Diverging Flows, Common Pressures

iFlow > Investor Trends

Appearing every Wednesday, Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

iFlow > Investor Trends

Appearing every Wednesday, Investor Trends provides a deep dive into patterns and behaviors in equity, bond and currency markets around the globe, underpinned with deeper macro insights.

Geoff Yu

Time to Read: 5 minutes

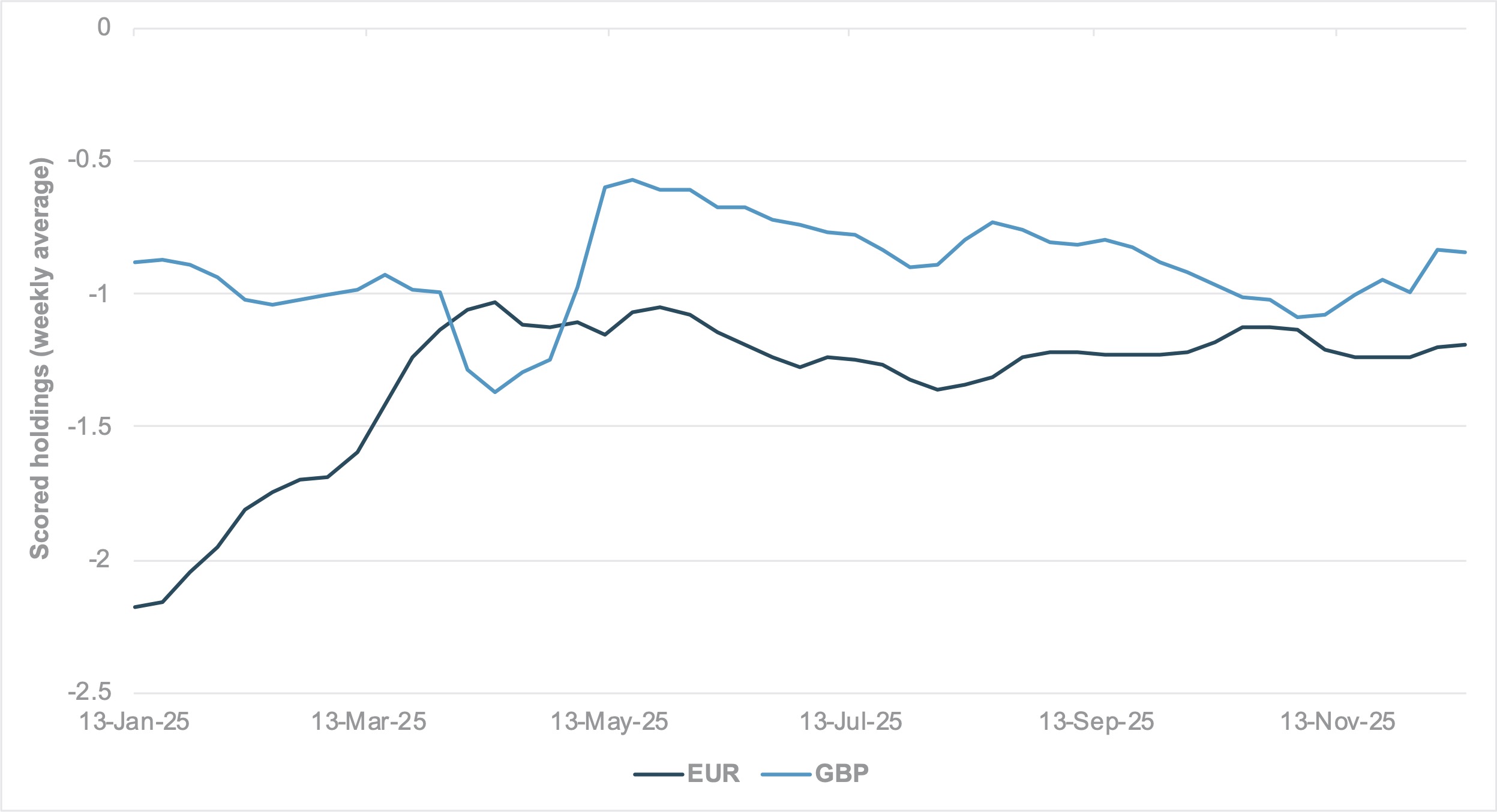

EXHIBIT #1: SCORED HOLDINGS, CROSS-BORDER BASIS, GBP AND EUR

Source: BNY iFlow

Our take

Expectations remain for the Bank of England (BoE) to cut rates on Thursday, while the European Central Bank (ECB) looks set to release a fresh set of forecast upgrades that will begin to nudge policy expectations in the opposite direction. For now, the main question is to what extent U.K. rates can decline, as every single monetary policy committee vote over the next six months is expected to remain very close.

The latest U.K. labor market data indicate that the slowdown in wage growth sought by the less dovish members remains elusive. Until that changes, markets will likely take a cautious tone on BoE easing. This is well reflected in iFlow, as on an outright basis, hedging against the pound (GBP) remains relatively expensive, especially now that the Fed’s rate advantage over GBP is minimal.

Our data show that for all the improvement in euro (EUR) holdings this year, the currency only briefly managed to surpass GBP in cross-border holdings – during the extreme period of stress around “Liberation Day.” Uncertainty surrounding the U.K. budget in November added pressure to GBP, but divergence is picking up again. The ECB’s pivot has not generated much change in EUR hedging interest, but based on current trends, cross-border GBP hedges look set to end the year in a better position compared to the rolling 12-month average, even after the currency’s recent recovery.

Forward look

The other G10 currencies priced with a hawkish “tilt” this month have struggled recently, suggesting that market expectations for shorter policy cycles may be premature. Even the more hawkish ECB members have warned that any moves remain some time away.

The euro’s strength toward year end has already generated some tightening, though the exchange rate channel has very little bearing on supply-based inflation pressures, which are driving the ECB’s thinking. Overall, we believe the improvement in EUR holdings through Q1 – from an extremely low base at the beginning of the year – has already set too high a bar for further improvement in EUR holdings or valuations. Even with upward revisions, it will take time before Eurozone growth is sufficiently strong to justify higher levels of net asset exposure.

EXHIBIT #2: SEMICONDUCTOR INDUSTRY GROUP FLOWS (GICS LEVEL 2), DM VS. EM

Source: BNY iFlow

Our take

The AI and semiconductor trade looks set to end the year on a softer note globally. APAC-listed companies that are part of the U.S. technology capital expenditure ecosystem have suffered notable declines through the month, and currencies such as the Taiwan dollar (TWD) and South Korean won (KRW) are also struggling.

Amid ongoing concerns over valuations and seasonal de-risking, last week’s FOMC decision also failed to ease global financial conditions beyond what was priced. Although the currency transmission is apparent, our equity flow figures do not point to emerging market (EM)-linked semiconductor names as a simple “high-beta” proxy for developed market (DM) performance.

For example, through much of the October tech selloff, DM semiconductor makers clearly struggled, while EM counterparts performed strongly. At present, roles have reversed, and DM names are finding some support after the adjustment in valuations (Exhibit #2).

Forward look

The dominant economies in EM’s semiconductor industry are in APAC, but the roles of Chinese, South Korean and Taiwanese companies in the global supply chain are complex and increasingly subject to different investment cycles.

The Sino–U.S. trade detente and China’s prospect of better access to advanced chips should encourage some degree of convergence, but given China’s strategic needs, there is a strong chance that flows may stay domestic, even if DM counterparts begin to struggle with valuations.

The biggest question is how much investment and access cross-border investors will have to this industry group. We have long seen China (and EM APAC in general) as having a disproportionately low level of equity positioning relative to the U.S. and developed markets. Improvements in semiconductor and tech sector holdings are needed to close the gap. In this context, the lack of alignment between EM and DM sectoral flows is probably a positive driver for allocations.

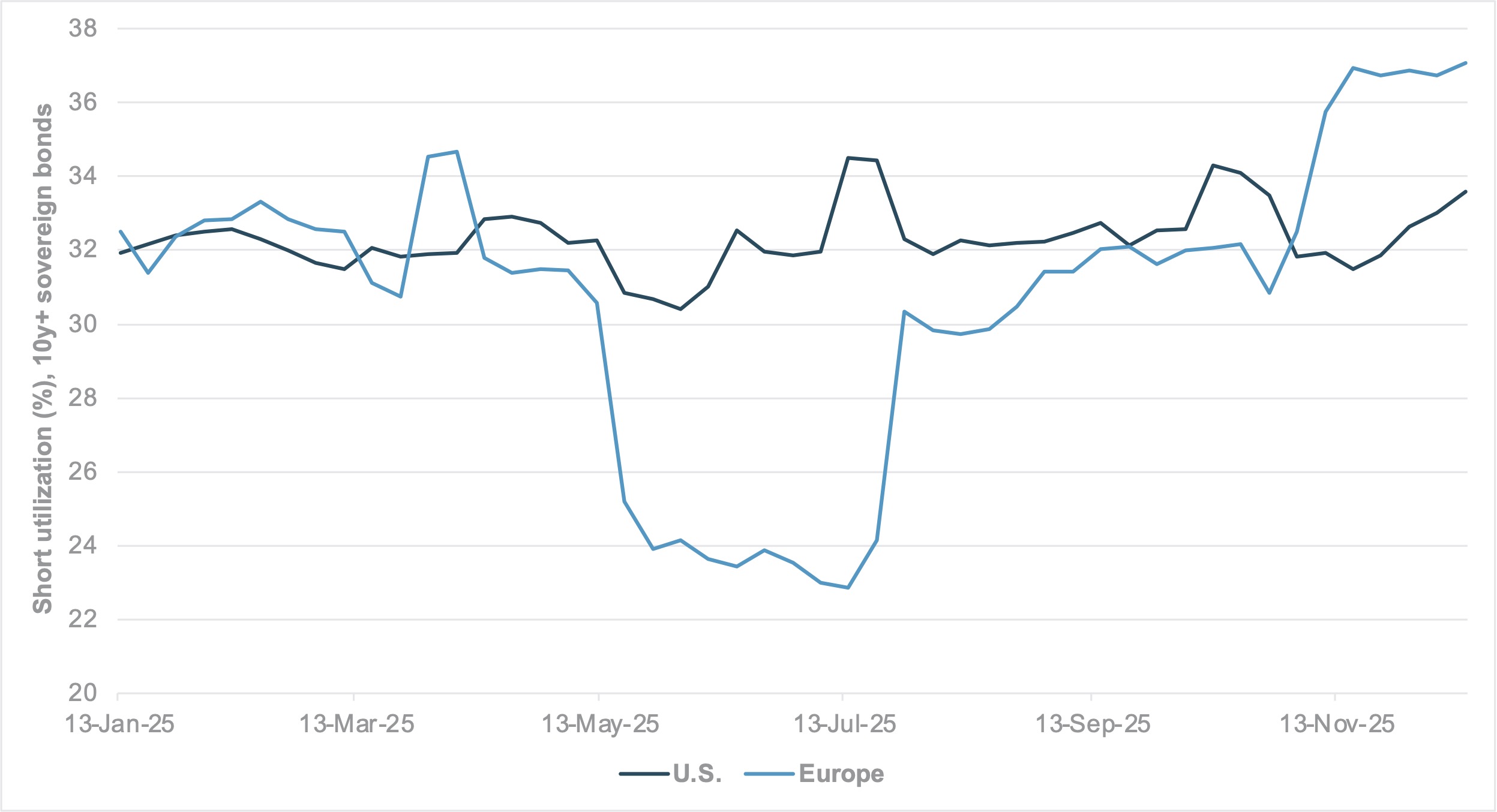

EXHIBIT #3: SHORT UTILIZATION, U.S. VS. EUROPEAN BONDS

Source: BNY iFlow

Our take

One of the key things to watch for the December round of ECB staff projections is the decomposition of “upward revisions” that led to the market pricing in tightening over the medium term. For now, inflation is not expected to move materially above the 2.0% target, which means that upon decomposition, growth will be driven by non-inflationary elements such as productivity – the very gains that stronger domestic fiscal impulse is designed to drive.

Without taking a view on the outcome of Ukraine peace talks, we assume that public sector investment to further boost competitiveness and counter industry challenges stemming from U.S. tariffs and Chinese competition will continue. Yet, it seems the market cannot shake off the risk that Eurozone growth could prove far more stagflation-based, which would align that economy more with Anglosphere peers. After all, it is in services where labor supply continues to face struggles, and fiscal expansion will continue to challenge public sector productivity.

The recent shift in growth and inflation expectations in broader developed Europe has driven short utilization in sovereign bonds at the long end of the curve to the highest levels this year. These levels are well above those for the same segment of the curve in the U.S. Treasury market (Exhibit #3). This is the clearest sign yet that the market continues to take a skeptical view on real rates in Europe, except that low nominal levels have been supplanted by higher inflation.

Forward look

We believe the Eurozone will face a litany of supply pressures next year. Escalation in EU–China trade tensions will compound existing pressures from uncertain U.S.–EU trade relations, while there are no clear signs that domestic supply challenges will improve soon.

In contrast, despite concerns over fiscal dominance, the U.S. curve is much better behaved for now. A softer labor market will help limit earnings growth, and for now the market is not pricing in excessive Fed easing that would undermine U.S. real rates. Upon factoring in structural strength in U.S. productivity growth, there is a stronger case for higher real rates in the U.S.

However, this will not help the dollar, as the exchange rate is now seen as compensating for other factors that affect cross-border interest. The bottom line is that European assets are pricing in reflation, but asset allocators are adding to protection against stagflation in the process.