Bitcoin Breaks the Mood

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

Last week left investors nauseous after roller-coaster price moves in technology shares and a Federal Reserve rate repricing for December. Federal Market Open Committee (FOMC) minutes showed the debate over easing remains too close to call, while the September jobs data didn’t provide much clarity.

Nvidia’s earnings beat expectations but concerns over supply–demand balance kept bubble fears alive. At the same time, cash holdings drew attention, as investors began deleveraging speculative positions, most notably in crypto. Bitcoin plunged more than 30% in just 45 days.

The pace of the crypto bear market has become a red flag for other risks. Oil, tech shares, and Emerging Market (EM) positions all appear interconnected through “bubble popping” fears. Debt markets also matter, with credit discussions reflecting late-cycle economics as the global easing cycle winds down.

This week and beyond, the mood hinges on whether the Fed and new data can restore confidence.

Will markets trade on liquidity into Thanksgiving?

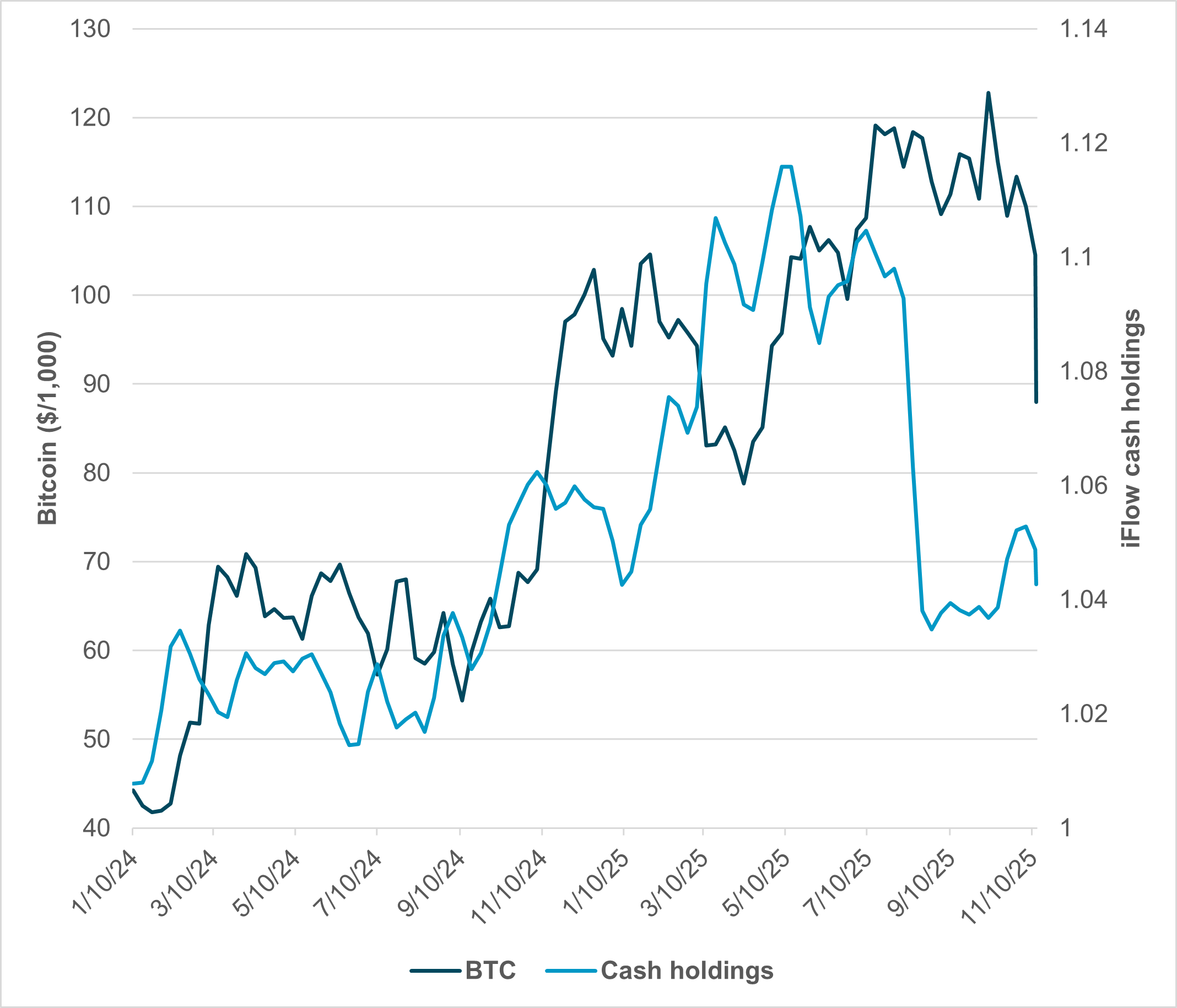

EXHIBIT #1: BITCOIN (BTC) AND IFLOW U.S. CASH HOLDINGS

Source: BNY, Bloomberg

Our take: We expect investor sentiment to remain volatile this week as cash demand rises and speculative positions suffer. The U.S. Treasury is set to sell $783bn in 11 auctions from Monday through Wednesday, creating a week with two definitive endpoints.

Wednesday is likely to bring a mad rush to clean risk into Thanksgiving and the all-important Black Friday sales. Friday will also be the corporate month end, likely prompting another rush to reset risk into December.

Exhibit #1 highlights the bitcoin-to-cash correlation that held through the summer. iFlow U.S. cash holdings are institutional, while bitcoin has been supported by retail investors. The break in that correlation now suggests something has changed. Bitcoin’s drop has erased $1.3tn in market capital.

Forward look: The role of institutional money in crypto markets accelerated with ETF approvals and the Trump election. Allocations to bitcoin and other coins have risen among real money investors, who viewed them as alternatives to the U.S. dollar (USD) and other fiat currencies, similar to gold.

Bitcoin also connects with broader technology shifts, from mining’s link to utilities and computer chips, to its emerging role in payments. AI’s success will ultimately be measured by its return on investment. Rethinking ecommerce on the current internet is part of the broader disruption expected from OpenAI and other large-language model (LLM) advances.

Investors now face a balancing act: navigating cash burn, momentum shifts, and the evolving role of stablecoins relative to bitcoin. Concerns over the USD and other fiat currencies as stores of value are clashing with cash needs. This week will likely test the market’s ability to find liquidity for a potential holiday rally, as cash competes with cash.

U.S. September data isn’t enough

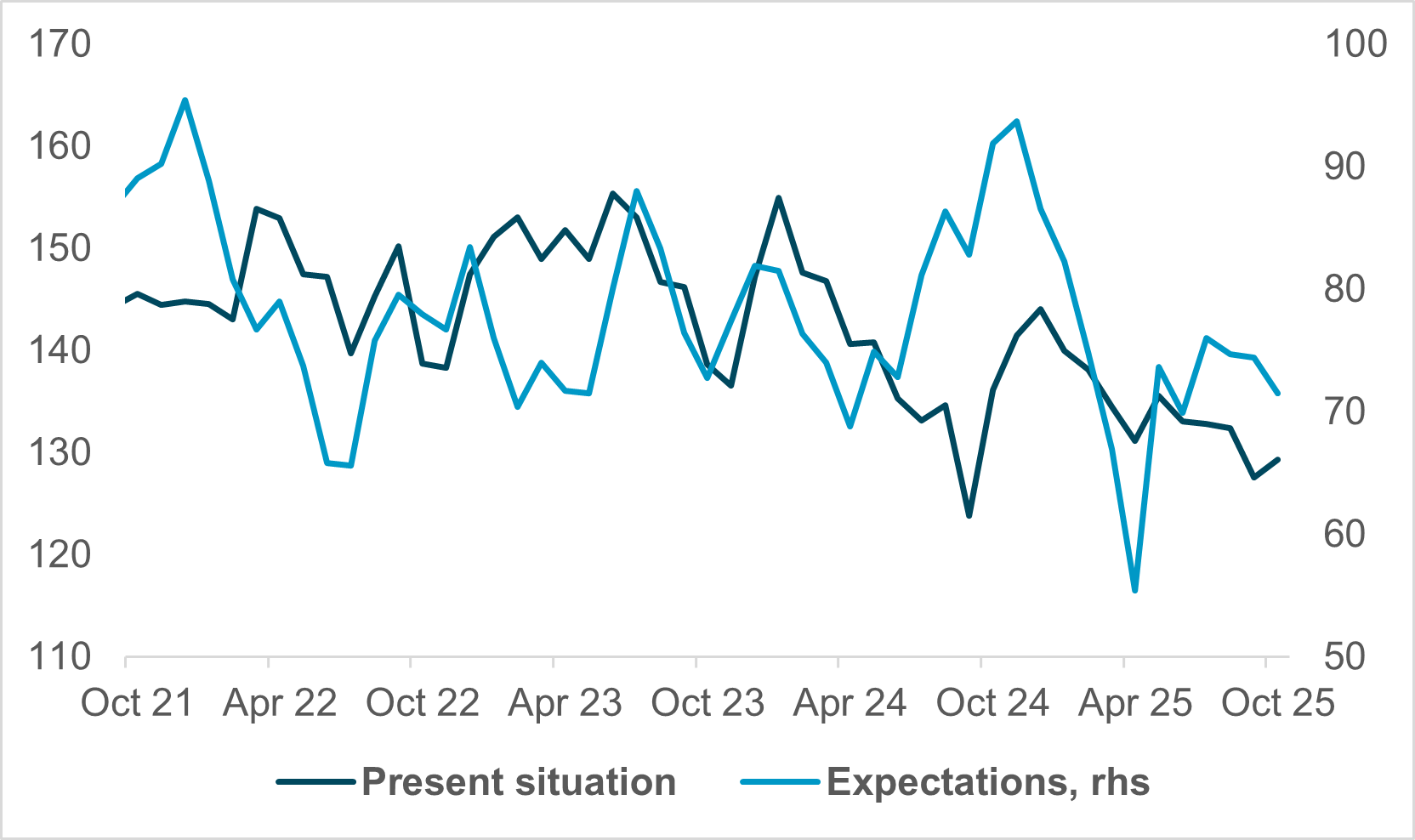

EXHIBIT #2: CONFERENCE BOARD CONSUMER CONFIDENCE

Source: BNY, Bloomberg

Our take: The good news in the U.S. is that we’re finally getting some data. The bad news is that most of the releases refer to September, while we wait for more current reference periods to catch up.

The crucial employment data for October and November won’t be published until December 16, nearly a week after the last FOMC of the year. The Fed won’t be flying completely blind. It will have nearly the full roster of September data, for what that’s worth, and it will also have the December Beige Book, out Wednesday, offering a qualitative assessment of economic trends across districts.

Forward look: Will September data matter? Probably not much. Just look at the mixed September employment report. Markets barely reacted, still waiting to sink their teeth into more timely information.

For what it’s worth, we’ll see the PPI and retail sales on Tuesday and jobless claims on Thursday. Regional PMIs will be published throughout the week. The Conference Board’s Consumer Confidence survey, especially its jobs component, is also due Tuesday.

EMEA: Defining week for the U.K. government and economy

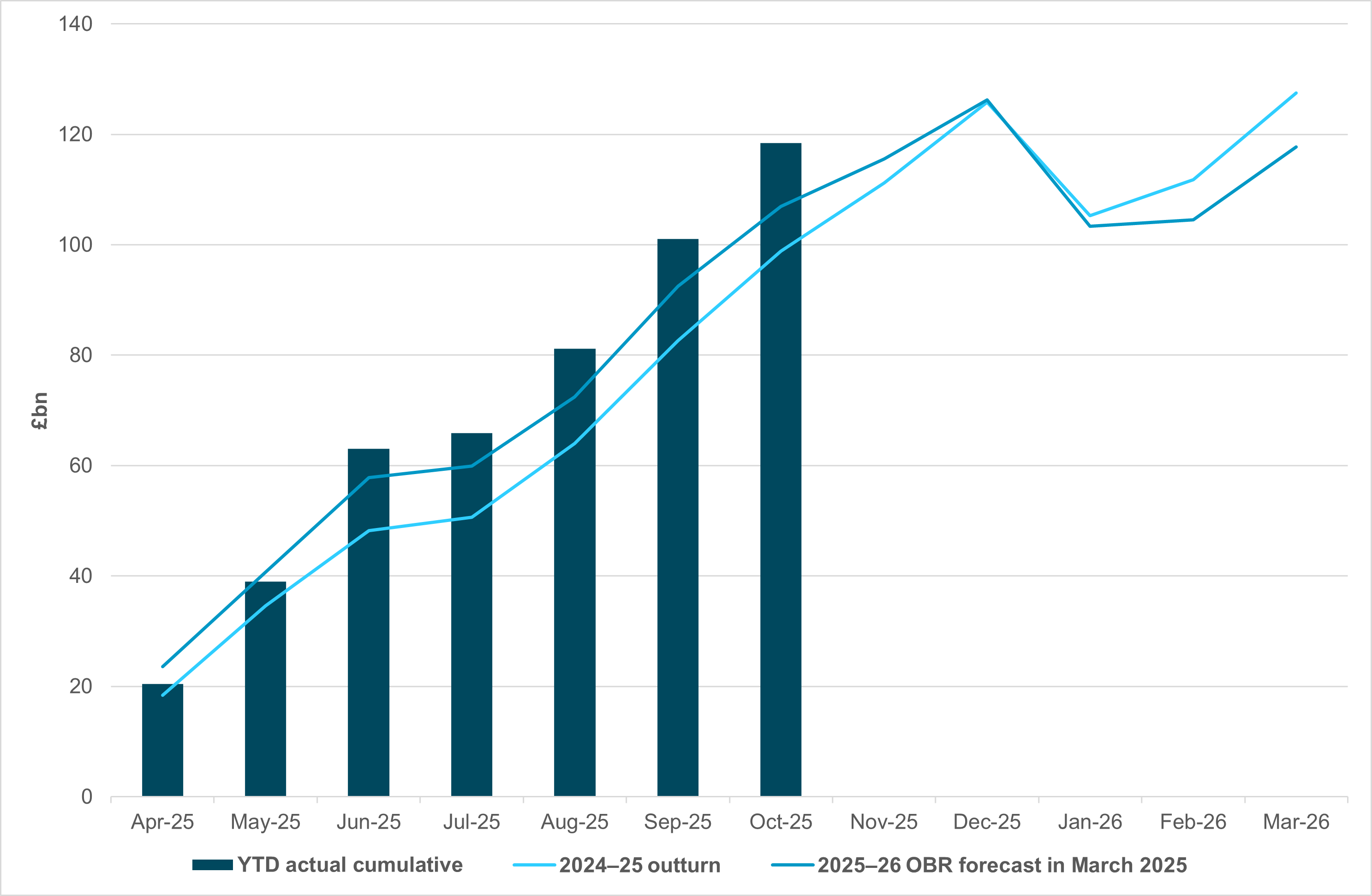

EXHIBIT #3: U.K. REALIZED BORROWING VS. OBR FORECASTS

Source: BNY

Our take: The final round of data ahead of Wednesday’s crucial U.K. budget brought more bad news for Chancellor Rachel Reeves. Borrowing once again came in higher than expected – the highest October level since October 1993, when the U.K. was still recovering from the Exchange Rate Mechanism (ERM) crisis.

Total borrowing is now about £10bn above the Office for Budget Responsibility’s (OBR) original projections for the current fiscal year (Exhibit #3), with little sign of improvement as growth continues to disappoint. The latest spending figures and leading indicators all point to further slowdown ahead, though the marginal softness in income growth will likely provide the Bank of England (BoE) with some easing room in December and beyond.

The main challenge for markets is not the scale of additional revenue generation, but the execution. The late shift away from broad-based income-tax increases – seen as a “clean” and “front-loaded” way to boost fiscal headroom – has given way to a likely hodgepodge of measures. These may not yield immediate gains and could continue to constrain spending and public investment in productivity.

The gilt market’s reaction to the OBR’s new assessments and upcoming gilt issuance forecasts will also be crucial. Any sign of an increase in gilt sales beyond £10bn for the next fiscal year risks material volatility in yields and spreads. Market reaction aside, how the budget is received by the government’s own parliamentary members will add another layer of uncertainty. Markets may begin to discount the sustainability of the current path if leadership questions arise.

Forward look: We continue to see downside risk in the pound (GBP) across the board. The recent adjustment in Fed expectations is unlikely to help. GBP weakness is also apparent against European currencies. The European Central Bank’s (ECB) policy resilience (justified or not), the Swiss franc’s (CHF) safety status amid risk aversion, and strong Nordic fiscal buffers all weigh on GBP.

On all counts, the U.K. is comparing unfavorably. If any of these factors were to change, we’d expect it to be ECB expectations, especially if leading indicators continue to disappoint. President Lagarde’s speech on Friday emphasized the need to build “resilience and strength” alongside a strong “domestic market.” But demand indicators are weakening, and industrial scarring remains a clear risk without urgent investment, which continues to disappoint.

Q3 GDP numbers and some preliminary CPI prints in the week ahead will also present challenges to the ECB’s current policy path if more downside surprises materialize.

On the geopolitical front, we expect a flurry of diplomatic activity as European leaders assess the latest peace proposal for Ukraine. The reported components of the plan will likely face strong opposition from European leaders, who will convene at the G20 to discuss a response. The immediate impact on oil prices has already appeared. But the knock-on impact on Central and Eastern Europe (CEE) will be significant, balancing factors of lower geopolitical risk premia against reduced defense spending.

The region remains overheld across asset classes. Domestic uncertainty, including fiscal strategies and central bank policy execution risks, continues to prompt hedging of currency risk. The market’s reaction to the surprise resignation of Deputy Governor Barnabas Virag of the Hungarian National Bank being the latest example.

APAC: South Korea BSI, Singapore, Australia and Japan CPI, and BI and RBNZ decisions

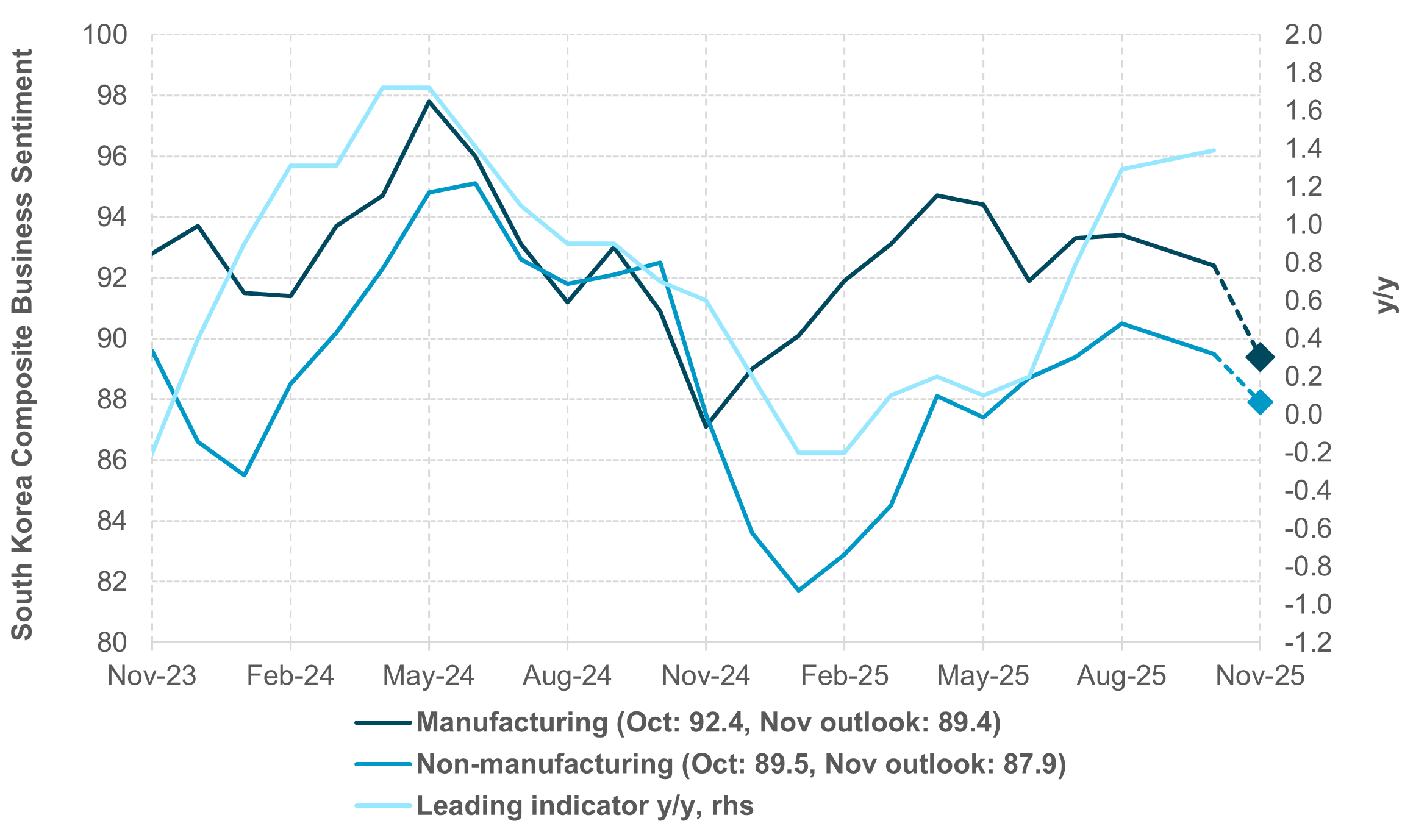

EXHIBIT #4: SOUTH KOREA RESILIENT UNDERLYING GROWTH AMID WEAKENED CONFIDENCE

Source: BNY, Bloomberg

Our take: In the Asia-Pacific (APAC) region, attention this week will center on South Korea. Key data releases include October retail sales, industrial production, the cyclical leading index, November consumer confidence report, and the composite business survey index. Additionally, Thailand and the Philippines will publish October export statistics, and updated inflation figures are anticipated from Singapore, Australia and Tokyo. Labor market reports will be available from Japan and Taiwan, alongside Q3 GDP results from both Taiwan and India.

Recently, business sentiment in South Korea was impacted by renewed trade and tariff uncertainties. These concerns have since eased following the successful conclusion of the ASEAN and APEC summits, during which several trade agreements were signed with the U.S. and regional partners. The November composite business survey index (BSI) in South Korea is projected to exceed earlier forecasts, reaching 89.4 for manufacturing and 87.9 for non-manufacturing sectors. Moreover, the leading index is expected to maintain momentum, offering an early signal for resilient Q4 GDP growth after 1.2% q/q and 1.7% y/y GDP growth in Q3 2025.

October export figures from Thailand and the Philippines will provide key insights into global demand trends. Meanwhile, Q3 GDP data from India, as well as consumer price index reports from Singapore, Australia, and Japan, will hold significant influence over monetary policy decisions within those economies. Any sign of decelerating growth momentum in India could prompt the Reserve Bank of India to reassess its interest rate strategy, having held rates steady over the past two meetings.

In Singapore, consistently low inflation – reflected in September’s headline and core y/y rates of 0.7% and 0.4%, respectively – should reinforce the Monetary Authority of Singapore’s dovish policy outlook. In Australia, a notable downside surprise in September's trimmed mean inflation (2.8% y/y) may be needed to shift forward-looking rate expectations, with markets currently pricing in less than a full 25bp cut until mid-2026. Tokyo’s November inflation print will also be important in shaping the Bank of Japan’s (BoJ) policy direction. BoJ faces a challenging task in maintaining price stability, financial stability and economic growth.

China’s data calendar remains light, featuring only October industrial profits, and no significant economic releases are scheduled for Malaysia or Indonesia.

In terms of monetary policy, the Bank of Korea convenes this week. Given the recent improvement in growth, enduring concerns regarding elevated household debt, rising housing prices in Seoul, and ongoing financial market volatility, there appears to be limited scope for near-term policy easing. The Reserve Bank of New Zealand is expected to cut by 25bp to 2.25%, for a total of 200bp rate reduction through 2025.

Forward look: As in the previous week, APAC assets will be influenced by global dynamics and external factors, particularly uncertainty in the AI and technology sectors, as well as near-term expectations for Fed policy rates.

Foreign investor flows are expected to shape market sentiment in the South Korea’s KOSPI and Taiwan’s Taiex, where recent outflows have contributed to volatility in the South Korean won (KRW) and Taiwan dollar (TWD). Excluding the impact of the USD and other external forces, multiple relative trading opportunities exist within the APAC region.

We hold a positive outlook on:

· Chinese yuan (CNY): Equity market resilience and expected foreign equity inflows

· Indonesian rupiah (IDR): Attractive valuations and macroeconomic strength

· Malaysian ringgit (MYR): Expected normalization following significant multi-year sell-offs

· TWD and KRW: Compelling value due to marked dislocations by excessive foreign outflows

We remain neutral on the Singapore dollar (SGD), due to limited flight-to-quality demand.

Conversely, we hold a negative view on:

· Philippine peso (PHP): Dovish central bank policies, weak growth and domestic instability

· Indian rupee (INR): Ongoing tariff-related risks

· Thai baht (THB): Elevated valuations

As investors head into year-end, the global landscape is marked by tightening liquidity, policy uncertainty, and diverging growth trajectories. The U.S. market remains fixated on the Federal Reserve’s next move, while the sharp correction in crypto and speculative tech highlights a broader re-pricing of risk.

The shift in institutional cash allocations versus digital assets reflects a broader structural shift in how investors view liquidity and alternative stores of value. In Europe, fiscal stress and weak growth metrics continue to undermine confidence in the U.K. and peripheral economies, emphasizing the need for credible policy execution over headline stimulus.

Meanwhile, Asia offers selective resilience, particularly in North Asia, where export momentum and policy discipline remain supportive.

For professional investors, the near-term challenge lies in balancing liquidity preservation with opportunistic positioning. Cash may remain king into December, but the coming weeks could also set the stage for a rebound, if macro data confirm disinflation and policymakers offer greater clarity.

As liquidity and sentiment stabilize, selectively re-entering risk – particularly quality credit and Asia equities – could define early 2026 performance.

The message for now: Stay patient, stay liquid, but prepare for rotation.

Central bank decisions

Israel, BoI (Monday, November 24): The Bank of Israel (BoI) is expected to resume easing with a 25bp rate cut to 4.50%. This marks only the second rate cut from the cycle peak in 2023, driven by extraordinary circumstances. As fiscal impulse fades and supply constraints ease, the BoI will remain alert to a material shift in the cyclical outlook and respond accordingly.

Crucially, inflation is expected to decline further. A recent BoI survey shows average inflation over the next 12 months falling below 2%. Governor Amir Yaron also highlighted the need for balance in fiscal outlays.

Additional easing is likely in response to recent strength in the Israeli shekel (ILS). However, local pricing suggests greater caution around rate cuts. The adjustment in the Fed outlook may offer some relief.

New Zealand, RBNZ (Wednesday, November 26): The Reserve Bank of New Zealand (RBNZ) is expected to cut rates by an additional 25bp to 2.25%, signaling a retreat from the idea that the New Zealand dollar (NZD) holds any carry preference.

Domestic demand is clearly weakening, though this has not yet led to a significant decline in headline inflation. The RBNZ has acknowledged in prior meetings that risks remain in both the upside and downside. Nonetheless, growth and investment continue to soften due to the tail effects of earlier fiscal consolidation, factors that require a strong offset.

NZD valuations will continue to struggle in such an environment, even if general risk sentiment stabilizes.

South Korea, BOK (Thursday, November 27): We expect the Bank of Korea (BoK) to hold its policy rate at 2.50% for the fourth consecutive meeting and maintain a dovish stance, leaving the option open for further easing.

While the economy has not fully recovered, there is evidence of an underlying growth momentum. However, the increasing volatility in financial markets should not be overlooked. It is premature to conclude that the easing cycle has ended.

Markets will closely monitor the BoK’s upcoming macroeconomic forecast, with a chance for upside GDP revision. As of August, the BoK projected GDP growth of 0.9% in 2025, rising to 1.6% in 2026. Headline inflation is expected to ease to 1.9% in 2026 (from 2.0% in 2025), while core inflation is forecast to remain stable at 1.9% in 2026.

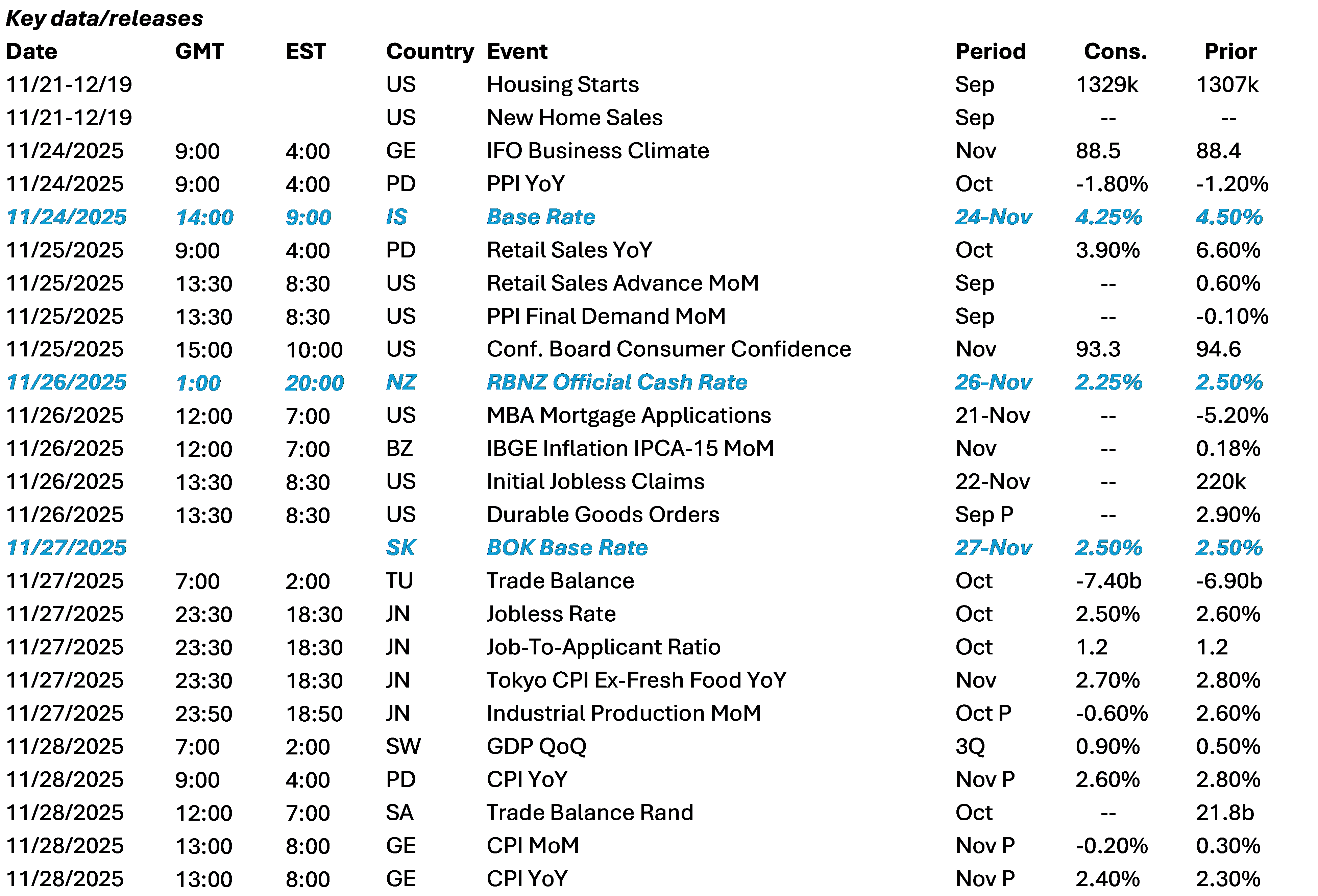

Data Calendar

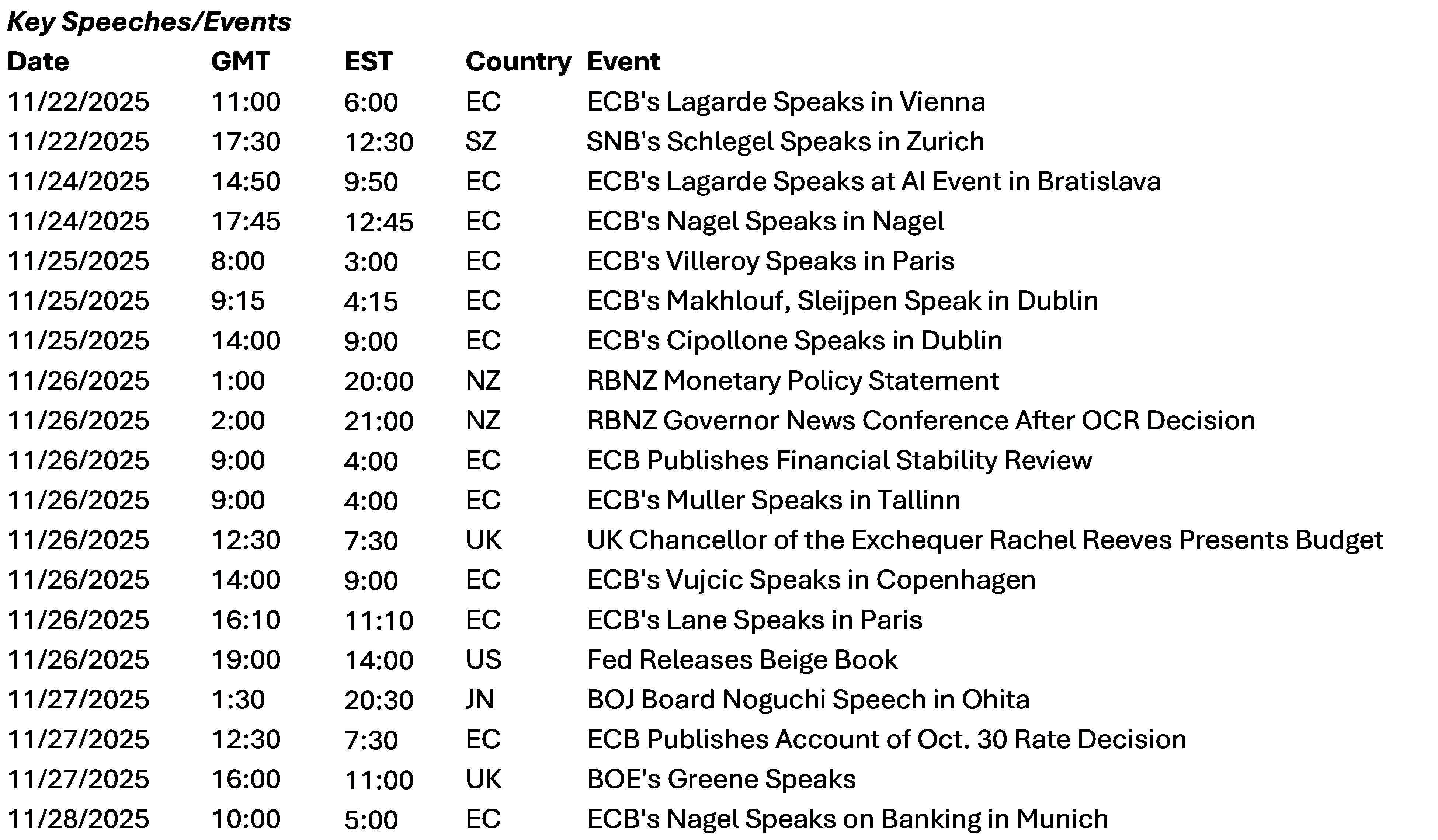

Event Calendar