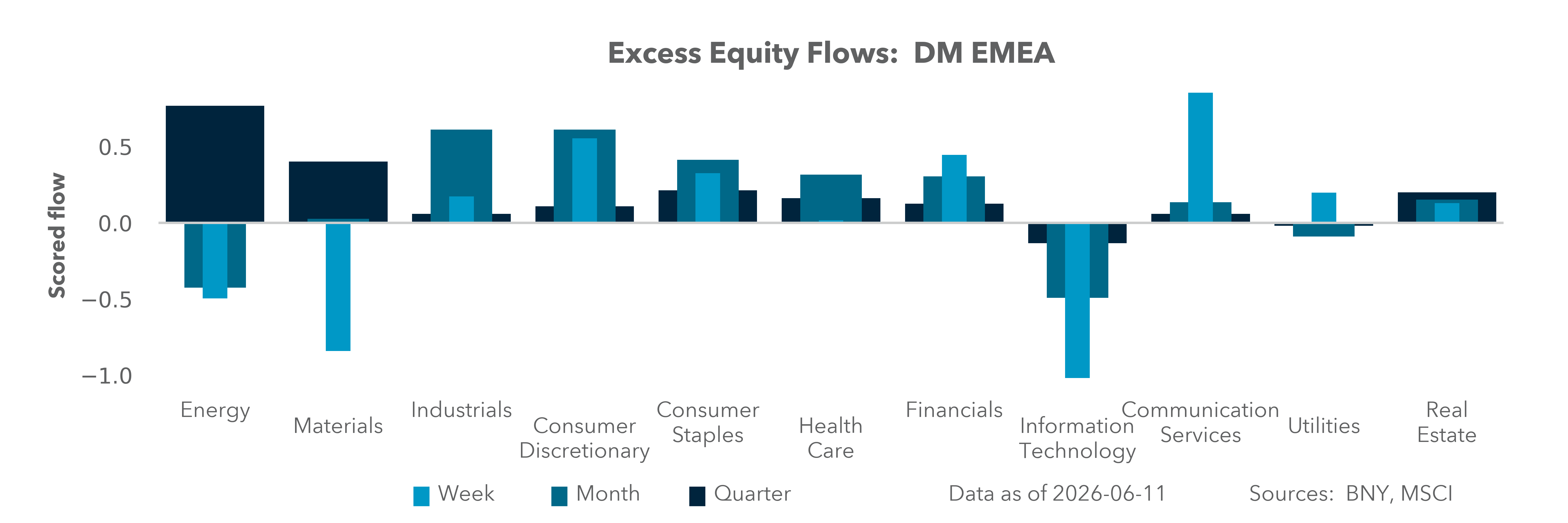

Politics, policy and peace hopes

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 8 minutes

Last week delivered the largest IPO in history with SpaceX, renewed hopes for a U.S.–Iran peace deal with oil lower again, and a rate hike from the ECB. Markets have been able to see through inflation and concentrate on putting cash to work into quarter end. But questions about growth and inflation persist. Markets may be pricing in more recovery and inflation than the data support. Consensus is forming around a U.S.–Iran agreement that stops short of genuine normalization, alongside ongoing energy constraints and supply-chain concerns. There are also new worries about AI price wars and more rate hike and political risks – the U.K.’s June 18 by-election will likely add to pressure on Prime Minister Keir Starmer. Together, these risks are worth monitoring as markets weigh momentum against value.

In focus this week:

What else could matter in the week ahead?

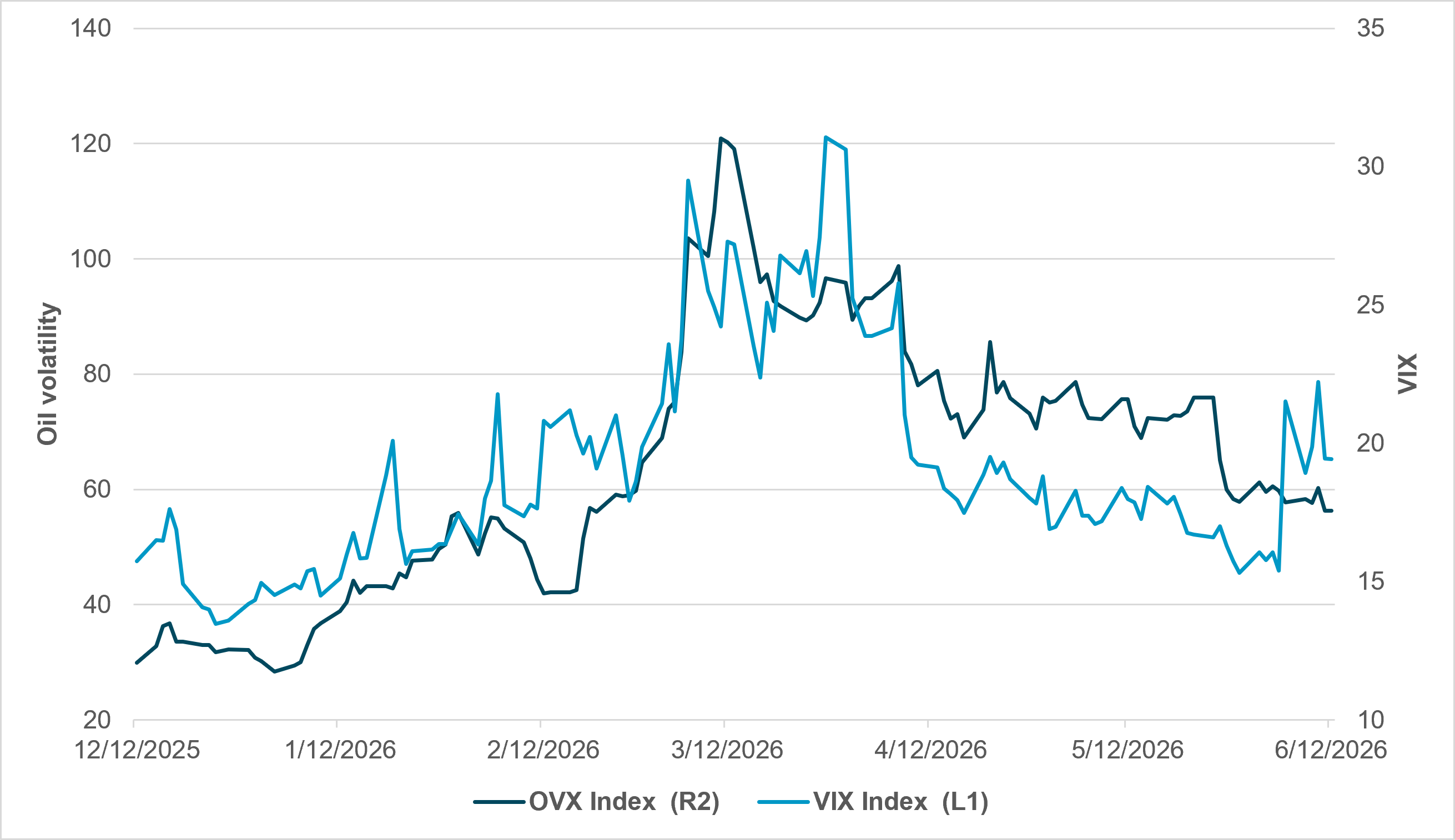

EXHIBIT #1: EQUITY VS. OIL IMPLIED VOLATILITY

Source: BNY, Bloomberg

Our take: The war with Iran was the notable trigger for oil volatility to dominate markets until the last two weeks. Peace hopes have pushed oil aside as a market driver, leaving equities to return to other factors – rates and margins – as counterweights to momentum. Despite the return to an equity uptrend, the jump in the VIX is worth watching. Rising FX and equity volatility, even as trends hold, suggests investors are shifting their focus from oil to more traditional concerns.

Forward look: The risks into this week are that the equity markets shift from growth to value on back of rate policy shifts. The SpaceX IPO tailwind will no longer support U.S. markets, and focus will shift to rotation and rebalancing risks into the Thursday option expiry. Value vs. growth factors will be critical. The June 19 U.S. holiday will also make for compressed trading and liquidity risks. Resetting the view on AI profitability will be one theme to watch should it continue to worry, given the next mega IPO: Anthropic.

North America: FOMC and the Warsh debut

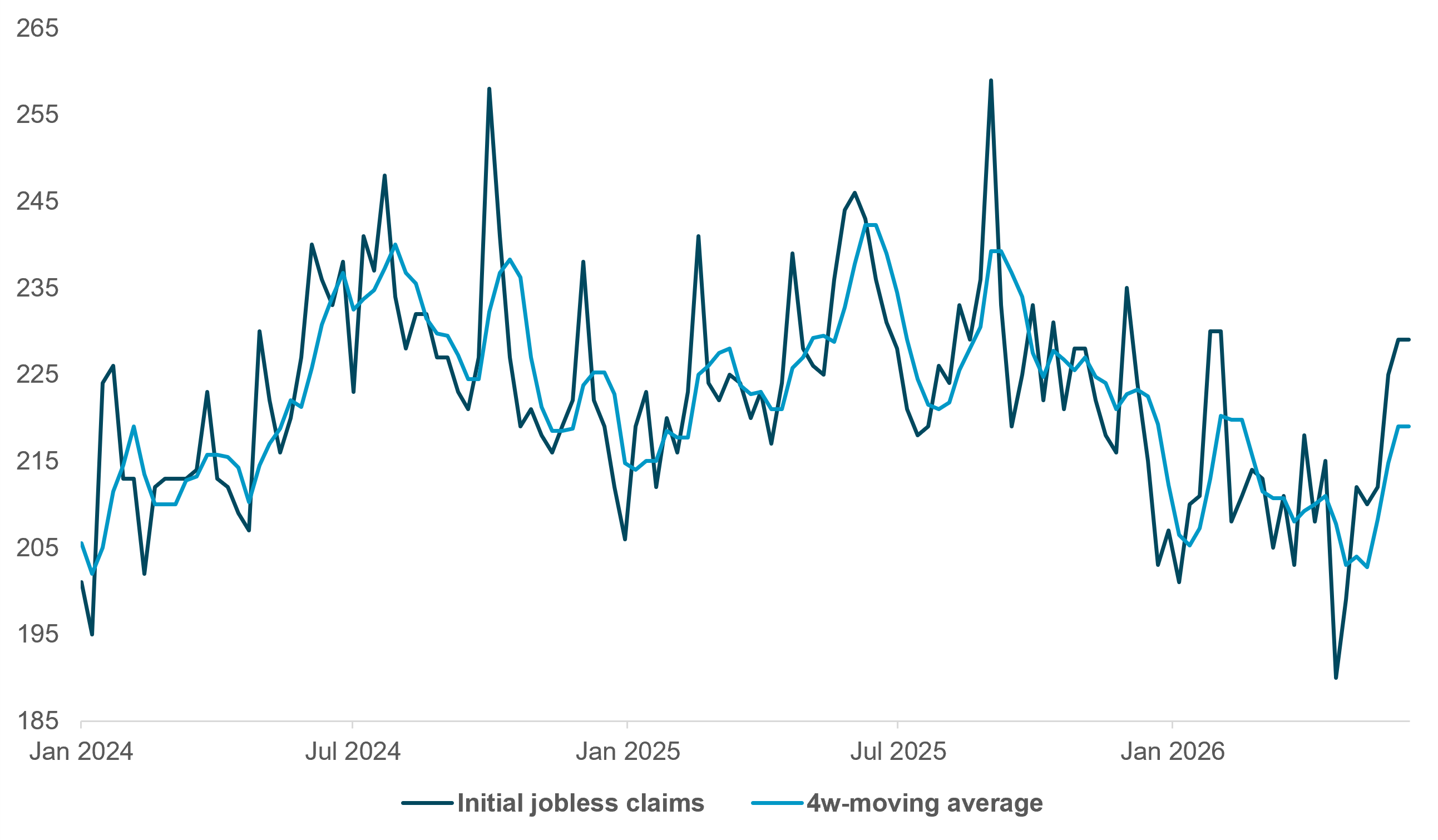

EXHIBIT #2: U.S. WEEKLY JOBLESS CLAIMS

Source: BNY, Bloomberg

Our take: Last week’s U.S. inflation data kept the market focused on the risk that price pressures will force the Federal Reserve’s hand to hike. CPI printed roughly in line with expectations but remained at an elevated level, while PPI came in hotter than anticipated, reinforcing the move higher in front-end rates. The Bank of Canada held rates steady, as expected, with Governor Tiff Macklem warning that economic weakness along with rising inflation was a policy “dilemma” for the bank.

This week, Chair Kevin Warsh’s first FOMC meeting is the clear focal point. The Committee is expected to leave rates unchanged, so the policy statement, press conference, and any nuance around the dots will matter more than the decision itself. Investors will be especially attentive to any early signals on Warsh’s communication style, and he will undoubtedly be asked about his ambitions on bank supervision, balance sheet policy, and forward guidance.

Data will be light, but weekly initial jobless claims will be in focus – they have run above the four-week moving average for over a month.

Forward look: The most important question is whether Warsh will use his first meeting to reset the Fed’s reaction function or simply preserve continuity. With inflation proving stubborn, markets will be looking for any indication that the Committee is more comfortable maintaining a restrictive stance for longer, which would support higher-for-longer pricing in front-end rates.

Any comments on balance sheet policy will also matter for term premium and long-end Treasury performance, particularly if the Fed sounds less inclined to accelerate runoff adjustments. Likewise, even subtle shifts in forward guidance could influence rate-cut expectations and volatility across equities, FX and credit. If Warsh adopts a less accommodative tone, it would likely reinforce a modestly hawkish market repricing. Without a fresh policy surprise, however, markets may treat the meeting as a communication test rather than a turning point.

EMEA: ECB stands alone as peers hold

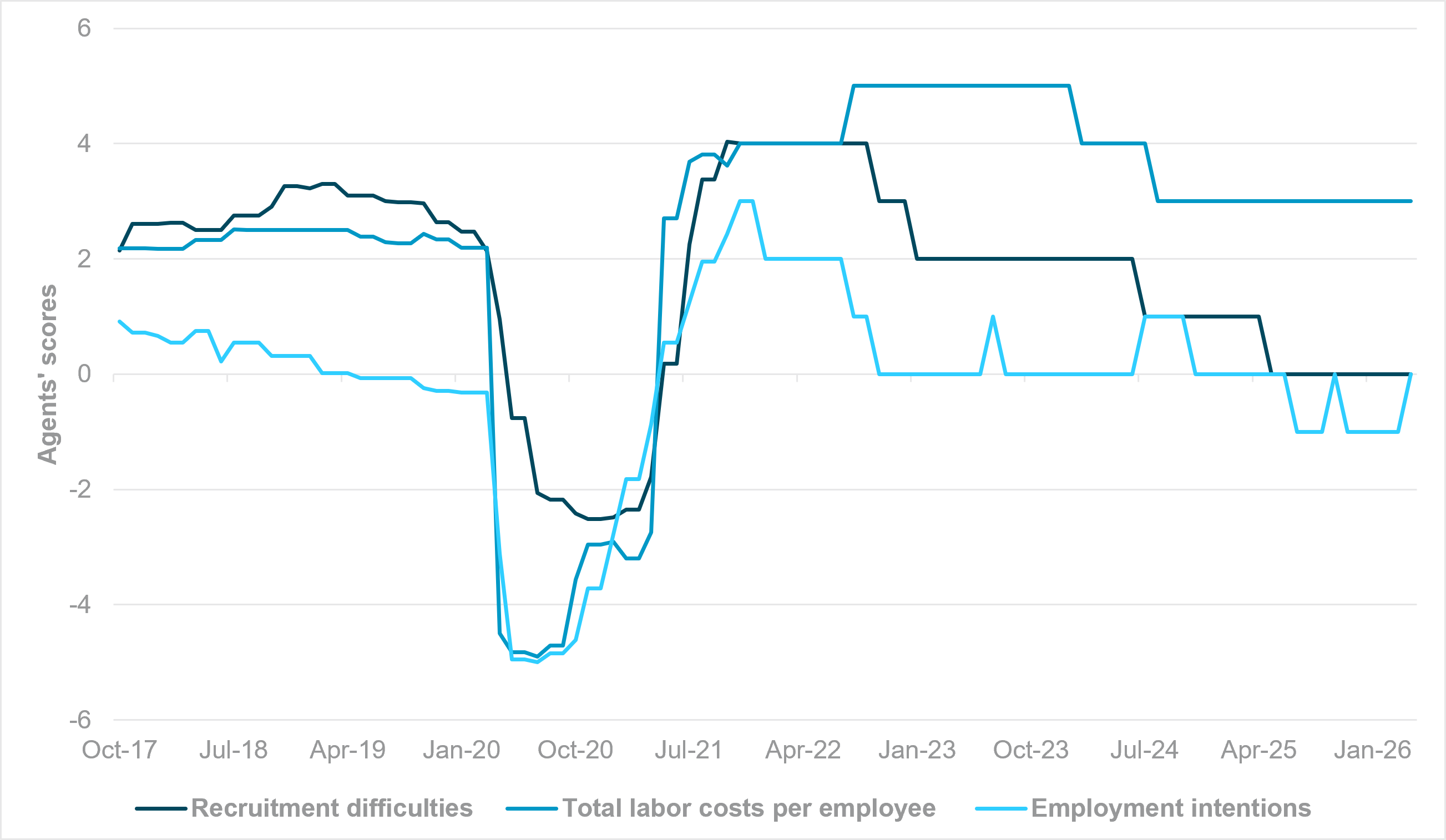

EXHIBIT #3: BOE REGIONAL AGENTS’ SURVEY – LABOR MARKET ASSESSMENT

Source: BNY

Our take: Several central banks will hold their policy decisions this week, but we don’t see any in a position to follow the ECB. President Christine Lagarde was clear that inflation was the only ECB mandate, and growth will happen with structural reform and implementation of other aspects of the Draghi Report. We expect the ECB’s peers to hold a more flexible view.

Even on core inflation alone, Lagarde acknowledged that wage growth would ease this year and that demand was softening – though not enough to require larger downward growth revisions, which might have delayed the hike.

The burden of proof is the opposite for peers such as Norges Bank and the BOE, where strong evidence of accelerating wage growth in response to the Middle East conflict would only trigger tightening. BOE Governor Andrew Bailey remains forthright that the labor market is loosening, and the most recent BOE regional agents’ survey supports this view. Employment intentions and recruitment difficulties remain unchanged, while expectations for total labor costs held steady (Exhibit 3). In Norway, wage growth has been revised higher – in part due to legacy strength in demand, which drove the prior Norges Bank hike – but expected total employment growth remains flat, while capacity utilization and labor supply constraints have continued to fall, negating the need for a follow-up hike for Western Europe’s most hawkish central bank.

The Riksbank, Swiss National Bank and Czech National Bank are all expected to remain on hold, and their strong balance of payments positions should allow sufficient room for passthrough to contain upside inflation risk.

Forward look: President Trump returns to Europe on Monday to attend the G7 summit in Paris, where EU leaders hope to bridge multiple divides, particularly on trade, as the U.S.–EU trade deal inches toward full approval. We also expect U.S. officials to press allies on the need to maintain a strong defensive posture fiscally – a commitment that has faced questions as governments seek support to absorb the energy supply shock. iFlow indicates that clients are increasingly wary of defense exposures in developed Europe – underscored by the recent collapse of a joint Franco-German fighter jet program – not just in terms of funding by implementation. In the U.K., the defense secretary’s recent resignation in protest over the government’s inability to provide more funding has only added to the country’s political instability. Thursday’s by-election in the Manchester constituency of Makerfield will be the main political event. Andy Burnham is widely seen as the front-runner for the Labour leadership, though the outcome is far from certain.

APAC: China activity data, regional indicators, and central bank decisions

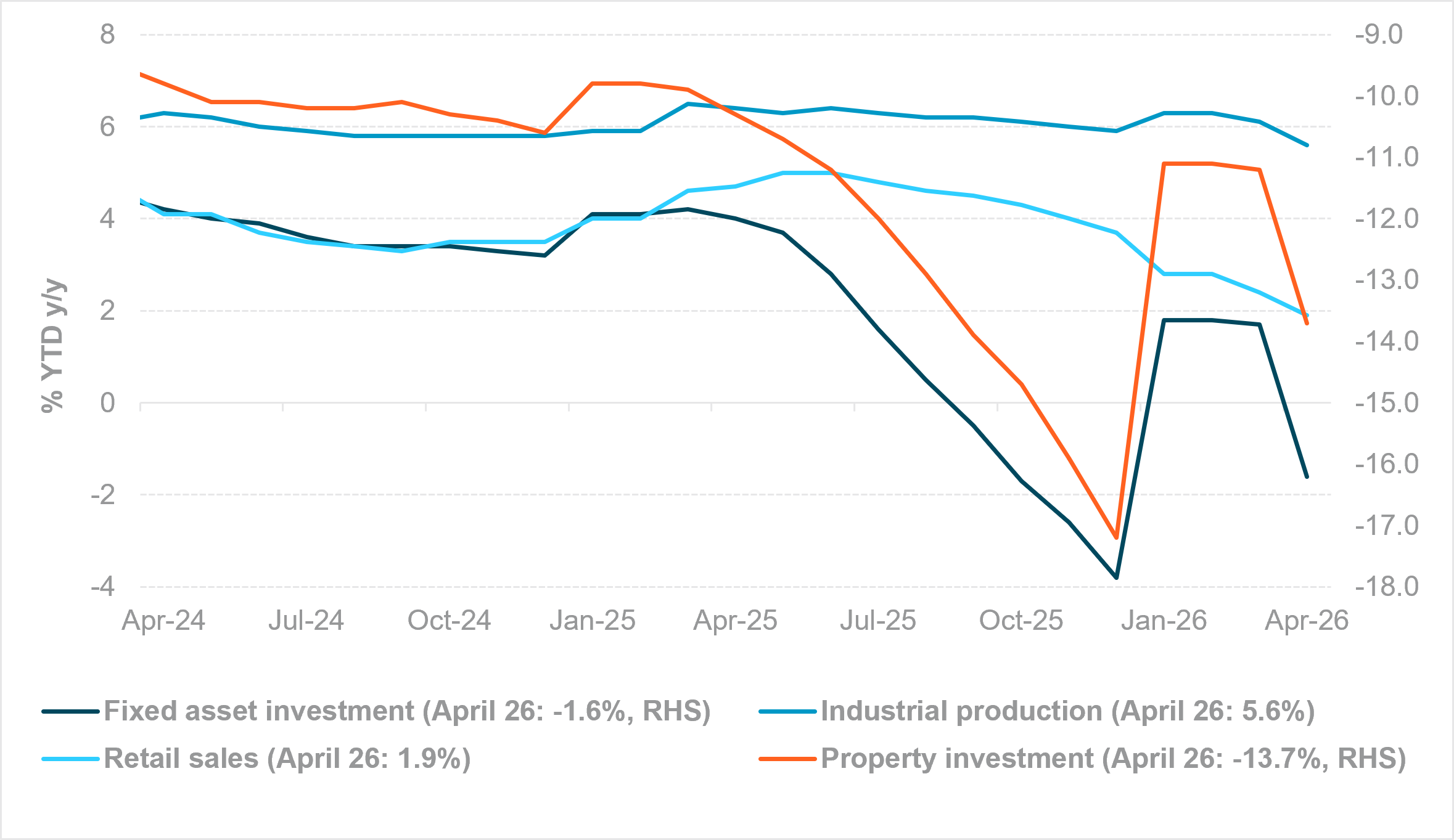

EXHIBIT #4: CHINA’S WEAKENING INVESTMENT TREND – ACTIVITY AND SPENDING

Source: BNY, Bloomberg

Our take: Regional central banks and China’s activity data dominate the APAC calendar this week. China’s May retail sales, industrial production, fixed-asset investment, unemployment, and property indicators will provide the latest assessment of domestic demand and housing-market conditions. Markets will be looking for signs of stabilization in activity and investment, as well as a sustained recovery in real estate – Tier-1 existing home prices rose for a second consecutive month in March and April.

In Japan, May CPI, exports, and trade data will take a back seat to the BOJ meeting, where a rate hike is widely expected. New Zealand’s Q1 GDP will offer the clearest gauge of the economy’s recovery. Elsewhere, Malaysia’s trade and CPI data, Singapore’s electronics exports, India’s trade and wholesale inflation, and South Korea’s import/export prices and PPI will provide insights into regional demand and inflation pressures. Monetary policy will remain in focus, with rate decisions due from the Reserve Bank of Australia, Bank Indonesia, Bangko Sentral ng Pilipinas, and Taiwan’s Central Bank.

Forward look: Sentiment across Asia remains fragile, driven by persistent and sizable capital outflows and broad-based declines across FX, equity and fixed-income markets. While aggressive smoothing and newly announced market reform measures have helped contain volatility, they have yet to restore confidence.

The South Korean won rallied sharply last week after authorities issued strong warnings against excessive market volatility and regulators inspected major FX banks for the first time since 2012. Nevertheless, KRW remains weaker on the month.

In India, the rupee failed to gain meaningful traction despite measures to attract foreign inflows, including the government securities expansion under the Fully Accessible Route, the removal of capital gains tax, and the elimination of the 20% withholding tax on interest income.

Bank Indonesia’s surprise 25bp off-cycle rate hike helped to stabilize IDR, but the sharp selloff in government bonds has become an additional source of concern. The 10y government bond yield rose more than 50bp last week, approaching the 7.50% level.

Attention now turns to this week’s FOMC meeting, which will be critical in shaping U.S. rate expectations, the direction of the USD and broader capital-flow dynamics. Markets will also monitor crude oil prices closely, with a potential U.S.–Iran peace agreement raising the prospect of lower geopolitical risk and a normalization in energy markets.

Financial markets are entering a critical period where policy decisions, economic data, and geopolitical developments will increasingly determine asset performance. While investor sentiment remains constructive, supported by strong liquidity and momentum, the tension between growth expectations and inflation risks is real. The Fed’s communication under new leadership, alongside BOJ’s policy path, could materially influence global rates, currencies and capital flows. At the same time, China’s growth trajectory will be closely scrutinized for evidence of stabilization or further weakness, with significant implications for commodities, emerging markets and cyclical sectors.

Political developments across Europe, energy security, and Middle East tensions compound the uncertainty. As quarter end approaches, investors may shift focus from momentum-driven gains toward valuation discipline and portfolio rebalancing. In this environment, flexibility, risk management, and careful monitoring of policy signals will be essential to navigating increasingly complex global markets.

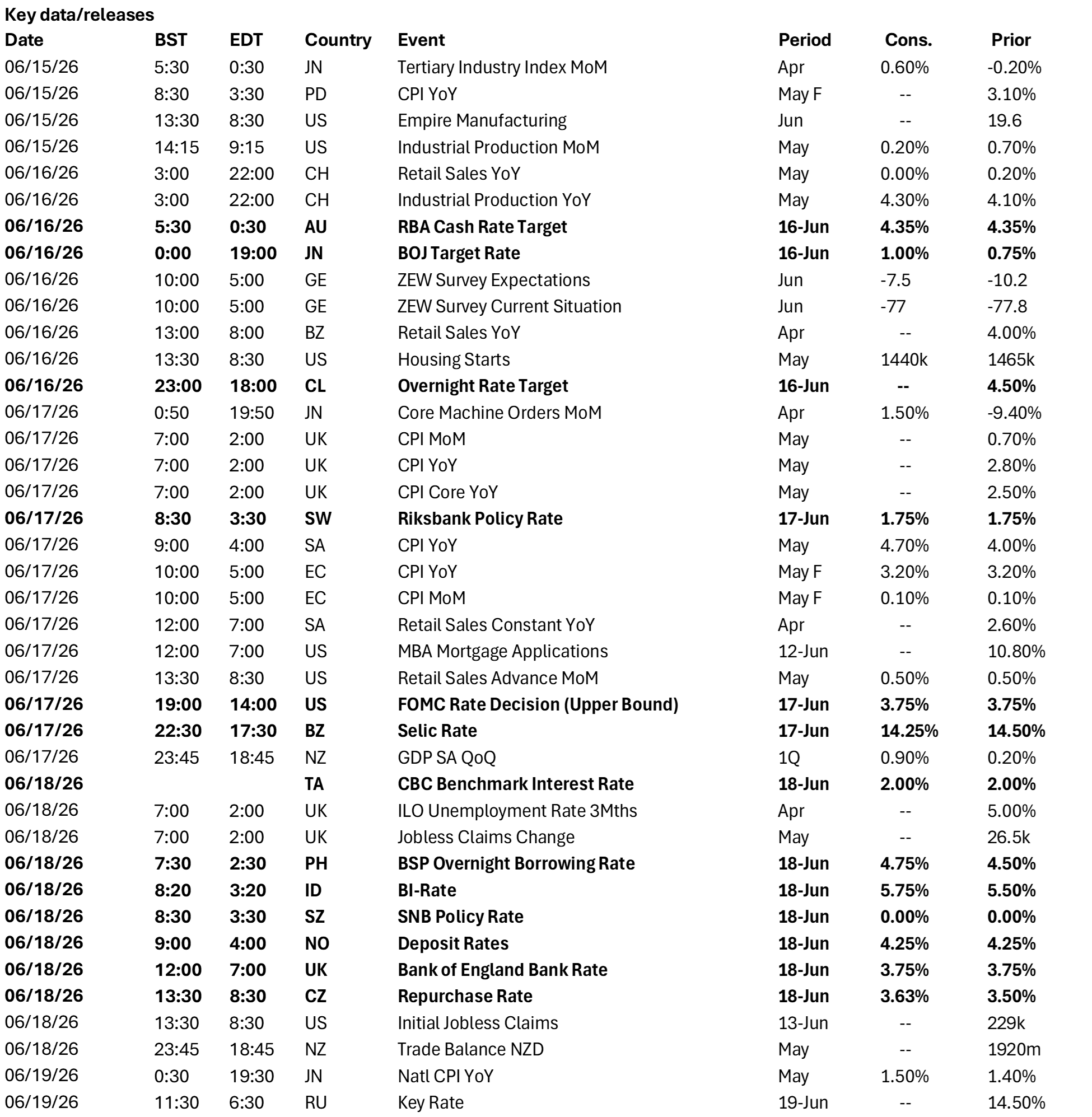

Central bank decisions

Australia, Reserve Bank of Australia (Tuesday, June 16): The RBA is expected to stay on hold for the June decision, but markets continue to anticipate a hike by year-end, which would consolidate the AUD’s status as the highest-yielding currency in G10 markets. Current levels of inflation are explicitly cited as too high by RBA officials, who hope to consolidate signs of slowing domestic demand, while expecting terms-of-trade improvements to soften tradables inflation.

Japan, Bank of Japan (Tuesday, June 16): The BOJ is expected to hike rates by 25bp to 1% - levels last seen over 30 years ago – but the market is far from convinced that financial conditions are tight enough to stem the ongoing losses in USDJPY. Despite repeated warnings and realized intervention, the breach of 160 in USDJPY has been achieved comfortably and further losses are possible if the BOJ’s policy path is not seen as keeping pace with any Fed tightening. The BOJ will commit loosely to further tightening but not at an optimal pace from an FX perspective.

Chile, Banco Centrale de Chile (Tuesday, June 16): The BCC is unlikely to pre-empt the Fed on Wednesday, but the risk of a hawkish FOMC outcome may justify greater vigilance. The April decision certainly did not rule out hikes up ahead if the inflation environment deteriorates beyond current survey-indicated expectations, and there is no guarantee that terms of trade, though broadly favorable for Chile at present, are improving sufficiently to cap inflation in the near term. The real rate buffer is being steadily eroded, and the next move will be a hike, subject to incoming data, which for now remains manageable.

Sweden, Sveriges Riksbank (Wednesday, June 17): Out of all western European central banks, the Riksbank is least likely to move at all given repeated downside surprised to inflation, despite the current risks from the global supply shock. However, May figures indicate some pick-up in sequential headline and core inflation, which means that some degree of vigilance is still necessary, especially if domestic demand remains in a strong spot despite external volatility.

U.S., Federal Reserve (Wednesday, June 17): Robust inflation numbers do not change our view on no hike from the Fed this week, nor for the rest of the year if this month or next produces peak inflation readings. Nevertheless, the dissenters from last meeting seem to have been joined by other members of the Committee in their intermeeting communications. Expect the statement to warn that rates could go either up or down going forward, or maybe even dropping the dovish implication all together. It will be Kevin Warsh’s first press conference as Fed Chair, so the interest will be as much on what he says in the press conference and his style as it is about rate decisions.

Brazil, Banco Central do Brasil (Wednesday, June 17): The current level of real rates means that COPOM can comfortably sustain an easing bias over the coming meeting cycles, but markets should not count on aggressive moves given the direction of travel for inflation elsewhere. Transmission from a more hawkish, less dovish Fed to LatAm financial conditions is swift, and if the market is exploring Fed hikes again, it would severely reduce the capacity for the BCB and peers to embark on more assertive easing.

Taiwan, Central Bank of the Republic of China (Thursday, June 18): We expect the CBC to keep rate unchanged at 2.00%. Taiwan continues to benefit from strong AI- and semiconductor-driven activity. Q1 GDP expanded to 14.5% y/y, while exports surged 51.7% y/y in May. Inflation has also firmed, with May headline and core CPI at 2.20% and 2.12% y/y, respectively, but CBC commented that inflation expectation has not risen significantly, and there is no imported inflation so far.

Philippines, Bangko Sentral Ng Pilipinas (Thursday, June 18): We expect the BSP to raise rates by 25bp to 4.75%, with a non-negligible risk of a larger 50bp move given elevated inflation pressures (May CPI: 6.8% y/y). The decision is complicated by a worsening stagflation backdrop, as growth momentum continues to soften (Q1 GDP: 2.8% y/y) while adverse terms-of-trade dynamics have contributed to currency weakness and higher inflation. The BSP is therefore likely to prioritize inflation and FX stability despite the growth slowdown.

Indonesia, Bank Indonesia (Thursday, June 18): We expect BI to deliver another 25bp rate hike to 5.75%, following the surprise 25bp off-cycle increase earlier in June. Persistent IDR depreciation has undermined market confidence and intensified capital outflow risks, leaving BI increasingly compelled to tighten policy to support the currency and attract inflows. Markets will also focus on BI’s updated macroeconomic projections, which currently envisage 2026 GDP growth of 4.9–5.7% and a current account deficit of 0.5–1.3% of GDP.

Switzerland, Schweizerische Nationalbank (Thursday, June 18): We don’t see any change in the SNB’s current stance or language on potential intervention. SNB President Schlegel has been consistent in his language on both aspects, highlighting that medium-term inflation expectations are not moving and they do have a heightened willingness to intervene. We believe market pricing of hikes by year-end are totally inconsistent with the central bank’s current stance – even if inflation does surprise higher, allowing greater exchange rate pass-through is an option.

Norway, Norges Bank (Thursday, June 18): No change is expected at the upcoming Norges Bank decision, but the policy board is highly unlikely to discount the possibility of further rate hikes as domestic inflation remains robust, with additional upside wage impulse possible from the positive terms-of-trade shock. Headline and underlying CPI continues to run comfortably above 3%, and markets would have also learned lessons from the surprise hike at the last meeting regarding Norges Bank’s current reaction function.

U.K., Bank of England (Thursday, June 18): The Bank of England is unlikely to follow the ECB in hiking rates as the doves and swing-voters on the monetary policy committee are clearly unconvinced of second-round risks. Bank of England Governor Bailey has been clear in his view that labor market slack and exigent tightening from changes in market pricing of rates should be sufficient to anchor inflation expectations for now, but there will likely be several dissenting votes in favor of a precautionary move.

Czechia, Česká národní banka (Thursday, June 18): Unlike peers in the rest of Central and Eastern Europe, the CNB does not have to contend with fiscal impulse in policy decisions. Both headline and sequential inflation are more than manageable for now, though wage growth remains robust and simply relying on household restraint (which is evident in the retail sales figures) is probably not enough from a policy standpoint. Real rates are not excessive by EM standards, but the CNB will need to react to any material changes in the ECB’s trajectory, so a hike cannot be ruled out.

Source: BNY

Source: BNY