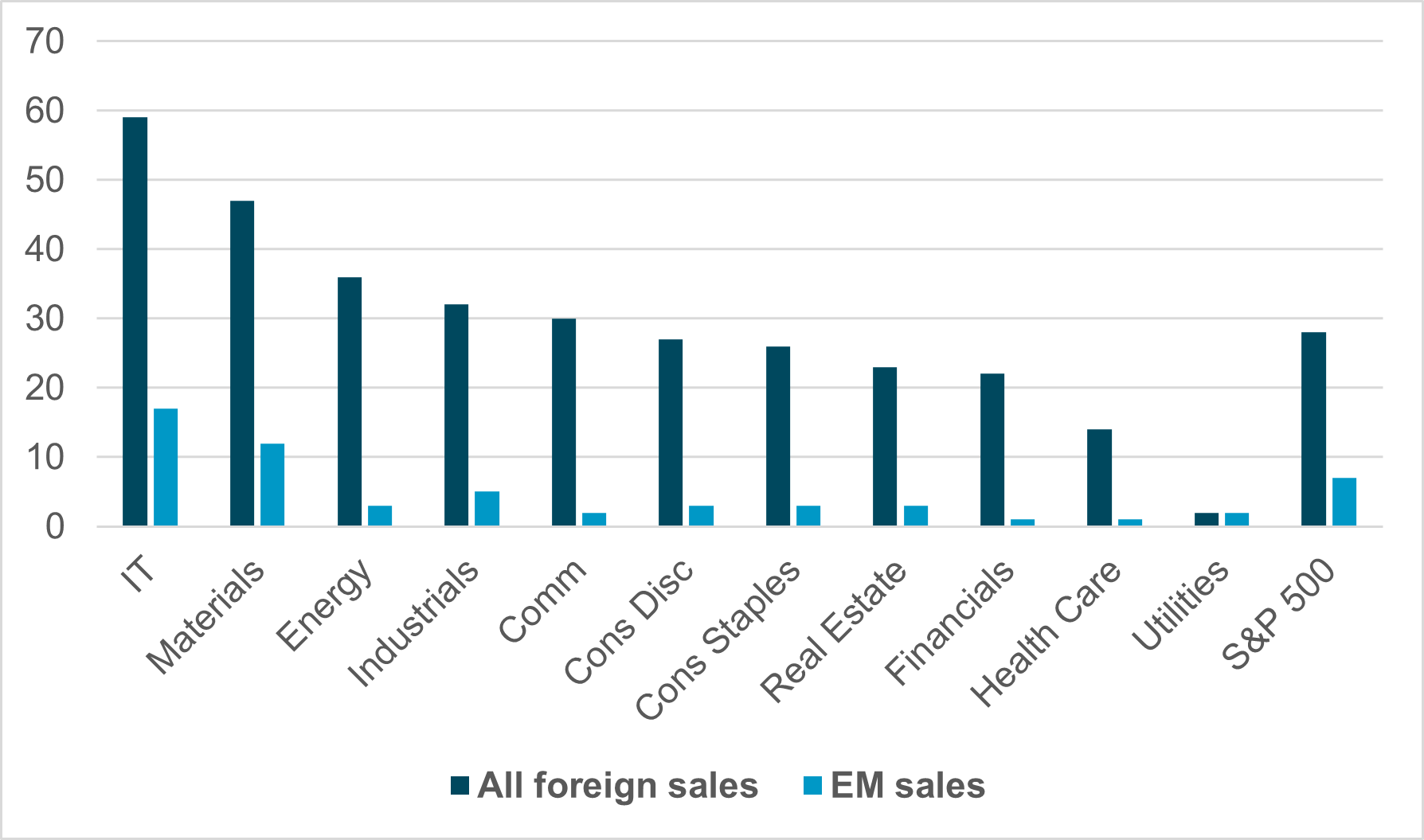

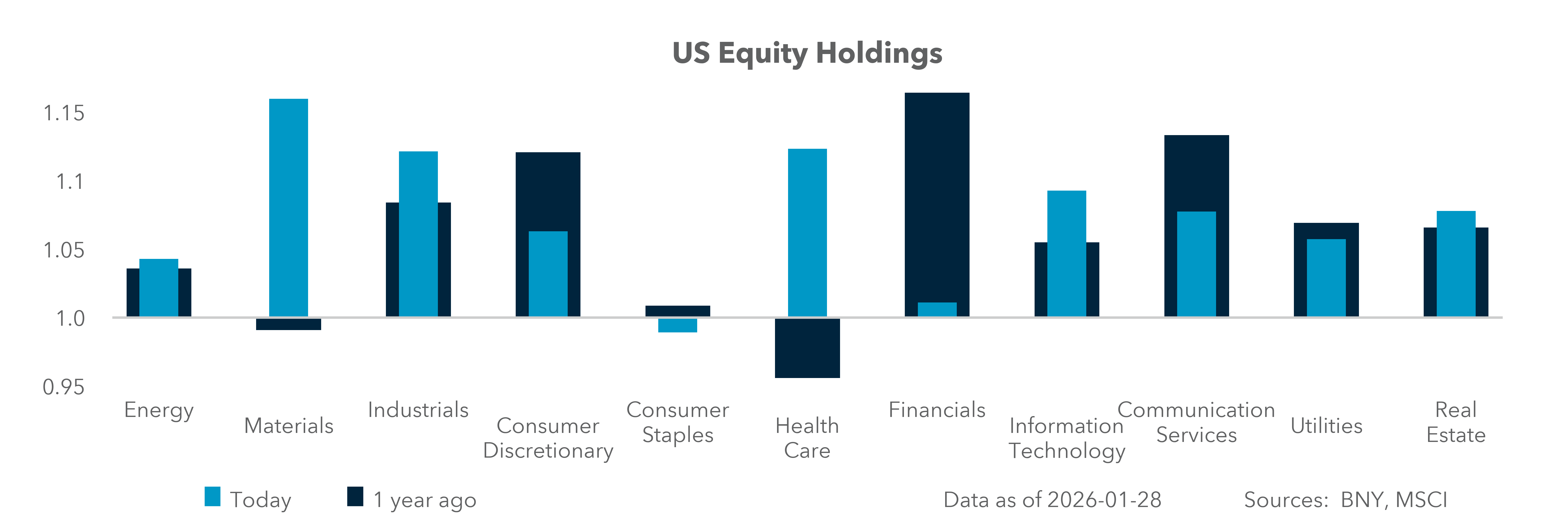

EXHIBIT #1: U.S. SECTOR EXPOSURE TO FOREIGN SALES

Source: BNY, Bloomberg

The U.S. dollar has quietly reasserted itself as one of the most important variables shaping equity returns. While inflation and rates dominated investor attention over the past cycle, recent market behavior suggests that currency dynamics – particularly USD weakness – are increasingly central to understanding sector leadership within the S&P 500.

A weaker dollar alters future earnings, shifts global competitiveness, and redirects capital flows across regions and asset classes. For equity investors, the implications extend beyond simple export exposure. FX movements are increasingly intertwined with evolving supply chains, technology leadership, and the use of sector allocations as implicit currency hedges. Geopolitical risks are now embedded in the dollar, the denominator of global returns. As the dollar’s long-term correlations with equities, breakeven inflation and alternatives like gold grow stronger, understanding how FX functions as both a shock absorber and volatility driver is critical.

This framework explains recent rotations across U.S. sectors and global markets – and suggests where relative returns may emerge next.

Our take

A weaker USD should benefit sectors that make money abroad. Last year, the 9% dollar decline clearly supported IT earnings. This year, after a 2% decline in January, the USD’s largest losses have been against EM currencies, benefiting IT and Materials. The rise in EM equities reflects improving export returns – stronger EM FX means greater costs for U.S. importers. AI and materials supply chains are directly linked to the FX shock absorber function. What matters to the S&P 500 is that the USD correlation is negative – the 10-year monthly correlation stands at –0.31, while breakeven inflation swaps correlate at 0.55.

The inflation impact of a weaker USD is becoming more important.

Forward look

The volatility of the USD – and what it does to underlying stock returns – is back in focus for investors and reinforces the negative feedback loop around USD hedging. Cross-border investors increasingly favor U.S. sectors exposed to a weaker USD, partly due to risk. We also note that USD losses in Q4 stalled. This raises the real risk of disappointment, particularly for sectors hit by lower offshore demand and profits.

Most importantly, USD weakness alters sector relationships as the U.S. economy evolves. Consider the shift since 1998: U.S. exports moved from industrial goods to tech-driven services, changing the USD’s impact on Industrials. Sector leadership rotation takes time and reflects the reality of a shifting economy.

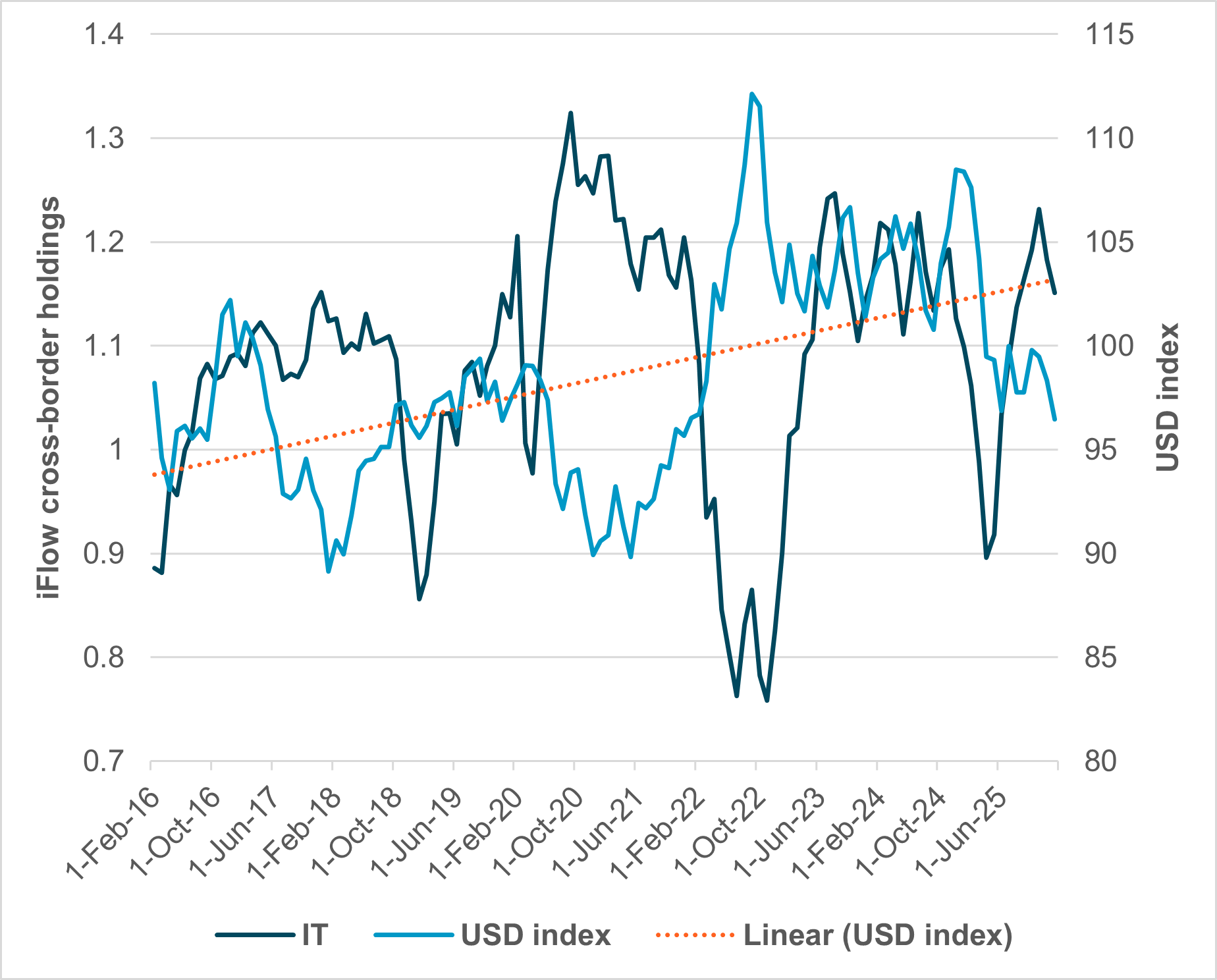

EXHIBIT #2: USD INDEX AGAINST CROSS-BORDER U.S. IT HOLDINGS

Source: BNY, Bloomberg

Our take

The relationship between the USD and foreign holdings of U.S. technology has been negatively correlated for most of the past decade. Current USD weakness will test whether the relationship is causal. Fears of a “sell America” trade surfaced in January but remain unconfirmed in USD or technology holdings. The link between inflation and margin pressure in domestic sectors, such as Utilities and Health Care, suggest global investors are watching to see whether a weaker USD sparks higher input costs.

Forward look

USD value remained stable from 2021 to 2024. The 2025 break from a 110–100 range to 100–90 is significant and likely to increase USD hedging, prompting a reassessment of how sectors benefit from dollar weakness. The recent move lower brings the USD back to levels last seen during the first Trump administration. At that time, Financials and Technology had similar market capitalizations. The dollar’s breaking trend is now influencing asset allocation both at home and abroad. Current U.S. rotation from big tech to small caps reflects a home bias, and Materials have been the one sector seeing the clearest rotation out of Tech. Meanwhile, rising EM holdings over DM suggest investors are positioning for USD weakness.

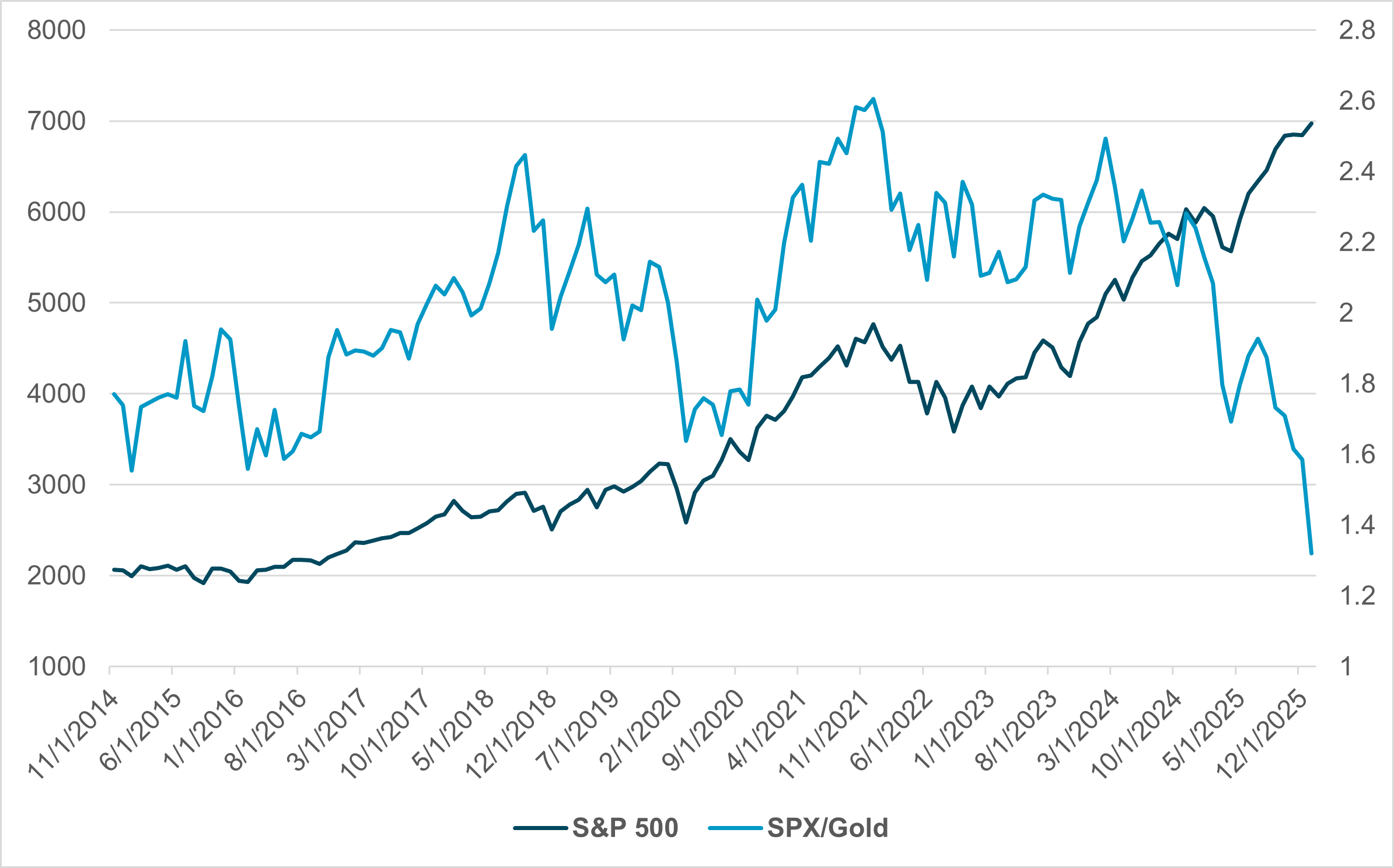

EXHIBIT #3: S&P 500 AND S&P 500 DENOMINATED IN GOLD

Source: BNY, Bloomberg

Our take

The best way to understand the USD’s significance is by comparing it to alternatives. Since November 2024, diversification away from the dollar, especially into gold, has become more pronounced. When returns are normalized in gold terms, interesting comparisons emerge. From November 2024 to present, South Korea’s KOSPI outperformed gold by 9%. In contrast, Japan’s Nikkei is down 56%, the Euro Stoxx 50 by 70%, and the S&P 500 by 75%. S&P 500 returns, measured in gold, are now below both 2014 and COVID-era lows.

Forward look

The role of the USD in driving diversification is not the whole story. When equities are measured in WTI, global performance looks stronger. WTI crude prices has declined –12.5% since November 2024. Bitcoin, another alternative, is up 28% since November 2024, outperforming both the S&P 500 and Euro Stoxx 50. Inflation-adjusted returns are also in focus, especially given the influence of breakeven inflation swaps on equity performance. Headline U.S. CPI was 2.75% in November 2024 and is now 2.70%, underscoring that the concern for the S&P 500 lies more with the dollar and other fiat currencies than with inflation.

The move up in gold reflects larger concerns than just inflation. The USD’s evolving role in payments, trade and global asset pricing must be evaluated against other global opportunities.

The central question for equity investors is no longer if the dollar matters, but how it reshapes relative returns across sectors, regions and asset classes. USD weakness has historically supported globally exposed S&P 500 sectors, particularly Technology and Materials, yet its impact evolves as the U.S. economy shifts from goods-based exports toward services and intellectual property. At the same time, global investors are increasingly sensitive to FX risk, using sector exposure, EM allocations and alternatives such as gold to reduce dollar dependence. The reaction of central bankers to such flows is also critical. The dollar’s recent range break introduces both opportunity and risk, particularly for sectors reliant on offshore demand, stable interest rates and modest volatility. Importantly, the dollar’s role now competes with inflation as a primary driver of equity performance. For portfolio construction, FX must be treated not as a macro afterthought, but as a structural force shaping equity leadership in an evolving global economy.