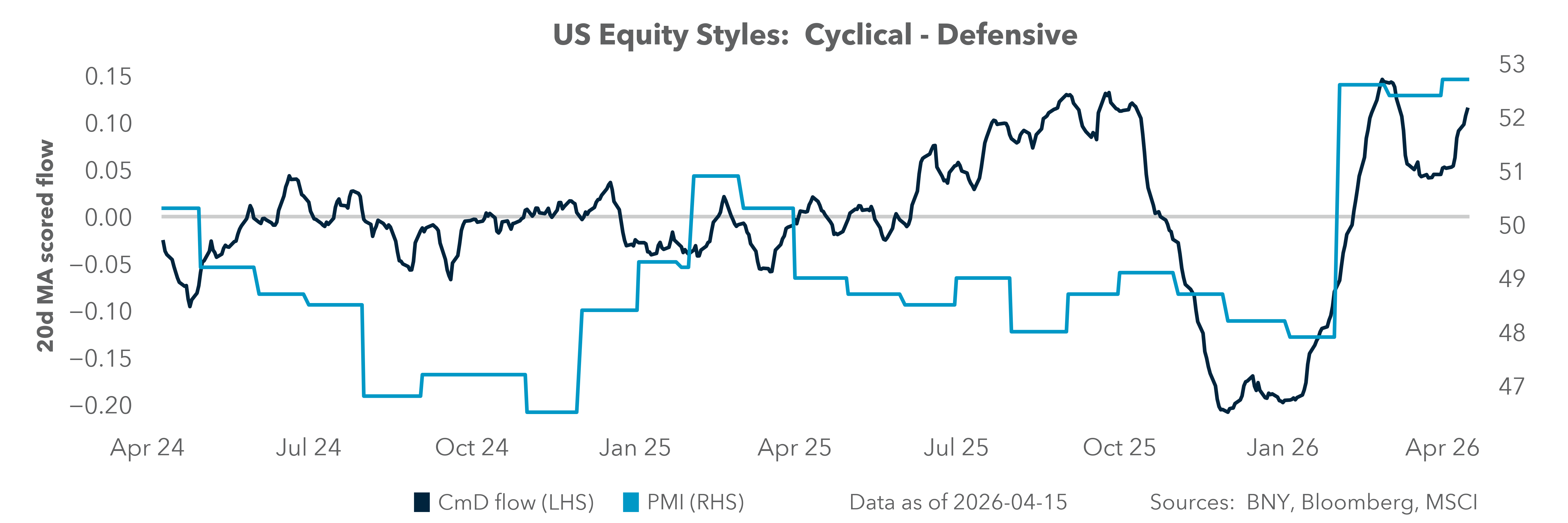

Correlated risk regime change

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

Q1 earnings started with a bang, with estimates for S&P 500 improving and whispers of 19% earnings, 16% margins in the U.S. Global equity markets are back to near-record levels, recovering most war-related losses. The surge in equity flows this week reflected both stronger earnings and hopes that the U.S.-Iran ceasefire would lead to a peace deal. The shift from missiles to words lifted risk-taking across asset classes, but the correlation of equities to USD, oil and bonds remains high, which is atypical during earnings season. The lack of divergence in risk-taking across assets makes equity allocation during earnings more complex.

We are in many ways restarting the year with some lessons from Q1 – namely fears stemming from uncertainty, unpredictability, and the prospect of future supply shocks. The cost of the war is not fully known, and in Europe, tax adjustments have mitigated energy costs, limiting overall inflation pass-through to consumers. In Asia, intervention has been more pronounced, with partial work weeks to conserve fuel and limited energy exports.

The EU’s fiscal costs are estimated at 0.6% of GDP; Asia’s are estimated at 1–2% of GDP. Bond markets have not fully priced in the cost of new fiscal spending or the inflationary effects of the supply shock. However, these factors have shifted monetary policy expectations from easing to tightening. Among developed market central banks, only the Fed is still seen as likely to ease, with markets pricing just a 40% chance of one cut by year end. Together, these factors cloud the risk-free rate anchor that underpins equity valuations.

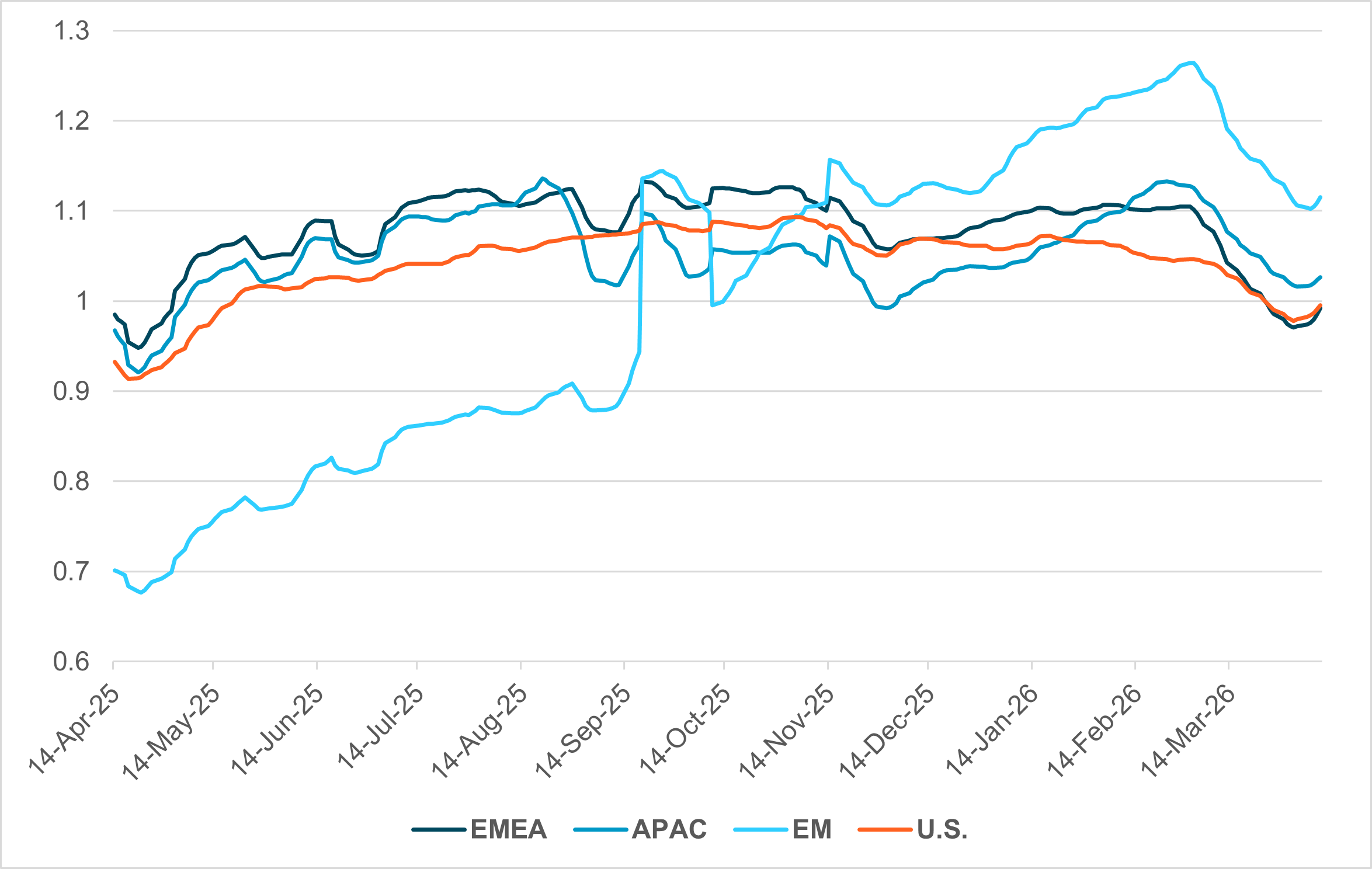

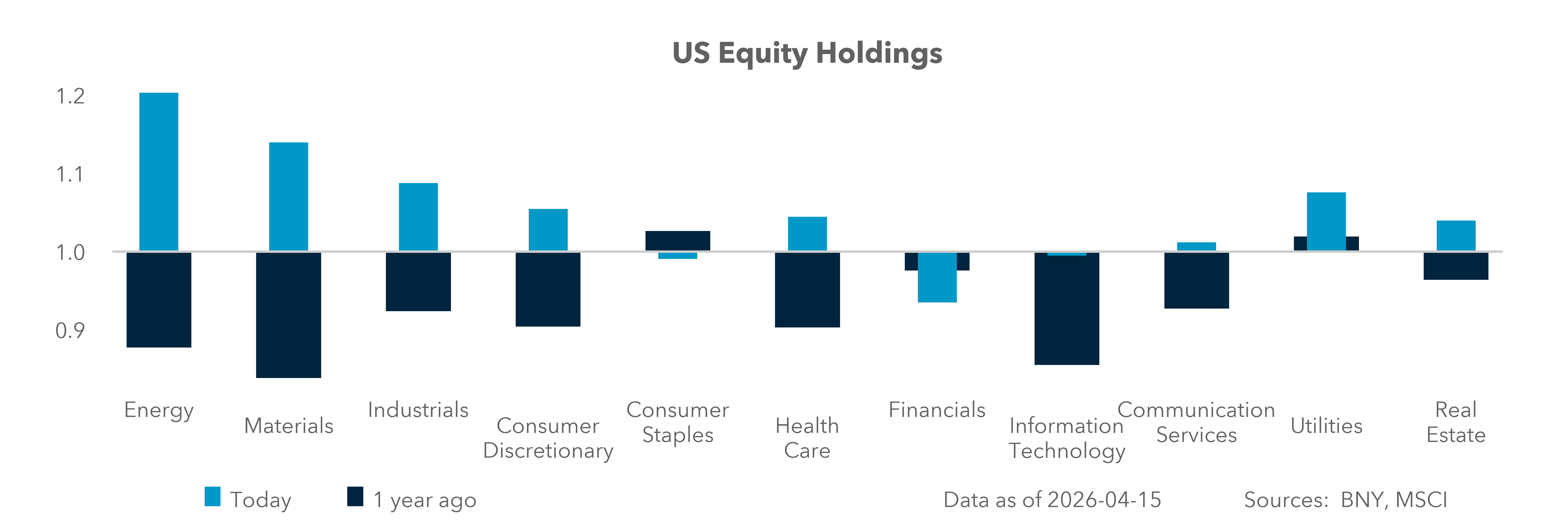

EXHIBIT #1: IFLOW REGIONAL EQUITY HOLDINGS FROM “LIBERATION DAY” TO IRAN CEASEFIRE

Source: BNY

Our take

The ceasefire effect on global equity flows stands out in our iFlow Mood index and in Exhibit #1 above as the bottoming of risk-off sentiment appears to be underway. The rally in equity holdings at the start of 2026 was most extreme in EM shares, and the 15% drawdown from peak holdings still leaves emerging markets vulnerable to further reallocation, if inflation and policy issues block earnings growth – particularly in Asia. The U.S. and EMEA are at the long-term average of holdings and have room to rally should earnings for the year remain robust. The APAC holdings remain elevated, reflecting ongoing positive outlooks for Japan.

Forward look

What are the risks that earnings will prove insufficient to support the ongoing equity bounce? There are four factors of concern for earnings season: 1) margin outlooks for all materials from the supply chain disruption, not just energy; 2) the role of central bank rate hikes, which risk derailing the equity recovery; 3) the role of potential re-escalation in the conflict – with oil prices, Strait of Hormuz vessel traffic and some products like jet fuel and petro chemicals as barometers; and 4) ongoing investor reluctance to shift allocations and chase momentum.

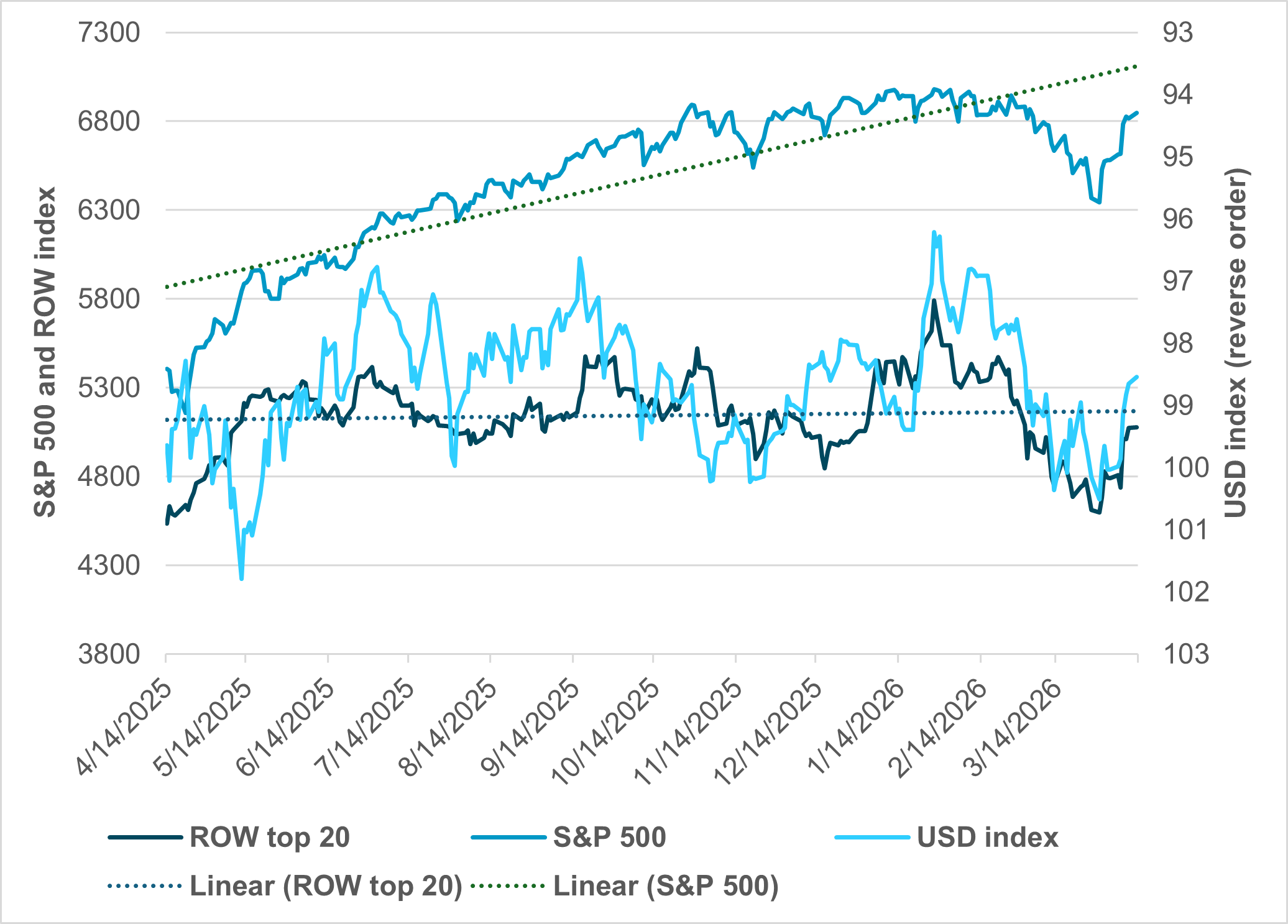

EXHIBIT #2: S&P 500, REST OF WORLD TOP 20 COMPANIES, AND THE USD INDEX

Source: BNY, Bloomberg

Our take

Since “liberation day,” the S&P 500 rose 26% while the Rest of World (ROW) top 20 companies rose 13%. The correlation of the ROW index to the USD index stands out in the last year. The current rally up in risk and the return of USD selling has been notable, as stock markets outside the U.S. have recovered to pre-war levels, as has the USD. The trend divergence between the S&P 500 and the ROW index is stark, particularly for momentum-driven investors.

Forward look

The role of the USD in driving investment flows will connect back to the way global companies manage the current supply shock. Margins and earnings in Q2 will be more critical than Q1 making CEO commentary about their outlooks key for moderating expectations. The other key factor for investors is the role of rate policy from the Fed and from other central banks. European Central Bank rate hike expectations (two hikes of 25bp in 2026 now priced) versus the Fed (a 40% chance of one cut) drove EUR from 1.15 to 1.18 this week. USD dynamics in emerging markets have also been caught in a feedback loop driven by central bank intervention risks. More intervention will keep front-end rates globally tighter. Overall, the investment decision for diversification that dominated EM flows at the start of the year will require a clear USD view along with growth signals and tamer inflation expectations.

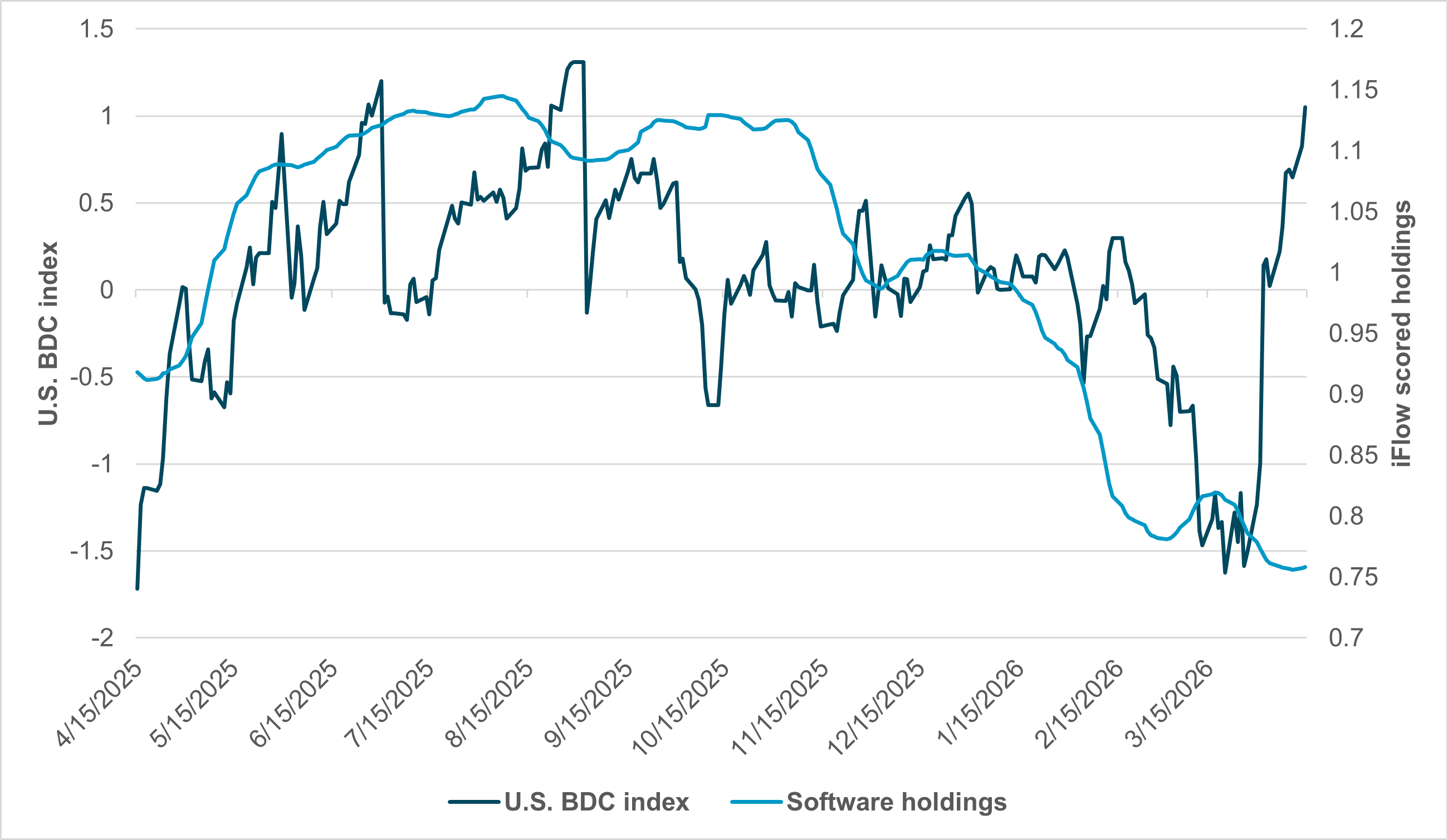

EXHIBIT #3: U.S. BDC INDEX VS. U.S. IFLOW EQUITY SOFTWARE SECTOR HOLDINGS

Source: BNY, Bloomberg

Our take

The fiscal response from governments to the energy supply shocks is ongoing, but IMF warnings about further fuel subsidies highlight concerns about debt levels globally. In 2025, total global government debt touched 94% of GDP. Rate concerns and growth risks were clearly embedded in pre-war fears about private credit. In the last week, a surge in BDC (Business Development Companies) supply was met with demand, and that rebound – along with the asset class finding a flow – has key implications for private credit for the rest of the year. The correlation of software as an industry to the U.S. BDC market has been notable since COVID. Current U.S. software equity holdings are 25% below their long-term average – below even the lows seen around “liberation day.”

Forward look

The software sector should see a rebound if private credit market concerns ease along with stronger Q1 earnings. The role of AI – particularly agentic work in coding – has been one driver of the software sell-off, while the cost of rolling over debt and growth concerns are the others. The landscape looks different now given the calm brought on by the ceasefire. Whether this translates into fewer concerns about the U.S. growth and credit cycle will be key for the software industry’s recovery, along with the sector’s actual earnings in the weeks ahead.

The durability of the equity rally will hinge less on backward-looking Q1 earnings strength and more on forward guidance around margins, cost pressures and demand resilience. Elevated cross-asset correlations and an uncertain rate backdrop reduce the reliability of traditional diversification, placing greater emphasis on macro signals – particularly USD direction, central bank policy divergence, and energy market stability. Equity investors should remain selective, prioritizing pricing power, balance sheet strength, and earnings visibility, while maintaining flexibility to adjust regional and sector exposures as clarity emerges on inflation trajectories and global policy responses.