Market Movers: Comebacks

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

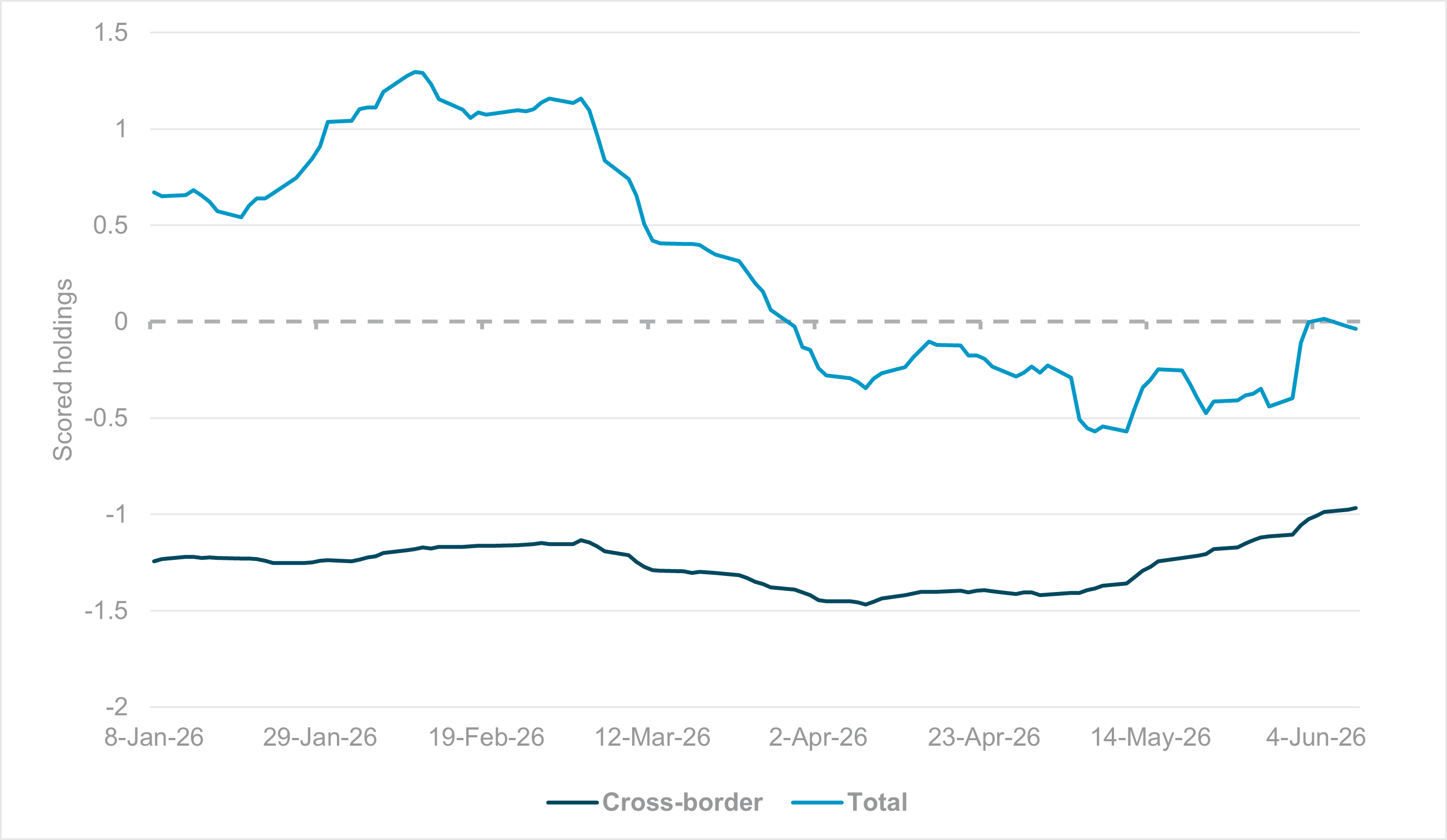

Domestic investors’ lack of hedging pressures EUR holdings

Source: BNY

Despite a late surge last week, the EUR is still heading into the ECB decision with very little momentum in yet another sign that a hawkish ECB is generating very little appetite for a pickup in exposures. Despite a widely anticipated hike and potential indication for an extended tightening cycle by the Governing Council, exogenous sources of risk aversion picking up and Fed pricing may shift more hawkish – the EUR may face significant headwinds in turning things around on policy differentials alone. In terms of flow distribution, we continue to see weakness in EURUSD and EURGBP, and both have started the week with additional hedging interest. We have highlighted the lack of interest in adding to EUR exposures against the majors. However, counting on a hawkish ECB to push for increased EUR holding on the crosses can only go so far, especially if ECB policy errs toward a preemptive, one-off move rather than a prolonged cycle, while outright cuts elsewhere may also prove elusive. The current evolution of holdings continues to underscore a major difference in behavior between local and cross-border investors. Cross-border holdings continue to improve, and hedging levels are now slightly below the rolling 12-month average. However, the aggregate figure has fallen again, indicating that onshore- or EUR-denominated accounts are continuing to take off hedges.

Risk trading overnight tracked the NBA Finals; early setbacks were overcome. Global equity markets rebounded after the U.S. ended Iran strikes, with oil lower after an initial 3% surge, leaving U.S. stock futures up 1% bouncing from five-week lows. AI and semiconductor shares led the rally. However, Hang Seng slipped 0.7% on fresh U.S. sanctions on Iran-linked companies and on an e-commerce scolding from regulators about promotions. Despite ECB rate hike expectations, bond yields were lower in the EU and the U.S. but mixed in APAC. South Korea’s 10y yields were up 2bp, contrasting with the 23rd day of foreign inflows, while Indonesia’s 10y yields jumped 12bp as IDR weakened and more BI hikes were expected. USD is bid waiting for PPI and watching JPY and EM weakness for intervention risks.

Bottom Line: The rebound in U.S. equities and focus on SpaceX pricing today won’t fully offset the U.S. PPI report and the implications of 5.4% core PPI vs. 2.9% core CPI. The rough version of margins matters to stock market outlooks and to liquidity. The 30-year bond sale will highlight the valuation problem of duration vs. growth hopes in some technology names. Cash levels and the role of safe havens will be important, as will how the ECB guides its own battle against stagflation risks. The USD-up, stocks-down dynamic is likely to be tested with EUR and MXN today. Central bankers still matter in the rebound equation for trading.

The U.S. and Iran exchanged strikes across the Middle East for a second straight day, deepening tensions and putting pressure on a fragile ceasefire agreed to in April. U.S. Central Command said it carried out self-defense strikes on military, surveillance and radar sites in southern Iran after Trump warned Washington would hit Iran hard. Iran retaliated with attacks on U.S. military assets in the region, including bases in Bahrain and Kuwait, while state media said the IRGC fired ballistic missiles at a U.S. command center in Jordan. Nonetheless, risk sentiment looks manageable for now as futures point to better opening for the U.S. session after yesterday’s selloff, while Brent crude prices are largely unchanged. Brent -0.742% to 92.41, WTI -0.556% to 89.53, Omani Crude +3.404% to 88.41, Dubai Crude +0.549% to 89.877.

Trump urged Republicans on Wednesday to quickly pass a third $350bn reconciliation bill and attach the Save America Act, framing the package as essential to national defense and the broader military budget. In a Truth Social post, he pressed Congress to act immediately, saying the bill would help fund priorities such as the Golden Dome, F-47 and B-21 production, and larger ammunition stockpiles. The comments followed skepticism from Senate appropriators Susan Collins and Mitch McConnell, who warned that a third bill could create funding instability. Trump also backed the controversial voting measure, despite Senate resistance and concerns over its citizenship, ID, and mail ballot provisions. S&P Mini +0.73% to 7,332, DXY +0.095% to 100.041, 10y UST -1.8bp to 4.534%.

France and Germany are discussing a major overhaul of the EU’s diplomatic machinery amid concerns that the European External Action Service is not equipped to respond effectively to growing geopolitical challenges. Proposals under consideration include reducing the autonomy of EU foreign policy chief Kaja Kallas, shifting some powers back to member states, the European Commission and the European Council, and restructuring the EU’s network of diplomatic delegations. The review reflects dissatisfaction with coordination during crises, including the wars in Ukraine and Iran, and broader concerns about overlapping responsibilities between EU institutions and national foreign ministries. Discussions are also linked to efforts to improve efficiency and reduce costs ahead of negotiations on the EU’s next budget. Any reform would require unanimous support from all 27 member states and is expected to influence the bloc’s upcoming security strategy. Euro Stoxx 50 +0.66% to 6050, EURUSD +0.035% to 1.1539, BBG AGG Euro Government High Grade EUR -1.6bp to 3.325%.

The Bank of Thailand said no special Monetary Policy Committee meeting is needed as the baht has moved steadily despite pressure from the U.S.–Iran conflict. BOT spokesperson Chayawadee Chai-anant said the currency has weakened only slightly, while Thailand’s external position remains strong enough to absorb global market volatility. The baht has fallen about 5.4% since the conflict began, less than many regional currencies, and foreign investors have sold only around USD 1.3bn of Thai assets, with signs of inflows returning to long term bonds and equities. The BOT stressed that international reserves, financial stability, and the current account continue to support the economy. Indonesia’s central bank hiked rates by 25bp in an emergency meeting and is expected to hike again in their scheduled meeting next week. SET +0.9% to 1,578, USDTHB +0.116% to 32.92, 10y TGN -2.1bp to 2.273%.

The European Central Bank is expected to raise rates to 2.25% from 2.00%.

The Turkish Central Bank is expected to keep rates on hold at 37%.

U.S. Initial Jobless Claims are forecast to ease to 220k vs. 225k.

U.S. May PPI Final Demand is forecast at 0.7% m/m, 6.4% y/y vs. 1.4% m/m, 6.0% y/y in April. PPI ex Food and Energy is expected at 0.5% m/m, 5.4% y/y vs. 1.0% m/m, 5.2% y/y in April. PPI ex Food, Energy and Trade is expected at 0.5% m/m, 4.9% y/y vs. 0.6% m/m, 4.4% y/y in April.

Canada April Building Permits are forecast to fall to -3.9% m/m vs. 10.3% m/m.

U.S. Treasury sells $70bn 4-week bills, $75bn 8-week bills and $22bn of 30y bonds reopening.

Mood: iFlow Mood improved slightly to -0.310, driven by reduced demand for core government bonds, although equity selling pressure remained persistent.

FX: Flows were mixed and moderate across the iFlow universe, with BRL standing out as the primary outflow. Within G10, USD, GBP, CAD and AUD were sold, while the remaining major currencies attracted modest inflows.

FI: Demand was concentrated in G10 and LatAm government bonds, led by the Eurozone and Colombia. In contrast, EMEA and APAC sovereign bonds faced selling pressure, particularly in South Africa, Hungary, China and Indonesia.

Equities: Selling was broad across LatAm, EMEA and APAC, led by South Korea, Indonesia, Chile and Mexico, while China and Thailand continued to attract inflows. Within G10, selling was concentrated in the U.K., whereas Australia saw continued buying interest. At the sector level, materials and information technology were sold, while communication services and utilities attracted strong inflows, particularly within developed market Americas.

“I am not discouraged, because every wrong attempt discarded is another step forward.” – Thomas Edison

“It does not matter how slowly you go as long as you do not stop.” – Confucius

The U.K. May 2026 RICS Residential Market Survey shows housing demand and sales remain subdued, but the pace of deterioration appears to be stabilizing. New buyer enquiries were unchanged at -34% m/m from the previous survey, and agreed sales held at -37% m/m, while the average time to complete a sale lengthened to 21.5 weeks, the longest since the series began. House prices were flat at a net balance of -35% m/m, suggesting declines are still modest. Near-term expectations remain cautious, with sales at -25% and prices at -45%, though the 12-month outlook improved slightly: sales rose to +2% and prices to +6%. On the supply side, new instructions weakened to -8%, and landlord instructions stayed negative at -28%, while tenant demand remained positive at +14%. FTSE 100 +0.47% to 10,303, GBPUSD +0.03% to 1.3372, 10y gilt +0.1bp to 4.932%.

Sweden CPI for May 2026 came in at 0.8% y/y, rebounding from -0.1% in April, while the monthly CPI rise was 1.0%. Statistics Sweden said the pickup was mainly driven by higher energy prices, especially fuel and electricity, alongside higher package holiday, accommodation, restaurant, and interest cost components. Food prices fell and continued to offset some of the upward pressure. The CPIF, the Riksbank target measure, rose to 1.5% from 0.8%, while CPIF excluding energy edged up to 0.5% from 0.0%. Overall, the release suggests firmer inflation pressures in May, but with underlying inflation still relatively contained. OMX +0.64% to 3,074, EURSEK +0.192% to 10.9979, 10y Swedish GB -0.3bp to 2.875%.

Sweden registered unemployed in May came in at 339,280 people, or 6.4% of the labor force, the lowest level since end-2023. The number of jobless people was down by almost 20,000 from a year earlier, while the unemployment rate fell from 6.8% in May 2025. Youth unemployment also improved, with 34,291 people aged 18 to 24 registered as unemployed, equal to 6.4%. Long term unemployment remained elevated at 150,431 people, and the seasonally adjusted series still suggested only a weak labor market recovery, with monthly changes remaining small through 2026.

Norges Bank’s Regional Network reported that recruitment difficulties have eased somewhat, with slightly fewer contacts facing capacity constraints and a smaller share now struggling to hire than in the previous survey. Contacts cut their growth expectations for Q2 2026 but still expect activity to improve again in Q3. They plan to raise employment slightly in both Q2 and Q3 2025. Most sectors, except oil services, see higher activity ahead, supported by data center construction, energy supply development and stronger defense investment, even as customers remain more cautious because of higher interest rates and rising costs. Contacts now estimate annual wage growth at 4.5% in 2026 and 4.1% in 2027, while profitability is broadly unchanged. OSE +0.42% to 1,990, EURNOK +0.552% to 10.9842, 10y NGB -1bp to 4.384%.

South Africa’s exports and imports for April 2026 showed diverging price trends in commodity unit values. Exported commodities recorded an annual increase of 8.5% and rose 0.6% from March to April, supported mainly by metal products, machinery and equipment, which was the largest contributor to the yearly gain, while other transportable goods and ores and minerals lifted the monthly rise. Imported commodities showed an annual decline of 3.3%, even though they increased 5.2% m/m. The annual fall was driven by lower unit values for metal products, machinery and equipment, food products, and crude petroleum, while the monthly rebound was led by other transportable goods, crude petroleum, and metal products, machinery and equipment. JSE TOP 40 -0.17% to 101,479, USDZAR -0.229% to 16.5415, 10y SAGB -0.5bp to 8.794%.

South Africa’s current account balance for Q1 2026 posted a much larger surplus of R190.7bn, up from R50.2bn in Q4 2025 and the biggest surplus since Q3 2021. As a share of GDP, the surplus widened to 2.4% from 0.6%. The improvement was driven by a stronger trade surplus, which increased to R437.9bn as merchandise and net gold exports rose and imports fell. Export values increased on higher prices and volumes, while import values declined on weaker prices and volumes. The services, income and current transfer deficit widened slightly to R247.2bn, though the services gap narrowed. Terms of trade improved further as export prices rose and import prices fell.

South Africa’s SACCI Business Confidence Index for May 2026 rose 0.5 index points m/m to 124.1 after a sharper 7.7-point drop in April, but it remained 8.3 points above May 2025 and averaged 129.0 in the first five months of 2026 vs. 120.0 a year earlier. The recovery reflected improved new vehicle sales, stronger merchandise export volumes and, to a lesser extent, imports, while lower overseas tourist arrivals and higher inflation weighed on sentiment. SACCI said the earlier drag from surging crude oil prices eased in May, helped by a steadier rand and lower fuel levy, although energy costs, inflation and broader external uncertainty continued to pressure business confidence.

South Africa mining production for April 2026 rose 8.2% y/y, led by strong gains in PGMs, manganese ore, and chromium ore, while coal was the main drag. On a seasonally adjusted basis, output increased 3.3% from March and 2.4% in the three months to April vs. the prior three months, with PGMs and gold the main contributors and coal and other metallic minerals weighing on growth. Mineral sales at current prices surged 30.3% year on year in April, boosted especially by PGMs, gold, chromium ore, and coal. Seasonally adjusted mineral sales also rose 3.1% m/m and 4.9% over the three-month comparison period.

Japan’s Business Outlook Survey for April–June 2026 showed a softer assessment of business conditions among large firms, with the all-industries index falling to -0.5 from 4.4 in January–March 2026. The dip in Q2 2026 seems to be temporary, as the Q3 outlook to 4.3 and further improve 4.5 in Q4 2026. Manufacturing turned negative at -1.8 from 3.8, with outlook at 4.4 and 5.8 in Q3 and Q4 2026, while non-manufacturing was unchanged at 0.0 from 4.6, with an outlook of 4.2 and 4.0 in the coming two quarters. Domestic economic conditions also weakened, with the large-firm all-industries index at -4.5 from 8.0, led by manufacturing at -6.4 from 6.1 and non-manufacturing at -3.6 from 8.8. Employment shortages eased but remained elevated, while firms still plan steady FY2026 sales growth of 3.3% and capital spending growth of 8.2%. Ordinary profits are projected to fall 2.4% y/y, suggesting profitability pressures despite continued investment plans. Nikkei +0.06% to 64,217, USDJPY -0.019% to 160.52, 10y JGB 0bp to 2.69%.

Tokyo business district office vacancy rates fell for a second consecutive month in May. The average vacancy rate in the five central wards of Tokyo (Chiyoda, Chuo, Minato, Shinjuku and Shibuya) declined to 2.07% in May, down 0.13 percentage points m/m, as lease cancellations tied to consolidation and downsizing were offset by additional floor space leases and new subdivisions. Vacancy in new buildings fell to 11.78% (-0.33 pp m/m), while existing building vacancy eased to 1.89% (-0.13 pp m/m). The total vacant area in the district decreased by about 10.8k tsubo over the month. Average asking rent rose to ¥22,845 in May, up 1.74% m/m and 9.96% y/y (up ¥391 m/m, ¥2,069 y/y).

Australia’s June Melbourne Institute Consumer Inflation Expectations eased for the second straight month to 5.5% from 5.9% highs in April 2026, suggesting households are becoming slightly less concerned about near-term inflation. Wage expectations were unchanged for a seventh consecutive month, indicating stable pay growth expectations despite the softer inflation outlook. The figures will come as a relief to the Reserve Bank of Australia, which is expected to keep rates on hold at 4.35% at next week’s policy decision. Markets are struggling to price in significant easing ahead, with only 60% of another 25bp in the current cash rate futures curve by the end of the year. ASX +0.41% to 5,540, AUDUSD -0.043% to 0.6996, 10y ACGB +0.5bp to 4.895%.

South Korea’s exports rose 86% y/y in the first 10 days of June 2026, reaching a record high as semiconductor shipments surged. Outbound shipments totaled $28.6bn, far above $15.4bn a year earlier. The daily average export volume increased 46.1% after adjusting for working days. Imports also climbed 35.6% y/y to $23.4bn, leaving a trade surplus of $5.28bn. By sector, chip exports more than tripled to $11bn on strong AI-related demand, while petroleum products and automobiles also posted solid gains. By destination, exports to China doubled to $6.18bn, shipments to the U.S. rose 54.4% to $4.53bn, and sales to Vietnam and the EU surged 102% and 46%. The data pointed to strong external momentum in early June, led by semiconductors and supported by broader export categories. KOSPI +0.43% to 7,764, USDKRW +0.556% to 1530.15, 10y KTB -0.7bp to 4.265%.

This Bank of Korea research paper examines whether AI adoption improves productivity over the first three years. Using household survey data, it finds that AI adoption reduces average work time by 3.8%, or about 1.5 hours per week, with larger effects for lower-skilled workers and heavy AI users. If all time savings were converted into output, the implied productivity gain would be around 1.0%. However, the study finds essentially no correlation between time savings and actual output growth, pointing to a “productivity disconnect.” Productivity gains are observed mainly among the self-employed, professionals, and intensive AI users, where incentives and job autonomy are stronger. The paper concludes AI is still in the “efficiency” stage and has not yet fully reached the “productivity” stage.

Thailand’s consumer confidence index fell to 49.5 in May 2026 from 50.6 in April, according to the University of the Thai Chamber of Commerce. The decline suggests weaker sentiment across both present and future conditions, with the present index easing to 33.6 from 34.7 and the future index slipping to 57.3 from 58.3. Views on economic conditions weakened to 43.1 from 44.1, employment to 47.5 from 48.6, and future income to 57.9 from 59.0. The report indicates continued caution among households, though confidence remains close to its six-month average of 51.7. SET +0.9% to 1,578, USDTHB +0.116% to 32.92, 10y TGN -2.1bp to 2.273%.

S&P Global Ratings upgraded Argentina’s long- and short-term sovereign credit ratings to B-/B from CCC+/C, with the long-term outlook stable. The agency said the move reflects easing economic vulnerabilities, improving external liquidity, and stronger access to financing, supported by continued fiscal surpluses, tighter monetary policy, and lower inflation. It noted that the government has been better able to service debt through broader market access, official lending support, and reserve accumulation by the central bank. S&P expects the fiscal austerity program to continue and foreign exchange reserves to rise, helping sustain growth and reduce inflation. Risks remain from Argentina’s fragile macroeconomic history, limited monetary flexibility, and vulnerability to shocks, but the rating agency sees the current policy mix as sufficient to avoid default or a distressed exchange over the next 12 to 18 months. IBG +0.13% to 134,432,400, USDARS -0.603% to 1433.245, 10y AGB +4.3bp to 8.589%.