Rotations, Value and Retail

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

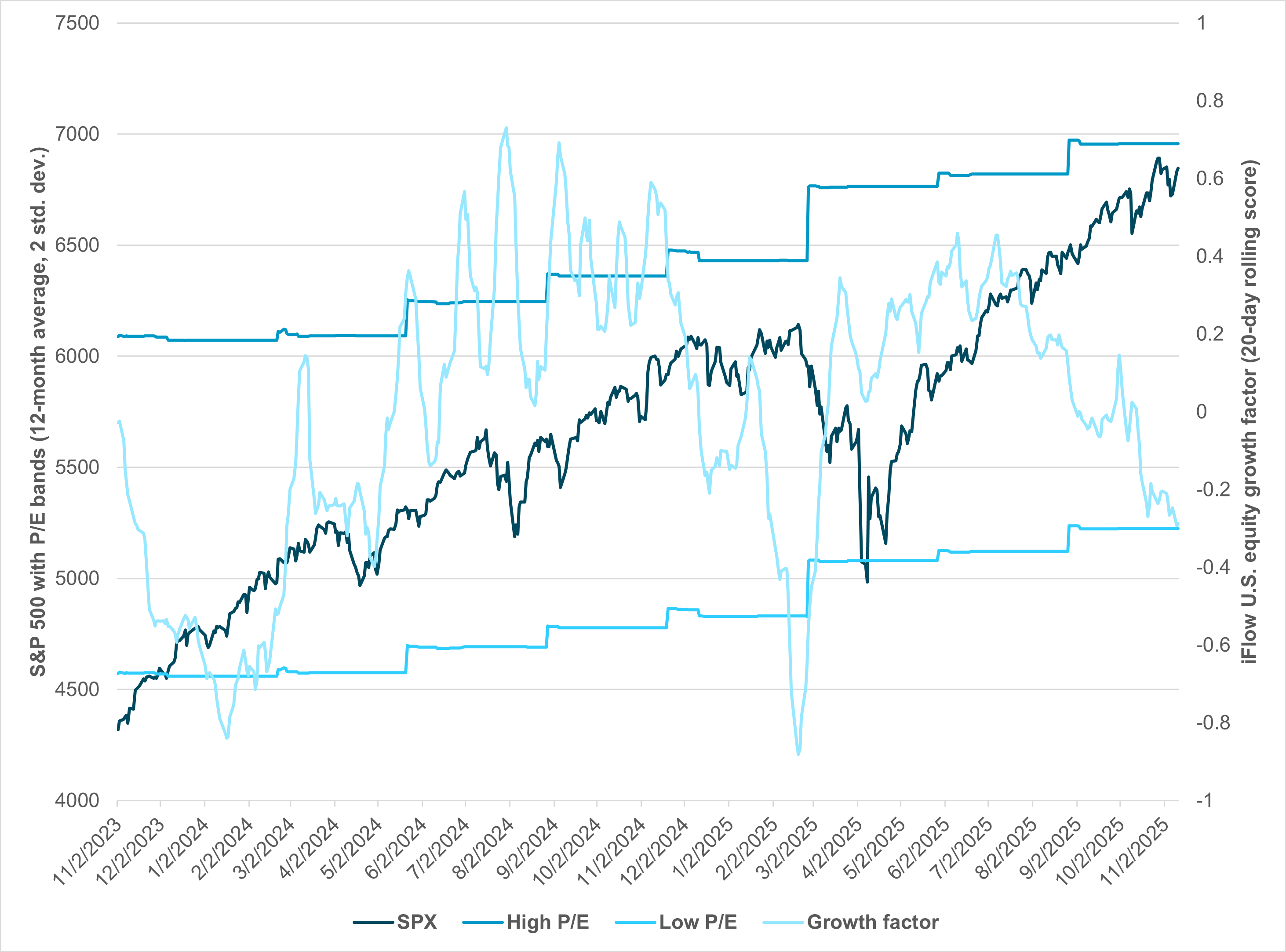

EXHIBIT #1: S&P 500 VALUATIONS VS. IFLOW GROWTH FACTOR FLOWS

Source: BNY, Bloomberg

Equity markets are entering a critical inflection point defined by valuation fatigue, rotation risk and macro-data dependence. Expensive global equity multiples, especially in U.S. tech and AI-linked names, are prompting reallocations toward cyclical and defensive sectors. This rotation reflects a nuanced investor shift from growth optimism to margin and rate sensitivity, with upcoming employment and consumer price index (CPI) data poised to reset Federal Open Market Committee (FOMC) expectations and the equity risk premium.

Elevated leverage across both retail and hedge fund segments amplifies the risk of sharper drawdowns should the macro data disappoint. The Nvidia earnings report on Nov. 19 will be another key event. Heading into year end, positioning for policy clarity and monitoring defensive sector leadership will be crucial to navigating potential volatility and identifying tactical re-entry points.

Our take

Markets are expensive, both in the U.S. and globally: This is the third year of double-digit returns for the S&P 500. The rally leader continues to be technology, specifically AI-linked companies. The last two weeks have tested this with a notable rotation out of technology shares in less-held sectors like energy, industrials and utilities.

The price action of the Dow Jones Industrial Average printing new highs and the Nasdaq down on the week suggests a clear shift in investor thinking. Exhibit #1 highlights the rally back in risk from April to now, with price-to-earnings bands of the S&P 500 based on two standard deviations from the rolling two-year average. The worry about value is clear and has capped the November rally, but the more interesting break is with growth as a factor for stock investors. The July peak in this factor suggests that rate cuts and margins are more important to flow right now.

Forward look

The selling of growth as a key factor in U.S. shares suggests investors are more biased toward leverage than growth. Worries about Q3 earnings emphasized margins and revenue, with fears of a U.S. slowdown. Traditionally, investors buy growth and value in an economic slowdown, but the current trajectory suggests something different – concerns about value are not linked to the economy, but to something else. iFlow data show ongoing home bias, where U.S. investors focus on U.S. assets, while EMEA and APAC investors start with their own markets.

The role of rates will be key for growth to return as a factor, with December releases of unemployment and CPI critical for the FOMC decision and for how investors rethink the equity risk premium. The current 10y U.S. bond yield near 4.10% is far from the 6.2% high in late 1999, when similar technology bubble worries dominated. The difference between then and now is the deflationary impact of globalization and the post-financial-crisis low-rate regime, which changes future bond yield expectations, and with them value metrics.

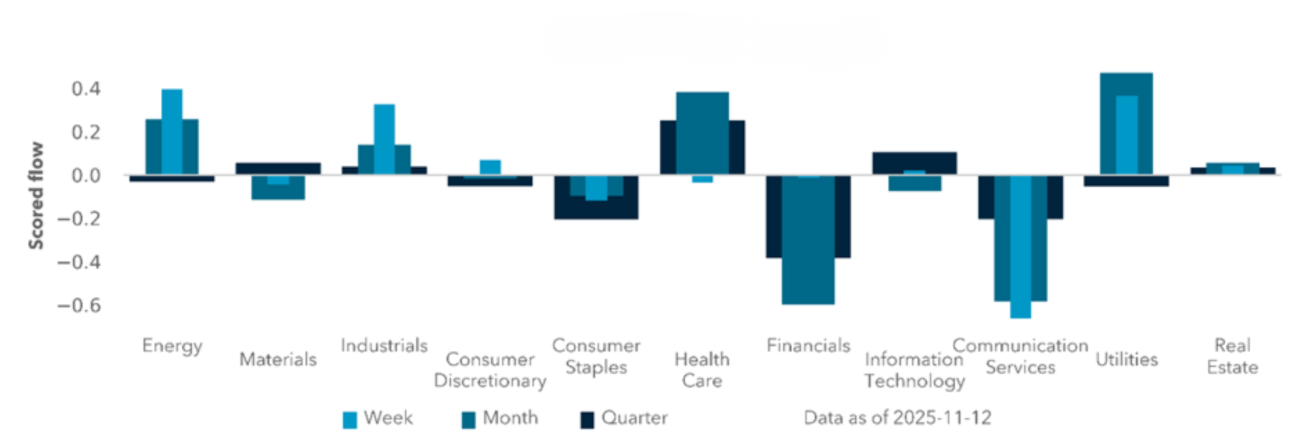

EXHIBIT #2: CURRENT INVESTOR FLOWS ACROSS U.S. EQUITY SECTORS

Source: BNY, MSCI

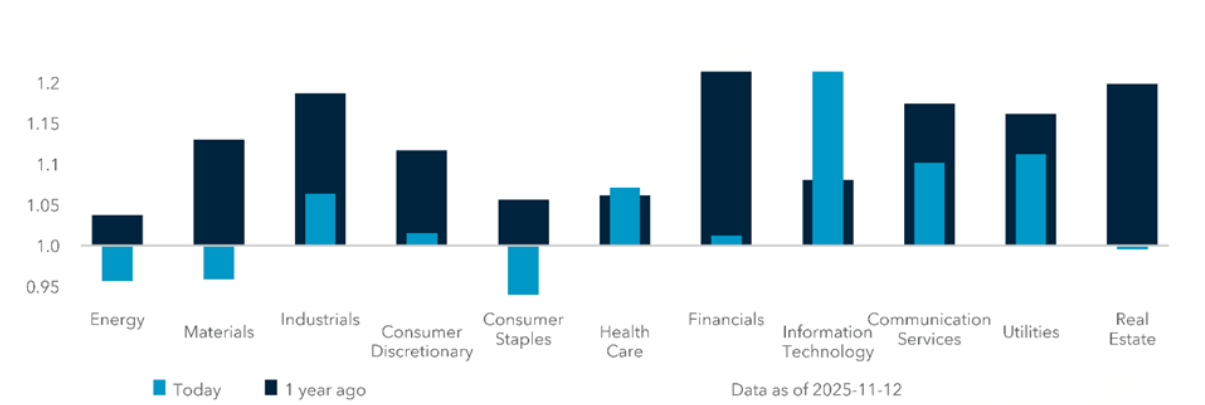

EXHIBIT #3: U.S. EQUITY HOLDINGS BY SECTOR VS. 2024

Source: BNY, MSCI

Our take

The current selling of technology, communications and financial sectors stands out over the last week. Technology, particularly hyperscalers, has dominated the press with notable concerns about investments in AI being funded by investment-grade issuance rather than cash. Further concerns about the extent to which OpenAI investments are intertwined with the semiconductor sector and the Magnificent 7 add to pressure to reduce overweight holdings. U.S. technology remains 15% overheld against the three-year average in iFlow. The interesting point about flows in Exhibit #2 is that selling in communications and financials is from a low base, with both sectors far below 2024 holding levels and just below the three-year average.

Forward look

The key risk for investors into year end comes from the FOMC decision and jobs and inflation data. The risk of the current rotation trade out of IT and communications continuing until then seems high, but after that, the focus will shift. Watching the health care and utility sectors is the best way to measure the difference between corrections of 5–10% versus tactical rotations in sector leadership.

EXHIBIT #4: ETF FLOWS VS. EQUITY HEDGE FUND INDEX

Source: BNY, Bloomberg

Our take

Retail flows from iFlow track broader ETF flows seen in markets across most periods. However, the current risk aversion in our retail flows stands out compared to overall equity ETF moves in October. May was the last notable pullback in ETF flows. That matched our retail story, with both bouncing back over the summer. Steady hedge fund returns and retail’s success in buying dips makes clear that both groups have incentives to hold their gains into year end. November ETF data aren't clear yet, but early signs point to significantly weaker inflows. The notable drop for equity inflows may continue. However, September data releases and potentially the October jobs reports in the next two weeks are likely to derail current de-risking trends and test the “buy-the-dip” wisdom of retail. Hedge funds tell a different story. With overall returns flat until the April rally, their strategies appear less inclined to participate now. past month.

Forward look

A larger U.S. stock market rotation may be underway. Valuations in the IT sector are stretched but seen as justified given strong margins and earnings growth. The top 10 companies in the S&P 500 now represent 40% of total market capitalization, suggesting significant concentration risks. Investors are overweight IT and underweight Financials. In past bubbles, 1999 centered on Technology, while 2008 centered on Financials. Expectations for rates and growth are at odds with current portfolio positioning. Risk that the Fed delivers less, inflation remains sticky, or growth proves stronger may drive a Q4 broadening of risk across other sectors.

The near-term equity landscape is more exposed to “melt-up dynamics” than to traditional correction risk, with positioning and sentiment already defensive. Sector rotations driven by valuation dispersion are likely to persist, reinforcing uneven market breadth until clearer policy and macro signals emerge. Nvidia earnings next week will serve as a key inflection point for technology leadership and broader market tone. Institutional investors have already shifted positions defensively, while retail and hedge fund liquidity constraints limit incremental buying power.

A potential reacceleration in government activity and underlying economic momentum could tilt the balance toward a constructive December, particularly given underweight foreign participation in U.S. equities. Ultimately, navigating between recession fears and bubble narratives may define the next phase – a tempered continuation of the current advance or a bigger reversal.