Market Movers: Limits Down

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Geoffrey Yu

Time to Read: 8 minutes

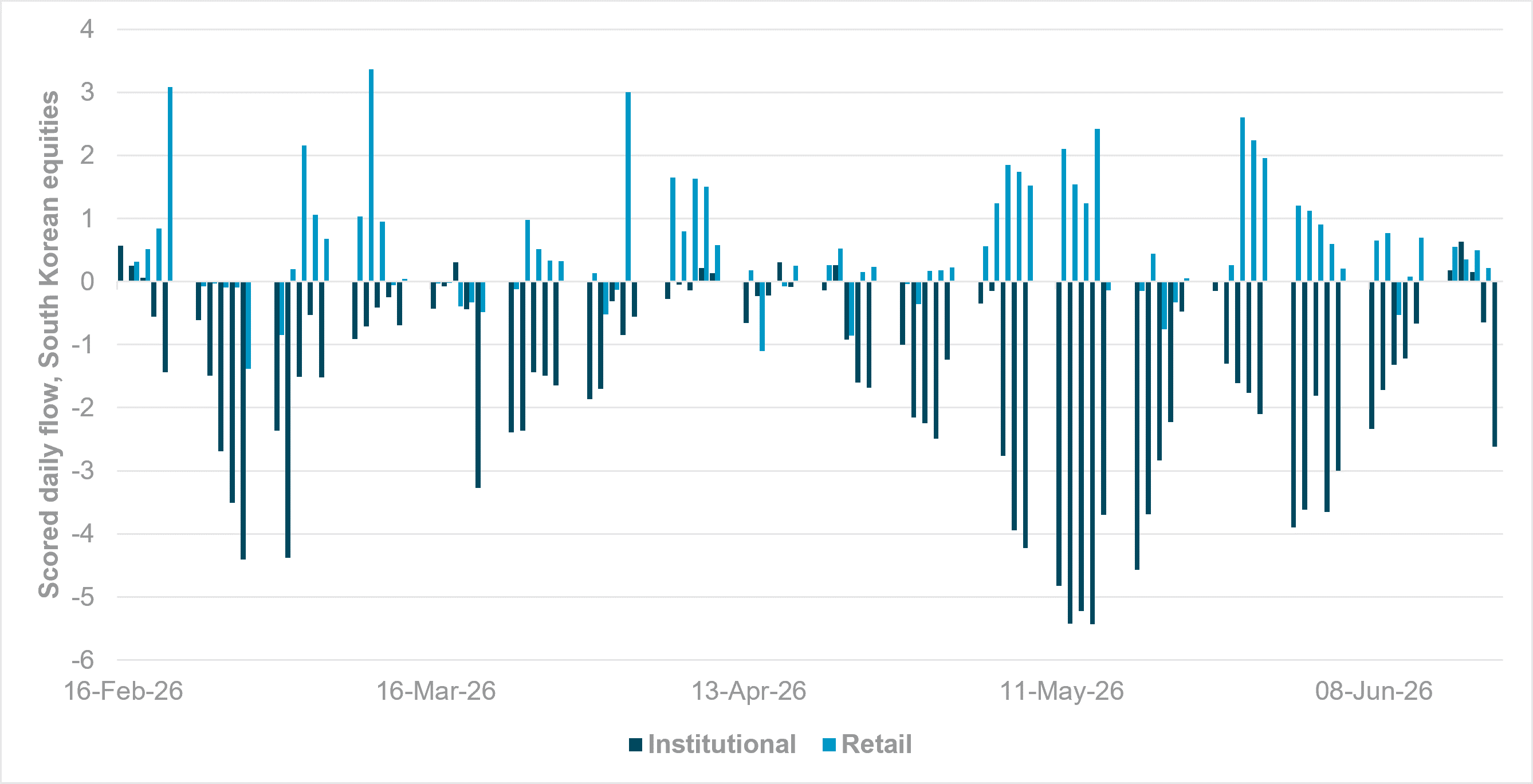

Retail flows struggling amid sustained institutional sales in South Korean equities

Source: BNY

Retail investor flow momentum into South Korea has continued to decline. Today’s sharp selloff in South Korean equities and broader weakness in global tech will add to scrutiny over retail flows into the AI/semiconductor theme. Our data indicate that these investors – who unlike institutional names are unconstrained by stock ownership cap – have been the clear drivers of flows throughout the past two months. At various points they have even forced institutional investors back into relevant indices, where capacity was available.

There are now signs, however, that retail investors, many of whom are leveraged, are struggling to maintain flow leadership. In the face of concerns over valuations and global financial conditions, retail investors in South Korean equities will need to contend with regulatory tightening ahead, as authorities act to contain financial stability risks. Regulatory tightening on leveraged products would directly compress the retail proxy demand that has been the counterweight to institutional selling.

However, holdings have contradicted the flow narrative. Before today’s sharp decline, our data indicated that all client holdings in South Korean equities remained at the 78th percentile YTD and that monthly holdings were at the 92nd percentile of six-monthly observations. These levels suggest institutional investors have not reduced their South Korean equity exposure on aggregate: the negative cumulative flow score reflects transaction-level selling pressure, not a drawdown in held positions. If holdings were declining alongside flows, the bearish read would be stronger.

Sentiment has deteriorated sharply, after a double-digit decline in the KOSPI sparked a broader global decline. Meanwhile, the dollar continues to perform strongly on a safety and yield basis, representing a new form of tightening in financial conditions and offsetting the easing arising from the declines in energy prices and improvement in global supply chains. We maintain that the setup for improved positions in risk (outside of crowded themes) remains favorable, but asset allocators will likely wait until after quarter-end rebalancing and the key earnings reports before deciding to re-engage.

Decomposing tech’s struggles: NASDAQ futures were down over 2% at the European open in response to the sharp selloff in technology stocks in Asia. Well-owned names seen as core participants in the global AI theme point to a strongly defensive posture ahead of key earnings reports from Wednesday onward. Meanwhile, the strength of issuance demand for related infrastructure is continuing to drive funding fears amid a more difficult rate environment. There is an urgency to see results from the current buildout, especially through productivity gains to help tame inflation, lest the Fed becomes the last resort to ensure price stability.

Chinese bear markets: The Hang Seng China Enterprises Index (HSCEI) has fallen 20% since October 2, taking it into bear market territory – the latest key China index to do so. The global tech rout has weighed on performance, but idiosyncratic factors remain unresolved. Beijing’s ongoing attempts to improve corporate profitability by curbing adverse competition practices have not borne fruit, while the surprising tolerance of RMB appreciation relative to peers may begin to impact export earnings as well. However, as is often the case in China, fiscal stimulus may not be far off, as symbolic financial thresholds are hit.

European PMIs: The composite Eurozone PMI was better than expected at 49.5 (consensus: 49.2), and manufacturing also showed some expansion at 51.3 (consensus: 51.6). However, the core names such as Germany and France continued to perform poorly. German manufacturing PMI was flat at 50.0, but services fell to a 43-month low of 46.8. The figures will certainly lead to questions over the ECB’s current assessment of Eurozone demand conditions to justify tightening. Reports of softer inflation pressures in the reports also lead us to question the necessity of further hikes.

Bottom line: Tech might be the trigger, but it appears that asset allocators are finding it difficult to reconcile current valuations with tightening financial conditions and global growth struggles outside of the AI ecosystem. A robust earnings outlook will help stabilize sentiment, and we also believe the market is obtaining clearer visibility over medium-term energy supplies, which is helping to contain inflation expectations and temper further central bank hawkishness. Nonetheless, if today’s price action points to AI exhaustion, fears will grow concerning the global economy’s ability to generate a clear and diversified growth narrative amid tighter funding and fiscal constraints.

South Korean stocks tumbled from Monday’s record high, as a sharp selloff in chip heavyweights shook investor confidence and exposed growing concern that the rally had become overstretched. The KOSPI closed down 10%, with losses deepening after a 20-minute trading suspension by the Korea Exchange, while SK Hynix and Samsung Electronics both fell more than 12%. Officials said they are considering stabilization measures for ETFs linked to the two chipmakers. The slide was amplified by heavy retail leverage, record margin debt and fears of forced liquidation, while attention has also turned to upcoming Micron results and signs of softer sentiment around the semiconductor trade. KOSPI -9.99% to 8204, USDKRW +0.013% to 1537.4, 10y KTB +2.2bp to 4.192%.

U.S.-Iran talks in Switzerland have produced what Vice President JD Vance called a “good foundation” for a possible deal to end the war, with a 60-day window now set for negotiations on Tehran’s nuclear program and other key issues. The interim understanding also includes measures to keep the Strait of Hormuz open and a U.S. Treasury 60-day sanctions waiver covering Iranian oil. Iranian officials said the strait will be managed by Iran in line with international law. Tanker traffic has already begun to recover. The discussions also touched on an end to fighting involving Hezbollah in southern Lebanon, where a ceasefire appears to be holding. Oil prices fell as markets reacted to the easing of immediate supply fears. Brent -0.835% to 77.25, WTI -0.623% to 73.4, Omani crude -1.486% to 70.94, Dubai crude -1.147% to 80.354.

Japan’s Finance Minister Satsuki Katayama said she held a phone call lasting nearly an hour with U.S. Treasury Secretary Scott Bessent on Monday, following last week’s G7 meeting in France. She said Japan and the U.S. still share a “solid understanding” that bold action can be taken if necessary on foreign exchange, signaling that the bilateral stance on intervention remains unchanged. Katayama said cooperation and alignment between the two sides have strengthened, but declined to comment on current FX levels. The remarks heightened market attention regarding possible Japanese intervention as the yen hovered near a 40-year low. The discussion also covered global financial markets and recent developments in Iran and the Strait of Hormuz. Nikkei -3.55% to 69788, USDJPY -0.093% to 161.42, 10y JGB -0.4bp to 2.679%.

Senior U.K. Labour Party figures are weighing whether to mount a leadership challenge to prevent Andy Burnham from becoming prime minister without a full contest, as Sir Keir Starmer prepares to step down and the party sets a rapid timetable to replace him. At least two MPs, Al Carns and Darren Jones, are being discussed as possible contenders, though neither has committed to running. Burnham, newly elected as an MP after his Makerfield by-election win, is widely seen as the frontrunner and has said he will stand. Some Labour MPs want open scrutiny of any would-be leader, while opposition parties have used the turmoil to attack Labour and call for a general election. FTSE 100 -0.88% to 10346, GBPUSD -0.197% to 1.3225, 10y gilt -2.7bp to 4.781%.

German flash PMI data for June showed the economy slipping further into contraction, with the composite output index falling to 48.0 points from 48.8 in May, an 18-month low. Services led the weakness, as the business activity index dropped to 46.8, while manufacturing output edged up to 50.8 and the headline manufacturing PMI held at 50.0. New orders declined for a fourth successive month, employment fell again and backlogs eased, pointing to limited capacity pressure. At the same time, inflationary pressures softened, with input cost and output price inflation slowing to four-month and three-month lows, respectively, suggesting some relief even as demand and confidence weakened. DAX -1.4% to 24787, EURUSD -0.175% to 1.1409, 10y Bund -2bp to 2.932%.

U.K. flash PMI data for June showed private sector activity contracting for the second month in a row, with the composite output index easing to 49.4 from 49.7 in May, the lowest in 14 months. Services remained the main drag, as the business activity index fell to 48.7, a 41-month low, while manufacturing stayed in expansion territory and output rose to 53.6, a 21-month high. Overall new business fell at the fastest pace in 14 months, backlogs declined and firms cut headcount. Input cost inflation remained elevated but has eased since April, while selling price increases also softened.

Japanese flash PMI data for June showed a stronger rise in private sector activity, with the composite output index climbing to 52.5 from 51.1 in May. Manufacturing remained the main driver, as factory output and new orders expanded at a solid pace, while services activity also returned to growth after stalling in May. Demand improved across both sectors, though export demand remained weak and foreign sales fell slightly. Employment increased further on rising backlogs. However, cost pressures intensified sharply, with input inflation hitting a near-four-year high and selling prices rising again. Business confidence remained positive but was below average amid concerns over inflation, supply chains and the Middle East conflict.

Indian flash PMI data for June showed the economy expanding at a solid but softer pace, with the HSBC Flash India Composite PMI Output Index easing to 57.4 from 59.3 in May, a three-month low. The Services PMI Business Activity Index fell to 57.3 from 59.8, while the Manufacturing PMI Output Index slipped to 57.4 from 58.0 and the headline Manufacturing PMI eased to 54.5 from 55.0. The report said demand growth slowed across goods and services, job creation weakened and inflationary pressures continued to recede. New orders still rose strongly, but export growth was mixed and business optimism softened. SENSEX -0.88% to 76417, USDINR +0.115% to 94.79, 10y INGB -0.3bp to 6.87%.

Mood: iFlow Mood narrowed further to -0.178, driven by a sharp moderation in demand for core government bonds, while equities continued to face outflow pressure.

FX: Flows were highly dispersed across the iFlow universe. AUD, NZD and SEK attracted strong inflows, offset by sizable outflows from JPY, NOK and CAD. Elsewhere, MXN, CZK, ILS and TRY saw solid demand, while HUF, PLN, ZAR and PEN were sold. Within APAC, KRW outflows dominated regional activity, contrasting with strong THB inflows.

FI: Demand was strongest for Eurozone and Indian government bonds, followed by Chinese government bonds. Flows elsewhere were mixed and generally moderate.

Equities: Moderate buying emerged across both developed and emerging markets, although selective selling persisted in Sweden, Türkiye and the Philippines.

Hungarian central bank rate decision: a 25bp cut to 6.0% vs. 6.25% is forecast.

U.S. June Philadelphia Fed Non-Manufacturing Activity is forecast at -16 vs. -23.6.

U.S. June preliminary S&P Global Manufacturing PMI is forecast to ease to 54.6 vs. 55.1. The preliminary S&P Global Services PMI is forecast to rise to 51.1 vs. 50.7, and the preliminary S&P Global Composite PMI is forecast to rise to 52.1 vs. 51.5.

U.S. June Richmond Fed Manufacturing Index is forecast to ease to 8 points vs. 13.0.

Central bank speakers: BoC Governor Tiff Macklem speaks on how shifts in the global financial system are reshaping economies and international relations, and on the importance of understanding these risks to build resilience in an increasingly uncertain world; ECB Vice President Boris Vujčić gives remarks and joins a panel discussion at the Monetary Policy Forum 2026; the BoE’s Alan Taylor speaks at the Monetary Policy Forum in London; the BoE’s Swati Dhingra speaks at a panel event titled “Brexit: Ten Years On.”

U.S. Treasury sells $65bn in 6-week bills and $69bn in 2y notes.

“The gem cannot be polished without friction.” – Confucius

“There may be hardships, but never failure.” – Chung Ju-yung, founder of Hyundai