The growth toll of an ECB hike

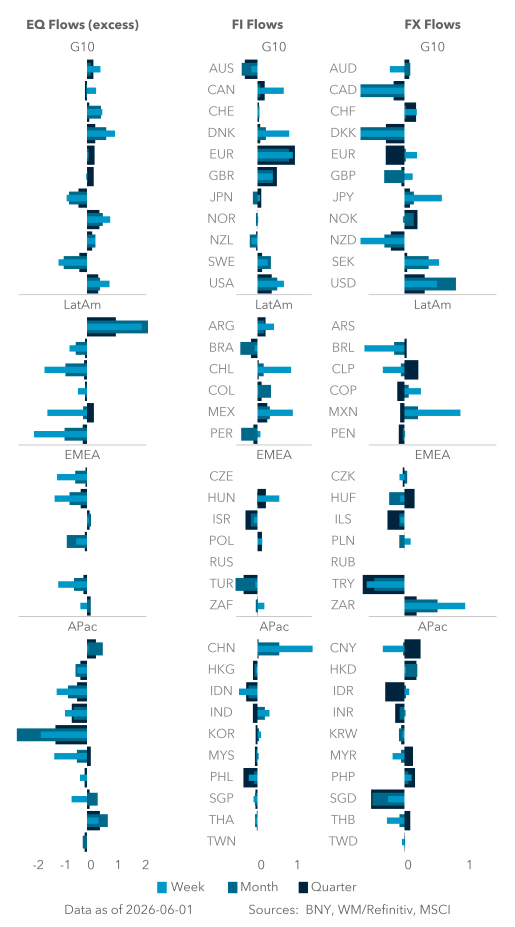

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 4 minutes

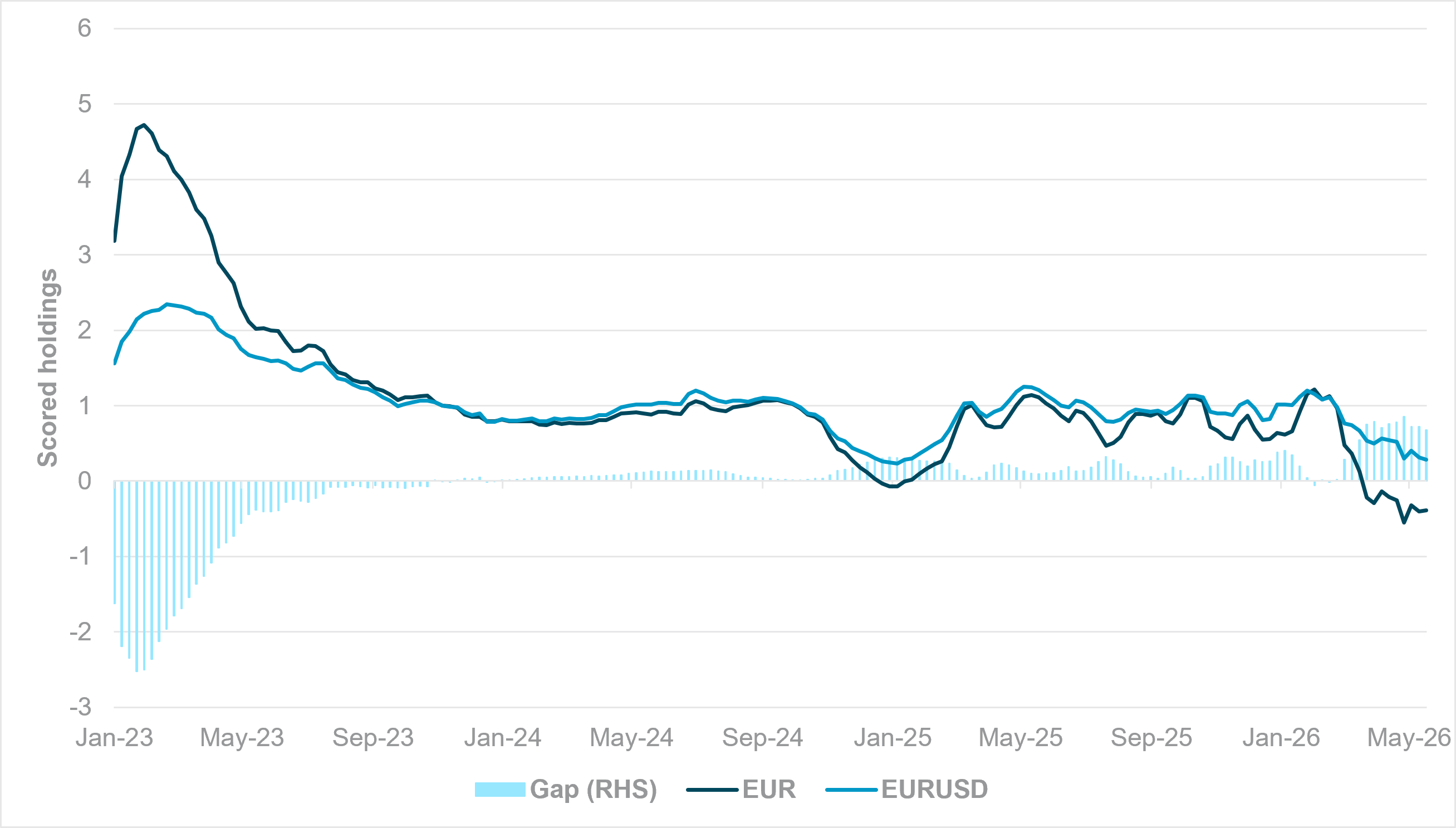

EXHIBIT #1: SCORED HOLDINGS IN EUR VS. EURUSD SINCE JANUARY 2023

Source: BNY

Our take

The ECB is fully expected to hike rates next week, but this is not generating any support whatsoever for the EUR. The currency’s current holdings position is net negative on an aggregate basis. Even during the last round of material weakness in sentiment – in Q4 2024 – the EUR only briefly dipped into this position, largely driven by extreme hedging interest by non-EUR (mainly cross-border) accounts. Surprisingly, cross-border behavior is more subdued at present, meaning onshore investors have actively reduced their exposures, limiting their hedges (forward EUR purchases) on overseas investments. Furthermore, we can see that EURUSD is currently moderately overheld, suggesting that there is still sufficient hedging in place on USD-denominated assets despite the dollar’s recent recovery. It is on the crosses where the EUR has significantly underperformed (Exhibit 1), and where a hawkish ECB has been of very little help.

Forward look

Outside of EURUSD, it is not difficult to see that the EUR doesn’t have strong advantages. For example, currencies such as AUD and NZD are also seen as hawkish, so the ECB’s stance is of little help. Against key APAC currencies, JPY, TWD, CNY and KRW all look materially undervalued. A reversal could come even before the energy shock subsides, given the currency preferences of the PBoC, BOJ, and more recently, the hawkish turn in the BOK. Crucially, in Europe, the EUR is largely underperforming. We maintain that the ECB hike risks adverse growth effects, and the BOE’s relative restraint is hurting EURGBP even as rate differentials continue to move in the EUR’s favor.

Meanwhile, the Scandis have stronger fiscal and growth buffers; even the CHF has now recovered to an overheld position for the first time since Q2 2022, when the SNB was more advanced than the ECB in tightening. The shift is being driven by CHF-denominated accounts, and as EURCHF is the dominant pair for such investors, it implies that Swiss asset pools are now forward hedging their overseas exposures, even with significant carry costs in play.

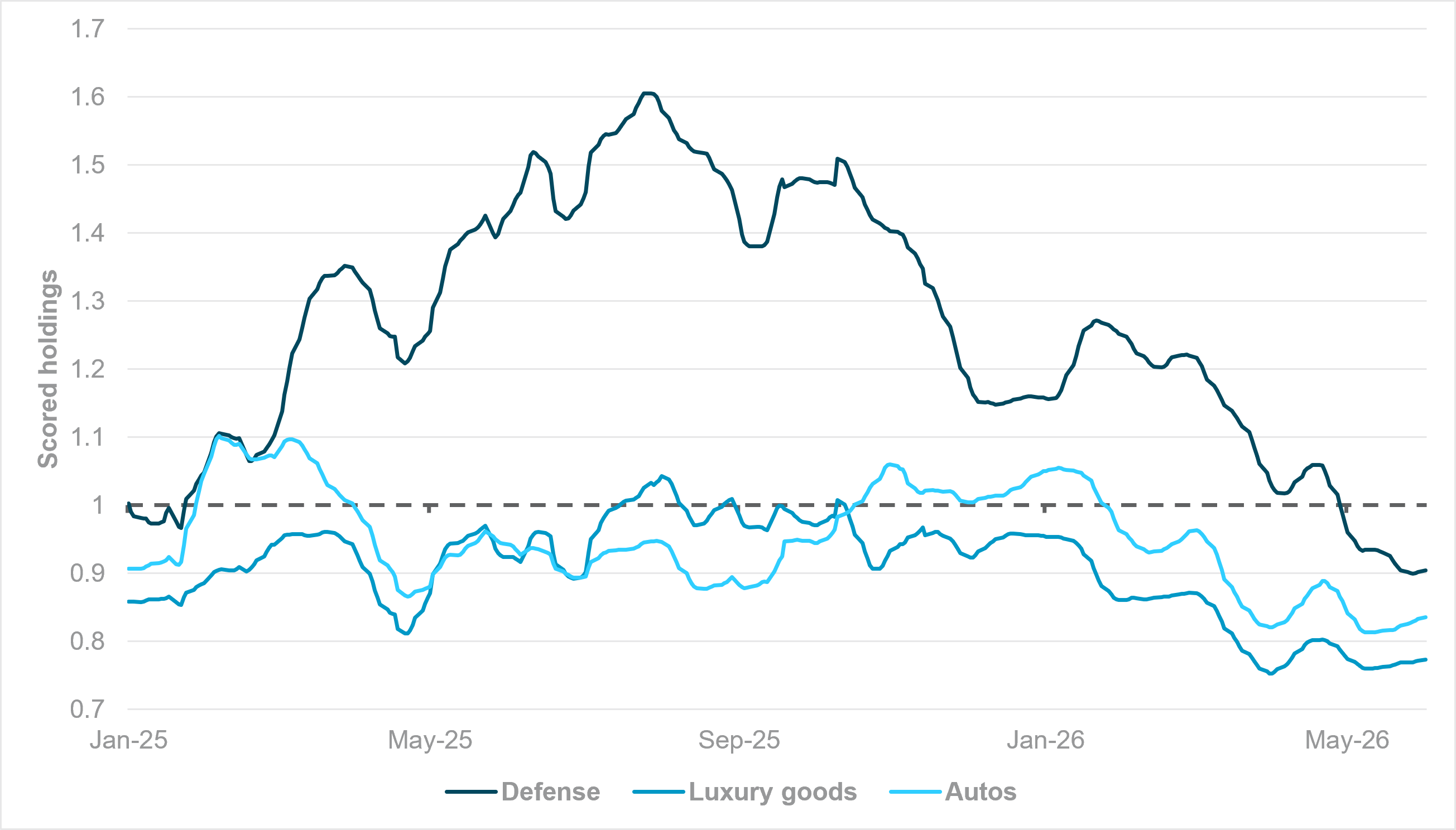

EXHIBIT #2: WEEKLY SMOOTHED HOLDINGS IN DEVELOPED EUROPEAN EQUITIES, GICS LEVEL 3

Source: BNY

Our take

From an equity perspective, Europe’s difficulties in generating growth look increasingly structural rather than cyclical. French President Emmanuel Macron has just touted close to €100bn in pledged investments at this week’s Choose France summit, but the funds will likely shy away from the Eurozone’s traditional industrial sectors. Our clients’ holdings in defense, luxury goods and autos have fallen below the rolling 12-month average for the first time since January 2025. At that point, Eurozone growth sentiment was at its weakest, pressured by political instability and trade tensions with the U.S. Luxury goods and autos were already facing structural headwinds, largely attributed to changes in China’s demand composition and industrial strategy. On defense: last year’s “strategic autonomy” push set a high base. The drop-off suggests much of the planned investment will be difficult to realize, particularly as fiscal resources are increasingly directed toward energy resilience.

Forward look

Poor equity performance already represents a tightening in financial conditions and will draw unfavorable comparisons with the U.S. and some industrialized economies in Asia. While there are some critical infrastructure companies related to AI and semiconductor production in Europe, the continent continues to struggle to be a part of the conversation in generating growth from new industries. The ECB will protest that its mandate requires an immediate response, but compounding the tightening in financial conditions will not help equity positioning recovery. Either way, even if the AI theme unwinds, it is hard to see Europe benefiting, as a capital expenditure slowdown will likely depress valuations globally.

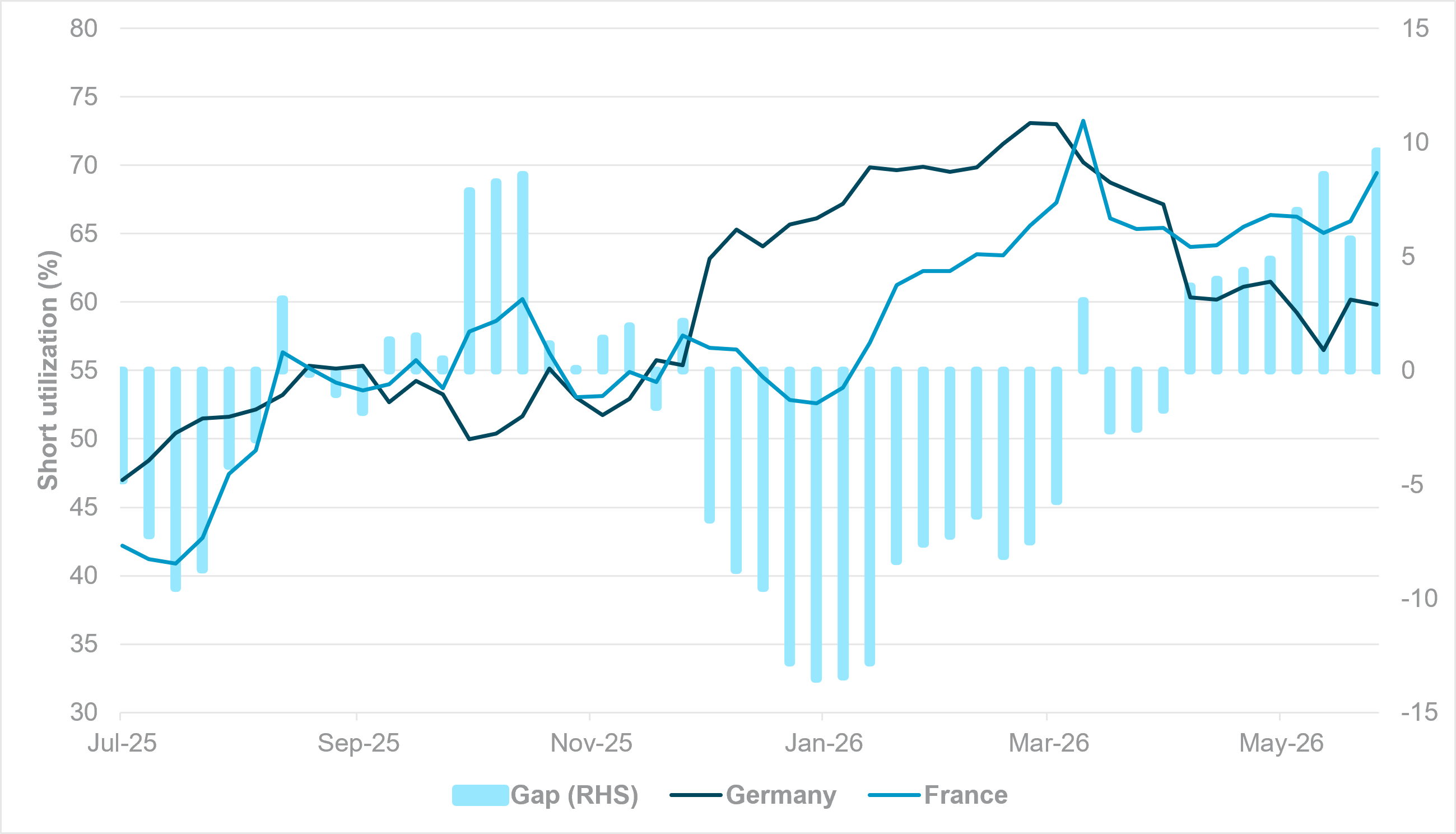

EXHIBIT #3: SHORT UTILIZATION AND GAP, FRENCH AND GERMAN GOVERNMENT DEBT

Source: BNY

Our take

With market scrutiny of central bank independence running high, Eurozone governments have largely kept their counsel on ECB hikes. However, a prolonged cycle would have material consequences for government bond curves. Eurozone governments are fully aware that a fiscal response on the scale of 2022 is difficult to execute – defense and competitiveness investment compete for the same resources – but the political cost of doing nothing in a cost-of-living crisis is high. Adding to borrowing costs in a stagflation-driven environment will likely prove contentious, especially if peers hold back because of concerns over domestic demand. We would not be surprised if President Macron reiterates his 2024 calls for the ECB to drop “a monetary policy whose sole objective is inflation.” Emmanuel Moulin, the new Banque de France Governor, has already indicated that he will bring the growth discussion to the Governing Council, noting before he took office that it was “essential … the ECB be able to take into account the impact of its decisions on growth.”

Forward look

We can see why Paris is more alarmed by the prospect of the ECB engaging in a prolonged cycle along the lines of what Governing Council member Gediminas Šimkus has suggested. Compared to Germany – even with industrial challenges currently in place – the market does not see France being able to “grow” its way toward debt sustainability. Short utilization data in iFlow indicate that between end-Q4 and early this year, improving growth signals and the ECB’s pivot toward ending its easing cycle pushed up short utilization in both German and French government debt, moving in tandem. The conflict did not materially drive such steepening risks higher, mostly due to the growth impact. However, over the past few weeks, as the ECB has become more hawkish, the market has concentrated its bearish view on French government debt (Exhibit 3). All else being equal, we believe this is fiscal premia in play as stagflation challenges one of the worst fiscal profiles in the G7. Given French officials’ prior and current warnings, we expect many on the Governing Council to push back against Šimkus’ recent calls to “not overemphasize” the effect of the hike on the Eurozone economy.