Liquidity and Rotations at Holiday Crossroads

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

The holidays beckon, but money knows no holiday. This week will pivot on liquidity to supply the now-expected “Santa Claus” rally in risk. Markets will also have a steady stream of economic data to consider – from the Reserve Bank of Australia’s meeting minutes to U.K. GDP, and from inflation reports in Japan, Singapore and Mexico to U.S. durable goods orders and industrial production.

The final week of the year will bridge U.S. retail sales and global manufacturing Purchasing Managers’ Indexes (PMIs). The results will set the pace for global growth in 2026, measured against the rebalancing of risks.

There are three key themes to watch:

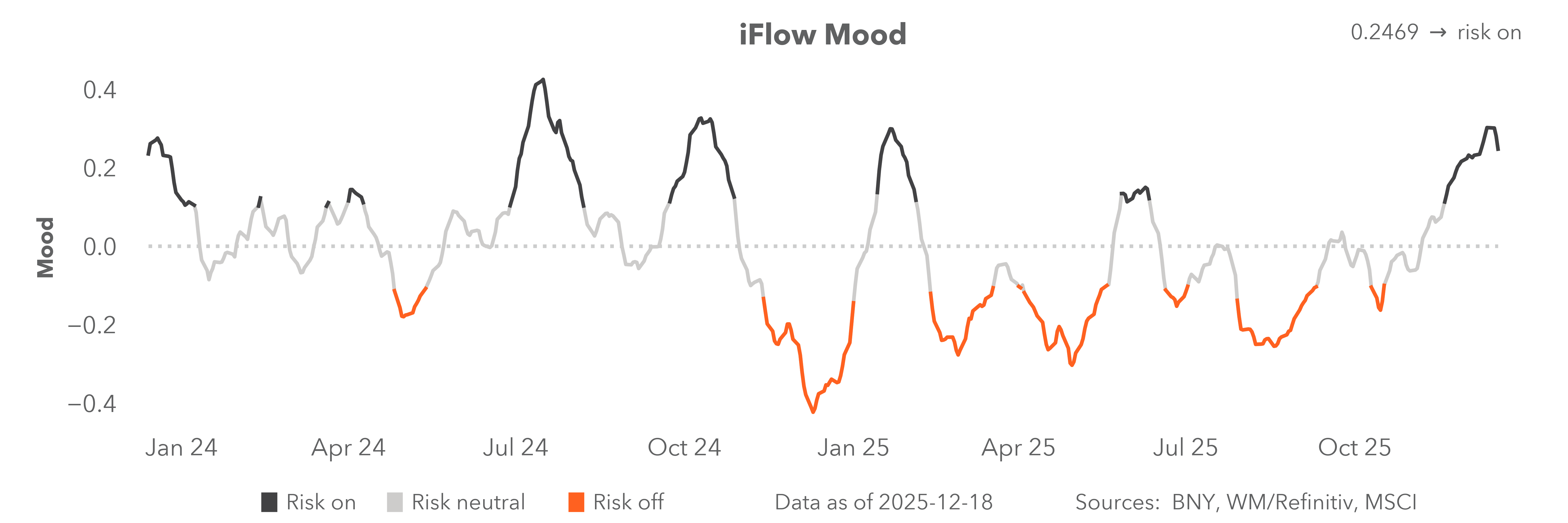

· Rotation trades are shifting from the Magnificent 7 to the other 493 shares in the S&P 500, and from U.S. to “rest of world” value trades. The iFlow Mood index appears to be topping out just into the new year. The same risk appears in carry trades, as 2026 brings a greater focus on factor-driven markets over interest rate spreads.

· IPOs and M&A remain important to equities globally, as will foreign direct investment flows and business investment plans. The Q4 earnings confessional period, ahead of reports from the middle of January, will be crucial for risk management.

· USD downside bias continues, as equities melt up and rates grind down. Dollar hedging is likely to rise into the new year. A breakout from recent ranges would require a shock from an unknown unknown risk, with EUR 1.18, JPY 154, and GBP 1.35 all in play.

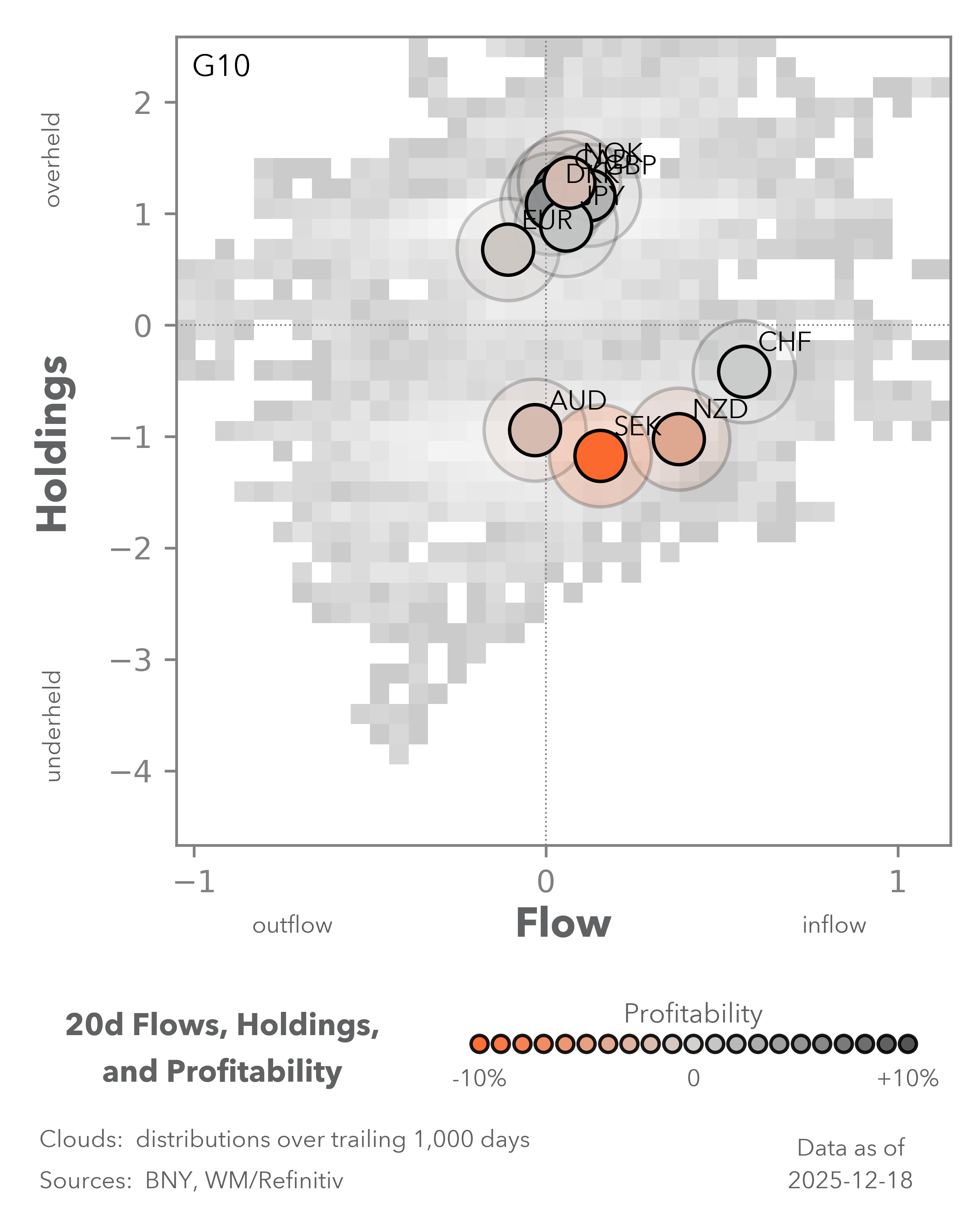

Is there enough cash on the sidelines to buy the dip?

EXHIBIT #1: U.S. IFLOW HOLDINGS OF CASH, BONDS AND STOCKS

Source: BNY

Our take: The last two weeks of 2025 will be filled with holiday cheer, a lack of active trading and less news – yet persistent volatility. This period begins with fixed income markets, including U.S. Treasury coupon supply, and continues with yet more data.

Current U.S. equity holdings are 3% above the 10y average. Fixed income is 4% below average, and cash is 3% below. The focus on U.S. cash is notable this time, given recent Fed rate cuts and lingering uncertainty over easing plans for January and beyond. Recent economic data, along with Fedspeak, suggest the Fed is more likely to wait in January, unless upcoming reports on holiday spending or the December jobs data due Friday, January 9, shift the outlook. What stands out in iFlow cash holdings is the divergence between foreign and domestic accounts.

Forward look: Average current cross-border cash holdings are 29% below the 10y average. The implication is if there is a dip to buy in U.S. bonds or stocks early in 2026, or a surprise later in the year, it will likely be domestic investors stepping in to save the day. Overall, cash levels are 8% above their 2022 lows. The more likely scenario for risk involves fixed income, where any clarity on Fed policy could push markets toward a more normalized asset allocation for 2026. Bond holdings reflect doubts about Fed policy, risks of a potential 2026 government shutdown and increased demand for cash from the rest of the world. The lack of cross-border USD holdings reflects foreign investors’ need for domestic cash, as global rate cycles turn toward tightening – starting with Japan, continuing with Australia, and potentially extending to the European Central Bank (ECB).

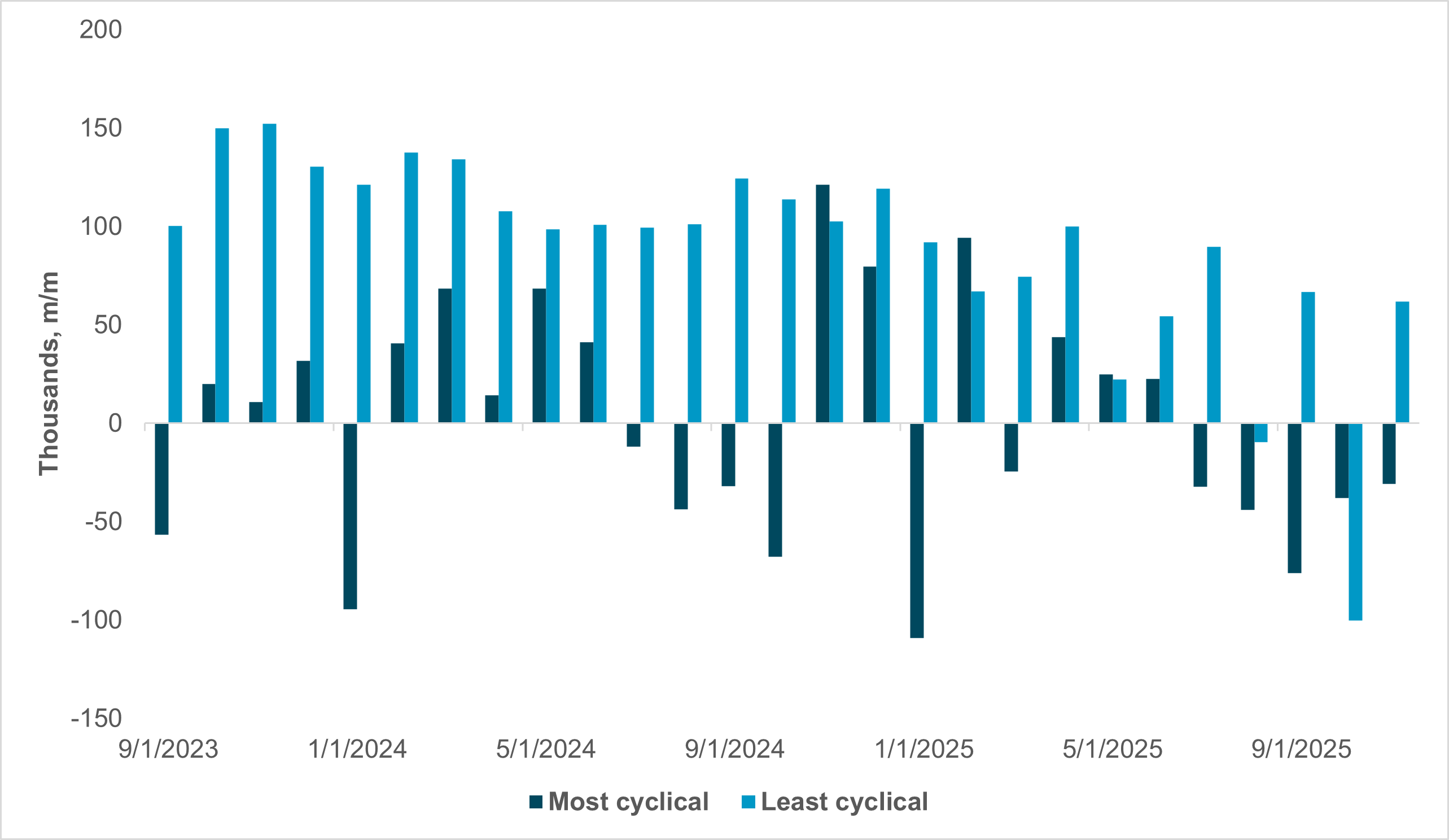

U.S. jobs remain central to a soft patch or a bumpy landing

EXHIBIT #2: CYCLICAL VS. NON-CYCLICAL U.S. EMPLOYMENT

Source: BNY, Bloomberg

Our take: The worry for investors and U.S. markets continues to rest on consumers and jobs. Last week brought jobs and CPI data, with non-government payrolls in line and inflation appearing tame. The path to additional Fed easing appears clear, but the urgency may hinge on the January 9 jobs report. A Dallas Fed study classified employment sectors into three categories: “most cyclical,” “moderately cyclical” and “least cyclical.” Most cyclicals include transportation and warehousing, arts and entertainment, construction, durable goods, and manufacturing. Moderately cyclical sectors include retail trade, nondurable manufacturing, accommodation, and wholesale trade. Least cyclical sectors include government, health care, and education.

Exhibit #2, highlights the monthly job changes in the most versus least cyclical sectors. Cyclical employment has deteriorated for five straight months, posting negative growth during that period. U.S. equity markets reflect a defensive-over-cyclical bias in outlook.

Forward look: The next two weeks will focus on retail sales and durable goods orders. Liquidity will also be a focus, with $183bn in 2y, 5y and 7y coupons, along with the usual T-bill sales. Consumer behavior and holiday shopping trends will be closely watched, as will retail sector profitability reports. Politics may continue to matter, but more likely around the dinner table, as families compare notes on the economy and outlook for next year.

EMEA: Draghi report must return to the fore across Europe

EXHIBIT #3: RELATIVE PRODUCTIVITY – U.K., GERMANY AND FRANCE VS. THE U.S.

Source: BNY

Our take: Final 2025 policy decisions across Europe signaled surprising growth resilience, though central banks continue to struggle with inflation pressures. The Bank of England avoided extrapolating recent demand-side data weakness into a prolonged easing cycle. Sweden and Switzerland are broadly following the ECB’s lead in ending easing, aiming to avoid premature rate hikes.

Yet, the risk is that the region will continue to struggle to generate “non-accelerating inflation” growth, and the specter of stagflation will not go away. While worst-case scenarios from trade and fiscal stress have been avoided for now, generating structural improvements in competitiveness, with productivity growth at its core, remains elusive. Due to the focus on trade matters and the more recent push for a settlement in Ukraine, the European Union’s domestic reform agenda, with productivity growth at its heart, has faded into the background. The U.K. is similarly struggling, and downward revisions in productivity growth were a critical factor behind the 2025 budgetary adjustment. The warnings from the Draghi plan on competitiveness apply across the region: “An environment of historically high public debt-to-GDP ratios, potentially higher real interest rates than seen in the last decade, and rising spending needs for the decarbonization, digitalization and defense, stagnant GDP growth could eventually lead to public debt levels becoming unsustainable and Europe being forced to give up one or more of these goals.”

Relative productivity for the U.K., Germany and France, compared to the U.S., has fallen sharply over the past three decades (Exhibit #3), and OECD forecasts still point to difficulties in reversing this divergence. ECB President Christine Lagarde announced during her December press conference that AI-based investment was contributing to Eurozone growth and driving upward forecast revisions. This does point to a more optimistic scenario surrounding potential productivity gains. We believe the U.K. will see similar benefits, but reconciling AI-driven growth with a social contract that differs from the U.S. presents challenges, especially given weak political mandates in the largest economies. This is even before considering the impact on the manufacturing sector from trade imbalances with China.

In the absence of data over the holiday period, it will be a time for reassessment of policy priorities. Despite ongoing external uncertainties, domestic reform, at both the national and EU level, must swiftly return to the top of policy agendas.

Forward look: The holiday period is unlikely to see much ECB movement, but diplomacy is expected to remain frantic as all parties push for a resolution in Ukraine. There is also a significant amount of legislative work to complete in Western Europe, especially related to budgets, and we doubt that the market’s tolerance for fiscal dominance risk will ease anytime soon.

There are two main risks for Eurozone assets. First, the positioning setup is now quite different from the start of 2025. The euro (EUR) is not only richly valued but is no longer excessively under-owned or over-hedged. Sovereign bonds have also generally performed well throughout the year.

This means the bar for a renewed sell-off across asset classes is extremely low. While increased German issuance is welcome, and the budgetary outlook is positive for Italy and Spain, France’s failure to improve fiscal credibility – combined with additional signs of stagflation – will likely lead to more defensive asset allocation strategies. The significant pick-up in FX hedging across Eastern European economies is already a case in point. However, there have been no efforts to exercise restraint due to local political needs.

ECB President Lagarde noted during her press conference that the central bank was “paying attention” to the RMB. However, she declined to comment on whether its nominal and real valuations would factor into their outlook, in line with the Governing Council’s general stance on exchange rates.

The December ECB staff projections indicate that EURUSD could rise to 1.27 by 2028, but this would only generate a cumulative 50bp downside risk to their baseline inflation scenarios. However, it may also be time to model the effect of EURCNY, particularly through the PPI channel, where political pressure to push back against EUR strength is likely to be strongest.

For now, we do not expect European policymakers or the European Council to take a strong stance on the matter. If China walks the walk on boosting domestic demand, increased imports of goods and services should begin to eat into broader balance of payments and offer some relief to the Eurozone. Assuming a turnaround in Chinese PPI and successful productivity in the Eurozone and European Union, the ECB’s current forecasts should hold.

We expect the ECB mantra of being “in a good place” to persist through the first few meetings. But the proof will be in the data, and the risk remains that geopolitical or structural challenges may soon move beyond the ECB’s control.

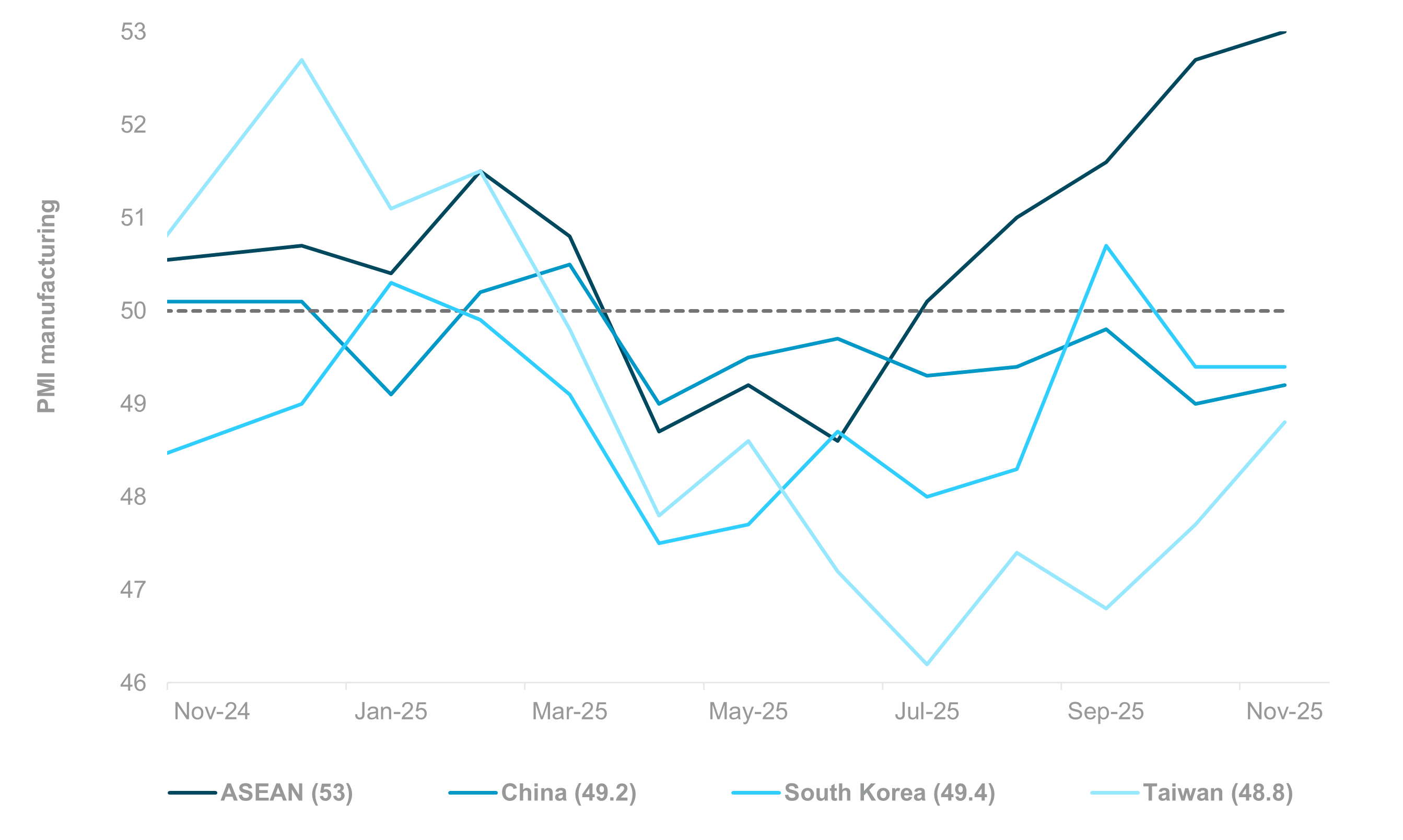

APAC: Regional PMI and CPI in focus

EXHIBIT #4: NORTH ASIA BUSINESS SENTIMENT LAGGED ASEAN RECOVERY

Source: BNY, Bloomberg

Our take: In the Asia-Pacific (APAC) region, attention through year-end will center on the release of December PMI figures, as well as regional inflation data from South Korea, Malaysia, Indonesia, Singapore and Japan. South Korea, Taiwan, Thailand, the Philippines and Indonesia are scheduled to publish updated trade and export statistics. Additional data releases include South Korea’s industrial production, retail sales and consumer confidence; Singapore’s Q4 home prices and industrial production; Philippine bank lending metrics; and growth rates for India’s eight core industries. Japan will also release housing data, unemployment rates, retail sales, industrial output, and December Tokyo inflation.

Japanese economic data will be particularly influential in shaping near-term interest rate expectations. Furthermore, it will be important to monitor the fiscal implications for long-term government bond yields, especially given gradual adjustments in interest rate expectations.

Despite robust growth in AI-related exports and strong equity market performance, manufacturing PMI sentiment in South Korea and Taiwan has remained subdued. South Korea experienced a brief expansion in September but subsequently returned to contraction territory. In Taiwan, the manufacturing sector’s PMI registered nine consecutive months of contraction, standing at 48.8 as of November. Sentiment recovery in China has stalled alongside weakening macroeconomic conditions, including a negative y/y growth rate in fixed asset investment, slowing credit expansion, weaker retail sales, and declining home prices. We will closely monitor service and construction activity within the non-manufacturing PMI. Both currently remain in contraction territory, at 49.5 and 49.6, respectively. On a more positive note, manufacturing and business sentiment in other parts of the region have rebounded significantly. The ASEAN manufacturing PMI reached a record high of 53.0, driven by stronger growth in output and new orders.

Regional inflation trends merit close attention, particularly given declining commodity prices alongside currency volatility in South Korea. In November, South Korea recorded CPI and core CPI values of 2.4% and 1.97%, respectively. The Bank of Korea (BOK) has cautioned that sustained weakness in the won may drive inflation above forecasted levels, which could significantly affect policy decisions in 2026. Singapore’s November CPI is under scrutiny following a notable increase in core inflation, which rose from 0.4% in September to 1.2% in November. Continued upward momentum in inflation and GDP growth could prompt the Monetary Authority of Singapore (MAS) to adopt a fully neutral stance. The MAS currently projects both headline and core inflation to remain within the 0.5%-1.5% range in 2026. Regarding Indonesia, Bank Indonesia has downplayed recent increases in inflation – headline and core rates in November reached 2.72% and 2.36%, respectively – and maintains a dovish outlook, reiterating its intention to seek opportunities for further interest rate cuts.

There will be no central bank meetings for the remainder of the year. Regional monetary policy meetings will kick off in January, starting with the BOK, Bank Negara Malaysia, Bank of Japan and the MSA.

Forward Look: Trading conditions are expected to remain thin and volatile as we approach year end. However, our outlook for APAC heading into 2026 remains constructive. Given subdued growth projections for China, there is a strong possibility of early strategic positioning to build momentum in the first half of the year. This may result in positive growth surprises, particularly in high-tech development and domestic consumption. The Chinese yuan (CNY) is anticipated to benefit from renewed foreign equity inflows and favorable valuations.

In December, profit-taking outflows were especially notable in Taiwan and South Korea. This contrasts with steady, inflow-driven performance in Southeast Asian currencies, including the Malaysian ringgit (MYR), Singapore dollar (SGD), and Thai baht (THB).

We view these outflows as temporary and expect investors to re-enter the market early in the new year to capitalize on continued strength in semiconductor-related exports.

As markets transition into 2026, liquidity conditions, policy expectations and positioning imbalances will define early-year performance across asset classes. While holiday trading remains thin, the underlying signals – deteriorating cyclical employment in the U.S., constrained cross-border cash balances, and persistent divergence in global productivity – underscore a year that will require disciplined risk management.

Domestically, rate-cut timing will drive fixed-income recalibration and equity factor leadership, particularly as rotation away from megacaps broadens. Abroad, Europe’s structural competitiveness challenges and APAC’s uneven manufacturing sentiment create differentiated opportunities but also amplify sensitivity to policy missteps.

A weaker USD bias provides support for global risk assets, yet its path will hinge on growth resilience and the absence of geopolitical shocks. For finance professionals, early 2026 will be less about chasing momentum and more about assessing where liquidity, policy credibility, and structural reform can sustainably support earnings. Tactical flexibility will be essential as markets rebalance.

Central bank decisions

There will be no central bank decisions during the holiday period.

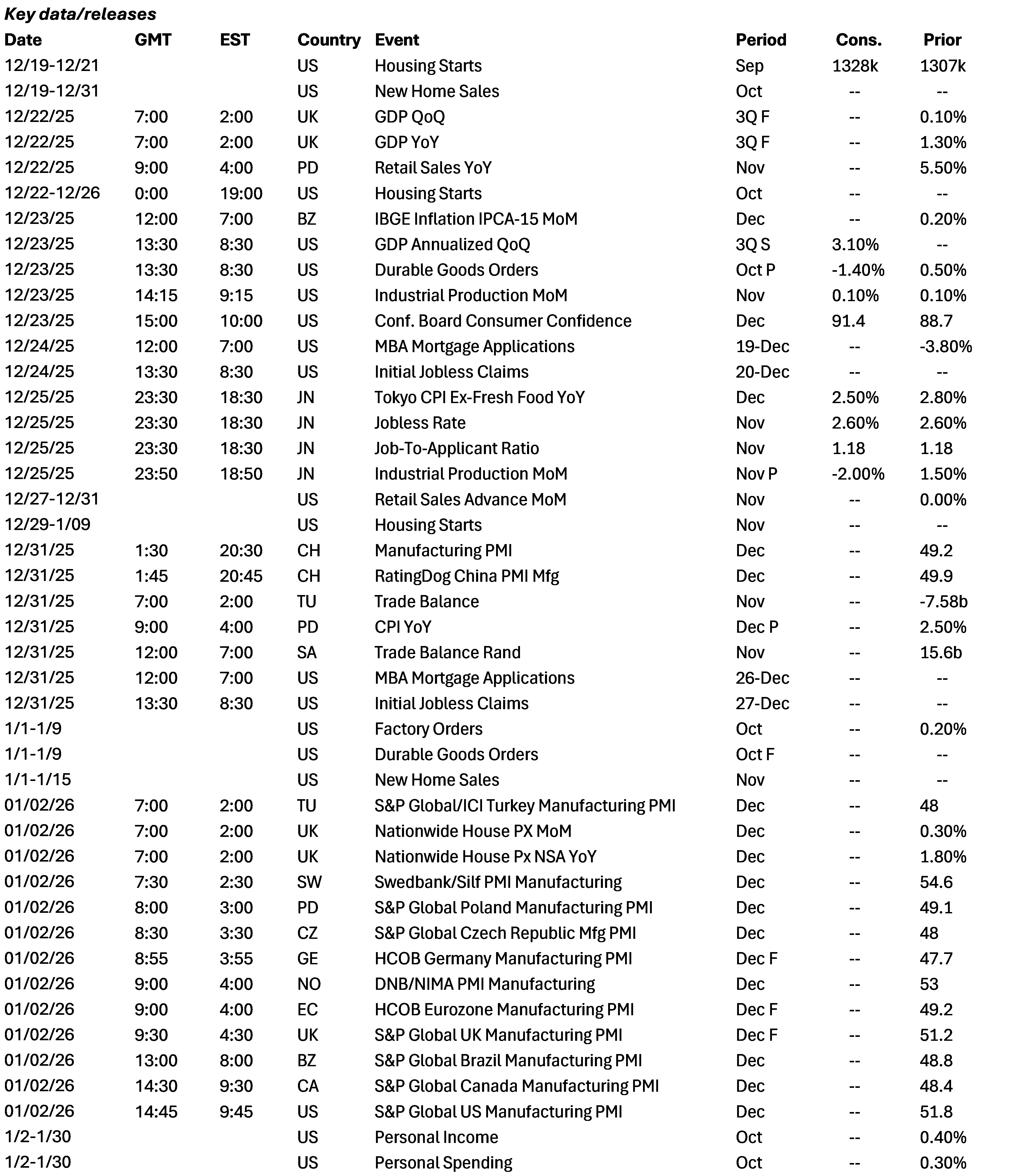

Data Calendar

Event Calendar