Market Movers: Reprieve

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Geoffrey Yu

Time to Read: 9 minutes

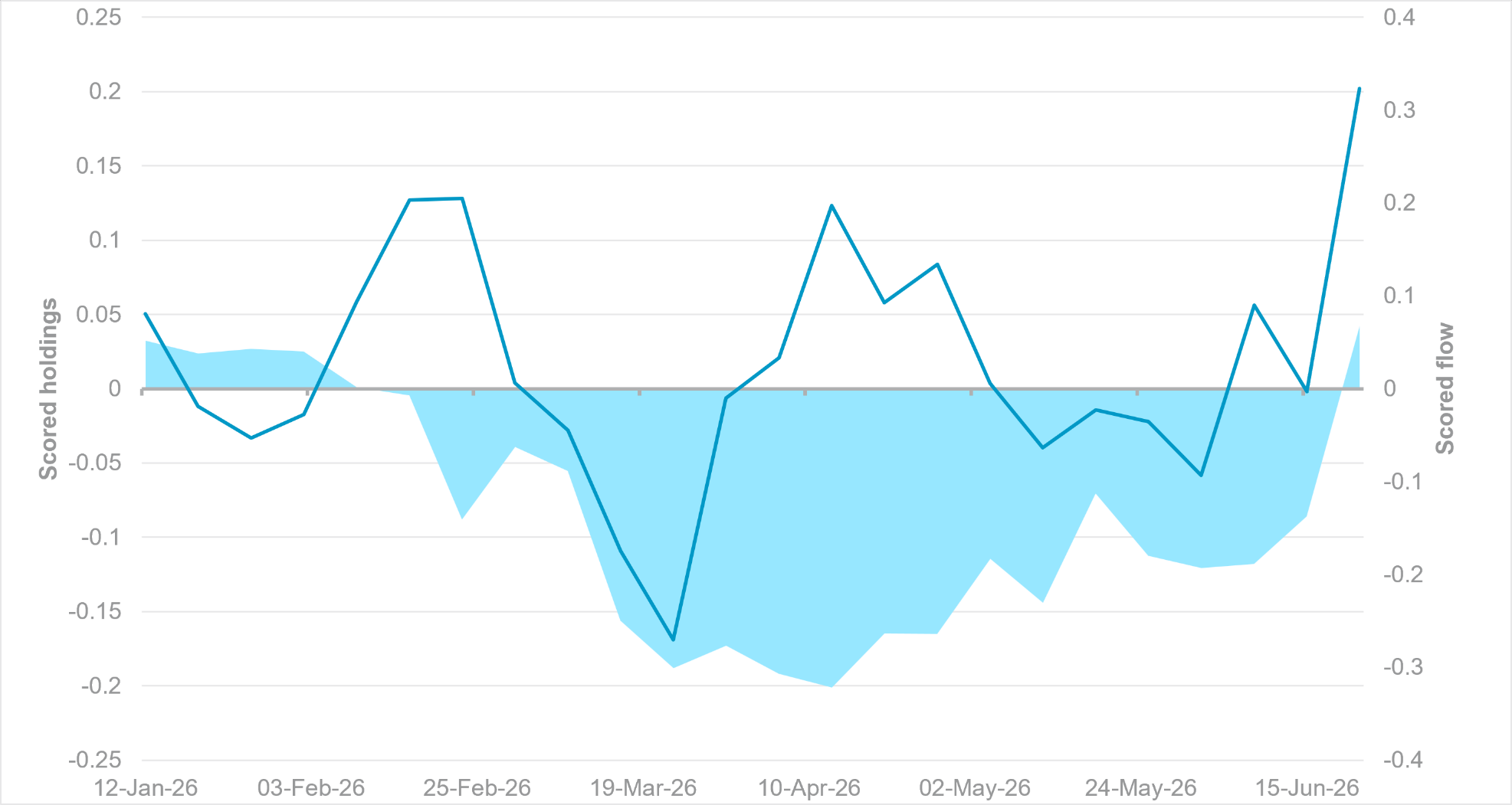

EM APAC FX finally returns to net overheld position as oil prices drop

Source: BNY

The combination of falling oil prices and policy vigilance has finally helped APAC currencies stabilize. Equity outflows from AI/semiconductor-linked markets remains a source of risk, but the main drag on performance – especially in ASEAN nations – has reversed considerably. Our data show that for the first time since early February, EM APAC currencies’ aggregate holdings are back into marginally positive territory. Purchases have accelerated considerably over the past three weeks, and the group was one of the biggest beneficiaries of portfolio adjustments on the June IMM dates.

The drop in import bills means EM economies are looking at significantly better balances of payments ahead, which will ease selling pressure on currencies and help rebuild reserves. In addition, easing supply chain fears will also help regional trade to normalize. This applies especially to refined products, where cessation of exports and other restrictions – particularly out of China – have exacerbated pricing and supply pressures in the region. In addition, central banks across ASEAN should also be commended for asserting their policy credibility despite the constraints. The Philippines and Indonesia have led the way in trying to push up real rates in defense of their currencies.

Challenges remain, and we do not see a sudden pivot in monetary policy stances in the near term. The Bank of Thailand’s decision overnight indicates that even in economies where accommodation is needed, inflation vigilance is stronger than usual. Furthermore, concerns will linger over fiscal positions, which we see as the bigger long-term challenge for a recovery in external positioning across APAC.

Despite another difficult session in Asia, the European and U.S. markets look set for a calmer session as investors look for the latest round of chipmaker earnings to allay fears over valuations and investment needs. The market continues to err on the side of “cracks” in the narrative rather than a full “break,” and further reprieves from supply chain improvements can swiftly be reflected in a pullback in policy expectations. Policy and market developments in South East Asia overnight – which was a major source of balance-of-payments risk in the early days of the war – indicate that the worst effects of the conflict are over. However, the market will swiftly move on from damage limitation to growth expectations, and the latter is a bigger challenge.

Global reserve management is in sharp focus as reports suggest Japan is undergoing a review of its current strategy, including using returns to support strained public finances. Multiple reports have emerged over recent months concerning changes in strategy by Middle Eastern reserve managers and sovereign wealth funds, mostly involving repatriation of overseas assets and greater deployment of reserve assets for domestic purposes. The catalysts are different for Japan and the Middle East, but the drivers are similar: constraints on domestic fiscal policy are emerging (very heavily so in the case of the Middle East) and questions over long-term returns will linger due to high valuations. Consequently, levels of passive rotation overseas, especially into the U.S., may not be as strong as any improvement in current accounts could indicate.

Indonesian equities are now down over 30% YTD, and broader asset outflows remain a challenge to financial accounts across the region. Structural matters aside, markets were particularly focused on the risk of MSCI downgrading the market from emerging market status, which had risked further selling by global index trackers. News of a five-month extension in its review and affirmation of positive steps already taken represent a clear reprieve, but more needs to be done. With volatility from the conflict likely out of the way and a new race emerging to attract global capital, we expect investors to continue to reward markets where the resolve for structural reform is strongest, whereas laggards face high rotation risk.

Supply chain security is now at the front of investors’ minds as conflicts – both in trade and kinetic – are leading to comprehensive reviews of national reliance globally. In the space of 24 hours, U.S. Treasury Secretary Scott Bessent announced a “redefining of US economic statecraft” around economic security, the EU joined Pax Silica – a U.S.-led effort to boost tech supply chains, and Beijing launched comprehensive rules for investigations into supply chain security. The latter rules have a heavy emphasis on dual-use strategic minerals – one of the West’s biggest areas of dependency on China. Ceasefires in the same conflicts are in place, but fragmentation is only increasing, with consequences for various forms of economic equilibrium in the years to come.

Bottom line: The long-term impact of the conflict and global trade/supply re-orientation will require risk premium extraction in asset allocation and for AI to deliver the hoped-for anticipated productivity gains. Meanwhile, investors, ratings agencies and index providers will continue to demand structural reform. For governments, the cost of realizing these is more often political than financial, especially if the benefits only materialize over the longer term. Beyond the technology investment themes, emerging markets are finding favor again, indicating that, for now, investors are giving any such reform plans the benefit of doubt.

U.S. Treasury Secretary Scott Bessent has said the Trump administration is redefining American economic statecraft around economic security, reciprocity and national capacity. Bessent argued that the U.S. must rebuild domestic production in strategic sectors such as semiconductors, AI, shipbuilding, critical minerals and pharmaceuticals, while reducing supply chain vulnerabilities and dependence on foreign chokepoints. He asserted that U.S. openness will increasingly be conditional on fair market access, non-discriminatory treatment and respect for sanctions and financial integrity. Bessent said he is confident that Federal Reserve Chair Kevin Warsh will balance inflation and growth and stressed that President Trump supports the Fed’s independence. He argued that inflation should ease as the Iran conflict subsides, saying lower gas prices will help bring consumer prices back toward target. NASDAQ Mini +0.48% to 29810, DXY +0.175% to 101.585, 10y UST -2bp to 4.477%.

The Ifo Institute has reported that German business sentiment improved slightly in June. Its business climate index rose to 85.6 points from 85.0 in May, a touch above market expectations. The survey, based on about 9,000 monthly business responses, showed firms are becoming a little more optimistic that conflict in the Middle East may ease soon, reducing uncertainty. Even so, the index remains subdued and well below normal levels, after it dropped steeply when the war in Iran erupted. The institute noted that April had recorded the weakest reading since May 2020, when pandemic lockdowns were weighing heavily on the German economy. DAX -0.77% to 24703, EURUSD -0.317% to 1.1346, 10y Bund -1.6bp to 2.903%.

The Japanese government has signaled that it will examine ways to improve management of its $1.3tn foreign exchange reserves, according to a draft growth strategy report reviewed by Reuters. The move reflects Prime Minister Sanae Takaichi’s push for proactive spending, while also seeking higher returns and support for strained public finances. The draft says officials will consider better use of public sector assets, including the foreign exchange fund special account, while respecting their original purpose. After Japan resumed large-scale yen buying intervention in late April, reserves fell sharply in May, underscoring limits on prolonged intervention. The report does not specify portfolio changes, and officials said major shifts would be unrealistic because the reserves must remain available for currency operations. Nikkei -0.88% to 69175, USDJPY +0.137% to 161.77, 10y JGB -0.3bp to 2.676%.

MSCI has granted Indonesia a five-month extension in its review of the country’s market status, delaying any decision on a potential downgrade from emerging to frontier market status until November. While the move removes an immediate risk, MSCI stressed that recent reforms are only a first step and that measurable progress will be required in the coming months. Investors viewed the decision as a reprieve rather than a resolution, with concerns remaining over foreign capital outflows, weak market performance and policy credibility. Indonesian equities have fallen around 30% this year, while overseas investors have withdrawn nearly $4bn. Analysts noted that a downgrade could trigger as much as $13bn of additional outflows. The extension keeps up the pressure on regulators to deliver reforms and improve market accessibility, with investor confidence still fragile amid fiscal concerns and rupiah weakness. JCI -3.56% to 5884, USDIDR +0.55% to 17943, 10y IDGB +3.5bp to 7.217%.

Thailand’s Monetary Policy Committee has unanimously voted to keep the policy rate unchanged at 1.00%, judging that the current accommodative stance remains appropriate despite a near-term rise in inflation. The MPC upgraded its growth outlook, forecasting that GDP will rise by 2.3% in 2026 and 1.8% in 2027, supported by stronger exports, investment linked to the technology and AI cycle, government support measures and easing Middle East tensions. However, policymakers stressed that growth remains weak and uneven, with SMEs and many households still facing significant challenges. Headline inflation is projected to average 2.8% in 2026, temporarily exceeding the target range on higher energy and production costs, before falling to 1.4% in 2027 as supply-side pressures ease. The MPC emphasized that inflation expectations remain anchored but said it would closely monitor cost pass-through and medium-term inflation risks. SET +0.45% to 1548, USDTHB +0.836% to 33.417, 10y TGN -1.8bp to 2.089%.

Malaysia’s Financial Markets Committee (FMC) has said the ringgit’s recent decline was driven mainly by global factors, including renewed expectations of higher U.S. policy rates, stronger dollar hedging and MSCI-related equity rebalancing. It noted that Malaysia’s macro fundamentals remain supportive, citing stronger-than-expected trade data and stable inflation. Non-resident outflows were described as a portfolio adjustment after earlier ringgit gains, while investors stayed neutral ahead of state elections. The onshore FX market was described as remaining healthy, with average daily turnover at $21.3bn this year versus $19.8bn in 2025, supported by balanced two-way flows. BNM said it will continue monitoring market developments to ensure orderly conditions, while stepping up inflow support measures such as the QRI program and efforts to repatriate and convert income from GLCs, GLICs and corporates. KLCI +0.13% to 1682, USDMYR -0.14% to 4.1357, 10y MGB +0.7bp to 3.62%.

Australia’s consumer price index rose 4.0% y/y in May, easing from 4.2% in April but remaining above target. Housing was the biggest contributor, up 6.5%, reflecting higher electricity, new dwelling and rent costs, while food and non-alcoholic beverages climbed 3.3%, as did transport. Underlying inflation stayed firm, with the trimmed mean advancing to 3.6% from 3.4% in April. Electricity costs were 21.1% higher y/y as government rebates expired, while automotive fuel fell 11.9% m/m, helping to temper headline inflation. ASX +0.07% to 5603, AUDUSD -0.391% to 0.689, 10y ACGB -1bp to 4.762%.

Polish unemployment fell to 5.9% in May. Registered unemployment came in at 915.9k, with 81.6k people newly registered unemployed. In other data, wholesale sales by retail enterprises rose 11.9% y/y in May, after a 9.9% increase in April, while m/m sales fell 1.2% following a 9.6% decline. The Central Statistical Office also reported that industrial export new orders strengthened in May, increasing by 6.2% y/y after a 0.6% fall a month earlier, and by 2.1% m/m after a 12.8% drop. In addition, the general synthetic economic situation index for Poland improved to 98.8 points in June from 98.5 in May and 96.7 in June 2025. WIG -0.43% to 136879, EURPLN +0.047% to 4.2866, 10y PGB -0.4bp to 5.418%.

Mood: iFlow Mood narrowed further to -0.160. Global equities remained under selling pressure, while core government bonds shifted to net selling for the first time since late April, signaling a notable change in defensive positioning.

FX: Flows were highly volatile, with large moves in both directions. Within the G10, CAD, JPY and NOK saw significant outflows, offset by strong inflows into AUD, NZD and SEK. In EMEA, ZAR, HUF and PLN remained under heavy selling pressure, while CZK, ILS and TRY attracted strong inflows. APAC flows were relatively subdued, dominated by KRW outflows and THB inflows.

FI: Eurozone and Indian government bonds led demand, while the rest of the iFlow universe saw broad-based selling, most notably in Brazilian and Colombian government bonds.

Equities: Sizable inflows were concentrated in China, India, Malaysia and Mexico, while the Philippines, South Korea and Sweden experienced the largest equity outflows.

U.S. Q1 current account balance is forecast to widen to -$210.6bn vs. -$190.7bn.

U.S. May new home sales are forecast to rise to 638k vs. 622k.

U.S. May final building permits are forecast to rise to 1.418 million vs. 1.413 million.

Bank of Canada releases the summary of deliberations from its June meeting.

Central bank speakers: Carolyn Rogers, Senior Deputy Governor of the Bank of Canada, participates in a panel discussion on the infrastructure needed to scale tokenized assets, including the role of central bank money in on-chain settlement, cross-border regulatory frameworks and interoperable financial networks; the BoE’s Sarah Breeden speaks about “The infrastructure gap: What it actually takes to put assets on-chain at scale”; the ECB’s Cipollone Piero gives a fireside chat on the digital euro; the BoE’s Swati Dhingra speaks on a panel.

U.S. Treasury sells 17-week bills, $28bn in a 2y FRN reopening and $70bn in 5y notes.

“The market is a pendulum that forever swings between unsustainable optimism and unjustified pessimism.” – Benjamin Graham

“The time of maximum pessimism is the best time to buy.” – Sir John Templeton