AI, power demand and equity leadership’s quiet repricing

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

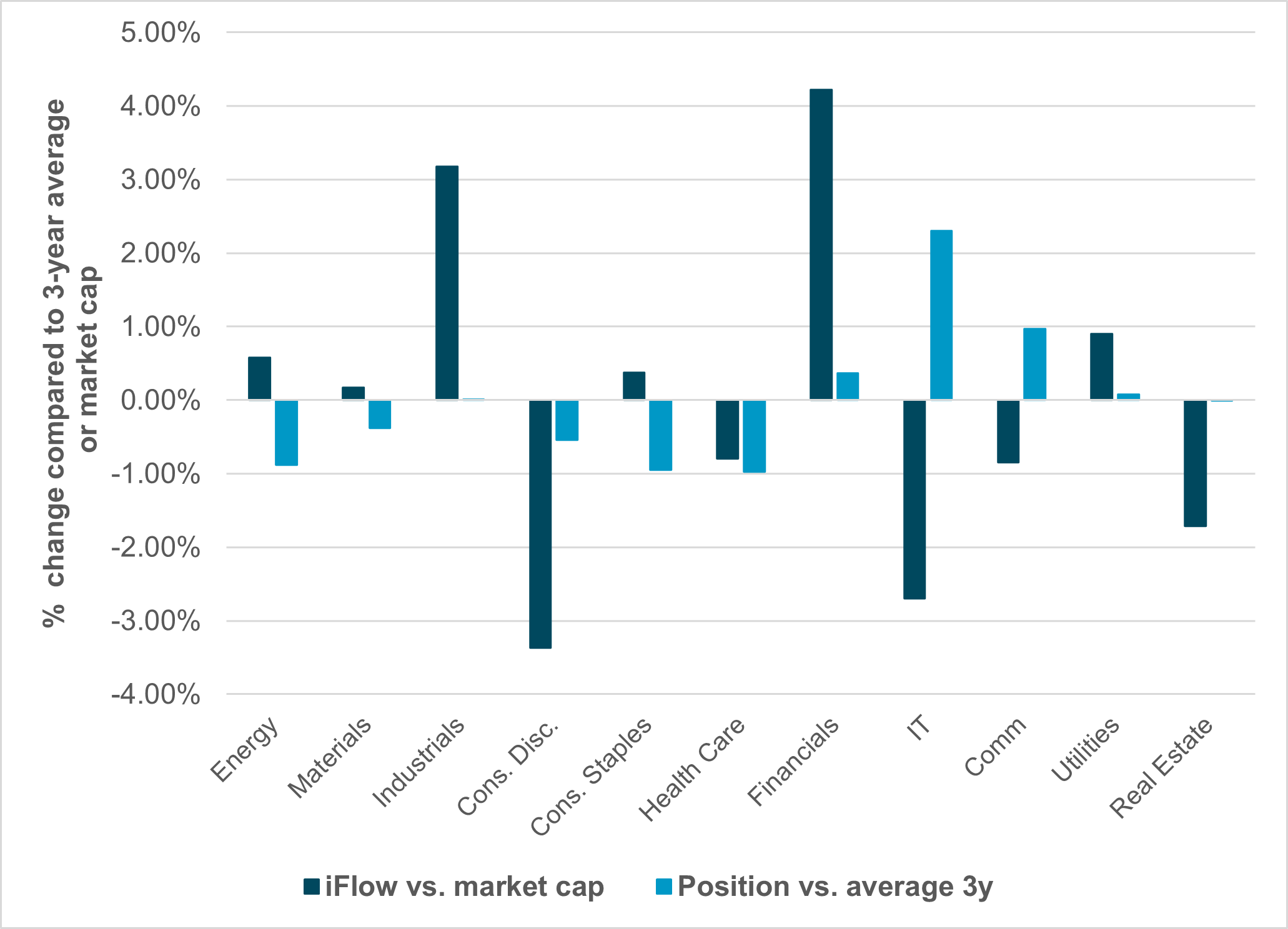

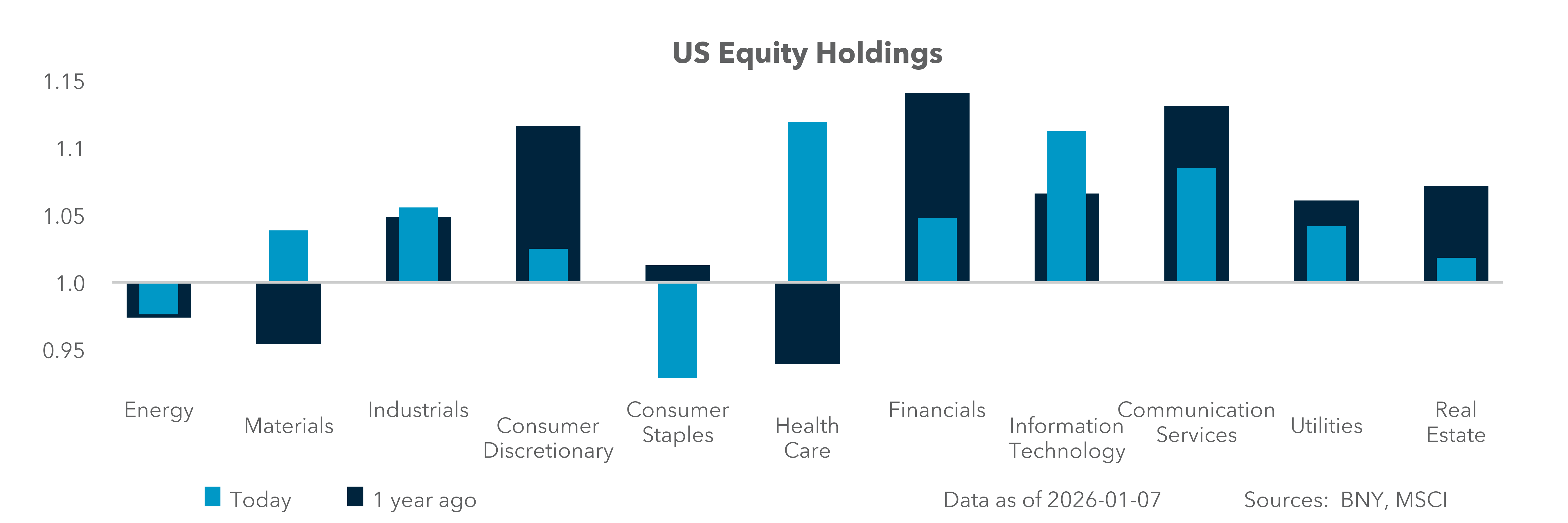

EXHIBIT #1: U.S. SECTOR POSITIONING 2026 VS. MARKET CAP AND HISTORY

Source: BNY, Bloomberg

Energy’s relevance in 2026 will persist beyond the news cycle. What stands out from iFlow positioning as we start the new year is that Energy is already set up for gains. Investors have flipped from underweight to overweight but remain below their longer-term average positioning, suggesting there is room to add should energy returns resurface after three down years. Information Technology has seen a notable downshift against market cap, but investors remain about 2% more overweight than average. To put this in perspective, positioning in sectors of this size typically shifts by less than 0.5% per year. The great rotation trade is already underway, with IT underweight relative to market cap, though not compared to the longer-term average. IT’s link to other sectors supports hopes for a broadening of returns from Industrials to Financials, and ongoing focus on Utilities.

Our take

While iFlow shows caution for IT compared to the market and support for Energy, the broader market has been more enthusiastic. U.S. foreign policy and natural resources dominated the week, though oil and natural gas prices have yet to attract significant investment flows compared to technology. The divergence between U.S. and China’s AI strategies remains a key theme. However, the bigger story for equities next week is how Energy, Utilities and Technology perform as Q4 earnings begin. Expectations for the year ahead are robust, with 15% earnings growth forecast, driven not by technology, but the rest of the market.

Big bank earnings will be key to sustaining the January rally. Supporting this outlook is the consensus: robust near-2% growth, fiscal support from the “big, beautiful” tax bill, lower interest rates from the Fed, stronger profits from AI productivity – and key to all of the above, lower energy costs. The biggest problem is that ROI for new energy projects requires stable pricing in crude oil and natural gas.

Forward look

The consensus for 2026 reflects the International Energy Agency (IEA) report on energy and AI. Surging data-center electricity demand reshapes the global power mix through 2035. While wind and solar renewables are the dominant growth sources globally and expected to expand rapidly, fossil fuels – especially natural gas and coal – remain essential in the near term to meet surging demand. Regional patterns differ markedly, with coal dominating China’s data-center supply and natural gas leading in the U.S., though both see increasing renewable and nuclear shares over time.

Here are the key points:

· Electricity generation for data centers more than doubles – from about 460 terawatt-hours (TWh) in 2024 to over 1,000 TWh by 2030 – reaching 1,300 TWh by 2035 in the base case.

· Renewables are the fastest-growing source, meeting around half of additional electricity demand to 2030, yet natural gas and coal together supply over 40% of near-term incremental needs.

· Nuclear’s role rises post-2030: Small modular reactors (SMRs) begin contributing, particularly in the U.S. and China, helping reduce coal-fired generation for data centers by 2035.

· CO₂ emissions from data-center electricity generation are expected to peak around 2030 at approximately 320 million metric tons, then decline modestly. By that time, data centers will account for about 3% of global electricity use and less than 1% of global CO₂ emissions.

Adoption and ongoing technology improvements are nearing the efficient frontier for energy use.

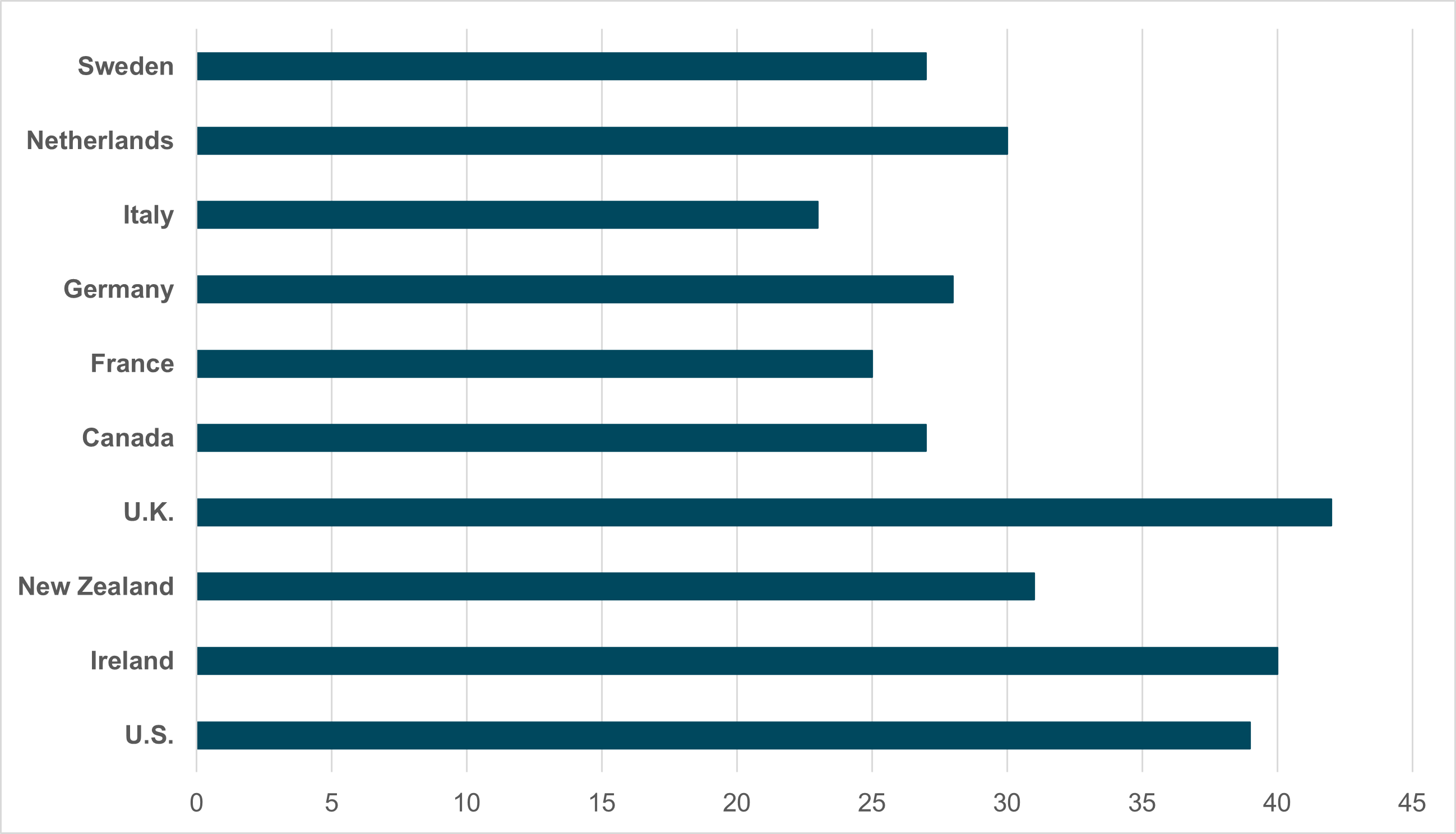

EXHIBIT #2: FRACTION OF LABOR FORCE USING LLMS AT WORK

Source: BNY, Hartley et al., SSRN

There are several blind spots in the IEA report, many of which revolve around the role of data centers in the U.S. and rest of world. The rapid adoption of AI tools is increasing demand for electricity and data center build out. However, more efficient models and chips powering chatbots are reducing energy need. Another factor is data fragmentation: global data centers must be built where AI is used, as regulations often have a home bias – particularly in APAC and increasingly in EMEA.

1) AI adoption is growing. While usage remains far from full capacity, it is already higher than many expect, suggesting that future data center demand may be overstated. The employment impact of AI remains contested, but large language model (LLM) use among highly paid, educated workers stands at 30% across G10 nations. This implies usage could double, but likely not triple, over the next few years. These trends have clear implications for both energy demand and data center buildouts. Energy intensity also depends on task type: LLMs used to rewrite emails consume far less energy than autonomous systems building a bridge.

2) AI costs are falling. While increased adoption tends to lower costs, we may already be near a sweet spot. Winner-take-all arguments may be overstated, and monopoly risks for LLMs could be diminishing. Competition and performance improvements have cut costs. Greater efficiency means energy use is less of a constraint, and different models are likely to gain market share for different tasks.

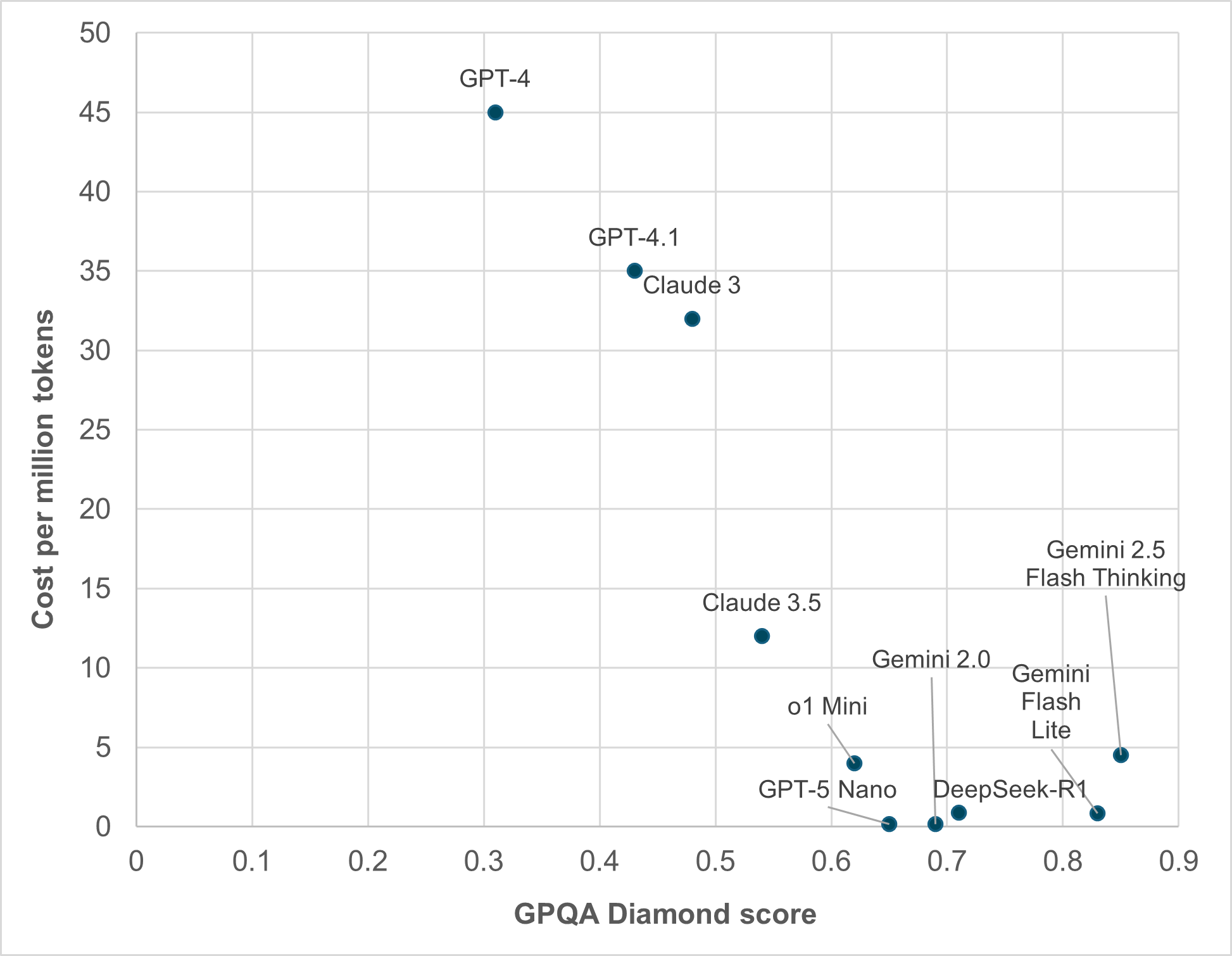

EXHIBIT #3: AI MODEL COST AND PERFORMANCE

Source: BNY, Mollick, One Useful Thing

The Diamond Score over 0.8 is seen as PhD-level equivalent. The Graduate-Level Google-Proof Q&A test (GPQA) presents extremely difficult multiple-choice questions to test advanced knowledge. Non-experts score around 34% even with internet access, while PhDs score 74–81% within their field. Model usage is measured in cost per million tokens.

Our take

Most AI users are not tapping the full capabilities of current models. The speed of improvement in cost and quality over the last 18 months has been more dramatic than even price moves in the Tech sector. This reflects the growing profitability of LLMs as broader use demonstrates real returns. Profitability is further boosted by energy-efficient improvements in speed and quality. For example, creating a five-minute AI-generated video requires roughly the same energy as:

Forward look

At the heart of investor concerns over an energy/AI cliff are the rapid pace of AI adoption, chip development and ongoing LLM model efficiency gains. The forward curve of crude oil suggests prices may fall to $45bbl before rebounding to $75bbl. AI demand and efficiency gains continue to accelerate, but the real energy shock risk lies more in constrained supply than surging demand. The bigger blind spot may be in the political risks linked to electricity and data across jurisdictions.

Equity market risks appear more linked to election outcomes and affordability concerns. In the near term, iFlow positioning suggests workers are rapidly adopting AI tools, while LLMs continue to improve and fall in cost. As earnings season unfolds, any upside surprise from hyperscalers or chipmakers could extend the three-year equity rally, despite ongoing valuation and margin concerns.

Looking ahead to 2026, Energy’s relevance is unlikely to fade with shifting headlines. Positioning data signal that investors are preparing for a more durable regime change, one in which energy security, electricity availability and price stability matter as much as innovation leadership. The IEA’s framework underscores this tension: AI-driven electricity demand is set to surge, yet efficiency gains in models and chips will temper worst-case energy scenarios. This creates a narrower path for returns – favoring incumbents with scale, balance-sheet strength, and regulatory alignment rather than speculative capacity builds.

For equities, the implication is broader than a simple Energy versus Technology trade. Utilities, Industrials and Financials stand to benefit from capex cycles tied to power grids, data infrastructure and project financing, while Technology’s leadership becomes more selective and earnings-dependent. Critically, stable or lower energy prices underpin the optimistic earnings outlook for the broader market – volatility, not scarcity, is the key risk for returns on new supply.

As Q4 earnings unfold, upside risk remains skewed toward companies able to monetize AI productivity without reigniting an energy cost shock. In that environment, rotation – not reversal – defines the next leg of the equity cycle.