LatAm asset allocation, AI and savings

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

After a week in the region, three themes stand out: how geopolitical flows are reshaping equity positioning, what pension reform means for domestic savings allocation, and whether the AI and data center buildout represents a genuine structural shift.

The week also delivered a clear signal: AI investment is ongoing and increasingly competitive. Nvidia’s earnings call points to a company shifting from pure growth to value. It raised its quarterly dividend from $0.01 to $0.25 and announced $80bn in buybacks, with $50bn earmarked for data center reinvestment. Earnings beat consensus but fell short of whisper numbers, suggesting upside is capped – supply constraints and war risk are doing their work.

For LatAm, AI’s near-term story is less about the tech sector than banking – a maturing population and rising fintech penetration are the real drivers. Chile and Brazil lead adoption; Colombia is catching up fast. However, flows over the last five months tell a different story: energy has dominated the safety-and-yield trade, ahead of metals and IT.

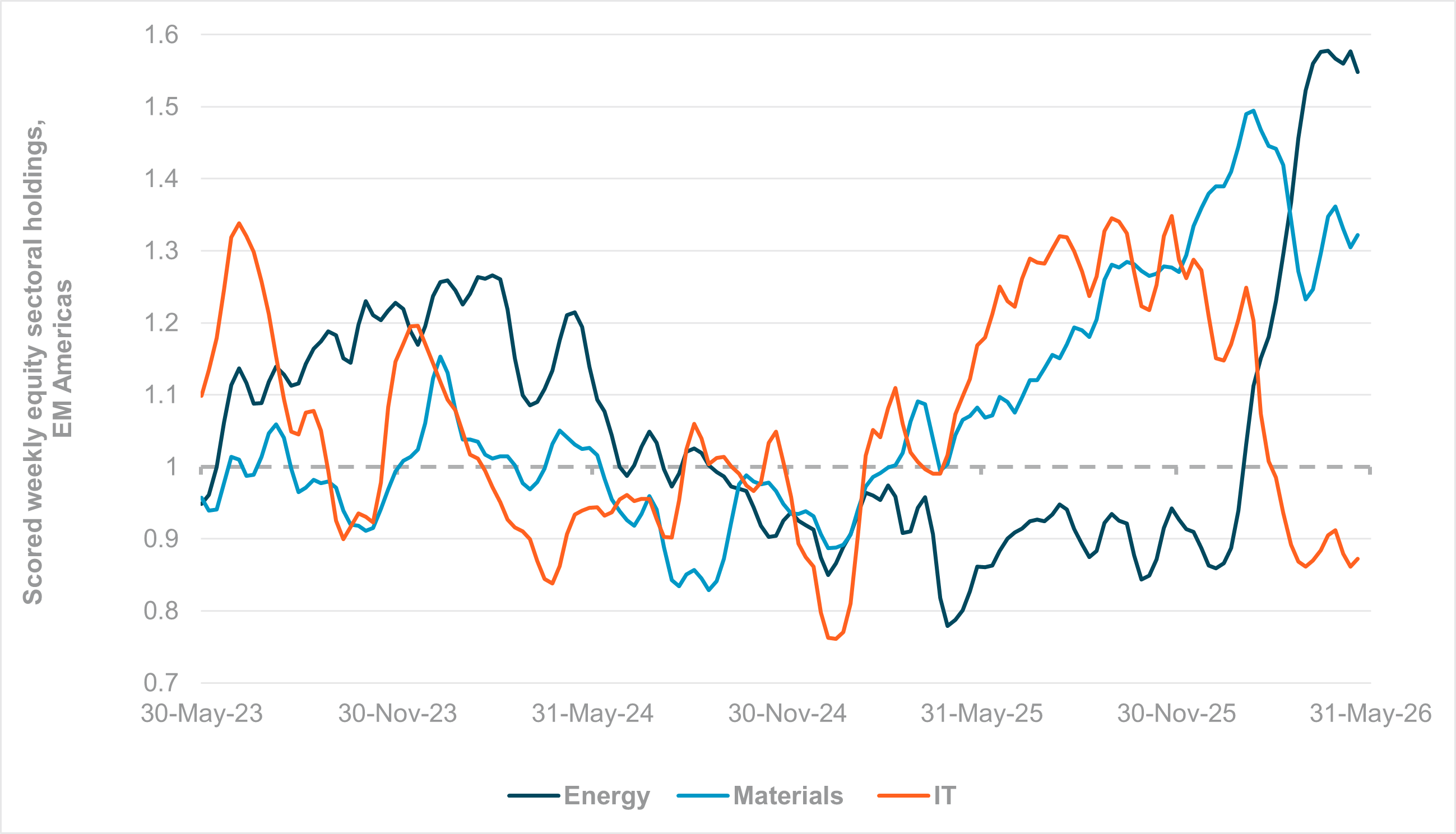

EXHIBIT #1: IFLOW WEEKLY HOLDINGS IN ENERGY, MATERIALS AND IT

Source: BNY

Our take

LatAm’s energy holdings spike started in January with the surprise U.S. action in Venezuela; it continues with the war in Iran. If peace talks lead to a sustainable deal to reopen the Strait of Hormuz, the risk for the region is in the unwind of energy as a safe-haven equity. Unlike the U.S. markets, where IT has held up against war inflation shocks, the LatAm region has seen a pullback in IT holdings. Materials have also suffered; copper, silver and other key metals peaked in early February and have retreated since.

Forward look

The spike in energy is notable – 50% over the three-year average in the span of five months. In comparison, materials are just 25% over the three-year average, while IT is 15% below. Markets are treating LatAm equities as a commodity hedge against war-driven supply shortages, even as real rates weigh on broader growth. Regional dynamics rest on demographics: the population is growing 0.6% y/y, and the average age is 31. Savings rates are rising, and urbanization is accelerating the shift from agriculture toward manufacturing and services. Banking, retail and education remain key growth industries, and AI will play a critical role in their profitability and productivity.

Chile and Brazil are driving the region’s data center expansion – from roughly 300 today to 400 by mid-2027. Beyond U.S. hyperscalers, the tech ecosystem pushing for this growth includes MercadoLibre, Globant, TOTVS, Nubank and Rappi. Cloud services are in demand, and fintech innovation is thriving across the region.

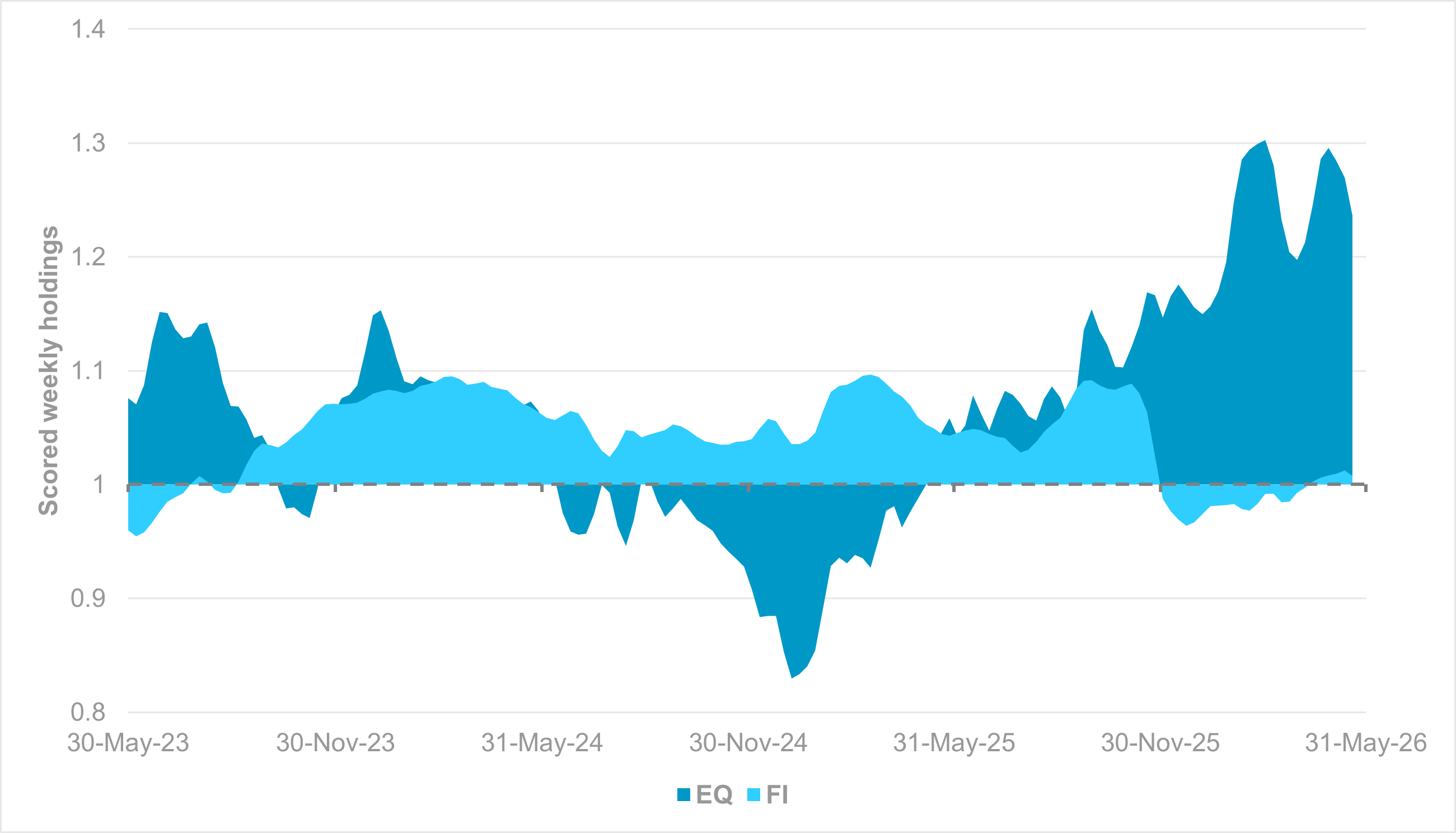

EXHIBIT #2: EM AMERICAS EQUITY AND SOVEREIGN BOND HOLDINGS

Source: BNY

Our take

LatAm bond holdings remain high but off September levels, when the FOMC was cutting U.S. rates and regional yields were at their widest spread relative to the rest of the world. Since the start of the U.S.–Iran war, bonds have seen modest inflows, but equities have led capital inflows – particularly energy and materials. Equity positioning looks stretched compared to the three- and five-year averages, while bonds are slightly underheld.

Forward look

Colombia’s “four pillar” pension system overhaul began in July 2025 with the enactment of a law replacing public/private competition with a unified state-run system. In the system’s core pillar for active workers, earnings up to 2.3 times the minimum wage are put entirely into a collective state-run fund. Earnings above the threshold are managed by private administrators.

The law has since prompted mandates across the region to shift private savings plans to state-run systems. Chile has passed a pension plan forcing a fiscal safety floor; the state fund (PGU) expands with a new 7% employer contribution. Over the last five years, both Peru and Chile saw a series of emergency acts allowing citizens to withdraw from their private savings to cushion economic hardships from Covid to the 2022 energy crisis. This left Chile’s AFP system holding 25% fewer assets. Peru saw a similar drawdown. The asset allocation between private and public funds has shifted and will continue to see significant volatility.

Money is being forced back home, pushing up equity investments and some bonds. Those withdrawals left a pro-cyclical fear factor for foreign investors, who remember the fire-sales in Peru and Chile. The net effect has been a rotation toward sovereign debt and away from corporate credit, constraining some growth sectors, while pushing private market capital offshore.

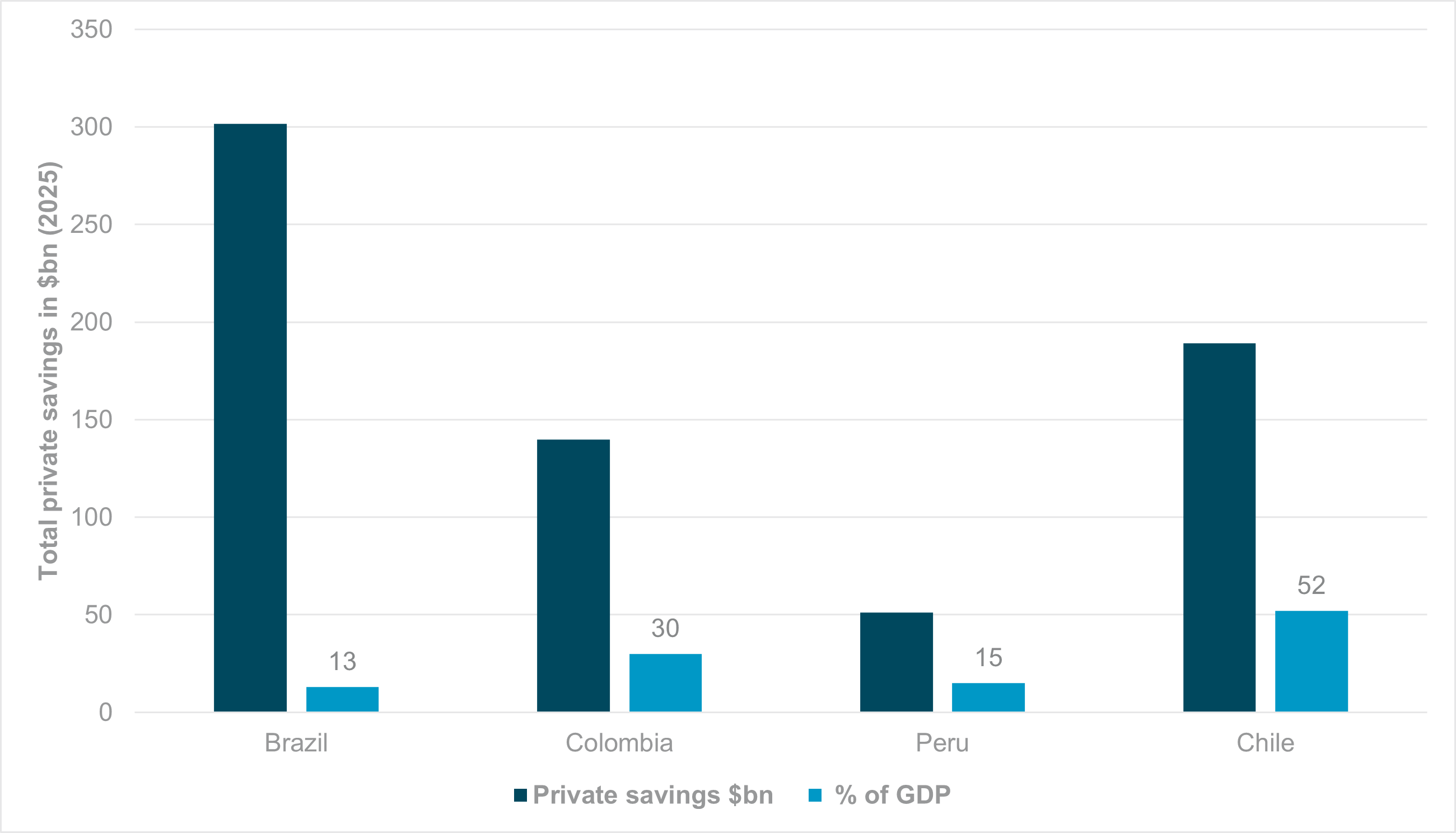

EXHIBIT #3: LATAM PRIVATE SAVINGS AS PERCENT OF GDP

Source: BNY, World Bank, Bloomberg

Our take

The savings drive in Colombia and Chile exceeds developed market averages, and reform in both nations adds to the focus on where the money will be invested over the next 5–10 years. Government-mandated asset allocation has caused some of the rise in regional equity holdings. Reform of the AFP system to target date funds will add to fixed income demands as well. Brazil and Peru show more modest savings rates, which makes government wealth funds and bank reserves the key buffer against cyclical downturns. Brazil holds $365bn in FX reserves, while Chile has $45bn – both are about 15% of their GDP. Across LatAm, there is over $1tn in public and private savings, making the region a significant investor to the U.S. and other countries.

Forward look

LatAm market capitalization is led by Brazil at $1tn, representing about 60% of GDP, while Chile is $270bn, reflecting 15% of GDP. Peru is at $75bn, 5% of GDP, and Colombia is at $65bn, 4.5% of GDP. The risk for pension reform and rising savings is the ceiling on how much can be productively invested at home before overvaluation sets in. That pressure to invest abroad also raises the case for proactive FX hedging policy.

Within that market cap, LatAm’s sector mix is heavily weighted toward financials, materials and energy. Financials account for 25%, materials 22% and energy 15%, with the remaining 38% spread across consumer, utilities and other sectors. The contrast with the U.S. – where IT and communications alone represent roughly 40% of market cap – reflects the different innovation profiles of the two markets. With IT at just 8% of market cap, LatAm’s technology sector has room to grow in the years ahead.

South America enters the next decade with a more balanced investment narrative than traditional commodity dependence alone. While energy and mining continue attracting flows during periods of geopolitical uncertainty, structural growth drivers are increasingly tied to domestic savings accumulation, pension reform, urbanization, and digital transformation. The expansion of private and sovereign savings pools across Brazil, Chile, Colombia, and Peru will gradually deepen local capital markets. Governments will need to balance domestic investment mandates against the risks of overvaluation and capital inefficiency.

At the same time, AI adoption across banking, retail, logistics, education and cloud services is accelerating, particularly in Brazil and Chile, where data center expansion is emerging as a major strategic investment theme. The region’s relatively young demographics, rising fintech penetration, and growing middle class support long-term productivity gains. LatAm is moving from a cyclical commodity allocation to a hybrid growth story, and the structural pieces are falling into place.