Market Movers: Ticking Clocks

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

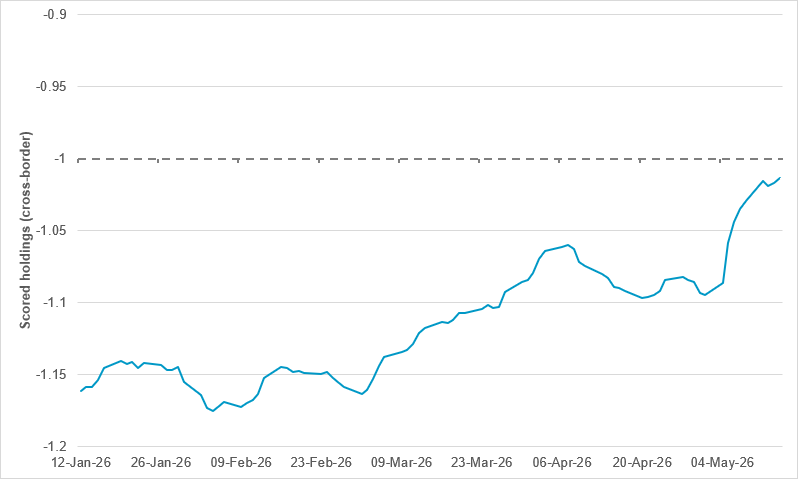

Dollar hedges shrinking back to rolling 12-month average

Source: BNY

While the conflict and growing inflation concerns remain the dominant global market themes, the market should also not lose sight of idiosyncratic themes that, at least in theory, have been in place since well before the current supply shock. Some are secular themes, whereas others are linked to localized issues such as elections or policy shifts.

The “hedging the U.S.” factor was a major driver at the beginning of the year. While investors were happy to maintain or even add to U.S. exposures on the back of AI investment-driven growth, that exceptionalism did not extend to the dollar. The Fed was seen as leading easing expectations and broadly easier financial conditions on a relative basis. Relative to asset price movements, iFlow’s cross-border USD holdings figures were at fairly low levels at the start of the year. However, these positions have faced stress since the end of February, with many prior assumptions being revisited. Toward mid-May, USD hedges underwent a new wave of unwinding, and cross-border holdings are now approaching the same level as the rolling 12-month average. This means that incremental hedging is no longer stronger than last year’s levels. Even with conflict resolution, the prospect of policy differentials no longer driving hedging interest could market a major shift in asset exposures.

The new week has brought with it broadening risk-off trading. Equities were down in APAC and EMEA, and U.S. futures were flat. Bonds were a mixed bag, with South Korea and New Zealand recording rises of 7-9bp in 10y yields, while the U.K. dropped 3bp and the U.S. was flat. USD is flat, with notable exceptions in emerging markets where IDR and INR both hit record lows and KRW dropped 1.6%, while NZD and GBP gained ground. The clock is ticking on escalation fears for the Iran conflict, as oil supply shocks widen.

Bottom line: The week ahead will bring the FOMC minutes and a debate about rate hike risks, along with earnings reports from NVIDIA and Walmart. The period of waiting may be coming to an end: investors want to see AI investments matched by earnings and ongoing demand. Digital timepieces don’t tick; they flicker. The worries about oil prices and demand destruction also hang over markets, and that threat will only increase the ticking sound and costs of waiting. Today’s U.S. session faces the ongoing toll of the Iran conflict on global growth, with more urgency emanating from bond markets as they reflect the higher inflation and weaker expansion numbers globally. Whether productivity and AI can manage to offset this will be a key alarm bell for traders.

G7 finance ministers and central bank governors meeting in Paris are set to focus on mounting inflation risks, bond market volatility and widening global economic imbalances following a sharp selloff in sovereign debt markets linked to the Iran conflict and rising energy prices. French Finance Minister Roland Lescure is expected to push for greater coordination on responses to inflation shocks and reducing vulnerabilities in the global economy, while acknowledging significant disagreements within the group, particularly with the U.S. Discussions are also expected to center on trade imbalances, with France arguing that China under-consumes, the U.S. over-consumes and Europe under-invests. Officials are also expected to prioritize coordination on critical minerals and rare earth supply chains to reduce dependence on China, while reviewing the implications of the recent Trump-Xi summit and escalating geopolitical tensions. S&P Mini -0.39% to 7404, DXY -0.076% to 99.209, 10y UST +0.5bp to 4.598%.

Hungarian President Tamás Sulyok has rejected mounting political pressure to resign, insisting that his constitutional mandate obliges him to serve the entire nation and that there is no legal basis for stepping down. Responding to criticism from Prime Minister Péter Magyar and the governing Tisza Party, Sulyok argued that claims of being “unfit” or “unworthy” are political judgments with no constitutional standing. He said recent political developments reflect a broader attempt to reinterpret the role and powers of the presidency rather than a constitutional crisis, while maintaining that Hungary remains a democratic state governed by the rule of law. Sulyok acknowledged that future political demands could eventually lead to legal changes redefining the presidency but stressed that he will continue fulfilling his duties under the current constitutional framework. Budapest SI +0.1% to 131833, EURHUF -0.263% to 360.87, 10y HGB +8bp to 5.58%.

UAE Energy Minister Suhail Mohamed Al Mazrouei has said the country’s decision to leave OPEC and OPEC+ was a strategic economic move based on national interest, not political reasons. The move reflects the UAE’s long-term economic vision, evolving energy sector capabilities and commitment to global energy security and market stability. Previously producing over 3 million barrels per day (bpd), the UAE’s output has dropped to 1.8-2.1 million bpd due to the conflict in the region. Abu Dhabi is accelerating the West-East pipeline project to double export capacity by 2027, aiming to bypass the Strait of Hormuz and enhance energy supply resilience. Brent +0.65% to 109.97, WTI +0.911% to 106.38, Omani crude +1.747% to 106.61, Dubai crude +1.748% to 104.398.

The Trump administration has allowed the sanctions waiver on some Russian crude oil sales to expire, ending a brief easing period despite tight global oil markets caused by the Iran war. The waivers, initially issued in March and April, were controversial, with European allies supporting sanctions to cut Russian revenue, while countries such as India and Indonesia lobbied for extensions. Treasury Secretary Scott Bessent noted that vulnerable countries sought the waiver to stabilize energy markets. The administration may reconsider issuing a new waiver due to ongoing market tightness and ally lobbying. A separate Iranian crude purchase waiver also expired in April.

U.S. May New York Fed Services business activity is expected at -12 vs. -14.0.

U.S. May NAHB Housing Market Index is expected to hold at 34.0 vs. 34.0.

U.S. Treasury sells $89bn in 13-week bills and $77bn in 26-week bills.

Mood: iFlow Mood slipped deeper into risk-off territory at -0.161, the weakest level since October 2025, driven by fading equity demand alongside selling pressure in core government bonds.

FX: EMEA currencies were broadly sold, while flows across the rest of the iFlow universe were mixed and moderate. EUR, AUD, NZD and USD attracted inflows, while DKK, HUF and GBP saw the largest outflows.

FI: Selling pressure was concentrated in Australian and Japanese government bonds. In contrast, Eurozone and Colombian government bonds, alongside U.K. gilts, saw solid demand, while U.S. Treasurys were bought modestly.

Equities: G10 equities were broadly sold, led by Sweden, the Eurozone and Japan. Flows across EMEA and LatAm were mixed and moderate, while APAC saw wider dispersion. Chinese and Thai equities attracted strong buying, whereas South Korean equities faced aggressive outflows.

“The clock of life is wound but once, and no one has the power, to tell just when its hands will stop, at late or early hour." – Robert H. Smith

“Time management is an oxymoron. Time is beyond our control, and the clock keeps ticking regardless of how we lead our lives. Priority management is the answer.” – John C. Maxwell

Italy’s trade data for March showed strong export and import growth, with exports rising 4.1% m/m and 7.4% y/y in value terms, while imports increased by 4.8% m/m and 8.0% y/y. Export growth was driven mainly by metals, refined petroleum products, automobiles, electronics, pharmaceuticals and machinery, with particularly strong demand from Switzerland, France, Germany, Spain and China. In contrast, exports to OPEC countries and Türkiye declined sharply. The trade surplus remained broadly stable at €4.7bn, with non-energy trade continuing to offset the energy deficit. Import prices rose sharply m/m due to higher energy and intermediate goods costs, while annual import price growth turned slightly positive, ending a prolonged period of declines. FTSE MIB -1.92% to 48174, EURUSD +0.078% to 1.1634, 10y BTP +0.2bp to 3.949%.

Spain’s property transaction data for March revealed mixed housing market conditions, with total property transfers rising 2.7% y/y while registered home sales declined by 2.2%. Overall registered property sales increased modestly, supported by gains in rural and non-residential urban properties, but residential transactions weakened, particularly in new housing, where sales fell 10.2% y/y. Existing home sales were broadly stable, rising slightly from a year earlier. Free-market housing continued to dominate transactions, while sales of protected housing declined sharply. Regional divergence remained pronounced, with Castilla La Mancha, Navarra and La Rioja recording the strongest increases in home sales, whereas Cantabria, the Basque Country and the Canary Islands posted the steepest declines. IBEX 35 -0.34% to 17534, EURUSD +0.078% to 1.1634, 10y Bono +0.2bp to 3.606%.

U.K. house prices showed unexpected resilience in May, Rightmove has reported, with the average asking price for properties coming to market rising 1.2% m/m, exceeding the typical seasonal increase and contrasting with softer signals from other housing indicators. Despite this, market conditions remain highly competitive, with buyer choice at its highest level for this time of year since 2015 and nearly one-third of listed homes undergoing price reductions. Rightmove warned that over-ambitious pricing is extending selling times significantly. Regional divergence remains pronounced, with stronger price growth in more affordable northern regions, while London and the South East continue to weaken amid affordability pressures. Although sales activity remains relatively stable compared with last year, the market continues to depend heavily on mortgage availability, particularly for first-time buyers. FTSE 100 -0.03% to 10192, GBPUSD +0.203% to 1.3353, 10y gilt -2.2bp to 5.15%.

Switzerland’s economy expanded by 1.4% in 2025, slightly stronger than the previous two years but still below the long-term average growth rate, while GDP per capita rose by 0.5%. Growth was supported mainly by the services sector, particularly finance and trade, whereas manufacturing continued to weigh on activity amid weak European industrial demand, elevated uncertainty from higher U.S. tariffs and a strong Swiss franc. Despite these headwinds, the Swiss economy showed resilience, with GDP standing 11.2% above pre-pandemic 2019 levels, outperforming the euro area though lagging the U.S. GDP per capita was estimated to be 4.8% above 2019 levels, reflecting moderate long-term gains and maintaining Switzerland’s position among the world’s highest-income economies. SMI -0.57% to 13144, EURCHF -0.139% to 0.91347, 10y Swiss GB +3.4bp to 0.569%.

The Swedish Riksbank’s April survey of money market participants showed inflation expectations remaining broadly anchored near target over the medium term, despite some easing in short-term expectations. CPI inflation expectations for one year ahead declined to 1.7% from 2.1% previously, while two-year and five-year expectations remained close to 2.2%. CPIF expectations showed a similar pattern, with shorter-term expectations softening but longer-term expectations stable around target. Participants continued to expect gradual policy tightening over time, with the policy rate seen rising from 1.8% in three months to 2.4% over five years. GDP growth expectations remained around 2% across forecast horizons, while the krona was expected to strengthen moderately against both the euro and the U.S. dollar. OMX -0.54% to 3020, EURSEK -0.15% to 10.9754, 10y Swedish GB +2bp to 2.948%.

New Zealand’s services sector contracted at a gentler pace in April, with the BusinessNZ Performance of Services Index (PSI) rising to 48.9 points from 46.2 in March. Over two-thirds of respondents cited negative factors, notably rising fuel prices linked to the conflict affecting shipping through the Strait of Hormuz. While the new orders sub-index expanded to 51.2 (March: 46), other sub-indexes, including supplier deliveries (46.6; March: 47.2), activity sales (48.9; March: 44.7) and employment (48.5; March: 46.6) contracted. Micro-businesses faced significant challenges (44.4), whereas medium-sized to large firms expanded at a healthy pace (55.5). The data reflect ongoing sector weakness amid external pressures. In other figures, non-resident bond holdings picked up in April to 58.9% of the total. NZX 50 -1.56% to 12763, NZDUSD +0.24% to 0.5853, 10y NZGB +7.5bp to 4.822%.

Türkiye’s unemployment rate edged down to 8.2% (seasonally adjusted) in Q1, as the unemployment count fell by 52,000 q/q. However, labor market conditions weakened more broadly, with employment falling by 301,000 and labor force participation declining to 52.6%. Employment losses were concentrated in services, construction, agriculture and industry, while the employment rate dropped to 48.3%. Youth unemployment remained elevated at 15.2%, with a particularly high rate among young women. At the same time, the broad underutilization rate increased to 30.4%, indicating persistent labor market slack despite the modest decrease in the headline unemployment rate. BI 100 -1.71% to 14122, USDTRY +0.161% to 45.5798, 10y TGB +29bp to 35.3%.

Türkiye’s consumer confidence index edged up to 85.8 points in May from 85.5 in April, indicating a modest improvement in household sentiment though confidence remained below the neutral 100-point level. The increase was driven mainly by stronger expectations regarding the general economic outlook over the next 12 months, which rose significantly over the month. Expectations regarding future household financial conditions also improved slightly, while intentions to spend on durable goods were broadly stable at a high level. In contrast, assessments of current household financial conditions deteriorated further, highlighting ongoing pressure on household purchasing power despite somewhat improved optimism on the broader economic outlook.

China’s April activity data were broadly soft at headline level, with slower industrial production and retail sales, and continued weakness in fixed asset investment and property. However, high-tech manufacturing and investment remained key growth drivers, reinforcing Beijing’s push toward higher-quality growth. Industrial production growth eased to 5.6% YTD y/y from 6.1% in March, though equipment manufacturing (+8.7%) and high-tech manufacturing (+12.6%) continued to outperform. Production of strategic sectors remained strong, including 3D printing devices (+50.9%), lithium batteries (+36.0%) and industrial robots (+25.7%). Services output rose 4.9% YTD y/y, supported by information technology and finance. Domestic demand remained weak. Retail sales slowed to 1.9% YTD y/y from 2.4%, with urban consumption particularly subdued (+1.8%). CSI 300 -0.54% to 4834, USDCNY -0.169% to 6.8012, 10y CGB -1.3bp to 1.751%.

Green shoots are again showing in Chinese real estate, with used home prices in T-1 cities posting m/m gains for a second month in a row. In April, first-tier cities saw new residential sales prices rise 0.1% m/m, with Shanghai (+0.4%), Guangzhou (+0.1%) and Shenzhen (+0.1%) up, while Beijing prices fell 0.2%. Second-tier city prices were down 0.1% m/m, a smaller drop than in March, and third-tier cities fell 0.3% m/m, unchanged from last month. Overall, new home prices and used home prices in 70 Chinese cities were down -0.19% and -0.23% m/m, respectively. Y/y, new home prices declined across all tiers: -2.1% in first-tier (Shanghai +3.7%), -3.3% in second-tier and -4.1% in third-tier cities. Second-hand home prices in first-tier cities rose 0.4% m/m but fell 6.8% y/y, with similar declines in lower tiers. Within the national accounts, property weakness continued to drag on investment and household confidence. Fixed asset investment fell 1.6% YTD y/y, while real estate investment contracted 13.7%, with property sales and floor space sold still declining sharply. Private investment also remained weak (-5.2% YTD y/y). In contrast, high-tech investment rose 6.1%, led by aerospace, information services and computer manufacturing.

South Korean bank lending to households grew by ₩2.1tn to ₩1.175qn in April vs. +₩0.5tn in March and +₩4.7tn in April 2025, driven mainly by housing-related loans. Home mortgage loans shifted from a small decline to a significant increase (+₩2.7tn), supported by rising housing transactions and demand for intermediate payment financing, offsetting weaker leasehold deposit loan demand (-₩0.6tn in April vs. -₩0.4tn in March). Other loans decreased by ₩0.6tn, reflecting repayments after individual investors’ net stock selling. KOSPI +0.31% to 7516, USDKRW -0.084% to 1496.8, 10y KTB +13.3bp to 4.22%.

South Korea has launched a second round of cash aid targeting the bottom 70% of income earners to alleviate financial pressure from rising fuel prices amid the Middle East crisis. About 36 million people are eligible, with payments ranging from 100,000 to 250,000 won depending on the region. Eligibility is based on March national health insurance payments, with single-person households earning up to ₩43.4mn annually qualifying. Applications are open until July 3, and funds must be used by August 31 at gas stations or small local businesses. The program excludes high-asset and high-financial-income individuals.

A South Korean court has partially granted Samsung Electronics’ injunction against a planned strike by its labor union, requiring the union to maintain safety and product protection operations at normal levels during the strike. This reflects the critical nature of semiconductor manufacturing. The court prohibited facility occupation and imposed daily fines on the union and its leaders for violations. The union plans a general strike over a performance bonus dispute, demanding removal of the 50% bonus cap and the awarding of 15% of operating profit in bonuses. Samsung opposes removing the cap but is offering special rewards if industry leadership is achieved.

Singapore’s external trade grew strongly in April. Non-oil domestic exports (NODX) rose 24.5% y/y, up from 15.3% in March, driven by electronics (+66.7%) including ICs, disk media products and PCs, supported by AI demand. Non-electronics NODX grew 10.9% (March: -0.6%), led by pharmaceuticals and specialized machinery. NODX to the U.S. (59.6% y/y), China (37.8% y/y) and South Korea (71.2% y/y) expanded, while exports to Indonesia (-60.8% y/y) contracted. Non-oil re-exports (NORX) increased by 29.6% (March: +60.8%), mainly attributable to electronics (+41.6%). Total merchandise trade rose 33.1% y/y (March: +38.3%), with exports up 31.8% and imports 34.7% higher. STI -0.15% to 4982, USDSGD -0.063% to 1.2797, 10y SGB +5.8bp to 2.137%.

Thai GDP was up 2.8% q/q in Q1, from +2.5% in Q4 2025, driven by rises of 1.2% in agriculture (Q4 2025: 0.6%) and 3.0% in non-agriculture (Q4 2025: 2.7%). Industrial output rose 1.8% (Q4 2025: 0.9%), led by mining, manufacturing and utilities, while services expanded by 3.6% (Q4 2025: 3.5%), supported by transportation, accommodation, finance and real estate. On the expenditure side, private consumption grew by 3.2% (Q4 2025: 3.3%), government spending by 3.4% (Q4 2025: 1.3%), gross fixed capital formation by 9.9% (Q4 2025: 8.1%), exports by 12.6% (Q4 2025: 5.9%) and imports by 21.1% (Q4 2025: 9.5%). Inventory accumulation occurred in gold, rubber, sugar and electronics. Seasonally adjusted GDP increased by 0.7% q/q (Q4 2025: 1.9% q/q). The Office of the National Economic and Social Development Council (NESDC) projects 2026 GDP at 1.5-2.5%, CPI at 2.0-3.0% and the current account at 1% of GDP. SET +0.1% to 1519, USDTHB -0.083% to 32.623, 10y TGN +5.2bp to 2.214%.

The Thai government under Prime Minister Anutin Charnvirakul is accelerating reforms of economic laws and regulations to remove business obstacles and enhance investment efficiency. Over 7,000 subordinate laws and ministerial regulations will be reviewed for retention, amendment or repeal, with digital systems introduced to reduce procedures and increase transparency. The private sector will propose 10-20 priority laws by early June for government action. The government is also promoting a “Super License” system to simplify permits and shifts from pre-approval to post-operation checks where suitable. These reforms build on successes such as the BOI Fast Pass, which helped investment grow 18% in Q1.

Indonesia’s external debt (ULN) reached $433.4bn in Q1, growing 0.8% y/y, which was slower than Q4 2025’s 1.9% y/y. Government ULN rose 3.8% y/y to $214.7bn, down from 5.5% y/y in Q4 2025, supported by foreign inflows into international government bonds. Key sectors funded include health and social services (22.1%), government administration and defense (20.2%), education (16.2%), construction (11.5%) and transportation (8.5%). Private sector ULN fell 1.8% y/y to $191.4bn, driven by contractions in financial and non-financial corporations. Indonesia’s ULN-to-GDP ratio dropped to 29.5% from 30.0%, with long-term debt dominating at 85.4%. JCI -2.93% to 6527, USDIDR +1.094% to 17656, 10y IDGB +11.7bp to 6.808%.