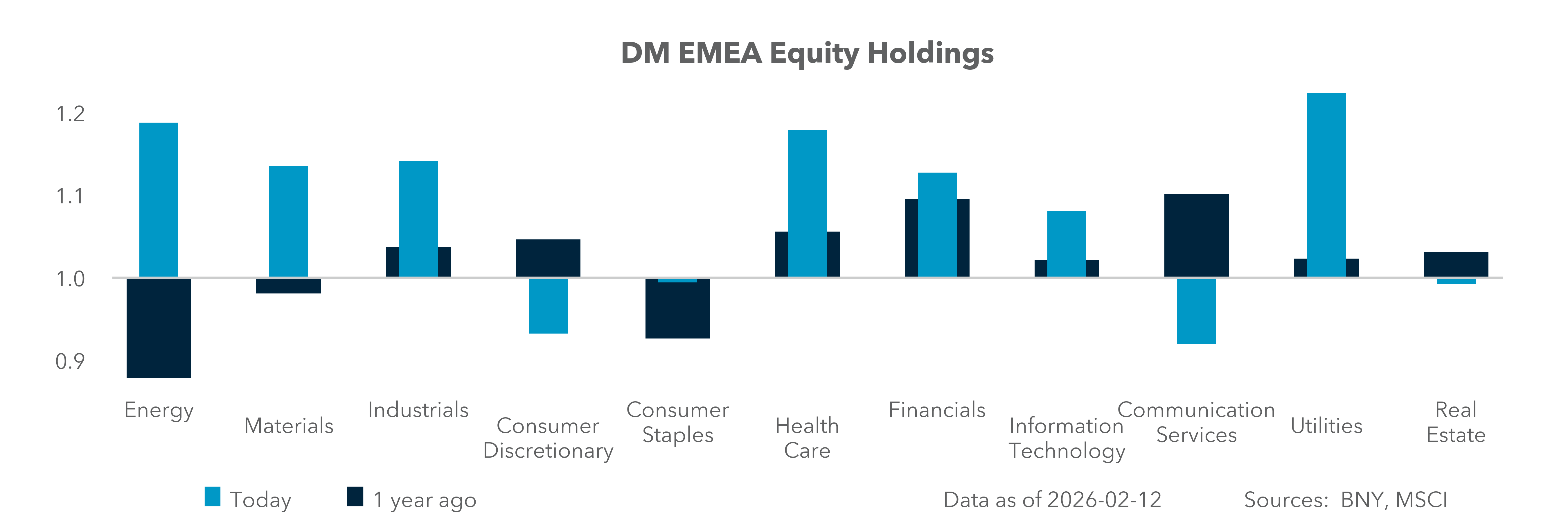

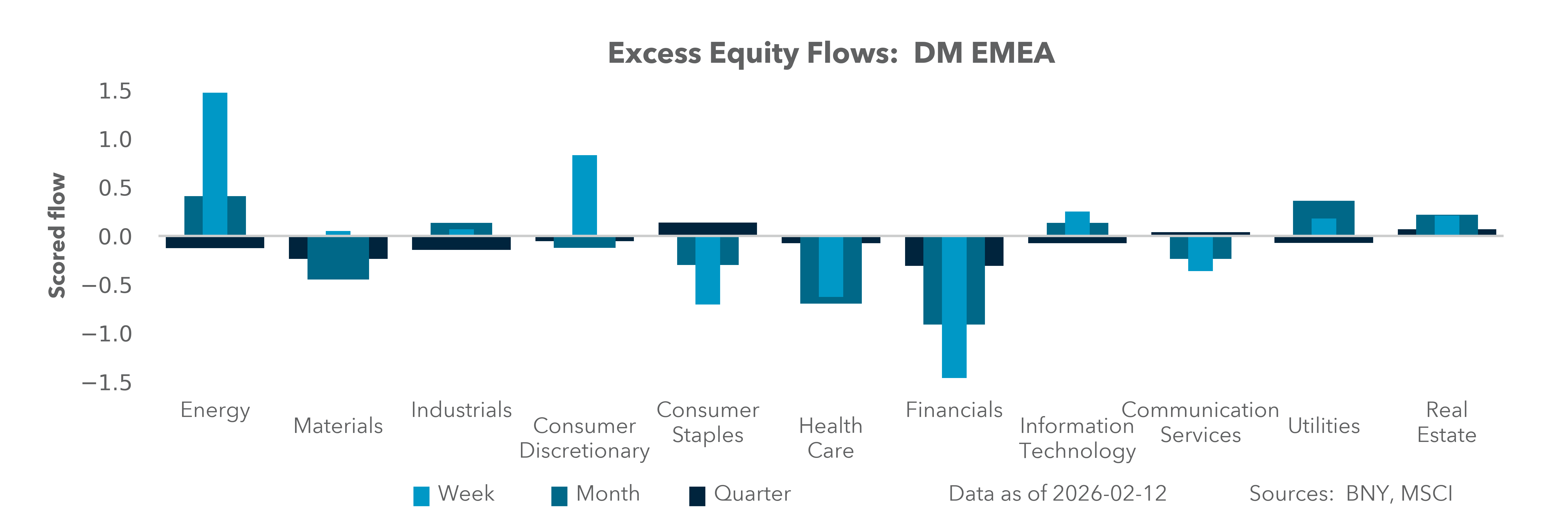

For much of the week, it appeared that any sector facing even a modicum of “AI-disruption risk” saw a retreat from asset allocators. What began as a U.S.-centric story broadened, though by the end of the week Europe started to provide a buffer. On the face of it, economies with lower services exposures, such as the U.K. and continental Europe, supposedly have a larger moat against AI, but the holdings base and valuations also matter. In absolute terms, the U.S. has been outperforming so much, even among cross-border investors, that the bar for a correction was low, even if this wasn’t as broad-based as earlier in the month. In relative terms, markets have to face up to the fact that financial conditions, on balance, will likely tighten from here and raise discount factors for asset allocation.

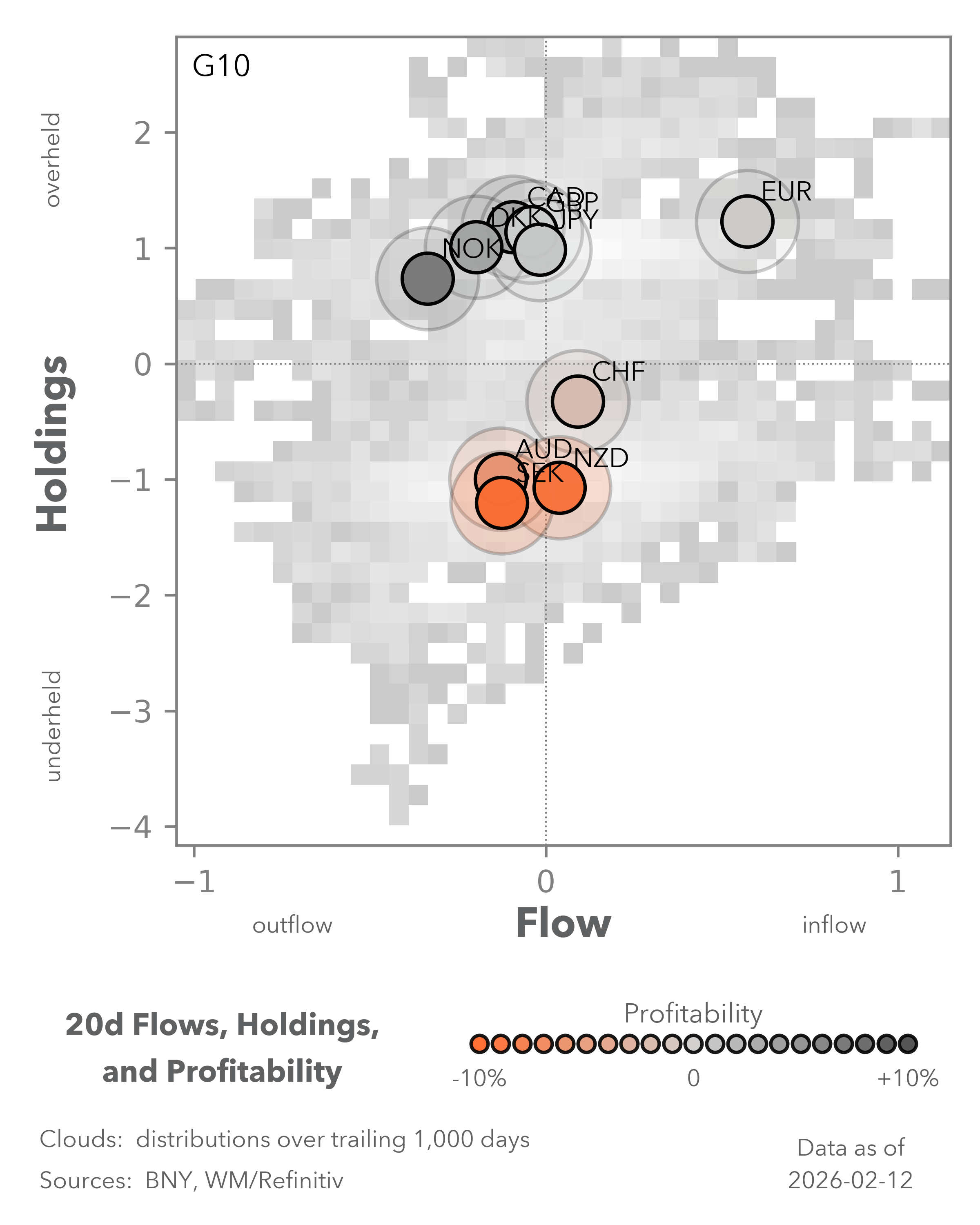

U.S. data are now looking marginally more than benign, while pivots toward tightening are being highlighted outright in G10 economies such as Australia and Norway. In hindsight, the ability of tech companies to raise century-maturity GBP-denominated debt could mark the low point of easy financial conditions through the credit channel. Coupled with attempts at further fiscal stimulus from the Eurozone, Japan, China and most likely the U.S., yield curves and even policy rates will be next. Stabilizing equity markets will help keep global financial conditions “in a good place,” but we anticipate a period of market asymmetry: Sentiment will react adversely to upside shocks in price-related data, while anything simply “benign” should not expect a fulsome response in asset prices.

1) Rotation: Our equity flow and holdings data indicate that significant rotation has taken place on an industry group level between software and semiconductors. The latter industry group continues to benefit from expectations of secular growth and strong balance sheets, but it will be a challenge for U.S. markets to maintain gains on the basis of flows into a single industry group or a cluster of industries. Fed speakers will likely continue to increase their emphasis on reacting to the distribution of growth rather than aggregate figures.

2) European sentiment: “Hard power” realism is now the guiding principle of European defense policy. The spending uplift in defense is real, but the current effect is one of ensuring that forward orders and expectations indices (such as the ZEW and PMIs due next week) no longer decline, but expansion, which could structurally lift growth, is a different story. National leaders will likely return from the Munich Security Summit with new investment plans, but action must be front-loaded, especially taking advantage of the opening provided by a more cautious European Central Bank (ECB).

3) APAC spending: Market activity in Asia Pacific will fall materially over the Lunar New Year holidays, but consumer-facing companies in the region and globally (e.g., European luxury goods companies) will be looking at consumption patterns hoping that China can lead the region in turning consumption around. Credit data for January do not bode well for demand, but with Japan’s new government pledging fiscal loosening and China approaching the usual planning season for fiscal announcements, upside risks should not be discounted. Crucially, stronger CPI figures in the region will help lift real effective exchange rates, which we still see as the “healthiest” form of dollar weakness.

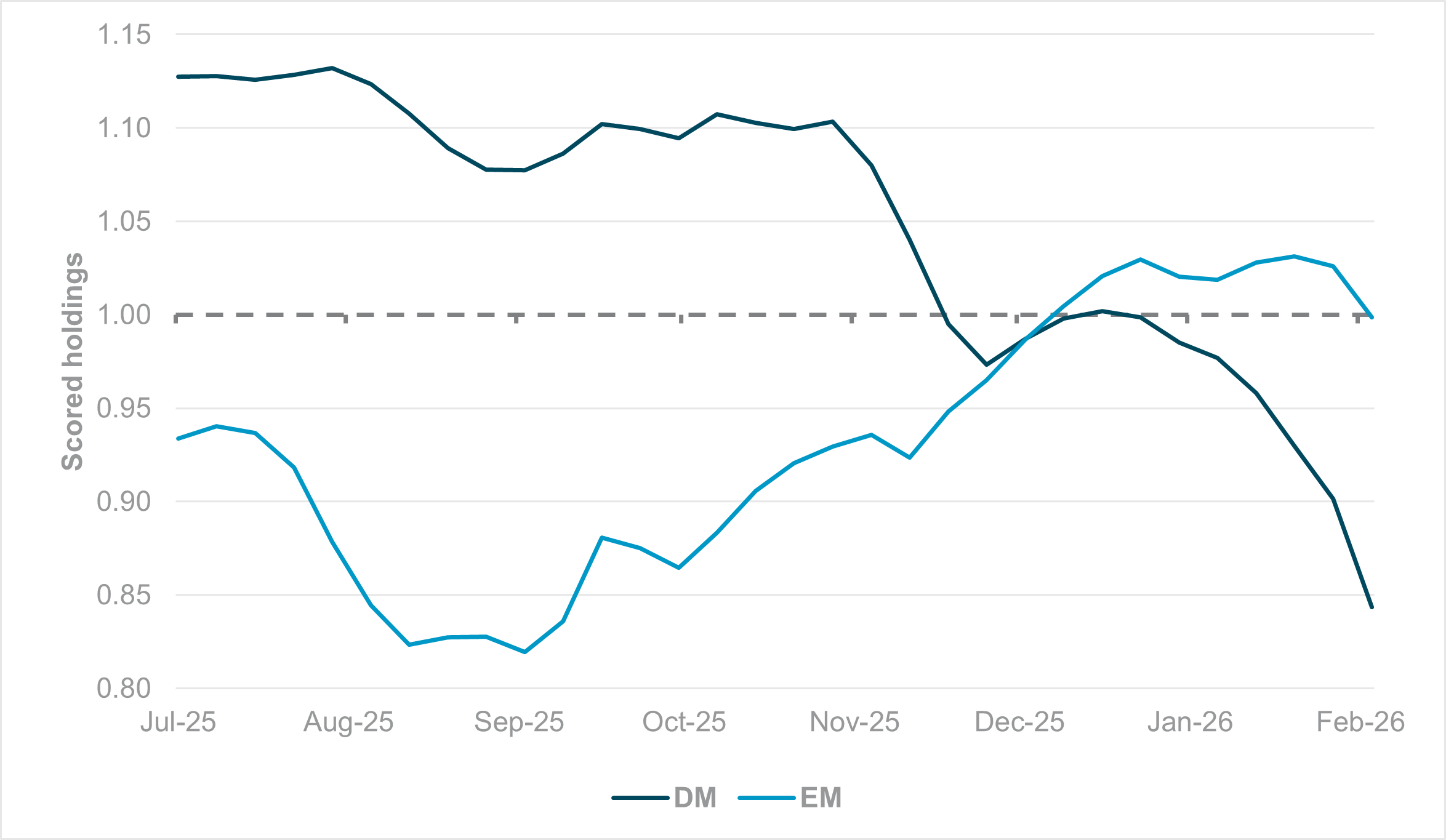

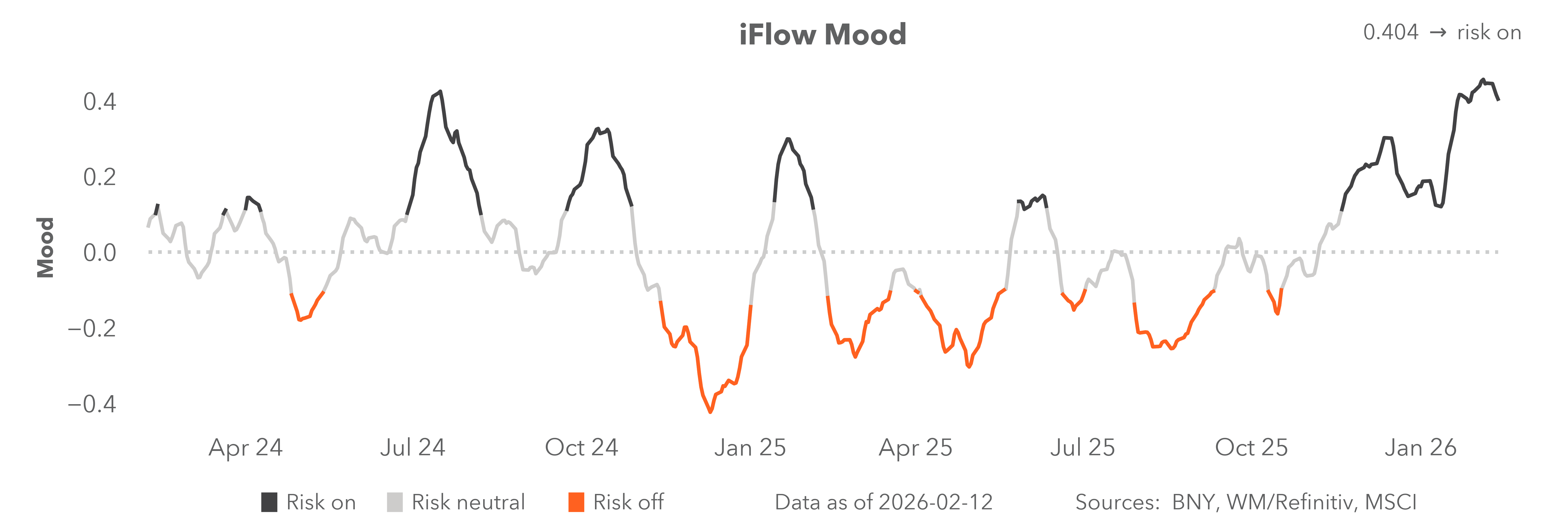

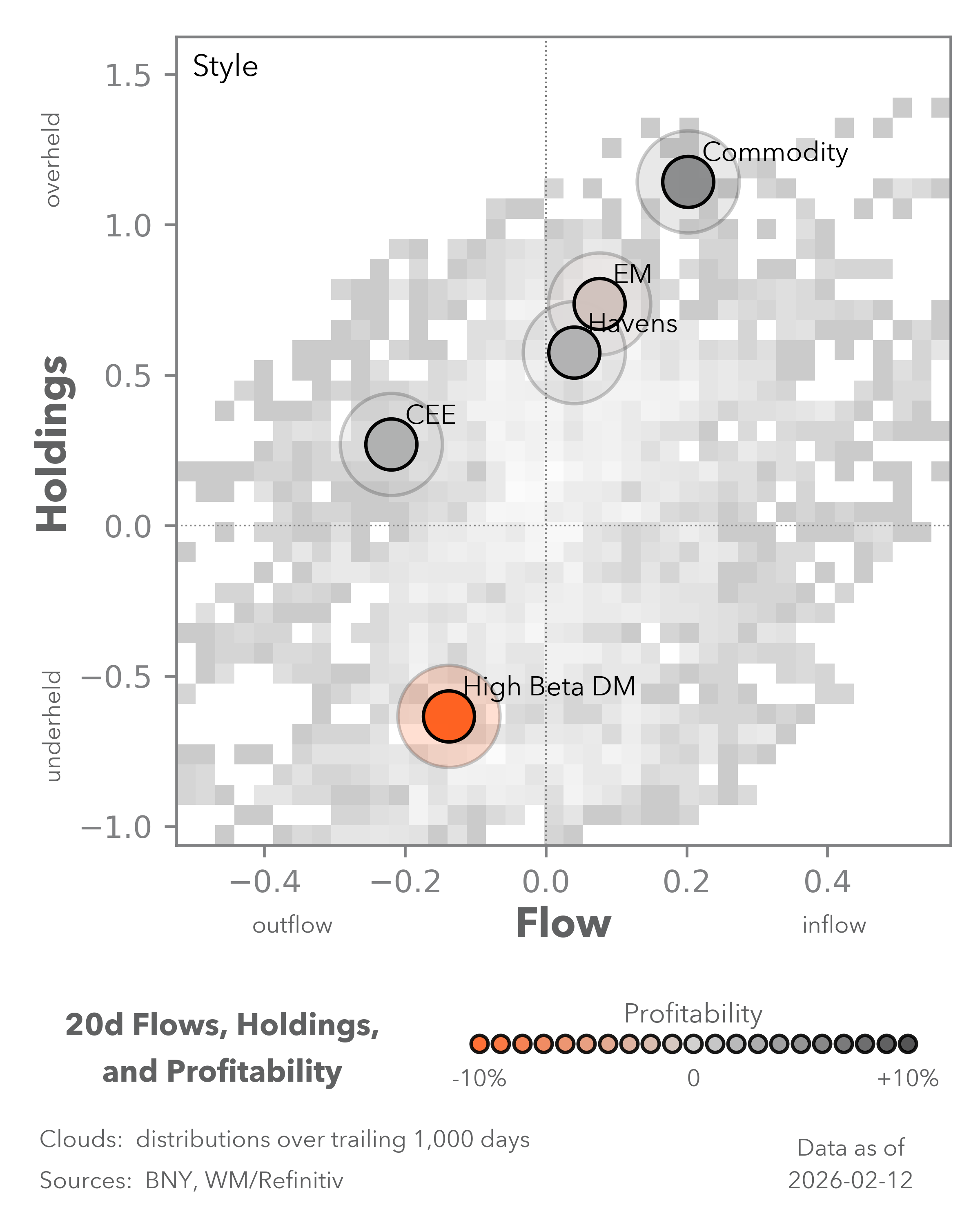

4) Carry trades: iFlow’s two main barometers for risk sentiment – iFlow Mood and iFlow Carry – have clearly peaked, but this doesn’t automatically point to a sudden reversal. Equity flows, even in the U.S., remain strong relative to developed market (DM) cash instruments, even if central banks are now more nuanced on their policy outlook. As mentioned above with respect to financial conditions, an acceleration in tightening to encourage higher cash flows is needed to truly cause a turn in risk. Meanwhile, FX carry trades have also peaked in holdings terms and on balance, high-yielding currencies are also facing their fair share of outflows. Latin American currencies are particularly exposed in this respect due to elevated holdings, meaning more politically painful hikes are likely essential to help avoid any form of disruptive unwinding.