No Holiday for Volatility

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 11 minutes

The last full week of trading in 2025 will deliver volatility, with key central bank rate decisions from the Bank of Japan (BoJ) to the Bank of England (BoE) and European Central Bank (ECB), along with U.S. jobs, CPI and flash PMI reports. How the soft patch of Q4 growth ends will depend on holiday sales, corporate profits and both fiscal and monetary policy.

Unlike 2024, this year’s final stretch is upbeat: global equity markets are at record highs, technology and AI allocations remain elevated, and outlooks for the year ahead are bright. What’s unclear is what will keep the holiday cheer intact through New Year’s, with politics and geopolitics acting as the fragile tape – from Ukraine peace talks and Chile’s election to U.S. pressure on Venezuela and Gen-Z upheaval in elections from Bulgaria to Thailand.

Looking into the next three weeks, we see three key themes:

1) Global rate cycle turning from easing to tightening. The BoJ will be on the front line of this shift, with debate focused on raising the terminal rate from 1% to 1.5%, which is the key guidance. Also key are the diverging policy paths among the U.S., U.K., and emerging markets (EM) like Brazil. The tone of U.S. Fedspeakers and incoming data will drive expectations for an extended pause.

2) Politics. With Chile’s presidential election this weekend, focus is returning to ballot boxes and polling data. The Bulgaria protests last week led to a surprise resignation by the minority government and new elections scheduled for January. Thailand’s prime minister also surprised markets by dissolving parliament, setting up late-January elections. How politics play out in the U.S., UK, and EU remains a key story for 2026, with polls driving markets.

3) Earnings. As we saw last week from Oracle and Broadcom, earnings significantly influence stock performance globally. Most of the results will be out by the end of next month, but from now until early January, expect early guidance to move markets. Also expect the retail reports to be crucial to judging overall U.S. growth and consumer health. AI-related bubble fears and valuation stretch collide with year-end positioning, as rotation pressure rises and blue chips set new records. Sector rotation – between IT, Health Care and Communications versus Financials, Consumer Staples and Industrials – will shape market reactions to data and policy talk.

Overall, the setup for next week suggests more volatility. The focus on bond yields globally is one key barometer as the U.S. yield curve is the steepest of the year. The implications of higher rates on credit and the U.S. dollar also matter. The FOMC’s reserve management process will be a key signal in calming year-end liquidity needs, as investors rush to clean up positions.

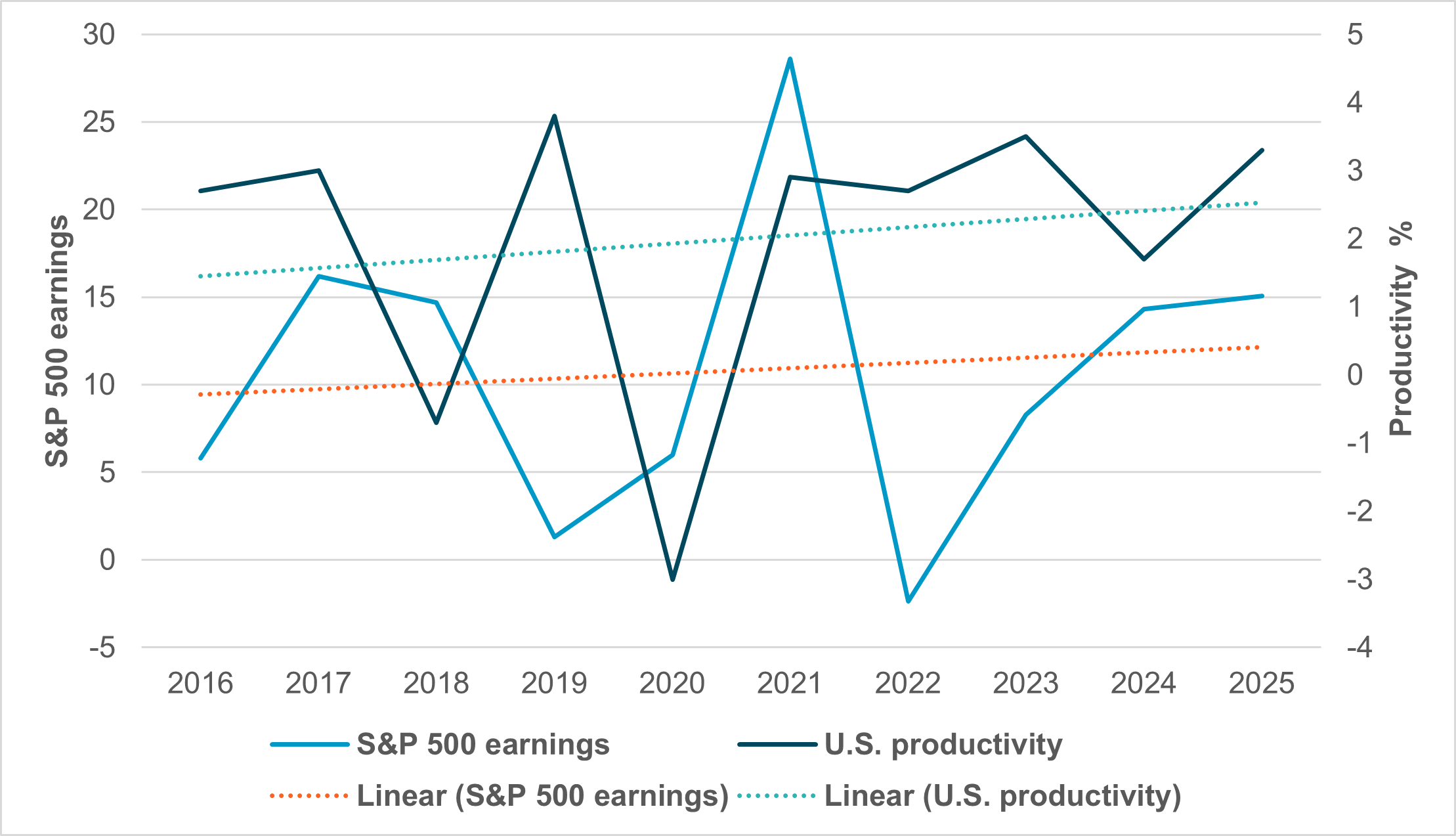

Will productivity drive markets in 2026 or will earnings still dominate?

EXHIBIT #1: U.S. S&P 500 EARNINGS VS. PRODUCTIVITY

Source: BNY, Bloomberg

The key risk for 2026 revolves around how inflation interacts with earnings, as AI investment lifts productivity expectations.

Our take: Fed Chair Jerome Powell, at his news conference following the Fed’s 25bp rate cut, noted that the U.S. economy’s elevated productivity rate – around 2% for the last several years – predates the recent AI boom, though the innovative technology is helping reinforce the trend. The impact of COVID-19 on the data is important, but so is the 2017 to 2019 period. The earnings trend remains flatter than the productivity one, suggesting the full benefit has yet to be reflected in market pricing. The ability to produce more output with fewer labor hours should help cap inflation fears.

Forward look: Whether Q4 growth and inflation reflect an ongoing productivity trend will shape how investors view 2026. This makes next week’s U.S. labor and CPI reports essential to understanding the medium-term risks ahead. Earnings will not be known until late January, but they will need to support the view that companies can absorb one-off tariff costs, raise wages and continue capital investments – all necessary to sustain expectations for equities and bonds.

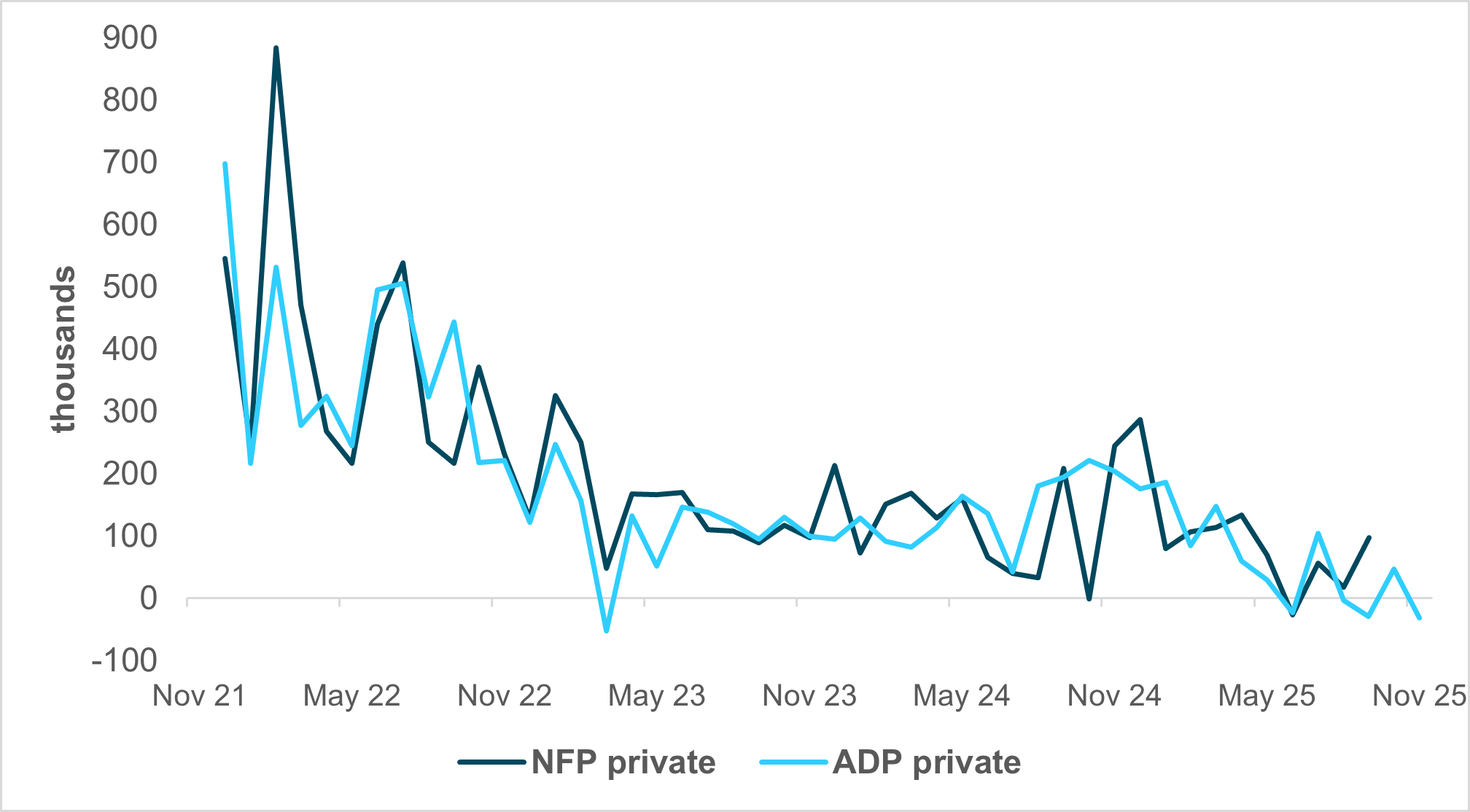

U.S. economic data will drive volatility around policy expectations

EXHIBIT #2: PRIVATE JOB GROWTH SUGGESTS TROUBLE FOR NFP

Source: BNY, Bloomberg

Our take: The final two weeks of the year are typically quiet – but not this year. A wave of U.S. government data is scheduled for release, some of it crucial to understanding where the economy is headed into 2026. Following the slightly hawkish FOMC cut last week, odds of a rate cut at the January 31 meeting have fallen to around 25%.

On Tuesday, we will finally get some comprehensive labor market data – October and November nonfarm payrolls, delayed by the shutdown. We won’t see October household data, including unemployment rate and demographic breakdown, since the Current Population Survey could not be conducted at the time. Fed Chair Powell noted that the establishment survey may be overstating job growth by as much as 60k. The October retail sales report will also be released on Tuesday. Together, these reports should help gauge the state of U.S. households from both employment and consumption perspectives.

November’s CPI is due Thursday, after the October release was skipped due to the shutdown. We will also get a few regional PMIs (Philadelphia and Kansas City), plus the final University of Michigan consumer sentiment reading. These will be overlaid with commentary from FOMC speakers, whose responses may vary based on the reports.

Forward look: Markets will reprice Fed rate cut odds into 2026 based on upcoming data and Fed commentary. But the macro-driven volatility will not end on December 19. The week between Christmas and New Year’s will be busier than usual on the data front. On December 23, we’ll get the first read on Q3 GDP, along with October durable goods orders. Retailer reports on holiday sales will also be a key focus.

By early January, we should have a solid set of data to assess how the economy performed in the last few months and whether we are truly at an inflection point.

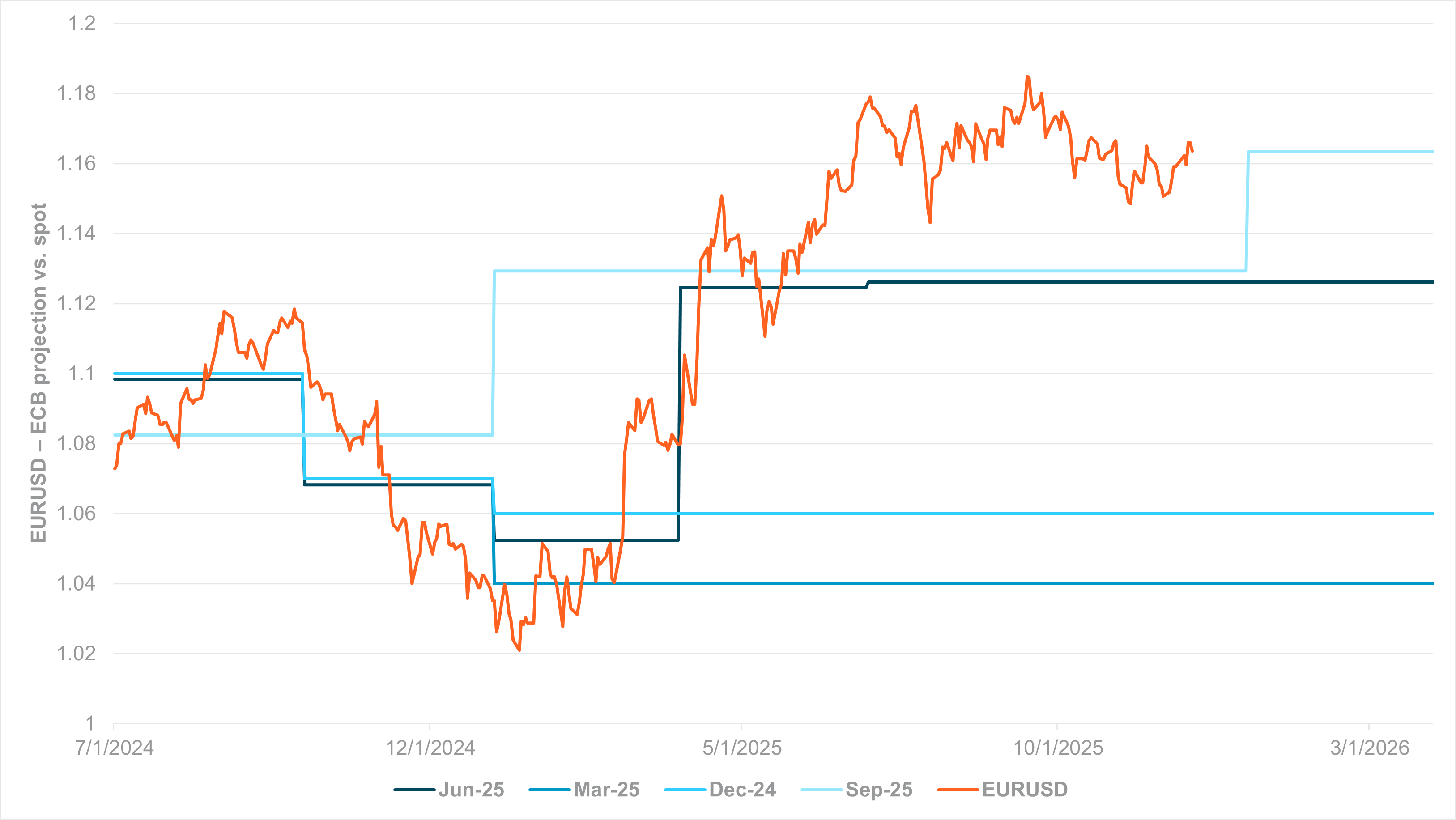

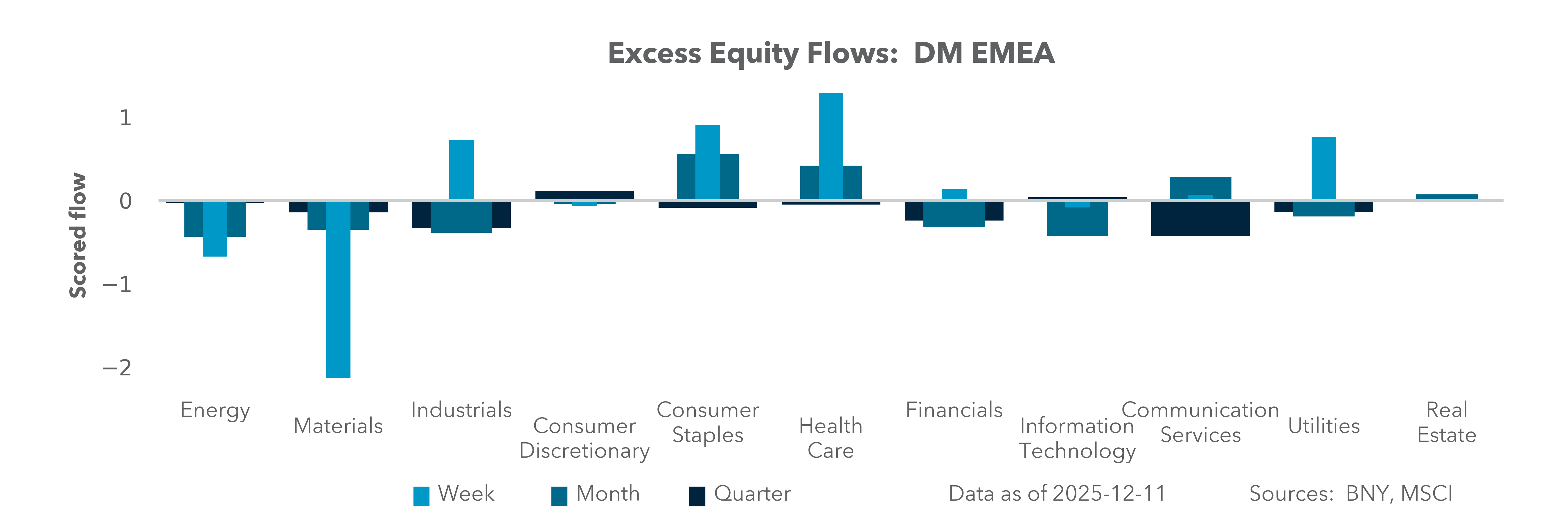

EMEA: ECB pivot may raise tolerance for euro strength

EXHIBIT #3: EURUSD ASSUMPTIONS VS. ACTUALS, LAST FOUR ECB ROUNDS

Source: BNY

Our take: Our expectation that the ECB would acknowledge manufacturing sector weakness and consider easing next year now looks unlikely. From national to pan-Eurozone levels, policymakers have signaled improved conditions, prompting upward revisions in the economic outlook. This suggests the staff projections will include higher FX assumptions and wider confidence intervals, effectively raising the ECB’s tolerance for euro (EUR) strength. EURUSD has traded well above the ECB’s September central tendencies (Exhibit #3), but even then, the ECB viewed a 1.20 level as having minimal impact on the 2026–2027 inflation outlook. The latest revisions suggest that a clear move above 1.20 in 2026 would also be acceptable.

From a disinflation or competitiveness perspective, European governments, the ECB and even the IMF are now squarely focused on China and the renminbi (CNY). EURCNY appears likely to end the year more than 10% higher. Warnings from Eurozone leaders and industry officials point to serious risk for regional manufacturers – risks that could carry political consequences. Beijing appears fully aware of these risks. The flurry of announcements on Friday, surrounding export licensing for steel and price-setting for vehicles, should be seen as pre-emptive measures to ease tensions.

Meanwhile, the Bank of England (BoE) is expected to cut rates by 25bp to 3.75%. Governor Andrew Bailey is likely to use his casting vote to support the cut. However, the market is now more focused on how deep the easing cycle will go, particularly if fiscal consolidation continues in 2026. Chancellor of the Exchequer Rachel Reeves has said nothing can be ruled out if public finances come under renewed pressure. Households appear to be responding by increasing precautionary savings. The governor has indicated this is a further sign of consumer weakness that may require a rate cut. The challenge is translating consumer restraint into softer wage growth, but factors driving wages are structural and supply driven. A majority at the BoE now believes that wage inflation alone should not prevent further policy support, even as broader inflation expectations remain elevated. GBP is holding up well as pre-budget hedges unwind, but its path against European currencies in 2026 will be more challenging.

Forward look: For the other key decisions in Europe, we doubt there will be much suspense as the crucial issues have been well-documented. Nordic economies continue to operate on their own terms. Despite strong savings buffers, their currencies and assets have not performed as though markets view them as safe havens. Recent unemployment figures could push the Riksbank’s bias toward downside risks. This is surprising, given the upward revisions in Eurozone conditions that should act as a tailwind. Fiscal rules will be difficult to adjust in support of stimulus. Still, leading indicators suggest better conditions ahead. We do not see the Riksbank in a position to fully rule out rate cuts, even if markets are leaning in that direction.

Norges Bank (NB) remains one of the best-positioned central banks for faster reflation, with the recent positive shift in global energy prices adding tailwinds from the offshore economy. If the International Energy Agency’s forecasts for improved supply-demand balances are realized, markets should be cautious in krone (NOK) positioning. Stronger oil revenue flows to support fiscal outlays will further reduce the need for NB to purchase NOK on the government’s behalf.

Both underlying and headline inflation remain robust, but signals around the demand outlook are mixed. Given the current uncertainty, we expect NB to err on the side of caution. Recent decisions in Canada and Australia, for example, suggest that a pivot toward early tightening remains only a tail risk.

Central and Eastern Europe (CEE) economies remain under close scrutiny, and both the Hungarian and Czech central banks (MNB and CNB, respectively) are expected to remain on hold. The Czech economy stands alone in the region with clear downside risk to inflation, and its funding status in iFlow has been clear-cut.

The ECB’s more robust outlook should set a floor in expectations. However, we remain concerned about the industrial side of the Eurozone economy, and the ongoing flurry of headlines surrounding the automotive industry will have material consequences for the Czech outlook.

In Hungary, we continue to see risks of additional hedging in the forint (HUF) as fiscal pressures continue to rise. Markets are also becoming more sensitive to political adjustments ahead of upcoming elections. Real rates will remain key to the sustainability of current HUF positions, and we see the MNB has having the strongest case for a pivot back toward tightening.

President Trump’s denial of U.S. Treasury support for the currency, along the lines of past Argentine policy, has raised the stakes. For now, however, elevated real rates should limit any material underperformance.

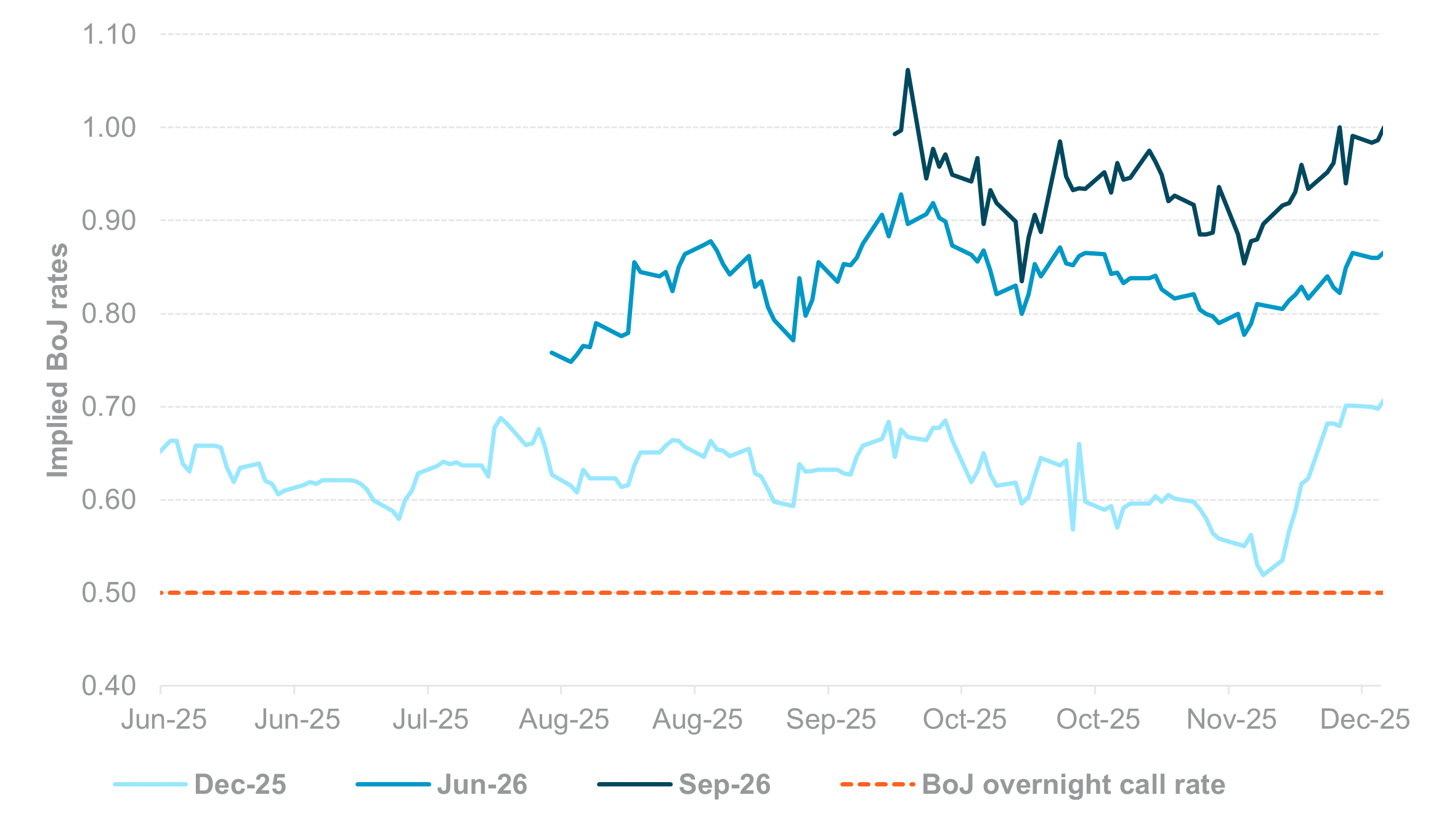

APAC: China investment data, Australia PMI and BoJ, BoT, BI and CBC decisions

EXHIBIT #4: BOJ INTEREST RATE EXPECTATIONS

Source: BNY, Bloomberg

Our take: This week in the Asia-Pacific (APAC) region, attention center on the BoJ’s policy decision. Markets will also focus on China’s November data, including home prices, retail sales, investment and activity. Trade figures for November are also scheduled to be released by Singapore, Malaysia, Thailand, India, New Zealand and Japan. Preliminary December PMI results will come from India, Australia, and Japan. Australia will report consumer confidence and inflation expectations. New Zealand will announce Q3 GDP and November’s Performance of Services Index. Japan will release both its Q4 Tankan survey and national CPI.

China’s October fixed asset investment declined by –1.7% YTD y/y, the lowest level since June 2020. Infrastructure investment within the tertiary industries stagnated, with just 0.1% growth YTD y/y. Property investment fell by –14.7% YTD y/y, nearing the record low of –16.3% seen in February 2020. Notably, the high-tech sector remains resilient, with strong YTD y/y growth in industrial robots (+17.9%), service robots (+12.8%), new energy vehicles (+19.3%), and integrated circuits (+17.7%). Retail sales growth moderated to 2.9% y/y, down from the peak of 6.4% y/y in May 2025.

November housing data will be closely watched as declines in new and existing home prices accelerate. New home prices fell –0.45% m/m and –2.6% y/y, while used homes dropped –0.66% m/m and –5.4% y/y. Against the backdrop of subdued market expectations for China’s economic recovery, the potential for positive surprises remains high. Elsewhere, export data from Singapore, Malaysia, Thailand, India, New Zealand and Japan may reveal improvements, echoing gains seen in China and South Korea after the post-APEC Summit trade de-escalation.

As market narratives turn more hawkish, asset prices and economic data releases in Australia and New Zealand are likely to face heightened sensitivity. New Zealand is set to publish its Q3 GDP figures, which are anticipated to return to positive year-on-year growth following five consecutive quarters of negative annual GDP since Q2 2024. According to the Reserve Bank of New Zealand’s November projections, Q3 GDP is estimated to grow 0.4% q/q and 0.8% y/y.

In monetary policy developments, the BoJ’s upcoming policy meeting will be a primary focus for markets, with a consensus expectation for a rate hike – marking the second such increase this year, following a similar move in January 2025. Current front-end yen (JPY) pricing suggests a 20bp hike is anticipated. Meanwhile, markets are pricing in potential rate cuts from the Bank of Thailand (BoT, currently at 1.5%) and Bank Indonesia (BI, currently at 4.75%), while Taiwan’s central bank (CBC, 2%) is expected to hold steady.

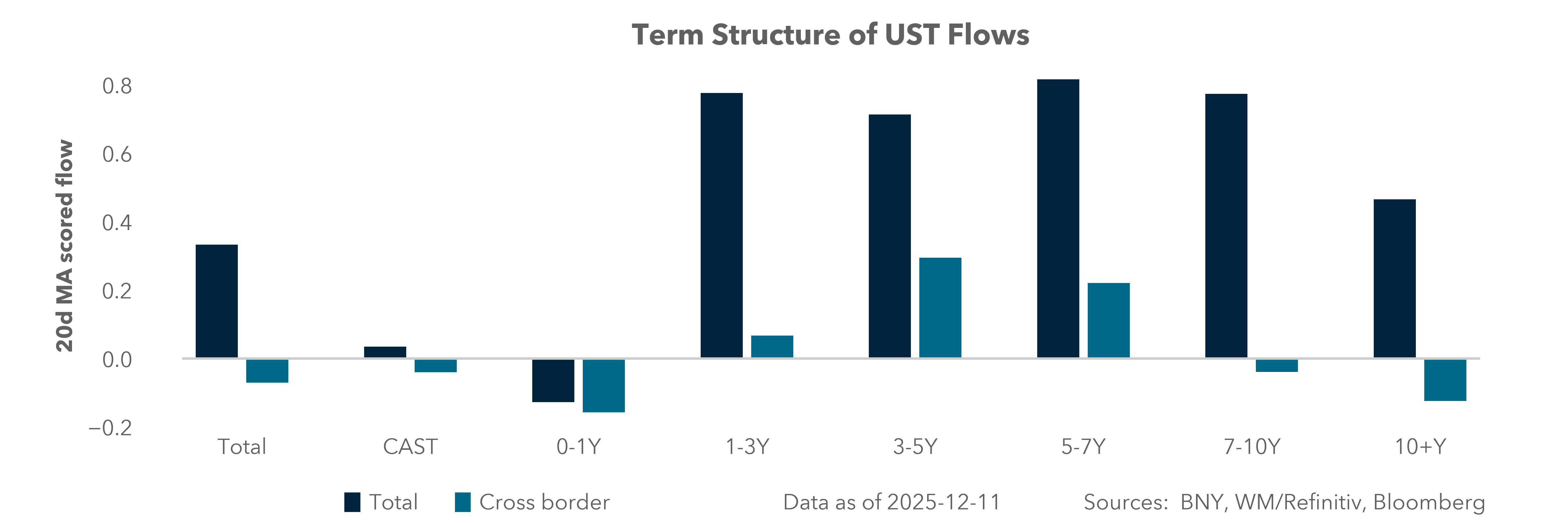

Forward Look: The BoJ’s decision will be key in shaping the direction of the JPY and government bond (JGB) yields into Q1 2026. The recent rise of long-end JGB yields has raised concerns about potential losses and market disruption. Note the surge in foreigners’ JGB purchases – around ¥14tn YTD, compared with ¥2.5tn in 2024. The 10y JGB yield has risen to 2% from 1.1% at the end of 2024, while the 30y yield climbed from 2.3% to around 3.4% over the same period.

Investor sentiment in APAC equities has improved following November’s volatility. According to iFlow data, equity inflows have strengthened in China and across the region. China December’s Politburo meeting and China Economic Work Conference set a supportive tone for 2026. Leaders emphasized plans for a “more proactive fiscal policy and moderately loose monetary policy,” alongside efforts to boost demand, optimize supply, and foster new high-quality productive forces. In the near term, foreign capital inflows, stable commodity prices, steady U.S. rates, and renewed growth momentum should all support investor appetite for Asia-related risk.

As investors enter the final weeks of 2025, markets face a potent mix of macro catalysts, political uncertainty and shifting earnings expectations that will shape positioning for early 2026. Central bank communication – particularly from the BoJ, BoE, and the Fed – will continue to steer rate expectations. Data releases across labor markets, inflation and consumption will either validate or challenge the soft-landing narrative. Geopolitics remains a decisive swing factor: elections from Chile to Thailand, Ukraine negotiations and U.S. policy direction could all abruptly reshape risk appetite.

Yet the central debate for 2026 will center on productivity – whether AI-driven gains materialize in earnings power or remain aspirational. Stabilizing yields, constructive capex trends and resilient consumption would support a risk-positive start to the year. But elevated uncertainty argues for disciplined exposure, selective sector allocation and readiness for event-driven volatility.

Central bank decisions

Hungary, MNB (Tuesday, December 16): The MNB is expected to keep rates on hold at 6.50%, as concerns over fiscal stimulus and its inflationary effects continue to undermine real rates. Headline inflation remains close to 4.0%. President Trump’s recent denial that financial support would be available for Hungary during times of stress also led to questions about the durability of current financial holdings. Given the ECB’s recent pivot indication, it will be essential for the MNB to anchor rate expectations over the medium term, though it is likely too early to signal a return to policy tightening.

Chile, Banco Central de Chile (BCC) (Tuesday, December 16): The BCC is expected to cut rates by a further 25bp to 4.50%, though recent activity data have been more robust. The unemployment rate has fallen to 8.4%, and retail sales rose 8.4% y/y, while CPI remains well above 3%. However, the forward outlook is challenging – industrial production has contracted, and questions remain over copper export volumes as China diversifies supply chains. Forward pricing suggests terminal rates below 4%, and markets will look to the BCC for guidance on the potential end of the easing cycle.

Thailand, BoT (Wednesday, December 17): Slowing growth, low inflation, currency strength and a split vote in October suggest room for future monetary easing. However, we expect the BoT to keep its policy rate at 1.50%, with cuts possible in 2026. Governor Vitai Ratanakorn has signaled caution, citing limited policy space and doubts about stimulus effectiveness. We will monitor upcoming macroeconomic forecasts. As of October 2025: GDP growth is projected at 1.6%, headline CPI at 0.5%, core CPI at 0.9%, a $13 billion current account surplus and 35 million tourists.

Indonesia, BI (Wednesday, December 17): BI is expected to keep its policy rate unchanged at 4.75% and is maintaining an easing bias. The priority remains improving the credit and interest rate transmission mechanism. Over the past month, average lending rates stayed elevated at 14.3% (from 14.5% on November 19). The central bank is likely to reiterate its “all out pro-growth” stance through a triple-intervention strategy in spot FX, domestic DNDF, and both government bond and offshore rupiah (IDR) markets.

Taiwan, CBC (Thursday, December 18): The CBC is expected to maintain rates at 2% with a neutral stance. All eyes will be on the CBC’s latest macro forecast, following persistent consensus-beating exports data. As of September 2025, the CBC forecasts 2026 GDP at 2.68% (versus DGBAS at 3.54%), and headline CPI at 1.66% (versus DGBAS at 1.61% y/y). We expect the CBC to hold the reserve requirement ratio steady and keep real estate-related loans unchanged.

Sweden, Riksbank (Thursday, December 18): The Riksbank is expected to keep rates on hold at 1.75% though divergence from the ECB is possible as inflation continues to surprise to the downside. Underlying inflation remains at 2.4%, with stronger services and wage growth supporting a more optimistic cyclical view. Policymakers still view the SEK as undervalued, but if the ECB pivots more strongly, current valuations may limit appetite for additional exposures.

Norway, NB (Thursday, December 18): NB remains one of the G10 names where markets are watching for early hikes. However, recent comments from peers, including the BoC and ECB, suggest hikes remain a distant risk. Core inflation fell by more than expected in November on a sequential basis, supporting a neutral stance in the near term. A marginal improvement in global oil demand could shift expectations for terms of trade.

U.K., BoE (Thursday, December 18): The BoE is expected to cut rates by 25bp to 3.75%, as markets increasingly price in a dovish path as the monetary policy committee continues to digest the implications of fiscal consolidation. Governor Bailey recently pointed to elevated levels of precautionary saving as a sign of consumer caution. As the potential casting vote on a split Monetary Policy Committee, Bailey’s preference for a cut appears clear. However, future moves will depend on the inflation path, and hawkish members continue to raise concerns above inflation persistence.

Eurozone, ECB (Thursday, December 18): The ECB is expected to keep rates steady while raising economic forecasts, as flagged by President Christine Lagarde in a recent speech in London. Similar comments from policymakers like Isabel Schnable and Francois Villeroy de Galhau contrast with a more cautious industry tone. Nonetheless, services’ output and inflation remain elevated, which could require a policy shift. The latest staff projections are also expected to show greater tolerance for EUR strength.

Czechia, CNB (Thursday, December 18): Despite another surprise sequential contraction in prices in November, the CNB is expected to hold rates at 3.5% to maintain a positive real rate buffer. Czechia is the only CEE economy not currently struggling with fiscal dominance risks. However, its alignment with the Eurozone cycle means a potential ECB pivot could influence CNB expectations, especially if industrial indicators improve. For now, domestic demand remains robust, and real wage growth continues.

Mexico, Banco de Mexico (Banxico) (Thursday, December 18): Banxico is expected to continue easing, with a 25bp cut bringing the overnight rate to 7%. With core inflation near 4.5%, the real rate buffer is present. However, markets may question the capacity for further cuts if there are any upside inflation surprises. The Fed’s current stance offers some breathing room, and Mexico’s trade outlook will also matter, given its exposure to the U.S. The recent 50% tariff hike on Chinese imports may also influence inflation expectations over the medium term.

Japan, BoJ (Friday, December 19): After much deliberation since the new government was sworn in, markets expect the BoJ to hike rates by 25bp, to 0.75%, offering much-needed relief to bond markets and the JPY, which has stabilized after material outflows since the September LDP leadership election. However, strong fiscal stimulus and the government’s preference for very moderate tightening suggest risks remain skewed toward renewed outflows from Japanese assets, even as valuations support the case for increased holdings, both domestically and globally.

Colombia, Banco de la República (BdlR) (Friday, December 19): The BdlR is expected to keep rates at 9.25% as rising risk premia tied to U.S. trade relations drive asset volatility. High nominal and real rates remain the central bank’s baseline stance. Even with real rates near 4%, easing capacity is limited ahead of the upcoming election. Domestic data remain robust, however, with the urban unemployment rate near record lows.

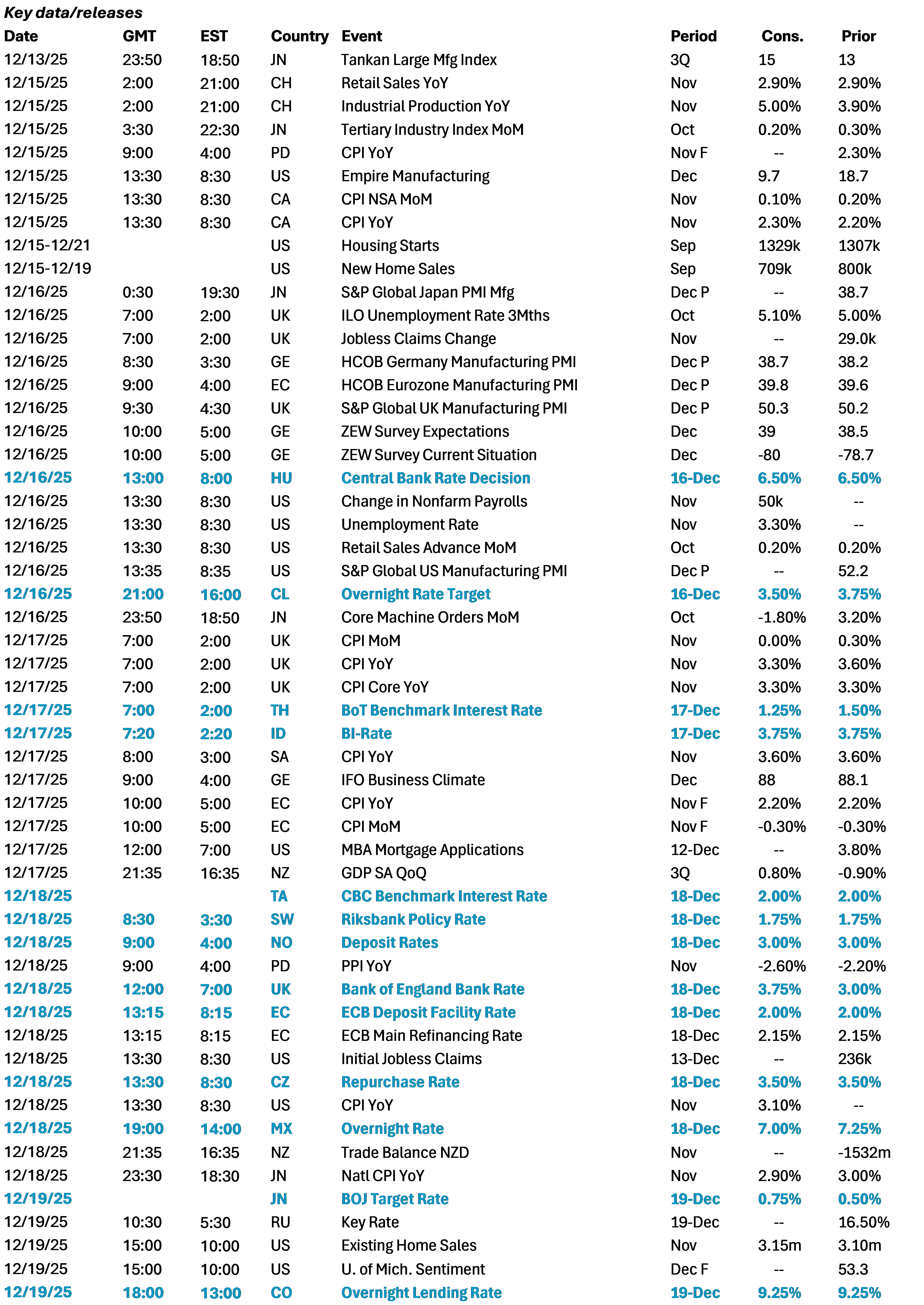

Data Calendar

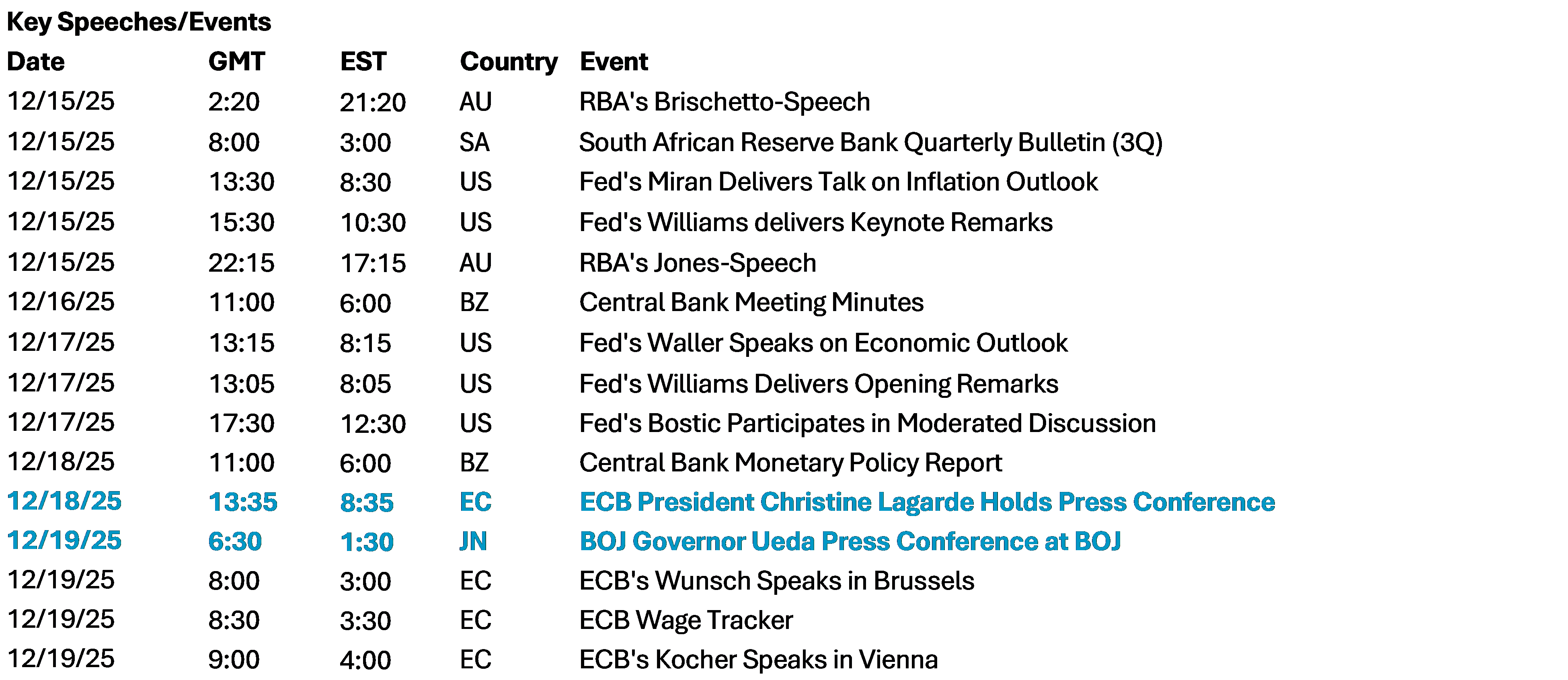

Event Calendar