Payments

Fast, secure and intelligent payments infrastructure.

Global trade has been tested repeatedly over the past decade by a series of major disruptions. From the COVID-19 pandemic to the current oil price shock, each disruption has exposed vulnerabilities in global networks and accelerated structural shifts that were already underway.

Supply chains have diversified while trade corridors have multiplied, with implications for the way banks and corporates transact across borders. Flexibility is more important than ever.

At the same time, the network infrastructure underpinning this activity is facing sustained pressure. Rising compliance costs, increased regulatory expectations and the operational burden of maintaining global trade relationships are driving banks to reassess the breadth of their networks.

The result is a paradox. As trade becomes more distributed, requiring broader and more dynamic connectivity, the ability to maintain direct connections grows more constrained. In this environment, the strategic question is no longer how many connections does an institution own, but rather how effectively can it access the networks that matter most?

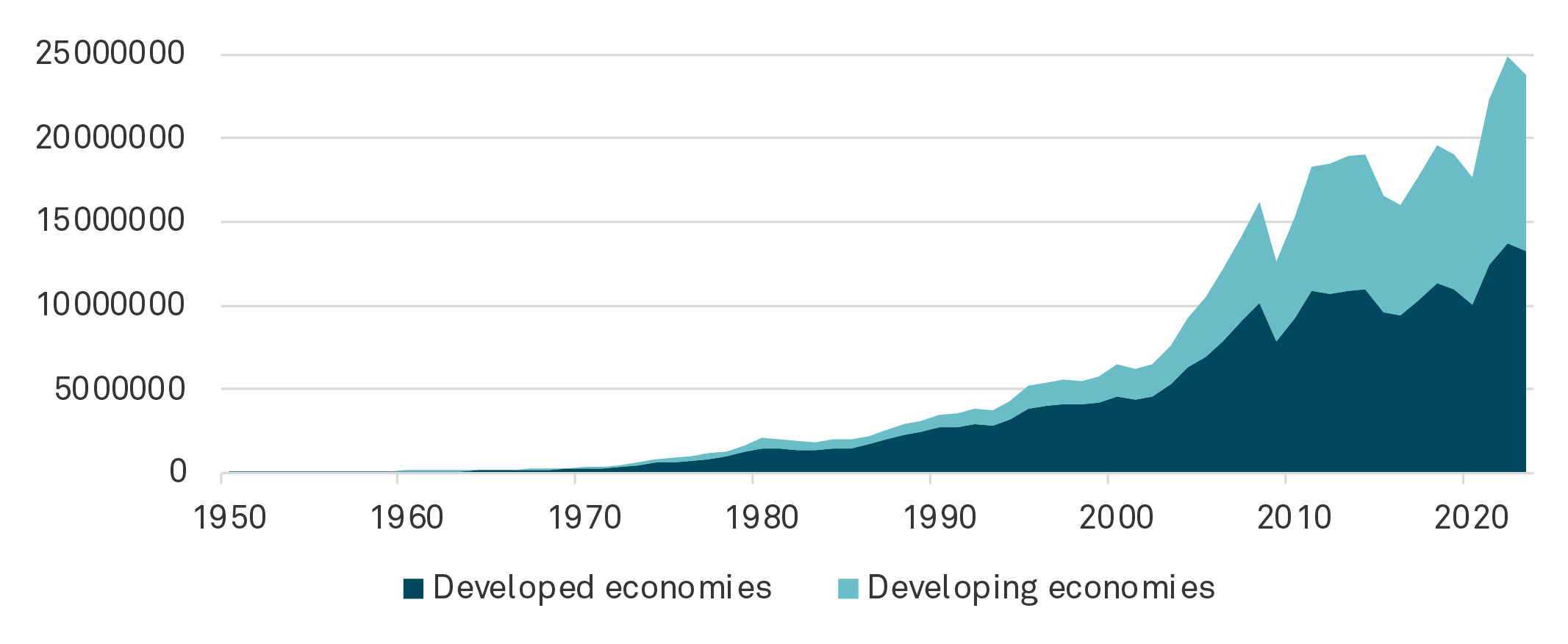

As the global economy evolves, the way banks finance trade is evolving with it. While the United States, China and Europe remain its principal anchors, a group of middle powers – from India and the GCC states to the fast-growing economies of Africa, Southeast Asia and Latin America – are playing an increasingly important role. Indeed, developing economies have significantly expanded their participation in global trade over the past six decades. Between 1964 and 2023, their share of global merchandise trade doubled from 22% to 44%, highlighting the rising importance of emerging markets within global production networks and supply chains1.

As a result, the trade landscape is now much more extensive, with a wider range of production hubs, diversified supply chains and an expanding network of regional trade corridors.

Rather than relying on a small number of dominant manufacturing centers, companies are increasingly distributing production, sourcing and logistics across several jurisdictions – resulting in a less concentrated trade ecosystem.

Firms must be able to engage with a broader set of counterparties across more markets, often dynamically adjusting their supply chains in response to geopolitical, economic or operational pressures.

This shift places a greater premium on reach and flexibility, both for corporates and for their banks. Financial institutions need to provide clients with the resources needed to support modern trade flows, while managing the increasing cost and complexity of maintaining a wide network of correspondent banking relationships.

The result is that traditional models may no longer be sufficient. Despite growing demand for connectivity, correspondent banking networks have been under pressure for more than a decade as rising compliance, know your customer (KYC) and anti-money laundering (AML) requirements increase the cost of maintaining relationships. This pressure is most acute for smaller and regional institutions, as well as in lower-volume corridors where the economics are hardest to justify.

This has led many institutions to rationalize their networks by focusing on core markets and counterparties, and reducing less frequently used relationships.

One area where this pressure is especially visible is in the management of SWIFT Relationship Management Application (RMA) connections. RMAs control which counterparties can exchange trade-related messages with one another. Without them, banks cannot directly send or receive the messages needed to support cross-border payments and instruments such as letters of credit.

As a result, banks are treating RMA networks more strategically, prioritizing high-volume corridors and reassessing lower-activity relationships. But as they streamline the RMAs they maintain, they also reduce the number of counterparties and corridors they can reach directly. In some cases, that can limit their ability to support clients, forcing them to decline transactions or rely on intermediaries.

To maintain client support, banks are increasingly rethinking how they access global networks – shifting away from owning a full set of RMA relationships toward accessing them through trusted providers. This approach allows institutions to remain selective in the relationships they maintain, reducing the compliance and operational burden of managing multiple connections while providing greater agility in responding to shifting trade corridors and client needs.

This evolution is not confined to trade finance. Across industries, access is increasingly displacing ownership as the dominant model – from enterprise software delivered on demand to models where businesses access and use physical equipment without owning it. This allows organizations to scale capabilities flexibly without carrying the full operational and capital burden of ownership.

Global institutions play a central role in enabling this shift in trade. By providing structured access to their networks, they allow clients to route instruments such as letters of credit through established channels, while also offering financing, confirmation or reimbursement services where required.

BNY illustrates this development through its Trade Network Access Service (TNAS). Thanks to its single digital interface, clients can view available RMA connections, validate transactional routes and review trade-related transactions without having to establish and maintain each bilateral relationship directly.

This model is already in use among leading financial institutions. For example, Mizuho Bank, a leading global bank with one of the largest customer bases in Japan, leverages TNAS across multiple branches to access BNY’s extensive trade network. In doing so, it provides scale and connectivity across its own multi-location network, creating multiple pathways for trade flows rather than one-to-one connections.

It also enables clients to benefit from the technological investments of larger institutions. In the case of TNAS, capabilities such as AI-driven data extraction from letters of credit helps automate processing workflows, reducing manual effort and operational risk, while the Real-Time Advice feature gives users visibility into the live status of a letter of credit within BNY’s processing workflow, enhancing transparency, control and predictability from receipt through to release to the next counterparty.

More broadly, the value of access-based models extends beyond operational efficiency. Strategic relationships with large global institutions can provide additional credit capacity and international reach, helping banks mitigate risk and support larger or more complex trade flows. Increasingly, these models are being delivered through digital platforms that bring network and credit access together. This allows institutions not only to manage RMA connectivity more effectively, but also to submit transactions for confirmation or discounting support where needed.

As the need for flexible and reliable cross-border connectivity increases, banks are, paradoxically, becoming more selective in the relationships they maintain – seemingly limiting their access to global markets. In reality, this reflects a deeper structural shift. What was once a manual, relationship-led process is becoming more transparent and platform-based – enabling banks to identify routes, initiate transactions and monitor activity more efficiently.

The implication is not simply that trade flows and corridors are shifting, but that banks’ role in those flows – and, ultimately, how they serve their clients – is evolving as well.

In this environment, reach is no longer defined by what relationships a bank owns, but by what it can access. Those institutions that can navigate networks intelligently, rather than replicate them, will be best positioned to support clients as global trade continues to evolve.

BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material and any products and services mentioned may be issued or provided in various countries by duly authorized and regulated subsidiaries, affiliates, and joint ventures of BNY. This material does not constitute a recommendation by BNY of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY. BNY has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY assumes no direct or consequential liability for any errors in or reliance upon this material.

This material may not be reproduced or disseminated in any form without the express prior written permission of BNY. BNY will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. Trademarks, service marks, logos and other intellectual property marks belong to their respective owners.

© 2026 BNY. All rights reserved. Member FDIC.