Volatility resets the narrative

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

The win-win hopes for 2026 – where U.S. and global growth are coupled with AI-driven productivity and ample cash to support ongoing trends – changed last week. The new narrative for markets isn’t so clear.

Headline and volatility noise need to subside first, allowing a rethink of the “own the U.S. but hedge it” story. We could blame the shift on AI adding to job worries, as new Anthropic tools drive down software and financial analysis companies. We also see a focus on AI investments and where the money comes from, with Oracle credit default swaps becoming a barometer for borrowing bubbles. Investment-grade issuance in 2026 is on pace to break $400bn by the end of February. The partial government shutdown in the U.S., the expected Liberal Democratic Party (LDP) win in Japan, ongoing EU budget debates, and the U.K.’s political paroxysm make clear that deficits are not going away, adding to a yield curve steepening bias. The week ahead will test investors’ patience for the noise and volatility.

1) Elections. The weekend election in Japan matters for the size and scope of the LDP win. A lower house with a 67% majority may lead to a weaker JPY if only because there will be a test of fiscal deficit control. Bank of Japan (BoJ) rate hikes and Japanese government bond instability may follow. Thailand’s election will also matter as the leading opposition party could end the string of failed leadership and solve the ongoing border crisis with Cambodia. The relationship between the THB and gold is also likely to shift with a new Gen Z government agenda.

2) U.S. CPI and jobs. U.S. data matter to markets again, with weaker JOLTS (Job Openings and Labor Turnover Survey), weekly claims, and a jump in layoffs leaving investors worried about the size and scope of any jobs shift relative to price. Affordability remains the key word for any discussion about 2026 politics and odds for policy shifts. FOMC speakers and other central bankers sounding less hawkish will be critical in calming markets.

3) Q4 earnings. The role of mega-cap tech earnings has been notable this year and won’t end until Nvidia reports on February 25. Until then, we are stuck watching adoption, margins and hiring plans. The rotation trade out of tech and into small- and medium-sized companies continues, as does the push for international diversification. The performance of the equal-weighted S&P 500 versus the market-cap index becomes the risk barometer.

4) Diversification and correlation. The failure of gold, silver and Bitcoin has prompted questions about USD alternatives and currency debasement. The correlation between the commodity-linked FX trade, bond markets with high real rates, and equity markets paying for value versus growth has shifted in the last week, challenging assumptions around diversification.

Is there cash to buy the dip?

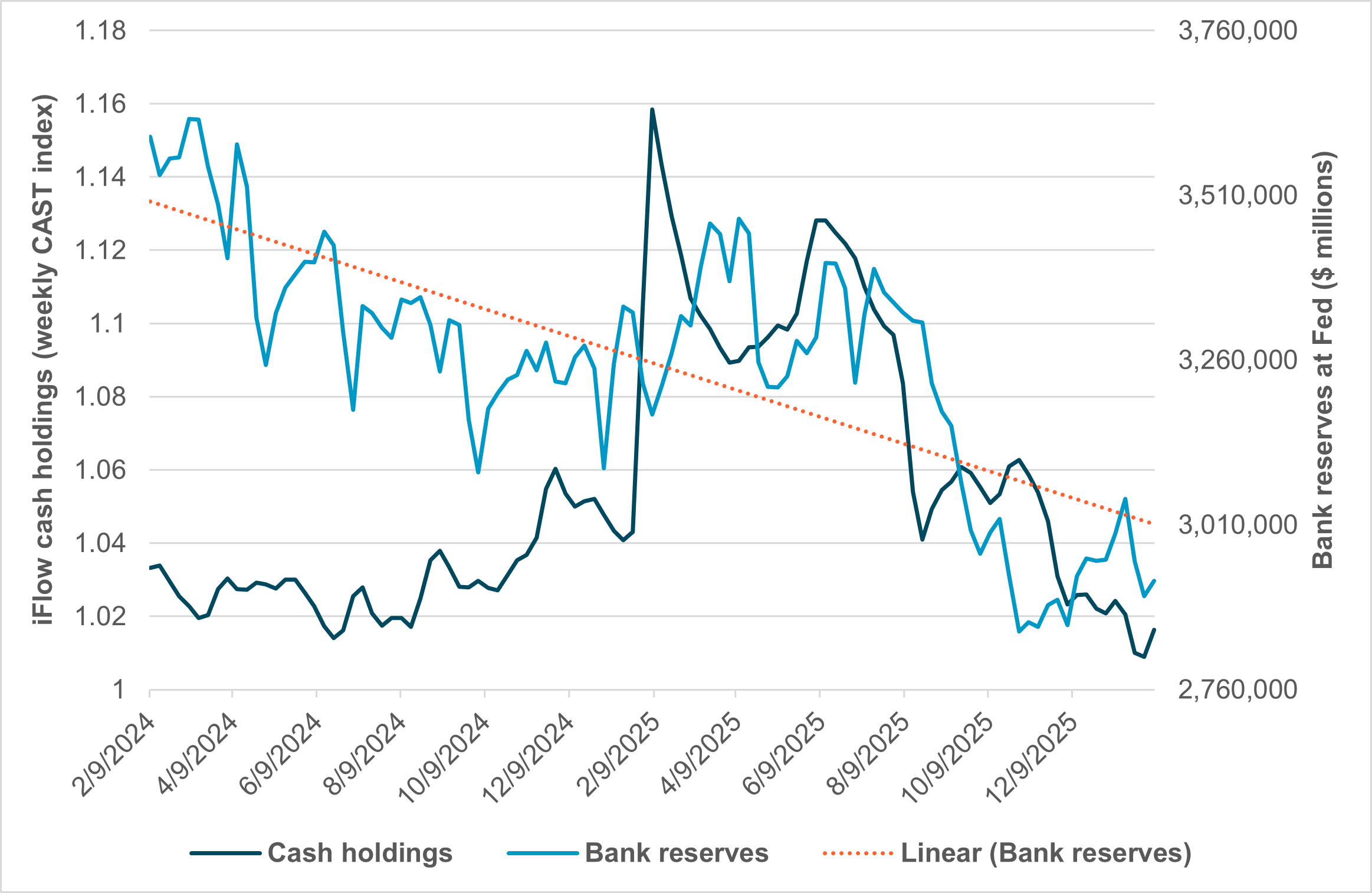

EXHIBIT #1: U.S. BANK RESERVES AND IFLOW CASH HOLDINGS

Source: BNY, Bloomberg

Our take: Cash competes with cash. The rise in T-bill issuance will come first from other cash holdings. iFlow cash holdings do not include money market funds, but they do cover other equivalents. The link between declining bank reserves and our cash holdings drifting lower suggests that the market has less liquidity to absorb shocks. The shift from abundant to ample reserves was the driving force for the Fed to start its $40bn-a-month T-bill buying.

Forward look: The key question for investors is whether that Fed action and recent market volatility force another reaction. There is a need for an alternative financial conditions index to answer the question that bothers many as we close another week of negative equity markets: Is there enough cash to buy the dip?

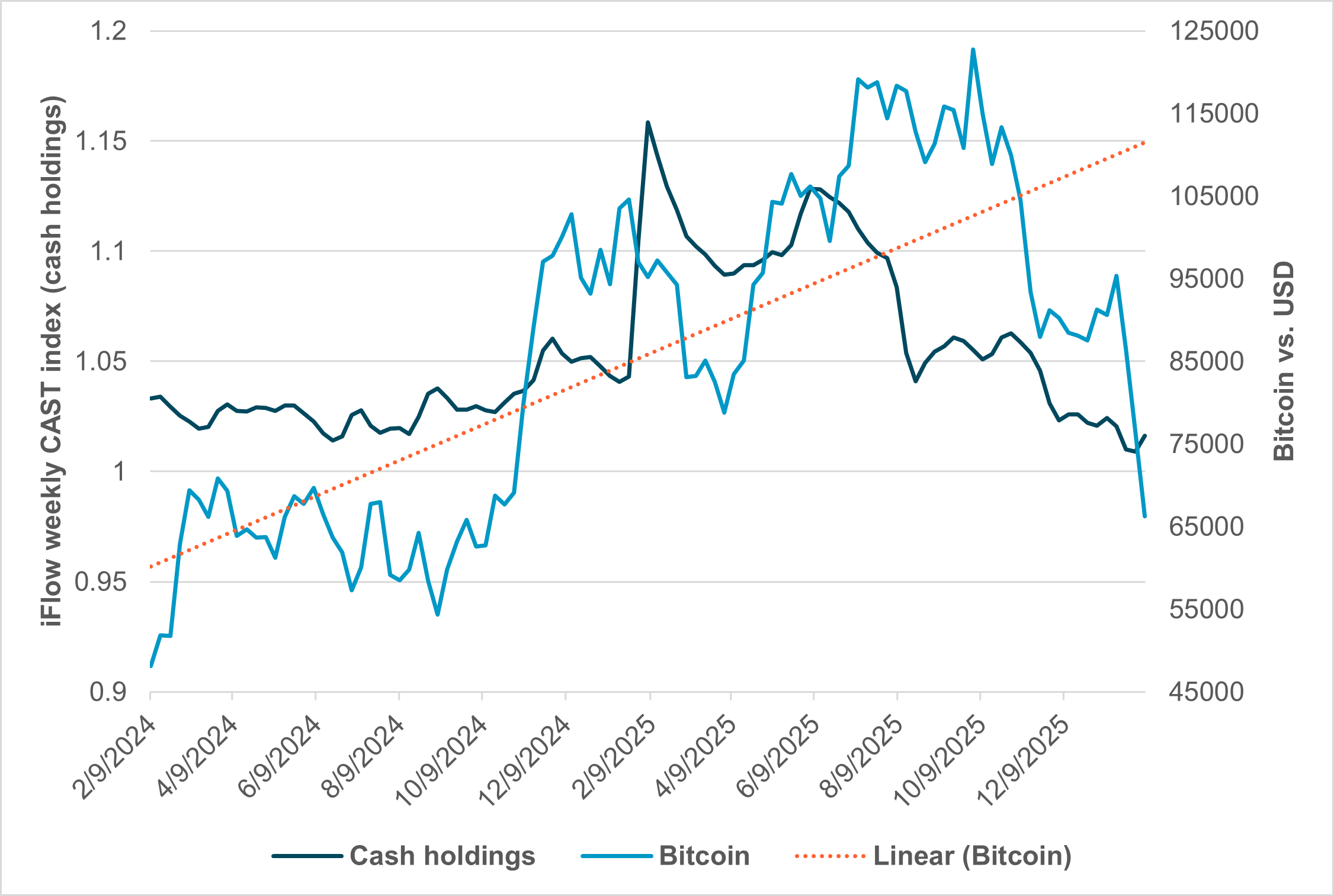

EXHIBIT #2: BITCOIN PRICE AND IFLOW CASH HOLDINGS

Source: BNY, Bloomberg

Our take: Cash competes with cash. The rise in T-bill issuance will come first from other cash holdings. iFlow cash holdings do not include money market funds, but they do cover other equivalents. The link between declining bank reserves and our cash holdings drifting lower suggests that the market has less liquidity to absorb shocks. The shift from abundant to ample reserves was the driving force for the Fed to start its $40bn-a-month T-bill buying.

Forward look: The key question for investors is whether that Fed action and recent market volatility force another reaction. There is a need for an alternative financial conditions index to answer the question that bothers many as we close another week of negative equity markets: Is there enough cash to buy the dip?

U.S. markets still watching jobs data and FOMC reaction

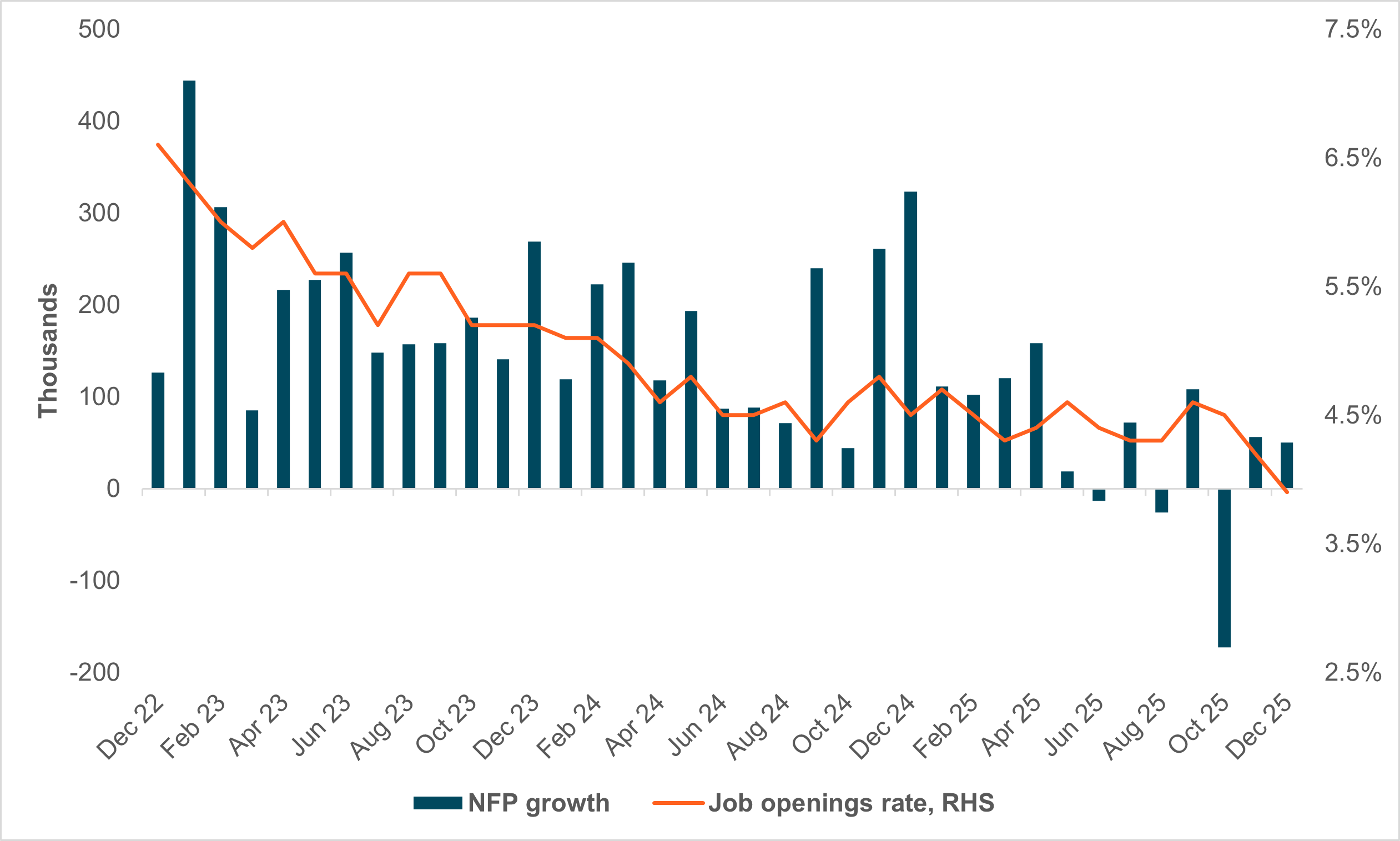

EXHIBIT #3: U.S. NONFARM PAYROLLS AND JOLTS

Source: BNY, Bloomberg

Our take: Last week’s brief government shutdown led to the postponement of the December employment report until Wednesday. Given poor labor data last week (Challenger job cuts, JOLTS, and claims), nonfarm payrolls (NFPs) will be closely watched. We have been long concerned that labor market weakness is the biggest risk to the macroeconomy. Expectations are for an increase in hiring of 70,000 (75,000 in private job creation), and a steady unemployment rate of 4.4%. We think the consensus is rather demanding and subject to downside surprise.

NFPs are not the only major data release this week, with CPI due on a foreboding Friday the 13th. PCE last month was slightly troubling, and stubborn, sticky inflation combined with a potentially moribund labor market makes the Fed’s interest rate path more problematic. Core inflation is expected to rise to 2.8%, which would represent movement in the wrong direction for January’s data. Monday’s retail sales are also a potentially important signal for consumption and growth.

Forward look: Fed speakers of note include Cleveland’s Beth Hammack and Dallas’s Lorie Logan, both voting members and inflation hawks, on Tuesday, with Logan speaking again the following day. We’ll of course be listening for their views on rates as well as any remarks that position FOMC members relative to Warsh’s nomination. Governor Christopher Waller, who dissented again in favor of a 25bp cut two weeks ago, is also on the schedule, but his remarks this time around will likely be limited to digital assets, the advertised topic of his speech on Monday.

EMEA: ECB forecast tolerance bands to be tested

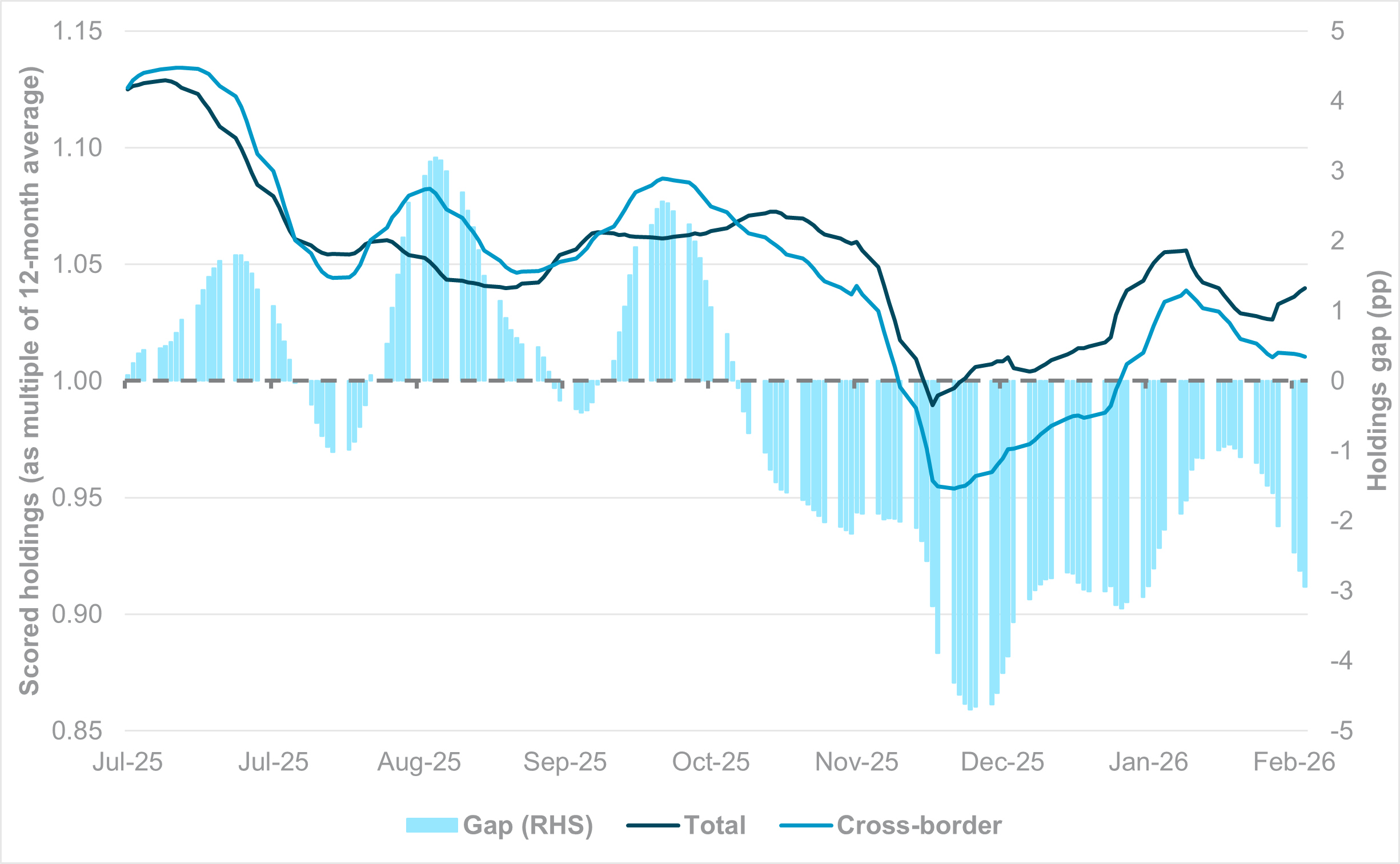

EXHIBIT #4: CLEAR DETERIORATION IN CROSS-BORDER GILT INTEREST

Source: BNY

Our take: European Central Bank (ECB) President Christine Lagarde attempted to tackle the impact of the euro’s strength head-on during the February policy decision. In our view, she was more candid about the risks than expected, which may help assuage internal concerns that “benign neglect” would remain the main approach. The day after the decision, Governing Council member Madis Müller stressed that the December outlook was still a “good basis” for decision-making.

We find this point extremely pertinent because even at current EUR levels just below 1.20, based on the December forecast projections, the exchange rate has moved beyond the 75th percentile of its forecast bands.

This entails two key technical assumptions. First, the thresholds were generated using implied volatility from the EURUSD options markets in November. Comparatively, risk appetite has deteriorated, so in theory the level of uncertainty should be greater and generate wider bands – rendering higher levels of EURUSD more tolerable. If the December assumptions still hold, then the Governing Council would implicitly not accept a sudden EUR surge.

The second and more challenging factor for the ECB is to gauge the impact of exchange rate pass-through (ERPT) as this is not static. If consumers of imports – both households and corporates – are now displaying higher price sensitivity because of economic uncertainty, then the impact of pass-through could be stronger through the income channel. A strong exchange rate would swiftly divert consumption to imports and hurt local producers, or export revenue would decline and the income loss could also cause a faster retrenchment in demand: these are two sides of the same coin.

In June, the ECB provided an updated ERPT model. Time-varying pass-through to import and consumer prices is estimated using single-equation regressions with drifting coefficients and stochastic volatility, covering Q1 1995 to Q4 2024 for import prices and Q1 1997 to Q4 2024 for consumer prices.

The model’s calculated impacts show the percentage effect on prices four quarters after a 1% depreciation in the euro nominal effective exchange rate. At the 84th percentile – which is realistically where current EURUSD exchange rates sit relative to December baseline – the disinflation drag is minimal, and this was largely reflected in the alternative forecasts in the ECB’s December projections.

This highlights a fundamental issue with prior data: ERPT is asymmetric, whereby a weaker exchange rate generates inflation, but a stronger exchange rate doesn’t necessarily do the same. Between 1995 and 2024 – the underlying sample set – Germany and the Eurozone displayed unmatched export prowess. There were no U.S. tariffs, and China was not yet a strong enough competitor in high-value-added capital goods.

This has changed markedly over the last 18 months, so we question whether these technical assumptions still apply. Lagarde acknowledged these factors openly during her press conference. Given the growth risks at stake, the ECB cannot afford to be reactive and lean more on judgment.

Forward look: With the large roster of ECB speakers this week, whether changes in the Governing Council’s judgment are taking place will be crucial for the euro and broader markets. In addition to EURUSD, how EURJPY behaves in the coming days after the Japanese lower-house election does have a bearing on the broader euro effective exchange rate.

The recent steepening in Eurozone sovereign curves has added to the urgency to manage financial conditions, though sovereign spreads remain sufficiently contained for now, suggesting markets are giving the fiscal trajectories of France and Italy the benefit of the doubt. Furthermore, the current tech-focused equity market adjustment will likely impact European bourses less, but local markets will not be immune to liquidation risk, representing another financial-conditions input that requires close monitoring.

Elsewhere, domestic political factors and broader geopolitical developments are in play. The Munich Security Conference will be held between February 13 and 15. The 2025 iteration forewarned many of the ruptures in the transatlantic alliance that were to come in the subsequent year. We expect the European tone to have hardened significantly, but the path toward strategic autonomy remains long and expensive.

Gilt markets will also be in focus given the re-emergence of political risk in the U.K. Our data indicate that cross-border investors continue to shy away from the market relative to local investors (Exhibit #4), so Downing Street will urgently need positive growth-related news from the national accounts and industrial production figures due on February 12.

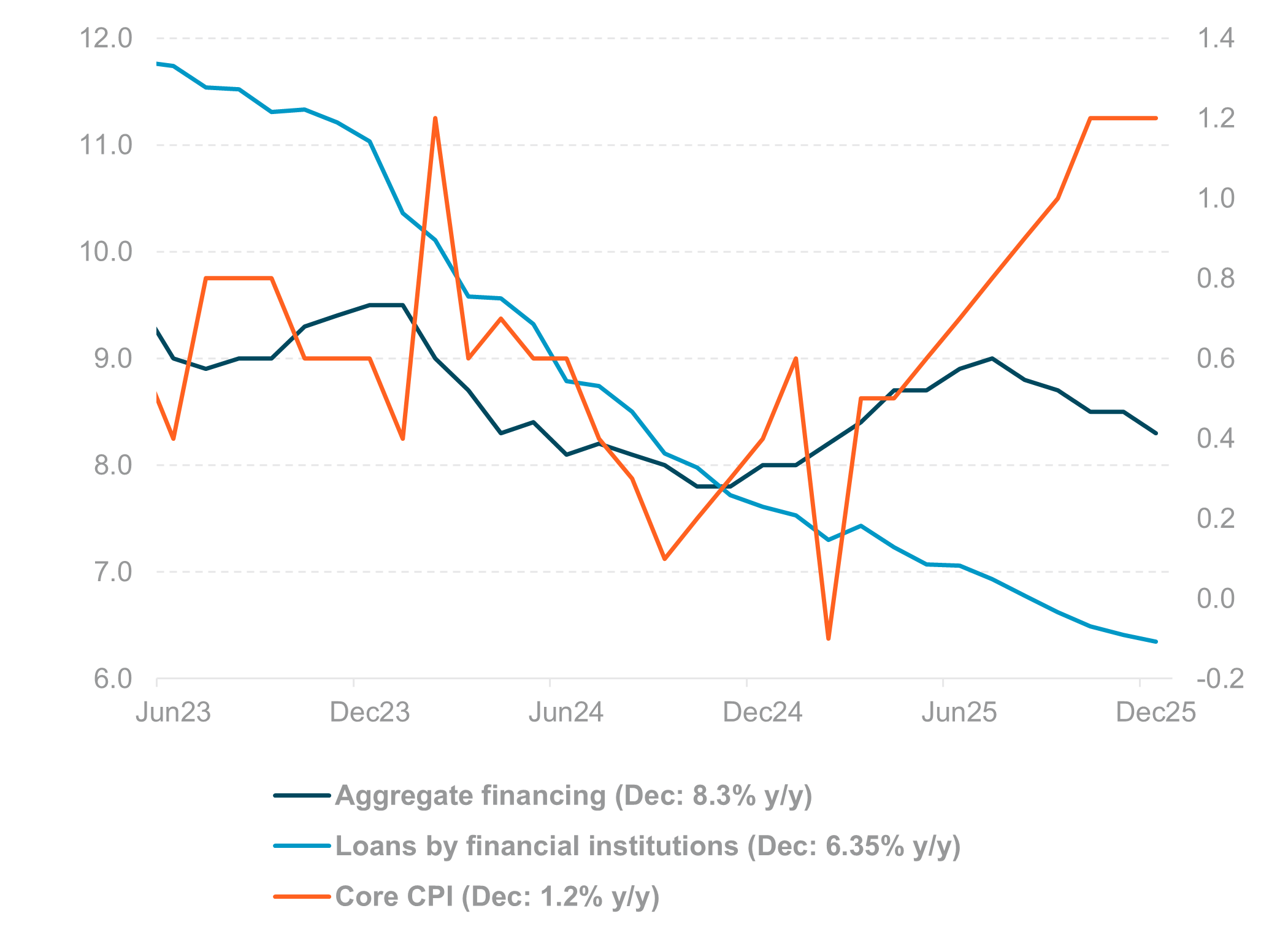

APAC: China credit, inflation and the need to prove growth momentum

EXHIBIT #5: CHINA CREDIT GROWTH AND INFLATION

Source: BNY

Our take: In the Asia Pacific (APAC) region, China’s January aggregate financing and M3 will be closely watched for signs that credit demand is stabilizing after the People’s Bank of China cut targeted policy tools and expanded lending quotas. China CPI and PPI will indicate whether deflationary pressures are bottoming out or becoming more entrenched. Note that China’s headline CPI rose to 0.8% y/y in December 2025, the highest reading since February 2023. China’s new home prices face renewed downside risk, with little sign of stabilization. Latest data showed that the 70-city average for new and existing home prices was –3% y/y and –6% y/y, respectively.

Elsewhere in North Asia, Taiwan’s January exports and trade data will be scrutinized for supportive evidence of an extended cyclical recovery in the global tech cycle. South Korea’s first 1–10-day exports will provide a timely read on external demand after a stellar 33.9% y/y export growth in January. South Korea’s January bank lending to households will be important from financial stability perspective, given elevated domestic household debt and house prices, especially in Seoul.

Japan’s data flow – including December real cash earnings, January PPI, the Eco Watchers survey, and Tokyo office vacancy rates – will shape expectations for wage-price dynamics and therefore the timing of the further BoJ policy normalization.

Across ASEAN and South Asia, the focus shifts to growth momentum, inflation and domestic demand. India’s January CPI, exports and trade data will be interesting, but market impact is likely to be limited given the Reserve Bank of India meeting last week. Trade deals between the EU and India, along with the lowering of tariffs on exports to the U.S. from 50% to 18%, may lend a boost to trade in the coming months. Malaysia’s December industrial production and manufacturing sales, together with Q4 and 2025 GDP, will frame the growth outlook heading into the new year, while Thailand and Indonesia’s January consumer confidence readings will signal the strength of household sentiment.

In Singapore, the focus will be on the potential upward revision of 2026 GDP growth compared with 1.0% to 3.0% as projected in November 2025.

In the Antipodes, Australia’s household spending, consumer confidence, NAB business confidence, home loan data, and inflation expectations will inform views on demand and disinflation, while New Zealand’s PMI manufacturing and Q1 two-year inflation expectations will be key for its central bank’s policy outlook.

Lastly, there are no monetary policy meetings this week. New Zealand (February 18), Indonesia (February 19), the Philippines (February 19) will convene next week, followed by Thailand (February 25) and South Korea (February 26) later in the month.

Forward look: Global market volatility increased sharply in February, driven more by AI sector sensitivity and asset prices than by geopolitical or trade issues. While recent turbulence has impacted investor sentiment, it has not changed our medium-term positive outlook for APAC. However, heightened risk aversion could prompt short-term reductions in risk exposure. Within the region, India benefits from reduced U.S. tariffs, with the equity market the key beneficiary. Gains in the Indian rupee and government bonds are expected to be short-lived, as deficits remain the top concern.

Confidence in Indonesian assets has dampened on a potential MSCI downgrade and Moody’s revision of the outlook from stable to negative amid policy uncertainty. Chinese equity inflows are likely to strengthen the CNY, while the South Korean won is influenced by both foreign investment and domestic outflows in equities.

As the new week begins, investors face a market environment defined less by conviction and more by recalibration. The optimistic 2026 narrative of synchronized growth, abundant liquidity, and AI-driven productivity has been interrupted by volatility, labor market uncertainty and tighter financial conditions.

With key U.S. inflation and employment data ahead, alongside critical central bank commentary, markets will test whether recent weakness reflects a temporary adjustment or a more durable shift in risk appetite.

Liquidity dynamics – particularly declining bank reserves and rising bill issuance – suggest less capacity to absorb shocks, raising the bar for “buy the dip” strategies. At the same time, failed diversification across gold, crypto and commodities forces a rethink of portfolio construction.

For financial professionals, the focus should remain on correlations, cash management and policy signals rather than headline-driven momentum. Patience, disciplined risk management and sensitivity to macro inflection points will be essential as markets attempt to find firmer footing.

Central bank decisions

Peru, Central Reserve Bank of Peru (BCRP) (Thursday, February 12): We believe the BCRP decision could attract more attention than usual, as positioning in the country’s assets remains at extremes and vulnerable following the correction in silver prices. We do not expect the BCRP to take a medium-term view on terms of trade or structural factors for now, but there is limited scope for a stronger easing bias as inflation is ticking up gently and the labor market remains tight. EM central banks are predisposed to keep rates on hold during periods of market volatility, and the PEN will need strong real rate support for the time being.

Source: BNY

Source: BNY