Inflation cools; the real challenges remain

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Geoff Yu

Time to Read: 8 minutes

Bottom line: Markets have moved from relief to validation. Softer U.S. labor data and better inflation prints have reduced the urgency around further tightening, but they haven’t settled whether growth is slowing in a manageable way or whether policy expectations have moved too far.

The global narrative is becoming less uniform. In the U.S., the question is whether the Fed can stay patient without seeing inflation risks reemerge. In Europe, the debate is moving away from emergency inflation management and back toward growth, fiscal credibility and defense financing. Asian markets need evidence that policy support and the technology cycle are feeding through into broader demand rather than remaining concentrated in a narrow set of sectors. Korean equities and the yen are likely to remain the main volatility channels.

Across emerging markets, the flow picture still looks more like rotation than retreat. Higher U.S. yields are forcing investors to reassess crowded bond exposure, but the adjustment is not yet a broad exit from risk. That distinction matters: equities, selective carry and currencies with stronger domestic anchors can still attract capital even as duration remains vulnerable.

Call to action: Prefer rotation into Latin American equities and selective carry, while staying alert to Asia FX volatility and Europe’s fiscal trade-off. Treat duration relief cautiously until activity data confirm the softer labor and inflation signals.

In focus this week

U.S. services. ISM Services and S&P Global Services PMI will provide the first meaningful test of whether last week’s payroll weakness is spreading into broader activity. A softer set of prints would support the view that expectations for another Fed hike had moved too far, too fast. Firmer data would argue for more caution in treating one weak jobs report as a turning point.

China inflation and credit. China’s CPI, PPI and aggregate financing data will be the key APAC releases. The question is whether policy support is finally translating into firmer credit demand and more stable price pressures, or whether weak inflation still points to insufficient domestic demand. The answer will matter for Chinese assets, regional FX and the broader read-through to Asia’s export cycle.

Final European CPI and Mexico inflation. Final inflation readings from Germany and France should confirm the broader European disinflation trend, reinforcing the shift in focus from inflation to fiscal policy. Mexico’s June inflation report will matter more for the policy path, testing whether Banxico can maintain its current stance or whether sticky price pressures require a more cautious tone.

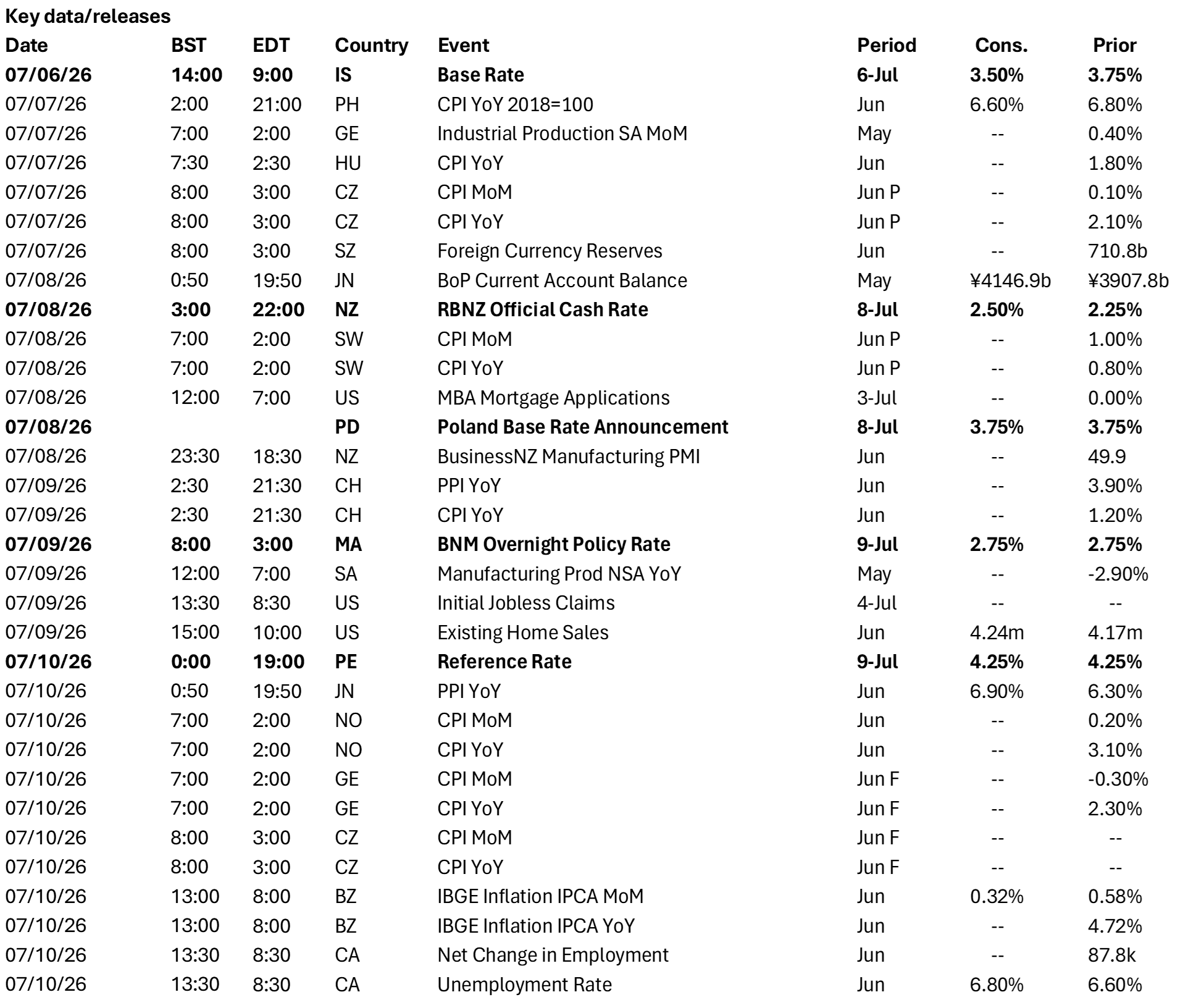

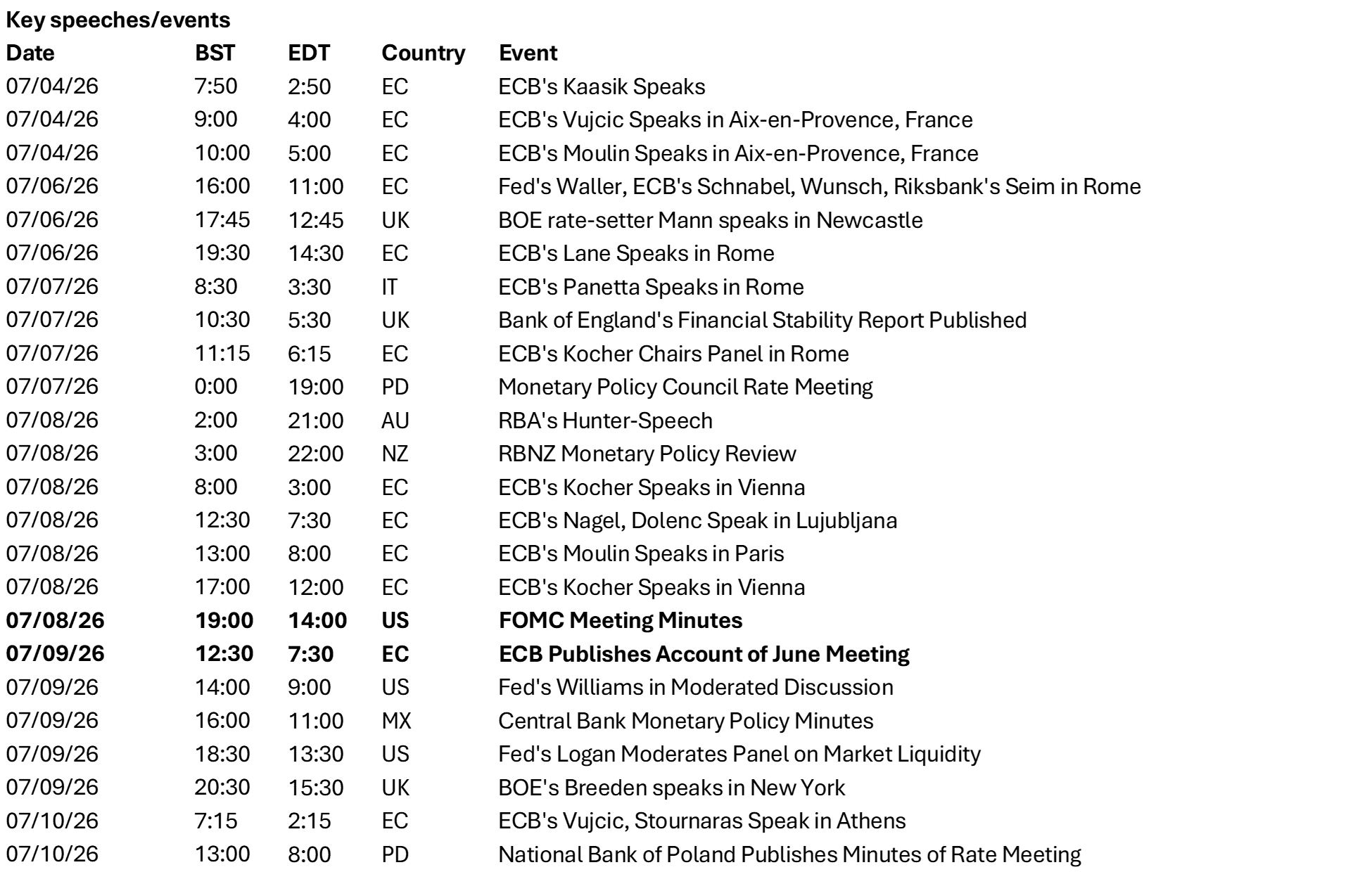

Poland, Peru and New Zealand. Rate decisions in Poland and Peru should show how difficult it is for smaller central banks to sound dovish while idiosyncratic risks remain elevated. In Poland, falling inflation reopens the door to easing, but fiscal credibility and borrowing needs argue for caution. In Peru, policymakers may prefer to stay on hold, but above-target inflation and sensitivity to the Fed outlook leave little room for an outright dovish turn. The Reserve Bank of New Zealand (RBNZ) is expected to hike, but the risk is that it disappoints the most hawkish pricing.

NATO Summit. The summit will put Europe’s fiscal trade-off back in focus. President Donald Trump is expected to press allies to shoulder more of the defense burden, just as EU governments face stretched deficits, heavy borrowing programs and weak growth. The strategic direction is clear; the funding model is the harder question.

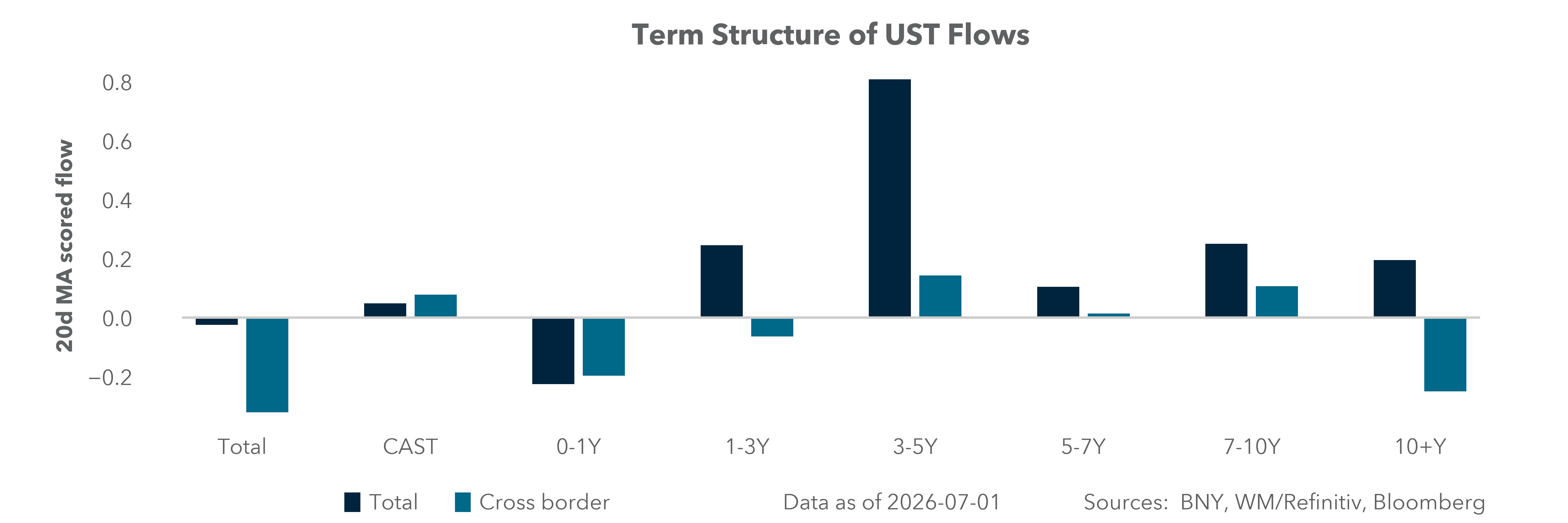

North America: Rate hike expectations will face ISM, PMI

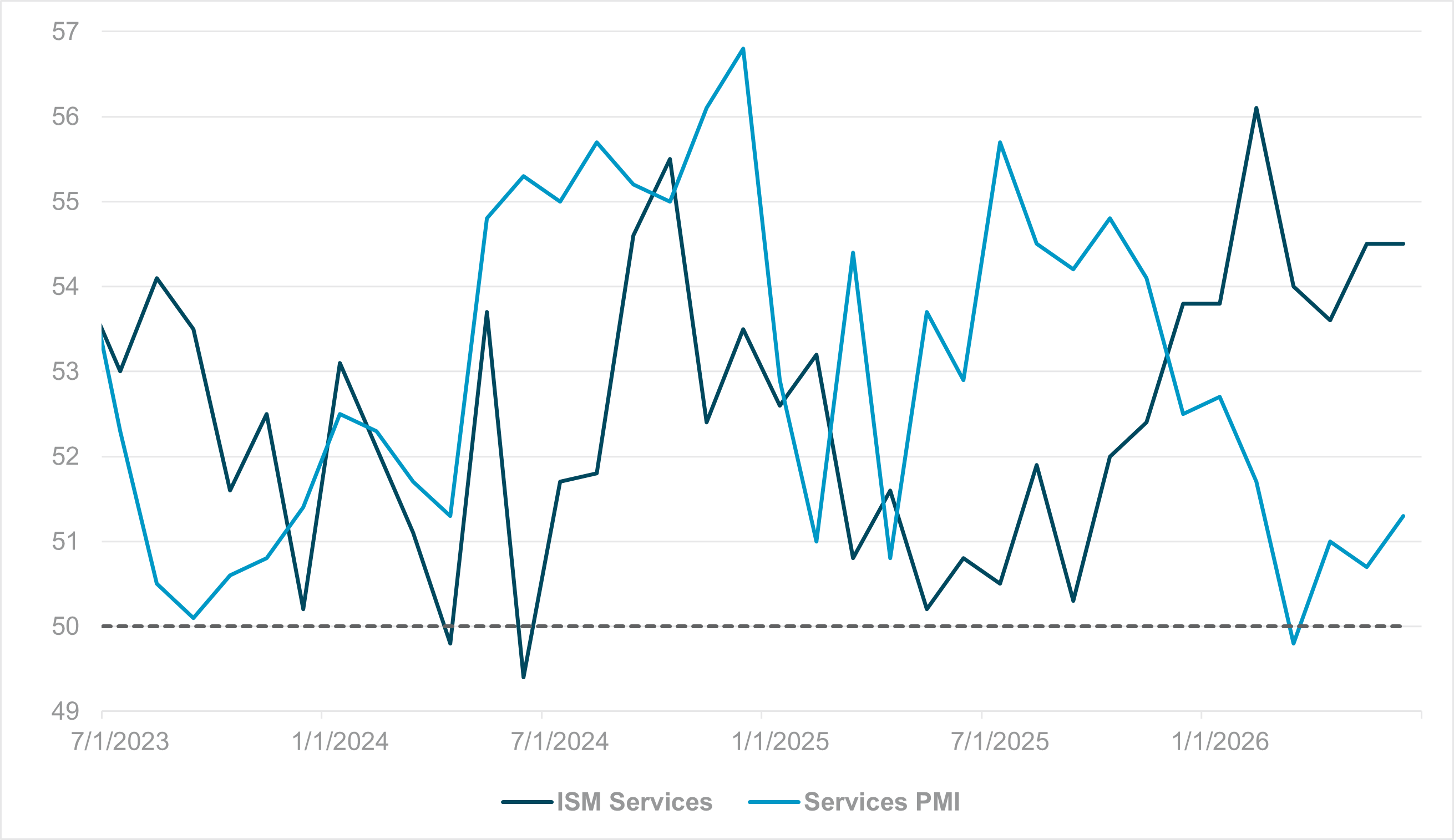

EXHIBIT #1: S&P SERVICES PMI AND ISM SERVICES INDEX REMAINED POSITIVE IN Q2

Source: BNY, Bloomberg

Our take: Last week’s weak NFP print was an indication that U.S. labor demand may be cooling more quickly after a string of recent strong payrolls, suggesting that market expectations for the Fed to hike may have been overdone. This week is lighter from a data perspective, but Monday’s S&P Global PMI and ISM Services will be the key reads, alongside a handful of Fed appearances that should keep markets attentive to the policy reaction function. Governor Christopher Waller’s appearance in Rome will be watched for any nuance on the labor-market outlook, while Dallas Fed President Lorie Logan’s panel on market liquidity is arguably the more interesting event given the ongoing discussion around Fed implementation and balance sheet mechanics.

Canada remains quiet, with only Friday’s unemployment rate offering any meaningful domestic data point.

Forward look: The most important releases this week are the U.S. Services PMIs and ISM Services, as they will help determine whether last week’s payroll weakness is starting to show up in broader activity data or remains an isolated labor-market signal. A softer set of prints would strengthen the case that the Fed isn’t inclined to hike immediately and could extend the recent easing in front-end yields, while firmer readings would argue for more caution in extrapolating from one soft NFP report. Logan’s remarks on liquidity and balance sheet normalization Thursday could influence term premium and money-market pricing even if they don’t directly alter the rate path.

In Canada, the unemployment report is unlikely to move the broader rates outlook unless it surprises materially, leaving U.S. data and Fed commentary the main drivers.

EMEA: Fiscal back in focus as inflation relief arrives

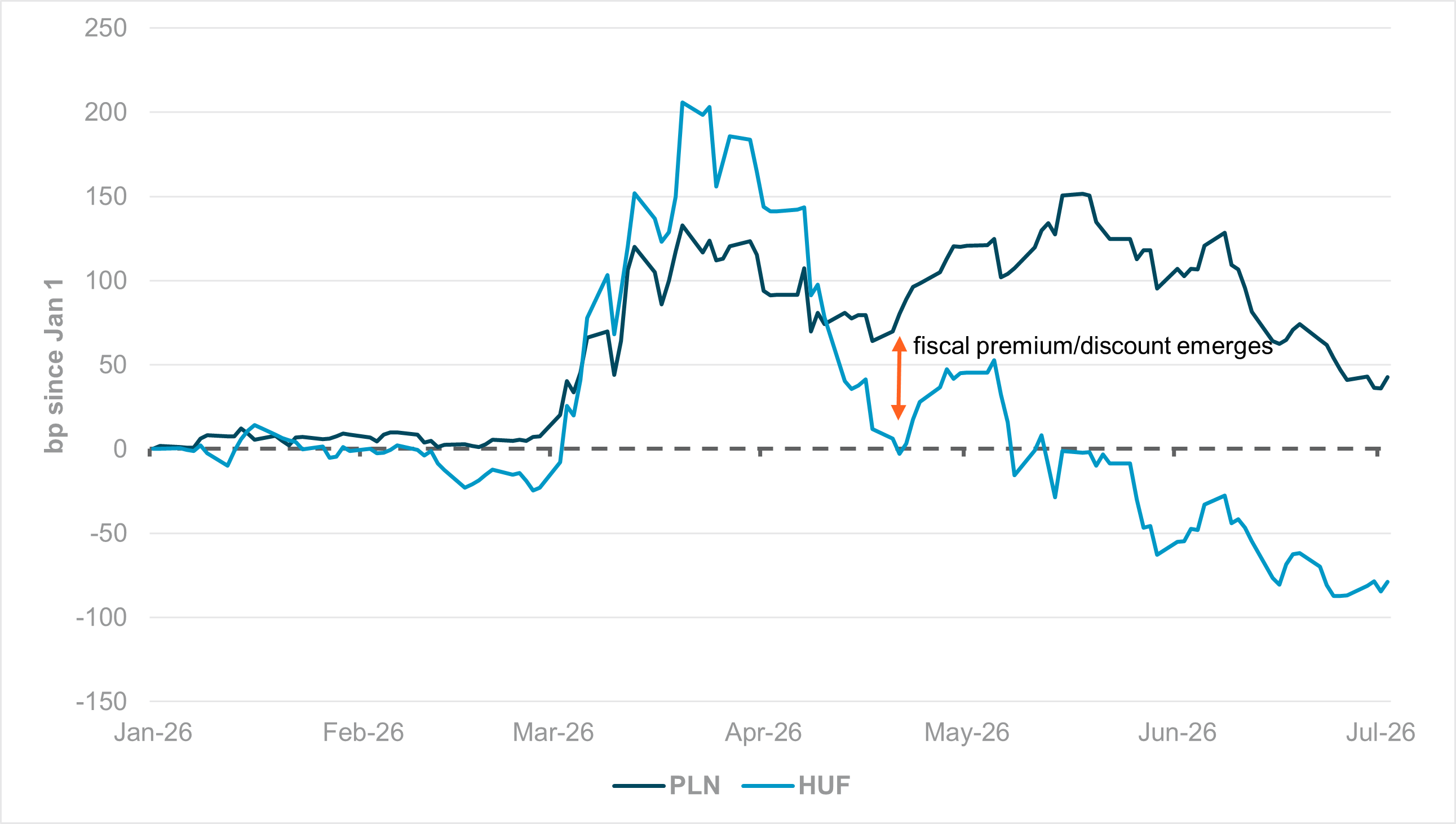

EXHIBIT #2: CHANGE IN 1Y1Y FORWARD RATE, HUNGARY AND POLAND

Source: BNY

Our take: June's preliminary inflation prints across Europe show a clear sequential slowdown, driven by the extended ceasefire and lower commodity prices. We expect inflation expectations to continue falling. For a continent starved of growth, the door is opening for a recovery pivot before political pressures on Brussels intensify. The first step is for central banks to move back toward neutral before considering a renewed easing cycle. Hungary has already begun this process, the ECB Governing Council is showing increasingly divergent views, and next week’s NBP decision will provide an early indication of whether Poland follows. Polish inflation has fallen sharply to 2.5% y/y in June, potentially reopening the door to further easing.

The constraint, however, is no longer energy or supply shocks, but the risk that financial conditions loosen faster than fiscal consolidation. Poland’s full-year fiscal deficit is still expected at 6.8% of GDP, while 37% of this year’s borrowing program remains outstanding. Any support from a flatter yield curve would therefore be welcome, particularly as work begins on next year’s budget.

Fiscal credibility is now essential for governments seeking to reduce borrowing costs toward pre-war levels, if that’s still achievable. Higher Fed expectations and tighter ECB policy are already exporting tighter financial conditions across Europe, leaving far less monetary policy space. Hungary illustrates the point. Markets initially priced a repeat of Budapest’s 2022 fiscal response to the energy shock, concerns reinforced by a Q1 fiscal deficit equivalent to 9% of GDP. Since then, the change of government, commitments to fiscal discipline, renewed prospects for EU funding and falling inflation have materially improved sentiment. Between March and June, the implied policy path gap moved by more than 230bp in Hungary’s favor relative to Poland, underlining how quickly fiscal credibility can alter market pricing. The challenge now is execution.

Forward look: Preliminary June inflation releases continue next week, with soft prints expected across the region. Hungarian CPI is forecast at just 1.8% y/y, below target and below expected Czech inflation (2.1% y/y), despite the Czech Republic never experiencing a comparable fiscal impulse. Sweden’s underlying inflation is also expected to remain below 2% y/y, reinforcing our view that market pricing for the Riksbank is more aggressive than the policy board’s own intentions, although policymakers are likely to tolerate further SEK appreciation given their assessment of currency valuations. Final June CPI releases for Germany and France are due on Friday.

The NATO Summit in Ankara is the key political event, with Trump expected to press European allies to shoulder a greater share of defense spending despite increasingly constrained public finances. Recent developments in Europe’s defense sector have weighed on performance, while structural challenges elsewhere in the economy persist. Ultimately, European policymakers continue to face the same fundamental question: how to generate stronger growth while financing an ever-expanding fiscal burden.

APAC: China credit, regional inflation to test whether policy support is gaining traction

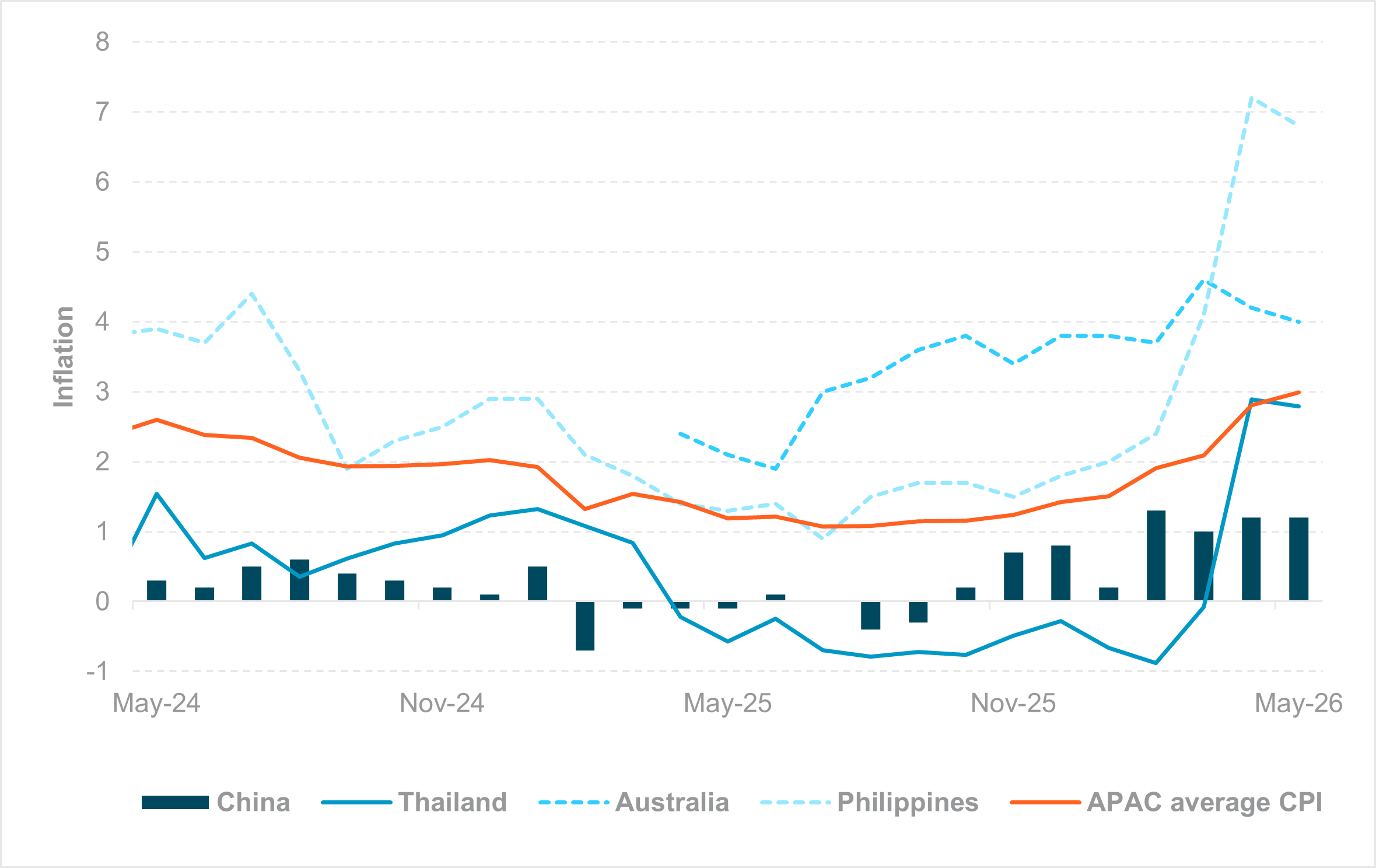

EXHIBIT #3: REGIONAL HEADLINE INFLATION PEAKED WITH CRUDE OIL

Source: BNY, Bloomberg

Our take: The week will be anchored by Asia’s inflation and credit data, with China’s June CPI, PPI and aggregate financing figures taking center stage. The releases will offer an important read on whether policy support is translating into firmer credit demand and stabilizing price pressures. Inflation data from Taiwan, Thailand and the Philippines will be closely monitor in light of the recent normalization in crude oil prices and what it means for the regional inflation picture. Singapore's potential Q2 GDP release could provide an early gauge of regional growth momentum.

Attention will then shift to policy, with decisions from the RBNZ and Bank Negara Malaysia expected to guide expectations for the regional rate outlook.

In Japan, household spending, real cash earnings and PPI will be closely watched ahead of the Bank of Japan’s next policy meeting for evidence that wage growth is feeding into stronger consumption and underlying inflation. Meanwhile, Taiwan’s June export data will provide another key test of whether AI- and semiconductor-driven demand continues to underpin Asia’s technology cycle.

Forward look: The normalization in crude oil prices has yet to offset persistent capital outflows and broad U.S. dollar strength. In India and Indonesia, stronger inflows into money market instruments and government bonds have provided little FX support as most purchases were FX-hedged. Despite fragile Asia FX amid elevated volatility, the macro backdrop has improved, with business confidence strengthening across the region – except in Indonesia where it has slipped back into contraction. We therefore caution against chasing Asia FX weakness. Three currencies stand out:

1) CNY: Minimal hedging demand leaves the yuan vulnerable if equity markets correct.

2) IDR: Weak domestic fundamentals leave USDIDR at risk of new highs, potentially forcing Bank Indonesia to tighten further.

3) KRW: Elevated KOSPI volatility has kept USDKRW biased higher. With the KOSPI down around 10% in early July, a deeper correction could trigger broader foreign selling beyond rebalancing flows.

Latin America: Asset rotation pointing to real rate fears

EXHIBIT #4: MONTHLY SMOOTHED FLOWS IN LATAM, EQUITIES VS. BONDS

Source: BNY, Bloomberg

Our take: Our longstanding concern about over-crowded exposure to Latin American bonds is beginning to materialize. End-June flows marked the first time in two months that the monthly smoothed flow score turned negative. More importantly, the pace of deterioration is approaching that seen in early March, when conflict-driven risk aversion drove regional bond flows to their weakest level of the year. This time, however, the catalyst is domestic to markets rather than geopolitics: renewed hawkish repricing of U.S. rates. We doubt the softer-than-expected U.S. payrolls report will materially alter that dynamic. Combined with stretched FX positioning, higher U.S. yields leave Latin America's yield-sensitive bond markets vulnerable to further adjustment.

That does not imply broad capital outflows from the region. Instead, our data point to rotation rather than retrenchment, with equity flows approaching net purchase territory after a particularly weak May. We view this as constructive. Equities are better positioned than duration if central banks ultimately catch up to easing expectations, while stronger U.S. growth – the driver of higher Treasury yields – should continue to support external demand for Latin America despite trade realignment and renewed uncertainty over USMCA. Given the structurally lower FX hedge ratios associated with equity inflows, this rotation does not undermine our constructive tactical view on Latin American carry, where regional currencies remain our preferred expression.

Forward look: Peru’s central bank is expected to leave rates unchanged this week, although inflation remains above target and a hawkish bias is likely until the Fed signals a clearer shift in direction. Political developments will also stay in focus as President Keiko Fujimori forms her government; the appointment of economist Elmer Cuba as finance minister is likely to be welcomed by markets.

Mexico’s June inflation report will test the case for Banxico’s current policy stance, while Washington’s decision to move USMCA to rolling annual reviews adds a fresh layer of uncertainty for trade and investment that will require a more comprehensive policy response.

Central bank decisions

Israel, Bank of Israel (Monday, July 6): The BoI is expected to continue easing as inflation falls below 2%, with further risks to the downside as fiscal impulse drops. It has actively encouraged such expectations as current USDILS levels are quite uncomfortable, and keeping the pair above 3.0% after the decision will be considered a strong result. Growth is already expected to decelerate materially with the latest IMF revision (from 4.8% y/y to 3.5% y/y), and markets will be on the lookout for more active intervention signals. Nonetheless, general economic performance remains strong. Given the Fed’s current direction, the BoI will need to be wary of pushing too much in the opposite direction.

New Zealand, Reserve Bank of New Zealand (Wednesday, July 8): We expect the RBNZ to raise the Official Cash Rate by 25bp to 2.50%, marking its first rate hike since May 2023. The decision is supported by stronger-than-expected Q1 GDP growth of 1.5% y/y, continued labor market resilience, a marked improvement in business sentiment, and expectations of a surging Q2 CPI reading at the end of July, after inflation plateaued near the top of the 1–3% target range for the past three quarters through Q1 2026. The key focus will be its forward guidance and whether it would retain a hawkish bias, signaling further tightening and keeping the policy rate on track to reach 3.00% by Q1 2027.

Poland, Narodowy Bank Polski (Wednesday, July 8): The NBP is trying to hold the line on rates, and the inflation outlook is finally turning supportive. June preliminary inflation fell to 0.5% m/m, pushing the headline annualized rate back to 2.5% from 3.1% in May, helping support real rates and negating the need for swift convergence to the ECB. If the government pushes for much-needed fiscal consolidation thereafter, we see potential for further downside in inflation. Markets are currently pricing in unchanged rates over an extended period, but a slight upside bias will remain until the ECB signals precautionary moves are complete.

Malaysia, Bank Negara Malaysia (Thursday, July 9): We expect BNM to keep the Overnight Policy Rate unchanged at 2.75%. Domestic fundamentals remain supportive, with Q1 GDP growth of 5.4% y/y, robust export and industrial production momentum, and stable core inflation at 2.0%. We expect BNM to reiterate that the current monetary policy stance remains appropriate and consistent with the economic outlook, while remaining vigilant over domestic conditions and inflation risks. The tone is likely to stay constructive, but we do not expect the recent U.S. dollar strength and hedging-driven depreciation of the ringgit to prompt a more hawkish stance. Our base case is for BNM to keep policy unchanged through 2026.

Source: BNY

Source: BNY