Sentiment shifts: Rally meets reality

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

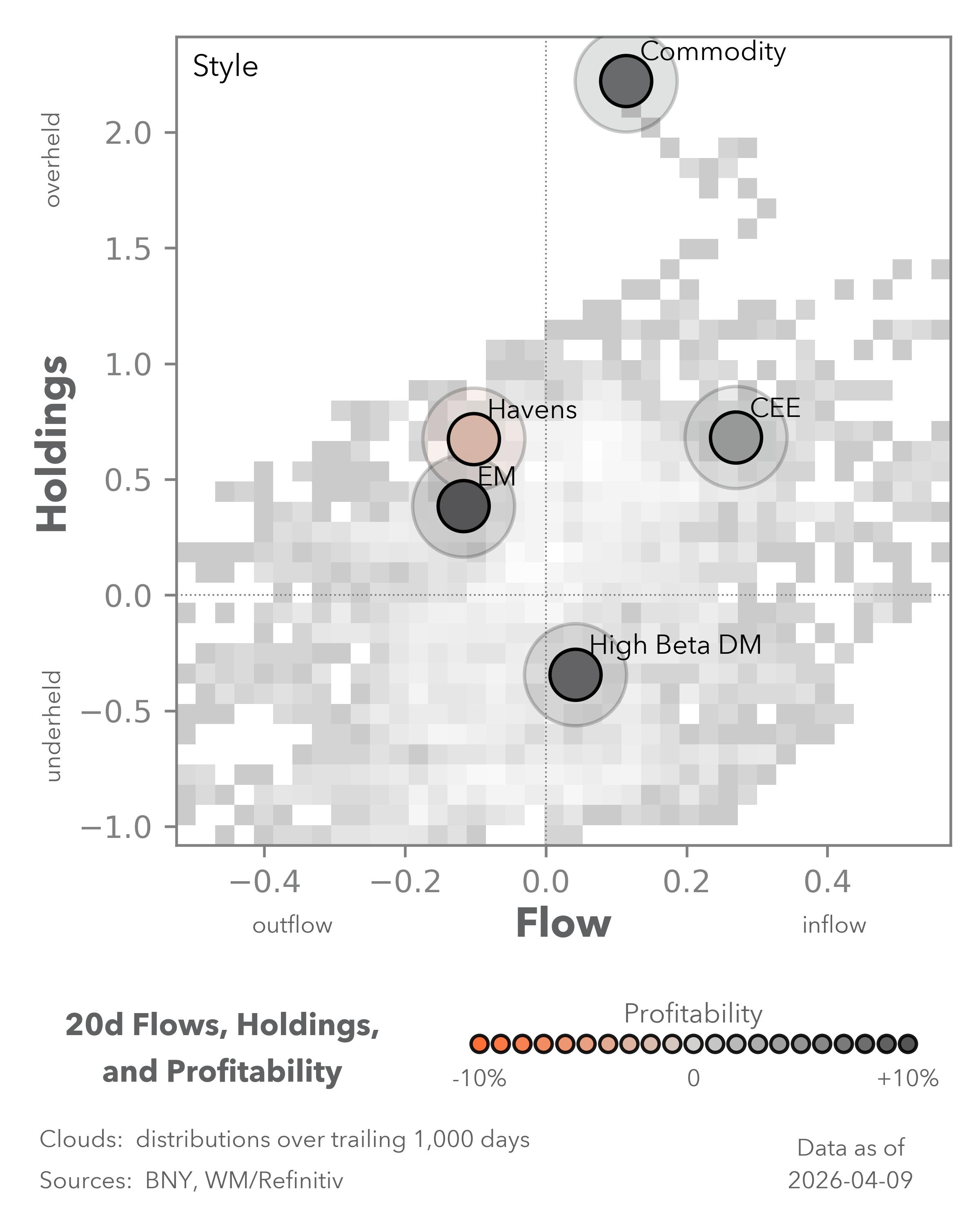

The relief rally across markets on the U.S.–Iran ceasefire stands out as the defining move of the past week. The moves in APAC equities, European bonds, and oil were four-sigma events – statistically expected less than once in a century. Of course, it did happen last April, when President Trump provided relief with a 90-day delay in his “liberation day” tariffs. For all markets, the shift from extreme volatility begs the question of whether a fragile ceasefire and nascent talks for peace can hold. Geopolitical risk remains hard to manage, with the search for new safe havens a key part of the discussion. Sharp pricing shifts in USD, CNY, EM bonds, and tech stocks are part of the puzzle.

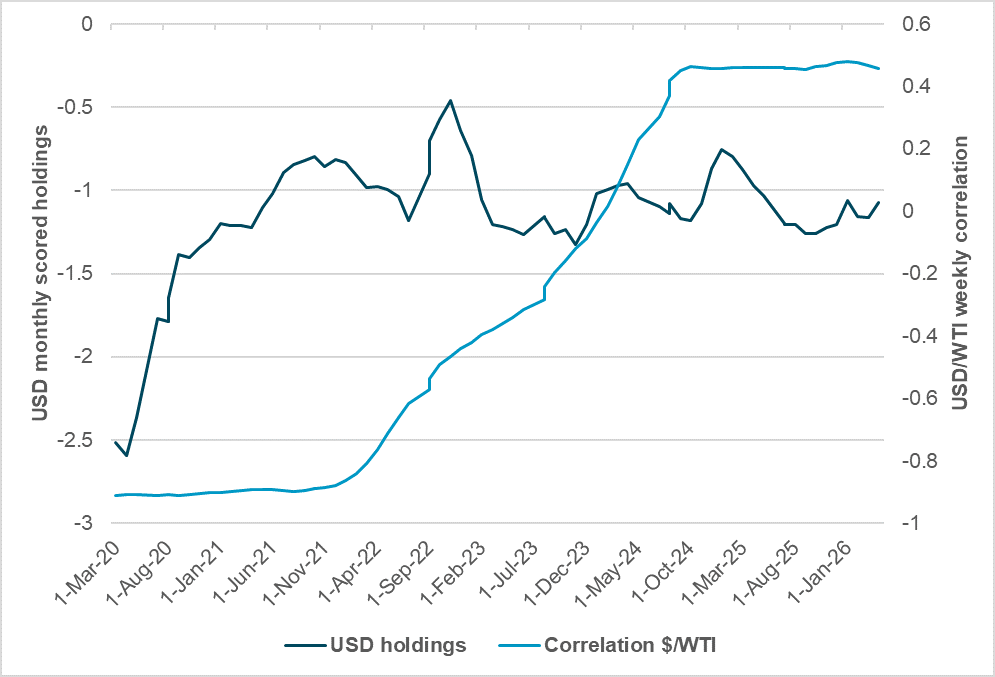

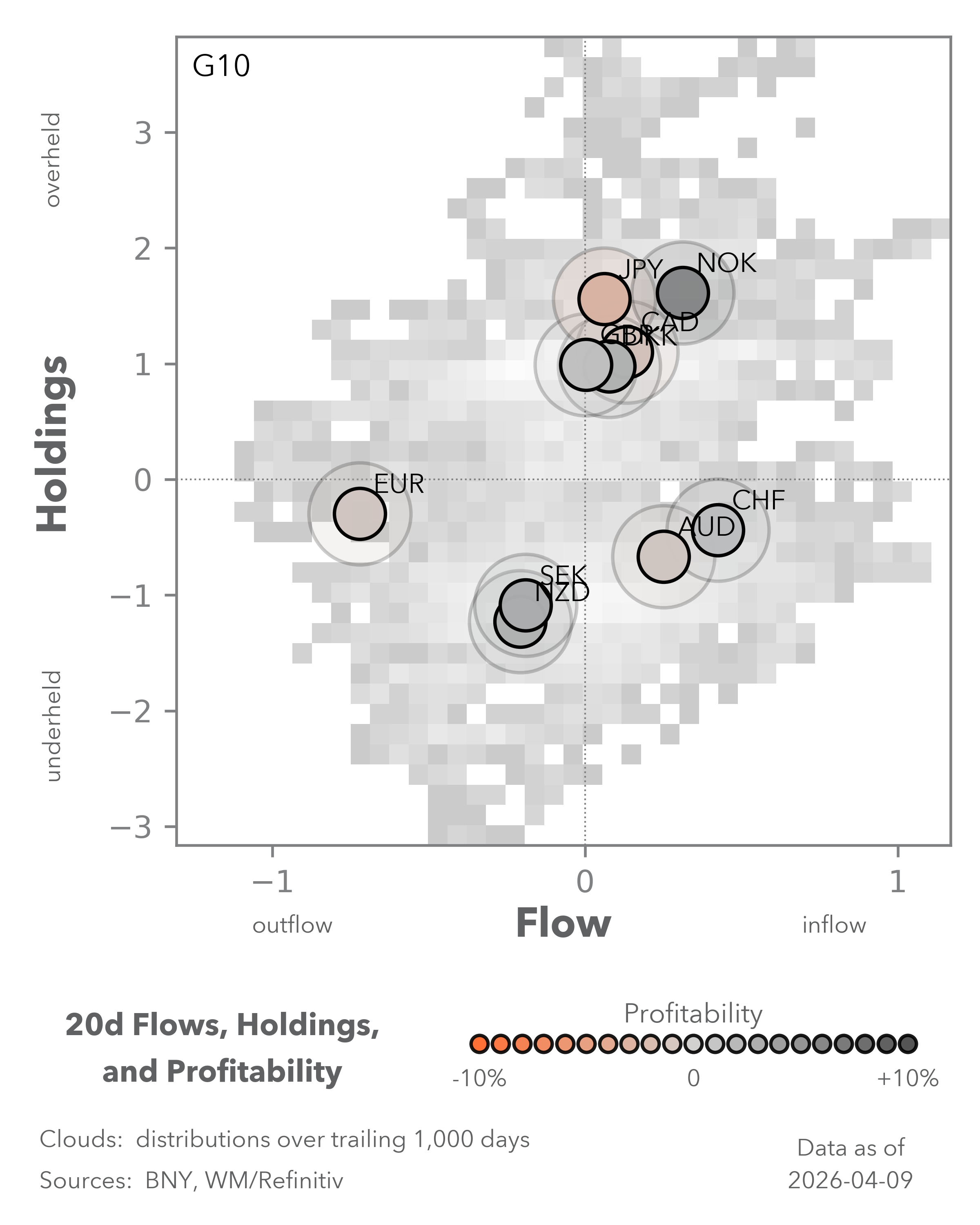

How much does oil dominate markets

EXHIBIT #1: USD HOLDINGS AGAINST WTI/USD CORRELATION

Source: BNY, Bloomberg

Our take: The USD’s link to WTI peaked in early March and continues to matter even after the ceasefire. Fears of stagflation remain even after the U.S. core CPI report on Friday. The Fed’s ability to look through the energy shock will rest on how this price shock transmits to the broader economy.

The USD-oil correlation shifted most significantly after COVID, with the war in Ukraine a key turning point. Last week’s dip in the correlation was modest, and the 0.45 it remains statistically significant – keeping the two assets closely linked in model-driven trading. The tendency for USD to rise with oil has also lifted USD-equity correlations. Notably, USD holdings tied to oil-linked positioning have also been rising since the war began.

Forward look: A reversal of USD down with oil is a key concern for investors and could also extend the nascent uptrend in equities. The duration of the war and the breadth of the energy supply shock from the Strait’s closure will be critical to how markets trade in the week ahead and beyond. The bigger surprise may come from USD holdings and hedging demand, which bear watching into any equity or bond rally tied to peace developments. How investors position and hedge into Q2 will determine whether the positive correlation between oil and global assets persists or breaks down.

North America: Stagflation signals and Fed speakers

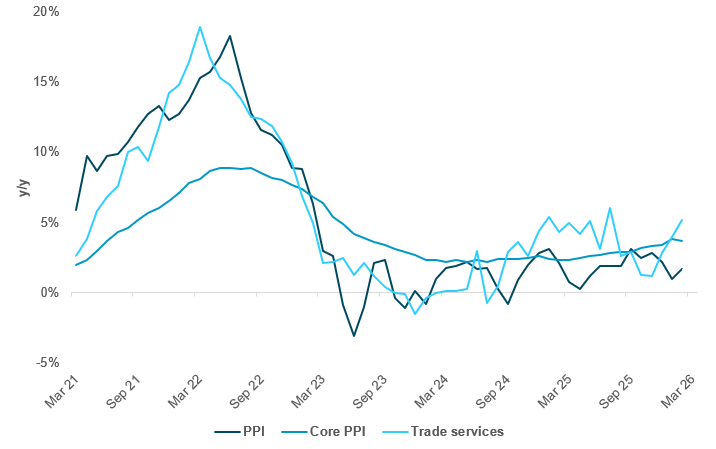

EXHIBIT #2: U.S. PPI TO PICK UP

Source: BNY Bloomberg

Our take: Though considerable data is due this week, most of it is second tier, including sentiment monitors: NFIB Small Business Optimism on Tuesday, Empire Manufacturing on Wednesday, and Philly Fed on Thursday.

The Federal Reserve also releases its April Beige Book on Wednesday. This comprehensive qualitative survey of regional business conditions could be particularly significant, as it will show how local firms across the country are faring against the backdrop of the war.

The March PPI, due Tuesday, will shed light on input costs for producers and suppliers, and on their capacity to pass those costs through to consumers. CPI last week was quite strong, as expected, and PPI should reiterate that message, especially for energy inputs. We’ll also watch the trade services measure – a proxy for markups – to gauge whether firms are passing on price increases on to customers. It has been rising notably in recent months.

Forward look: Fed speakers are abundant this week, ahead of the media blackout starting Friday. We’ll hear from key FOMC members, including Governors Stephen Miran (twice), Michael Barr (also twice), Michelle Bowman and Christopher Waller. The FOMC meeting the following week is unlikely to produce any rate changes. But Fed speakers this week will probably signal how key decision makers are weighing the employment-inflation trade-off, a calculation made more delicate by the Middle East conflict.

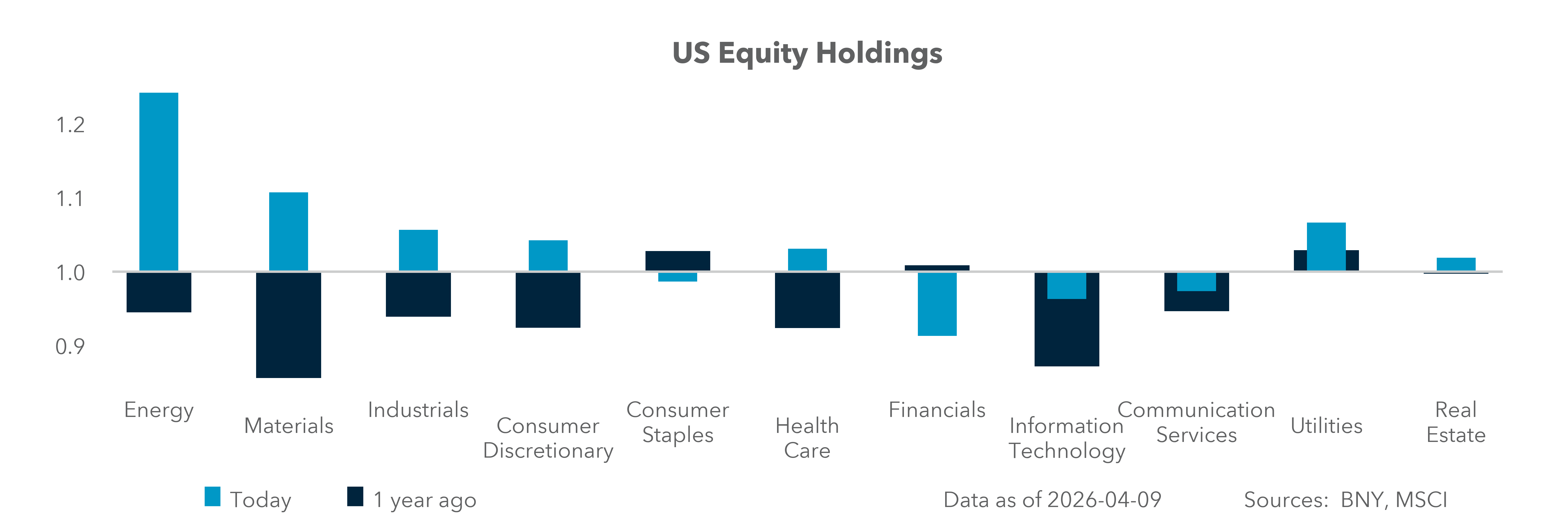

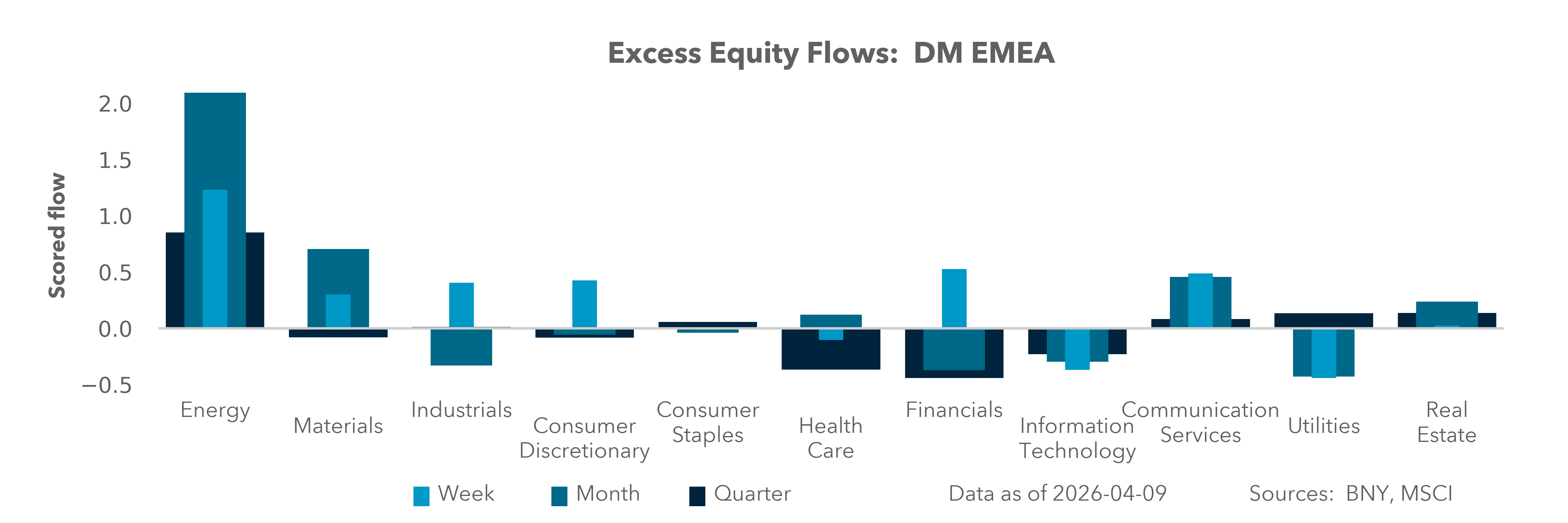

EMEA: Fiscal conservation likely to move up the agenda

EXHIBIT #3: EUROPEAN FIXED INCOME FLOWS BY MATURITY AND SECTORAL EQUITY FLOWS

Source: BNY

Our take: It will be a crucial week for policy communications as the European Central Bank (ECB) assesses next steps. Views on the April meeting vary widely. We believe, however, that the notion of a hike before second-round effects emerge remains a minority position on the Governing Council. March PMI figures indicate clear gains in input prices, but there is no commensurate reaction in labor yet. The consensus among governments and central banks is that the conflict’s growth impact will be negative over the medium term. Early tightening therefore risks tightening financial conditions at exactly the wrong point in the cycle. However, the pain for corporates from both the input price and demand side is very real, and even with a fragile cease fire in place, price normalization will take time. Households are already receiving some government support but calls for fiscal buffers to extend to corporates may also grow in the period ahead. Italy’s Prime Minister Giorgia Meloni has already stated that the EU should suspend deficit rules as the war continues. This will be politically fraught, especially if the loudest calls come from countries with weaker fiscal positions.

Given that most mainstream European parties – including those in government – remain politically weak, pushing back against a stronger fiscal response will be difficult. Fiscal restraint will be needed to avoid unsettling bond markets, as inflation remains an issue. Some industries may therefore face derating if the anticipated fiscal windfall fails to materialize.

The biggest casualty could be defense. Compared to other sectors in developed Europe, industrials and consumer discretionary have struggled materially over the past month (Exhibit #3). Weak growth is likely leading to credit concerns, which are also weighing on financials.

As real rates have risen on tightening expectations, duration is performing well; Europe is not facing a funding shortage for now, only higher costs. In the near term, we expect fiscal stimulus to lean stronger, subject to inflation risk – but selectivity is crucial. Industries and sectors that require discretionary government spending support will likely struggle as a result. Defense will be at the forefront of such risks.

Forward look: There will be more than a dozen ECB speeches in the week ahead, and any convergence in views could move markets. We still expect the ECB to hike once this year, but markets remain unsure whether the April meeting is “live.”

Elsewhere on the calendar, final CPI numbers are due across Europe. Central banks will be hoping that the relatively contained m/m inflation gains seen in March mark the high point in price transmission.

On the political side, the EU will need to assess the result of Hungary’s parliamentary elections, given the country’s centrality to a host of EU issues – such as the loan to Ukraine (which is again facing credit events), the trans-Atlantic relationship, energy policy, and legislative reach.

APAC: China GDP, regional inflation, exports, and MAS

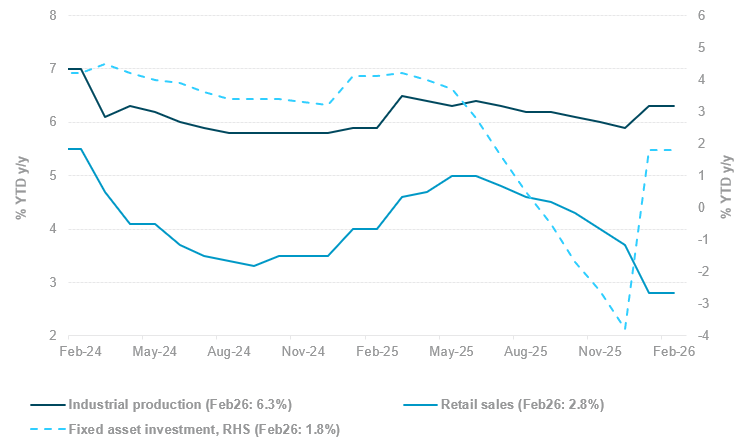

EXHIBIT #4: CHINA ACTIVITY AND INVESTMENT DATA

Source: BNY

Our take: China’s activity and investment data, regional inflation indicators, South Korea’s early-April export print, and the Monetary Authority of Singapore (MAS) policy meeting are in focus for APAC this week.

China’s Q1 GDP, alongside March retail sales, industrial production, and fixed asset investment, will be central to gauging growth momentum and the need for further policy support. Trade data (exports, trade balance) will provide signals on external demand amid global uncertainty, while property metrics (new/used home prices, investment and sales) remain key to assessing downside risks to growth and credit demand. Notably, Tier-1 new home prices rose 0.03% m/m in February – the first increase since April 2025 – pointing to tentative stabilization that could support sentiment and Chinese assets.

Monetary policy and inflation dynamics also warrant close attention. Singapore’s MAS decision, alongside Q1 GDP and export data, will shape near-term SGD direction; consensus expects a modest tightening of the SGD NEER slope on inflation concerns. Regional inflation prints – including India’s CPI/WPI, Malaysia’s CPI, South Korea’s import prices, New Zealand’s food prices, and Australia’s consumer inflation expectations – will be scrutinized for pass-through from the 51% m/m oil price surge.

Within G10, Australia’s labor market data will be key for AUD and the Reserve Bank of Australia’s May outlook, while Japan’s machine orders and department store sales will offer incremental signals on domestic demand.

Overall, the week is skewed toward validating China’s growth recovery and assessing policy calibration across Asia, with FX and rates balancing downside growth risks against rising inflation pressures. So far, business sentiment (PMIs) has been mixed – declining in Singapore, India, the Philippines, Indonesia, and Hong Kong, but improving in China, Thailand, Malaysia, and South Korea. Inflation dynamics are similarly mixed: price pressures remained steady in Indonesia (0.41% m/m vs. 0.68% in February) and South Korea (0.3% m/m, unchanged) but picked up notably in Thailand (0.6% m/m vs. -0.24% in February).

Forward look: Sentiment improved markedly last week following the announcement of the conditional, two-week ceasefire allowing the partial reopening of the Strait of Hormuz. The pullback in commodity prices triggered broad risk-covering across FX, equities, and fixed income. That said, we caution against chasing APAC FX, particularly in net oil-importing economies, as still-elevated crude prices will continue to pressure terms of trade via higher import costs. In contrast, conviction is stronger for a continued rebound in equities.

In fixed income, regional yields should retrace some of the embedded risk and inflation premium if Middle East tensions continue to ease. Encouragingly, iFlow equities holdings over the past month suggest investors remain constructively positioned on the region overall. We will closely monitor regional credit spreads, funding/basis conditions, and FX/equity volatility, alongside policy responses to rising energy costs and the pace of central bank FX intervention. Notably, FX reserve drawdowns have been significant across the region in March, led by India (-$40bn m/m), Thailand (-$16bn), and the Philippines (-$5.8bn), underscoring intensifying intervention pressures. Overall, we are positive on CNY, SGD and MYR and negative on INR, PHP and THB. We also see upside in KRW and TWD, supported by potential reversal of prior equity outflows.

Looking ahead, markets are likely to remain highly sensitive to the durability of the ceasefire and normalization of flows through the Strait of Hormuz, which remains the critical transmission channel into energy, inflation, and global risk pricing. While last week’s relief rally signals rapid repositioning out of extreme volatility, persistent supply constraints and geopolitical uncertainty suggest that cross-asset dispersion will remain elevated. Investors will increasingly focus on forward guidance from U.S. earnings, particularly around Q2 demand and supply-chain resilience, alongside signals from China’s growth trajectory and currency stability. At the policy level, central banks face a complex trade-off between absorbing energy-driven inflation and supporting weakening growth – a tension that reinforces stagflation risks, particularly in emerging markets. In this environment, asset allocation is likely to favor selectivity across regions, with continued emphasis on liquidity, downside hedging, and sensitivity to energy-linked macro dynamics.

Central bank decisions

Singapore, Monetary Authority of Singapore (Tuesday, April 14): While consensus leans toward tightening via a steeper SGD NEER slope – after four consecutive holds since July 2025 – we expect MAS to stay on hold across slope, center and width due to the heightening uncertainties in both growth and inflation. That said, risks are skewed toward tightening later in the year, with MAS likely to respond via slope steepening and potential recentering if oil-driven inflation materializes without meaningfully undermining growth. Focus will be on updated 2026 inflation forecasts (January: 1.0% to 2.0% for both headline and core).

Source: BNY

Source: BNY