Second-round effects

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

Europe and U.K. markets join summertime and move clocks ahead this weekend, but that won’t translate into clarity on the war. We don’t know what the oil price or second-round effects will be. All we know is that waiting has a time limit, and one day the war will end.

First-round effects are expected to push U.S. headline CPI to 4.5%–5.0%. Second-round effects are more complicated. Demand destruction is already visible, with consumers pulling back and companies likely cutting workers. Hits to GDP growth of 0.2% to 0.5% are also expected.

This stagflation risk is playing out globally, and the situation has a non-linear quality, with time a key variable. Last week highlighted some conflict-linked themes that will continue to matter into Q2.

Does the uncertainty of war matter in the long run?

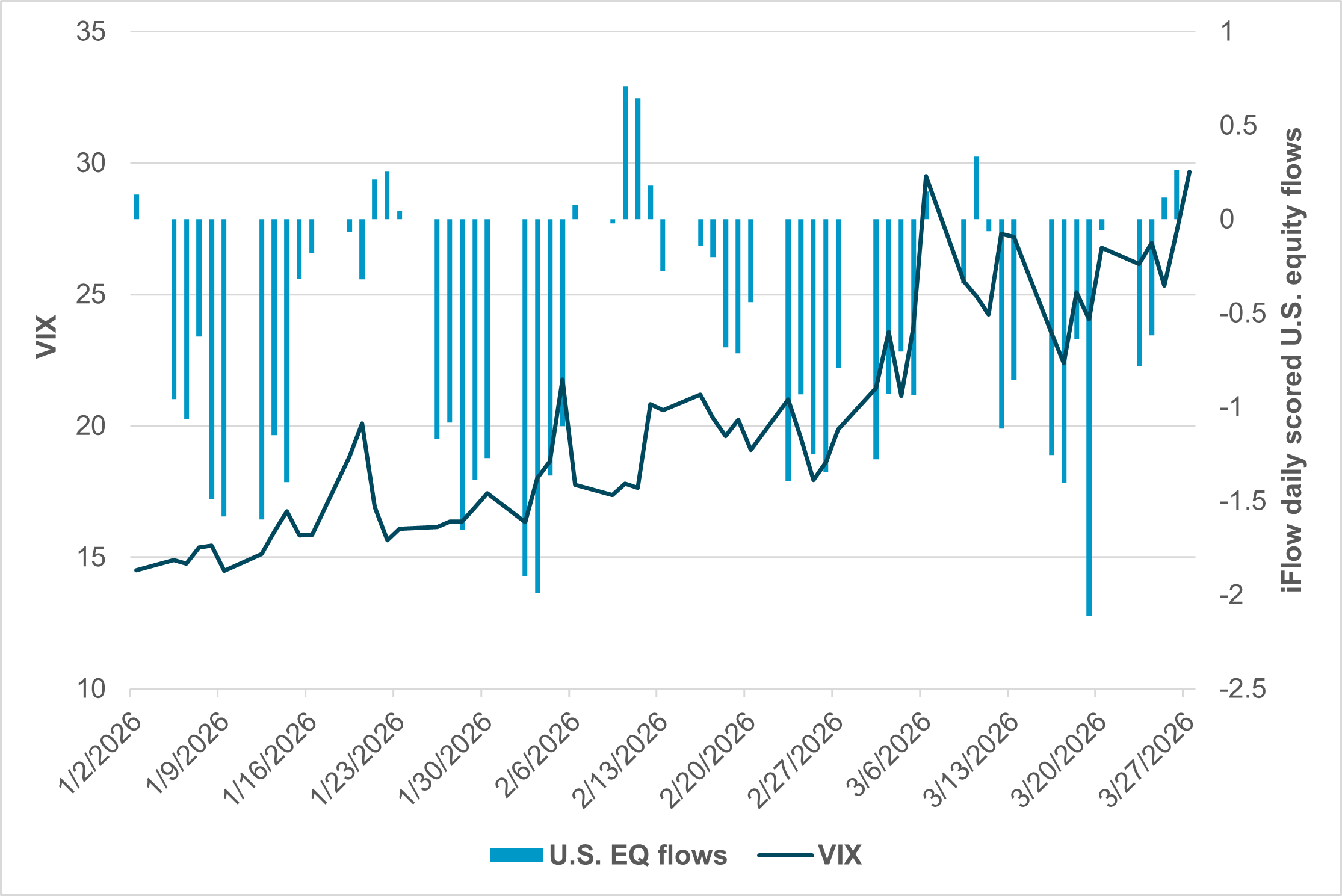

EXHIBIT #1: U.S. VIX VS. IFLOW DAILY U.S. EQUITY FLOWS

Source: BNY, Bloomberg

Our take: The VIX’s steady rise in 2026 reflects growing uncertainty over the direction of stocks. The markets have absorbed ongoing AI and credit worries, the Venezuela surprise and then the war in Iran. The biggest surprise was the VIX smile formation in March: it spiked on March 6, reversed on hopes of a short conflict, bottomed out just before option expiries, then bounced back to end the week near the highs. iFlow data show U.S. equity selling in March has been steady and positively, rather than negatively, correlated to the VIX. This suggests the war has changed the approach to risk. Last week’s dip-buying also showed up in our Mood index, which flipped from extreme negative to neutral.

Forward look: Retail has been a significant force in U.S. equities. Retail buying and selling has accounted for about 40% of market liquidity in 2026, and that’s not changing. Equity inflows were notable last week, and they suggest more of a buy-the-dip mentality. How long the war lasts will be critical to sustaining that. What seems less priced by our flows and the market is a more extreme shock – oil to $150/bbl would be one risk that isn’t in the flows. As we highlighted in our Equity outlook, trading the peace could be more difficult than the surprise of the war.

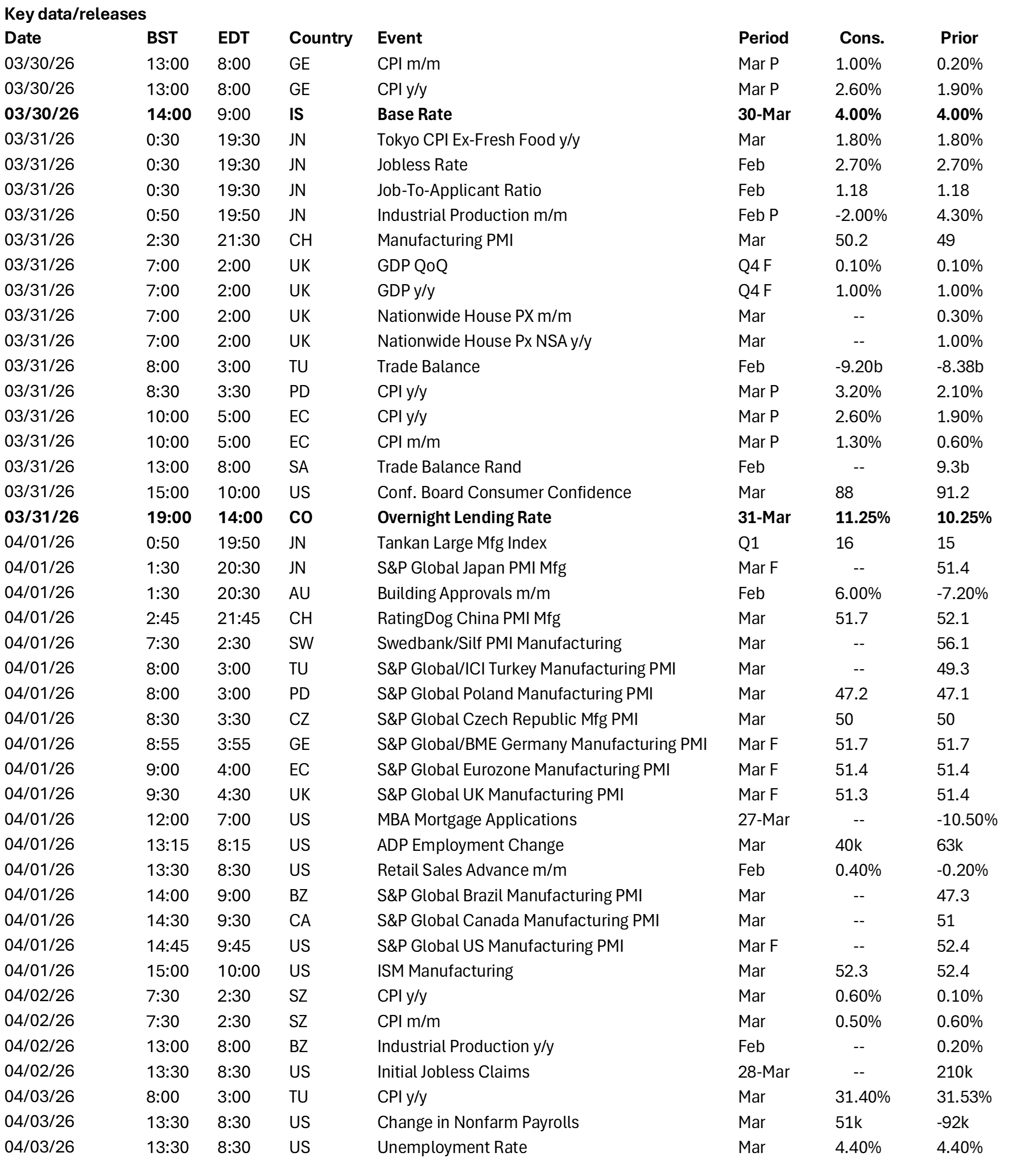

North America: Labor market data amid Iran talks

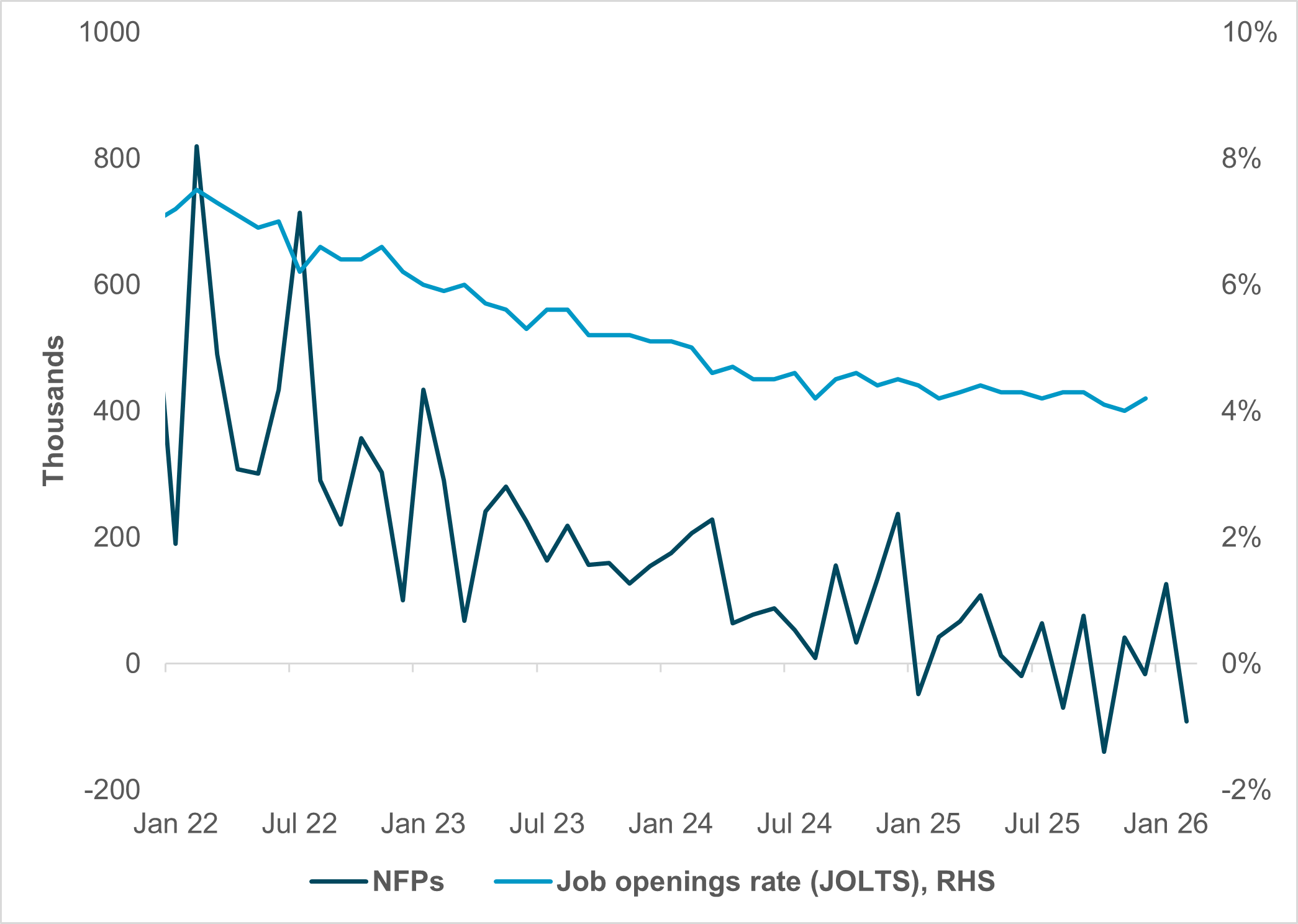

EXHIBIT #2: U.S. JOB OPENINGS AND PAYROLL GROWTH

Source: BNY, Bloomberg

Our take: In the eye of the storm, this week delivers a crucial run of U.S. labor market data. Given the weak February jobs report and a month of conflict in the Middle East, we’re keen to learn how the jobs situation has responded, if at all. Labor market concerns have been top of mind in the U.S. over the past few months, and as Fed Chair Jerome Powell said at the March FOMC press conference, net job creation in the U.S. in 2025 was nearly zero.

With the increase in input costs – as well as general uncertainty and market volatility – thanks to the Middle East conflict, we expect another troubling print. As of this writing, consensus expects just 51k jobs added, but the distribution around that median is quite wide, ranging from 11k to 95k.

Forward look: Before the NFP release on Friday, we’ll get the normal selection of appetizers, including the JOLTS report on labor turnover and job demand on Tuesday, the monthly ADP private payrolls estimate on Wednesday, and Challenger job cuts on Thursday. Good Friday will likely mean thin markets at the end of the week.

In addition to the smorgasbord of labor indicators, we see retail sales on Tuesday as well, although they will be February data, and therefore not conflict-affected. Still, given rising uncertainty around the labor market, we’re watching these data closely. The March ISM manufacturing PMI should prove important, reflecting industry’s mood since hostilities began.

Fed speakers will fill the airwaves next week, with Chair Powell giving remarks on Tuesday as the highlight. Many officials last week seemed focused on inflation risks from the conflict and sanguine about the employment picture. That could all change after this week.

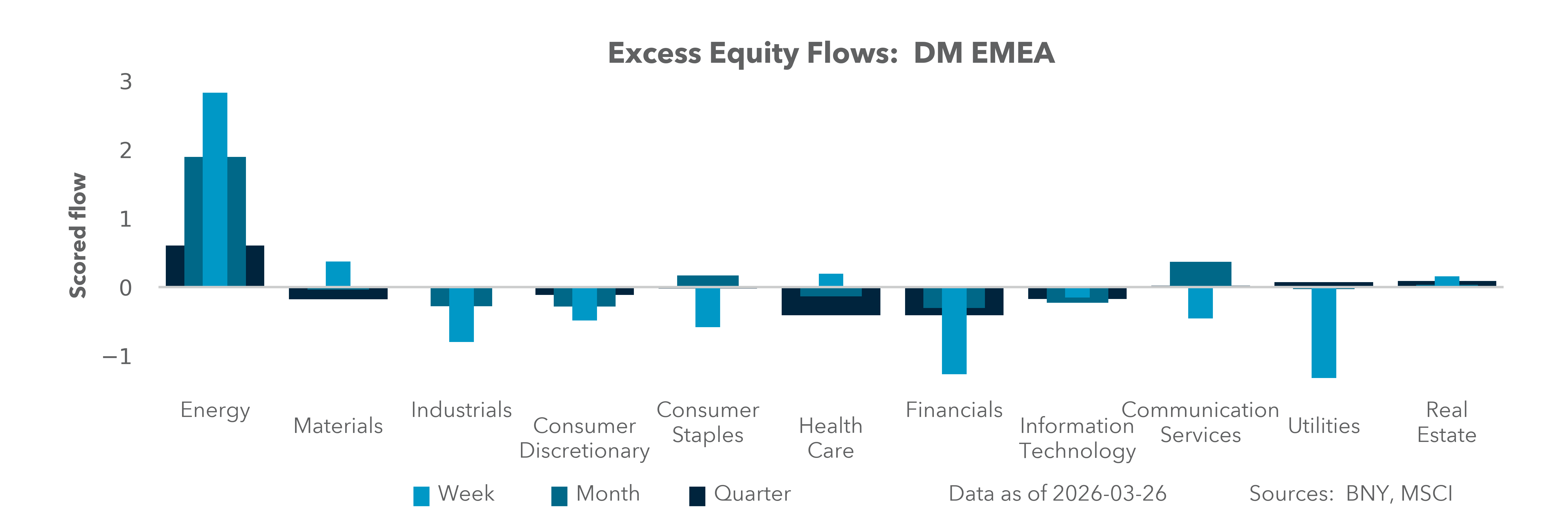

EMEA: Energy pressure builds as ECB splits emerge

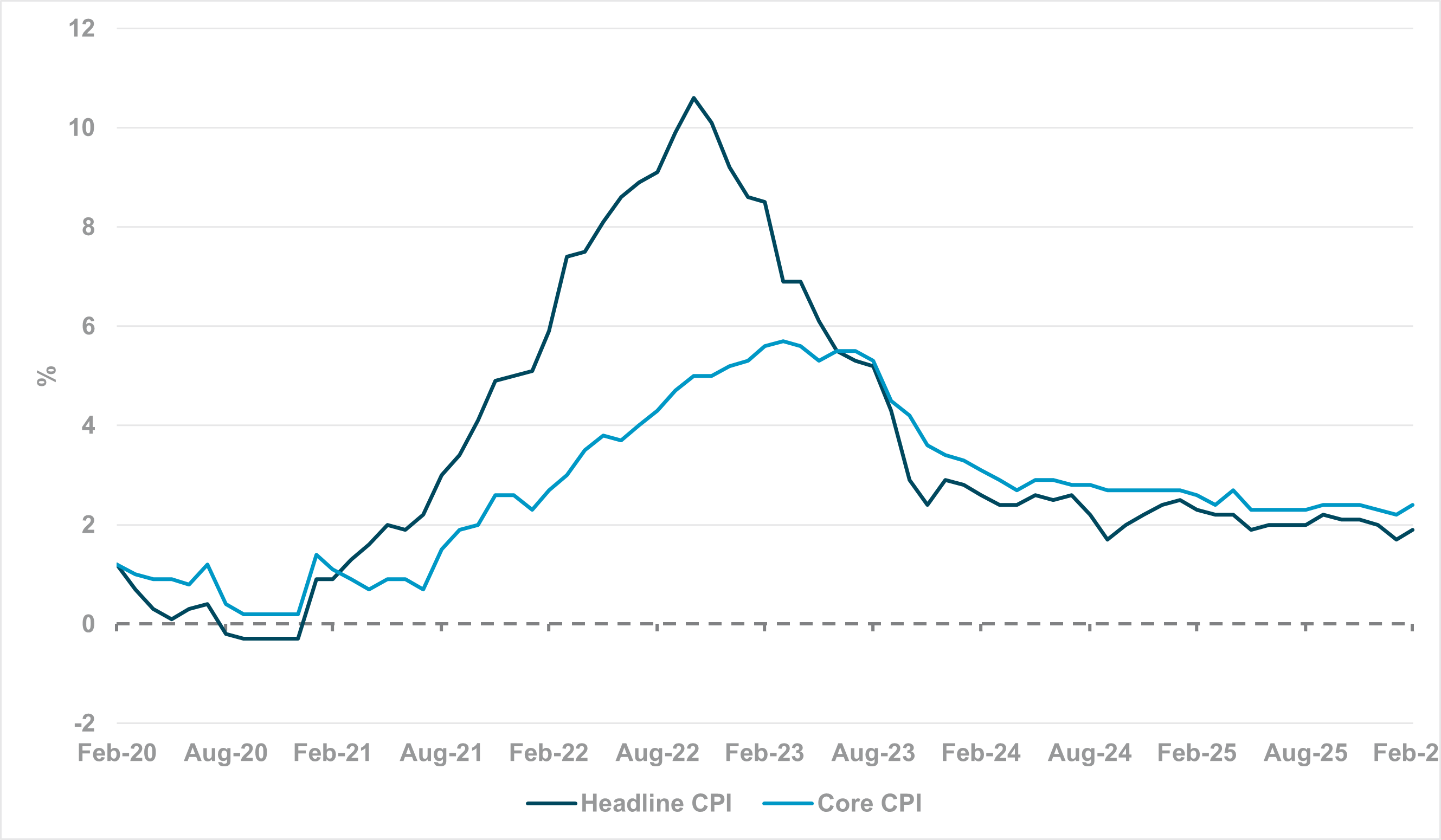

EXHIBIT #3: EUROZONE HEADLINE AND CORE CPI, FEB 2020 TO FEB 2026

Source: BNY

Our take: The International Energy Agency’s special briefing for EU finance ministers will likely trigger additional national-level support for motorists and industry. Shortages are not as acute as in the emerging world, and most scenarios point to resilience. However, there are individual products where supply, rather than price, could become critical. For example, key energy companies have warned that diesel supplies may run out next month, mirroring Australia’s challenges with aviation fuel. Export bans are reportedly being enacted across Asia to prioritize domestic supplies. In a broken market where supplies become non-existent, certain types of activity may simply cease. That is where the growth aspects of stagflation begin to pose a risk.

On the other hand, if households are forced to pull back on demand as well, core inflation may not rise as sharply, which could obviate the need for hikes to restrain economic activity. Consequently, the CPI figures in the week ahead will be essential for an initial read on how inflation dynamics are evolving. Spain’s March print has already hinted at the direction of travel: fuel costs pushed headline inflation up by 1.5% m/m, and the headline figure jumped from 2.5% y/y to 3.3% y/y accordingly. However, the core figure was unchanged at 2.7% y/y, supporting the view that households were cautious.

Core inflation across the Eurozone has been running ahead of headline over the last two years (Exhibit #3). During the 2022–2023 energy shock, headline inflation was the clear leader, but it dragged core prices higher because the cycle was different: global demand was recovering and households had strong wage bargaining power, which may not exist this time around. Consequently, we believe that most central banks will retain caution and look for second-round effects. Many officials expect strong demand-dampening effects as households conserve resources, but much will depend on the state of the cycle.

Furthermore, markets will need to acknowledge that the ECB could struggle for unanimity in the near term: Governing Council member Muller warned that the central bank “may not need fully visible second-round effects” before acting – a bold call, in our view, without sufficient information. Our bias remains that aggressive pricing of front-end hikes in the U.K. and Eurozone will come off, but the process will likely remain volatile.

Forward look: Inflation data aside, we expect wage data to carry significant weight in policy decisions in the near term. Due to inflation stabilization before the conflict, this year’s collective bargaining rounds were not expected to register material increases. While politically there will be calls for increased support, governments and central banks are highly averse to providing permanent subsidies in reaction to short-term shocks. The fiscal burden will be difficult to meet for the region, and such measures would undermine real rates through the core inflation channel, which have hitherto behaved well.

Germany will release unemployment figures for March, though the European Union’s aggregate figures will be from February. The final PMI reports for March are also due: all surveys have pointed to a sharp rise in input cost expectations, with no sign of immediate pass-through to output prices. This will be a key measure of second-round effects, and we expect ECB officials to track any sign of changes in corporate behavior accordingly.

APAC: Regional PMI, Japan Tankan, and South Korea exports in focus

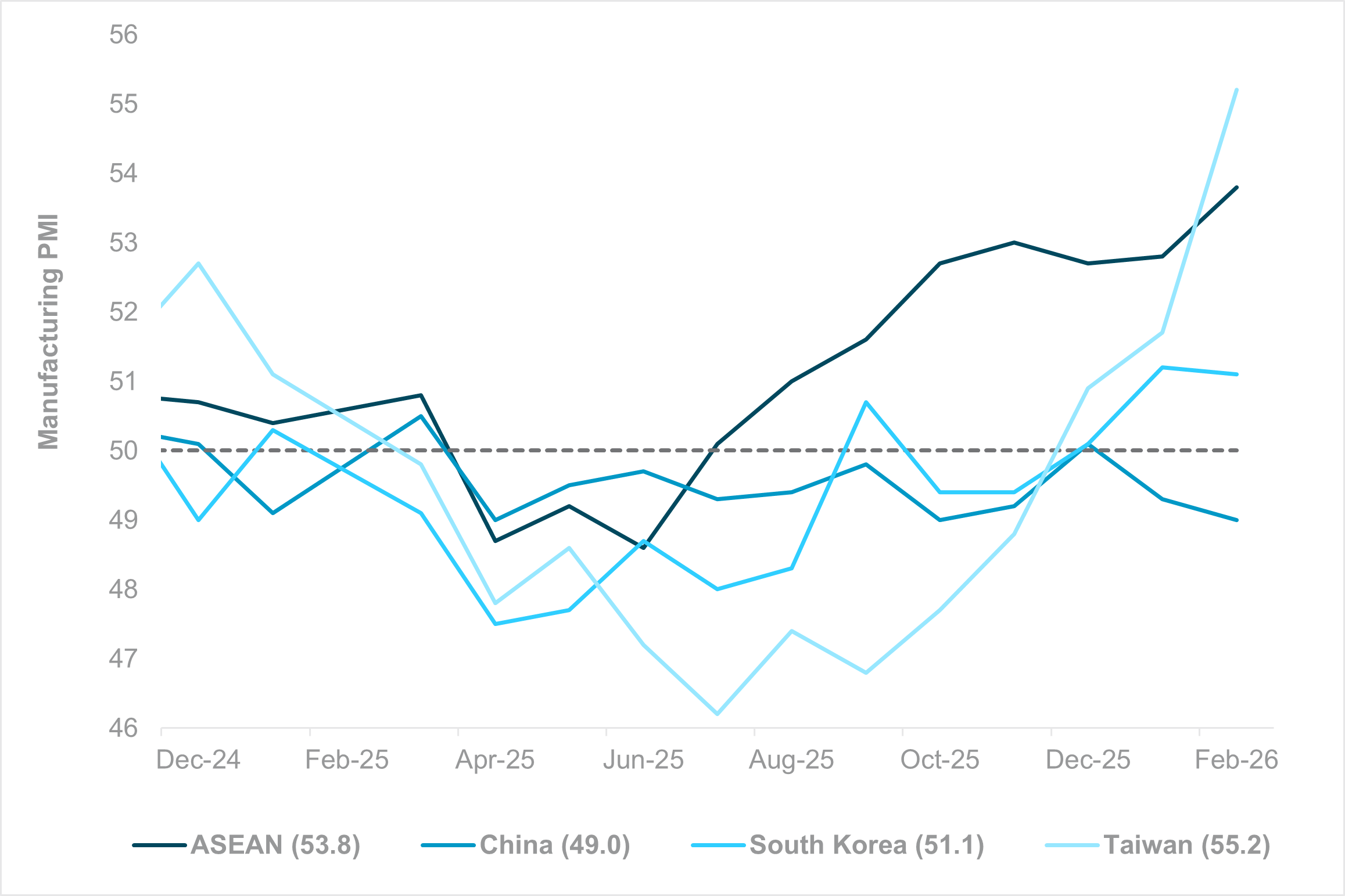

EXHIBIT #4: IMPROVING REGIONAL PMI MOMENTUM INTO IRAN CONFLICT

Source: BNY

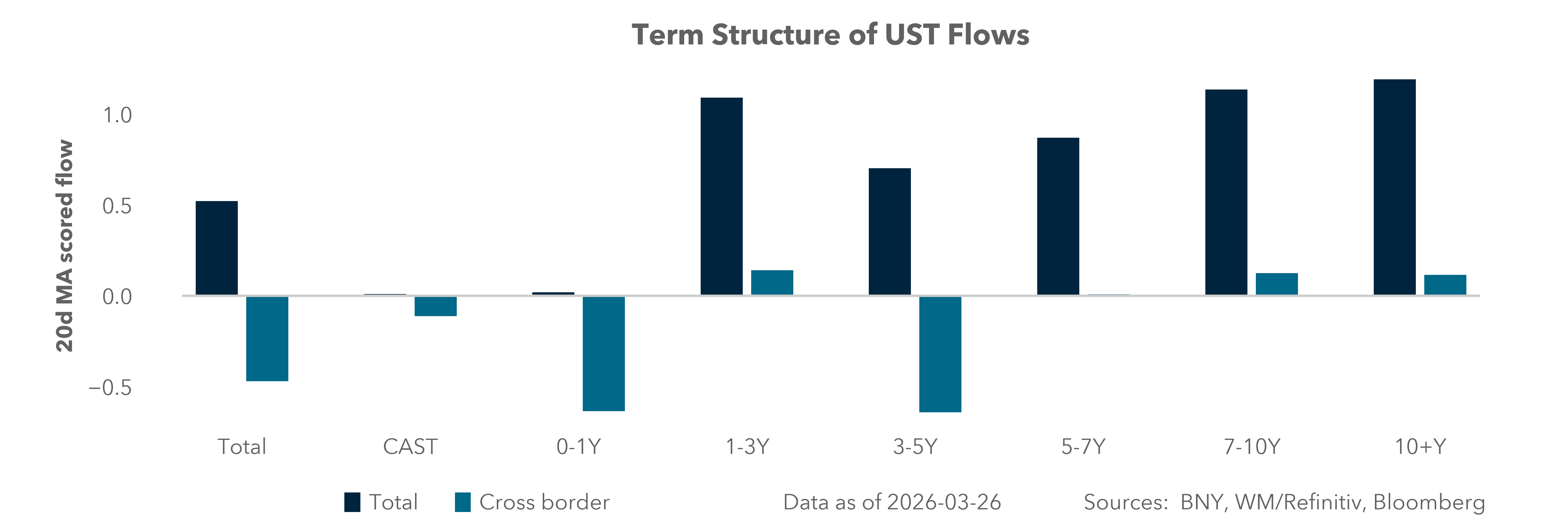

Our take: Next week’s Asia calendar is led by China and regional March PMI, alongside Japan’s Tokyo CPI and Q1 Tankan survey, and the start of South Korea’s inclusion in the FTSE World Government Bond Index (WGBI). Regional PMI will set the tone for risk appetite and serve as a gauge of business sentiment as well as the impact on input prices since the Iran conflict began. In Japan, Tokyo March CPI will be closely watched for potential impact from the surge in oil prices in March, while the Tankan capex reading will provide further evidence of growth momentum ahead of the BoJ meeting in late April. South Korea’s March exports, CPI and industrial production are likely to affirm continued growth momentum. The inclusion of South Korean government bonds into WGBI will run from April 2026 through November 2026, with an eventual weight of 2.05% of the index.

Across the rest of the region, focus will be on Indonesia’s CPI, Thailand’s exports, and Singapore’s electronics PMI as a proxy for the tech cycle. In the Antipodes, Australia’s credit, exports and trade and New Zealand’s labor market and housing indicators releases will drive near-term interest rate expectations.

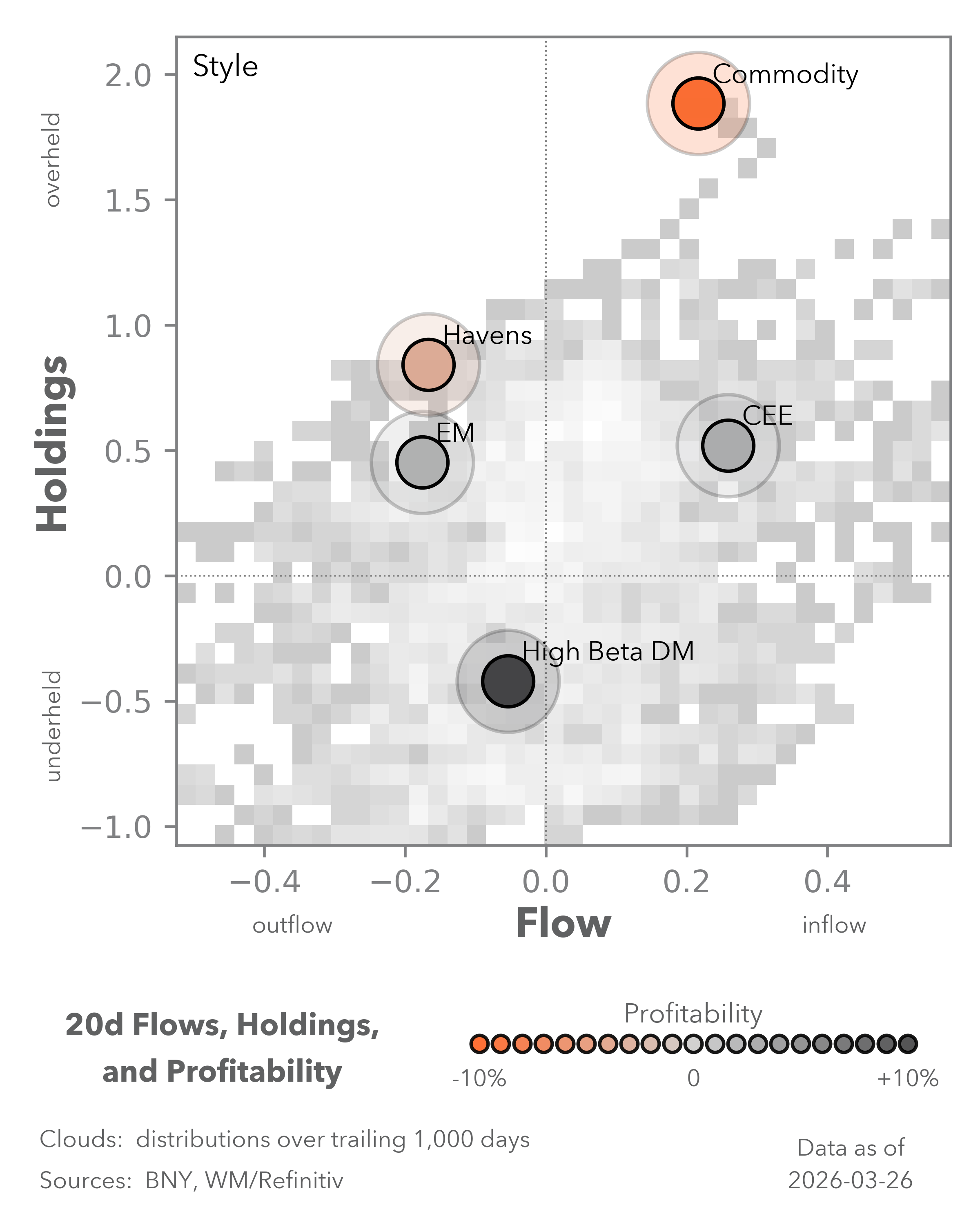

Forward look: The prospect of Middle East de-escalation has failed to lift sentiment. Investors remain focused on risk reduction and capital preservation, with persistent outflows. Foreign investors sold nearly $20bn of South Korean equities (more than $30bn YTD) and around $11bn of Taiwan equities in March. Oil has eased from highs but remains elevated, likely feeding into import prices and weighing on trade balances. Rising input cost pressures were highlighted in recent global PMI releases. Regional central banks are increasingly relying on macroprudential tools rather than monetary policy. This was reinforced by the Philippines’ off-cycle BSP meeting, which instead of delivering an emergency rate hike flagged that monetary policy has limited effectiveness in controlling supply-driven inflation. Regional governments have rolled out cost-of-living measures, including fuel subsidies, tax and tariff cuts, energy conservation, reserve releases, and price caps. Overall, risks remain skewed to the downside, weighed down by geopolitical uncertainty and the energy shock. Policy support may cushion equities but is likely negative for FX and fixed income.

Into Q2, markets will remain governed by the non-linear interplay of energy shocks, policy recalibration, and labor dynamics. Expect continued curve instability as central banks balance inflation spikes against weakening demand; Japan’s Tankan, U.S. ISM/PMIs, and Eurozone wage and CPI data will be pivotal for rate-path expectations. Equity leadership may be episodic: AI-driven productivity tailwinds persist, but job-market prints and data center supply constraints will challenge tech multiples. Retail flows, now a structural liquidity force, can amplify buy-the-dip behavior – yet an unpriced tail, such as oil at $150/bbl, would test that resilience. With VIX elevated, investors will likely favor barbelled positioning: quality balance sheets and cash-flow durability on one side, tactical exposure to energy and selective cyclicals on the other. Hedging should diversify beyond gold, bitcoin, and duration, given recent correlation instability. The path forward hinges on the war’s duration and second-round effects – risk management and data dependence remain the clearest edge.

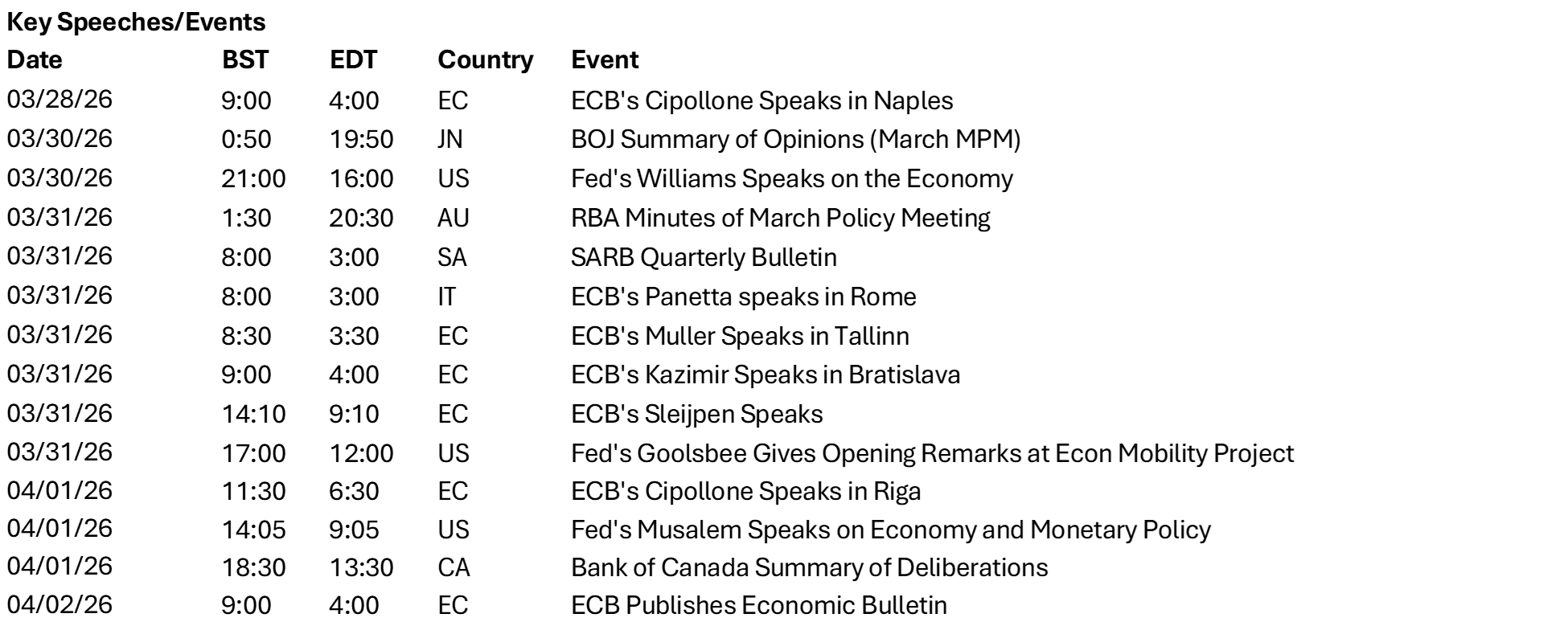

Central bank decisions

Israel, Bank of Israel (Monday, March 30): In hindsight, the prior BoI decision to unexpectedly keep rates unchanged in “view of a potential confrontation with Iran” proved prescient. The fiscal implications are clear, and the BoI is essentially returning to the extraordinary conditions that have prevailed for much of the last few years. This should ensure minimal disruption in the transition from loosening toward vigilance, a task eased by the rest of the world moving in a similar direction. For now, the ILS itself has seen limited impact, but a real rate buffer remains necessary. At 4% base rates, 200bp is sufficient but monthly prints will likely come in on the high side near term.

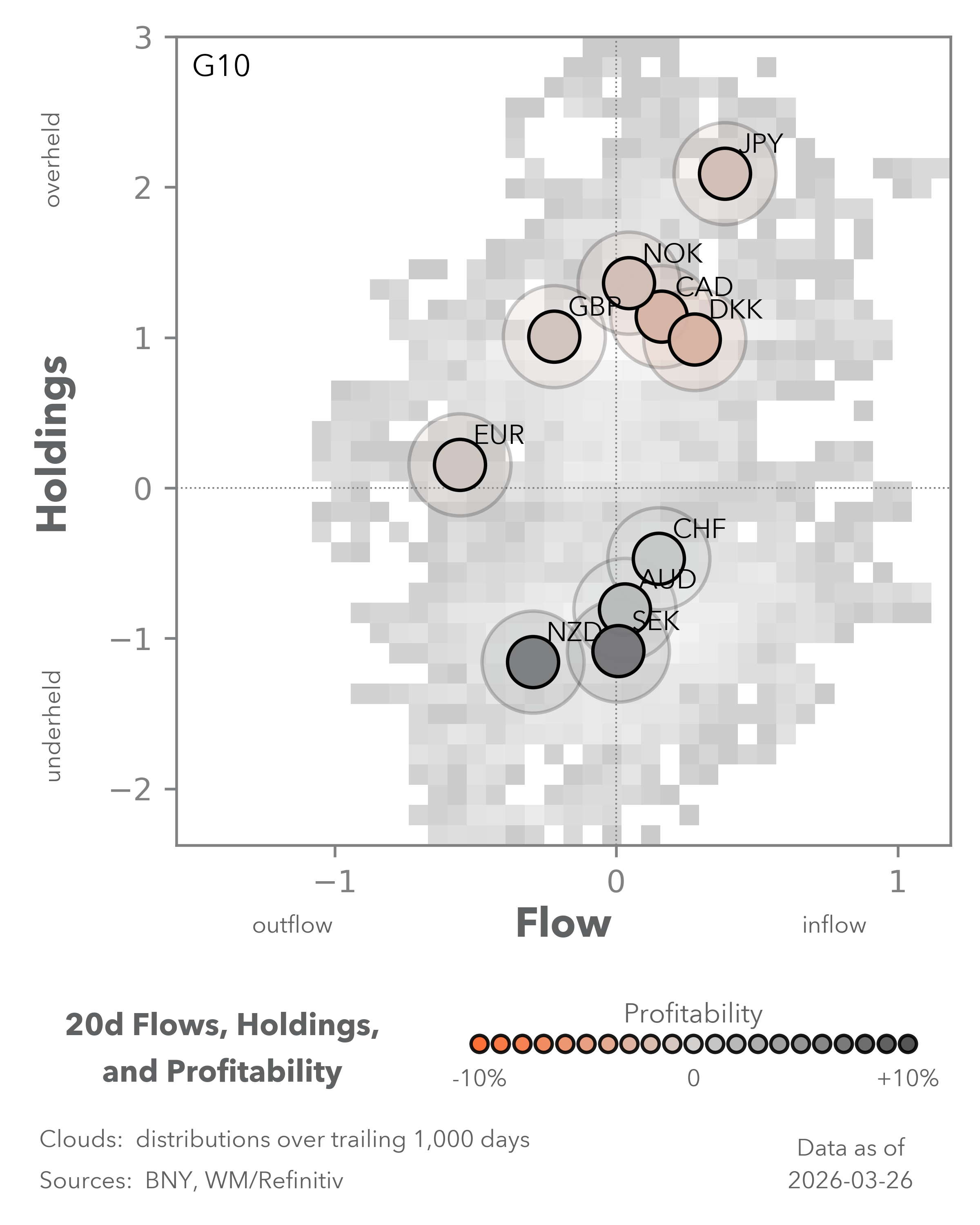

Colombia, Banco de la República (Tuesday, March 31): The BanRep had already shifted back to become the most hawkish LatAm central bank, and the upcoming decision will likely reinforce this view, with the market expecting a 100bp hike to 11.25%. Headline inflation is currently running well above 1% m/m, and this will start to drive up annualized rates. Global events have only added to the urgency of a more aggressive response. That said, COP remains one of the best-held currencies in iFlow, and LatAm FX is still seen as relatively insulated – though we would be cautious about adding aggressively to underlying holdings.

Source: BNY

Source: BNY