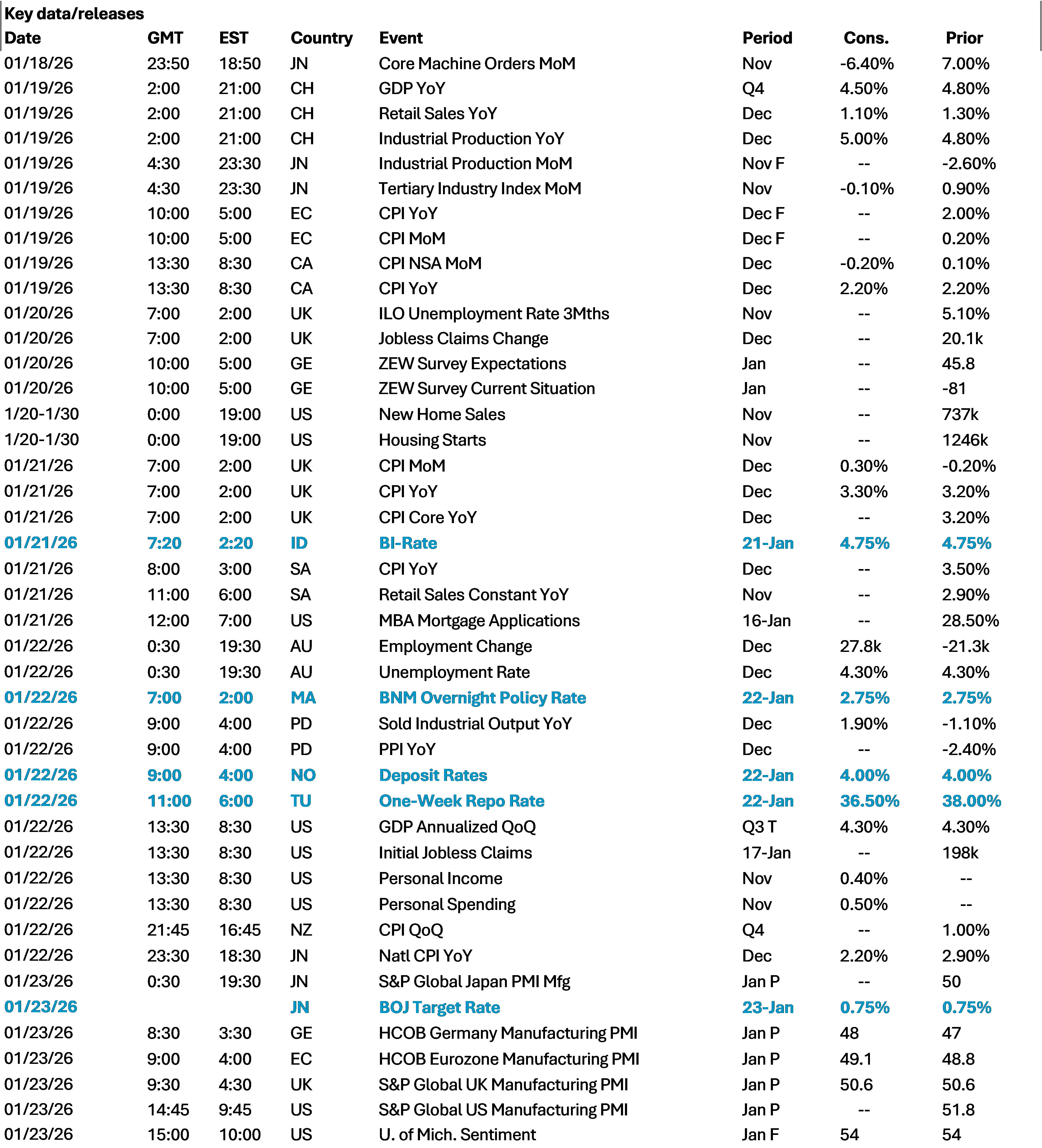

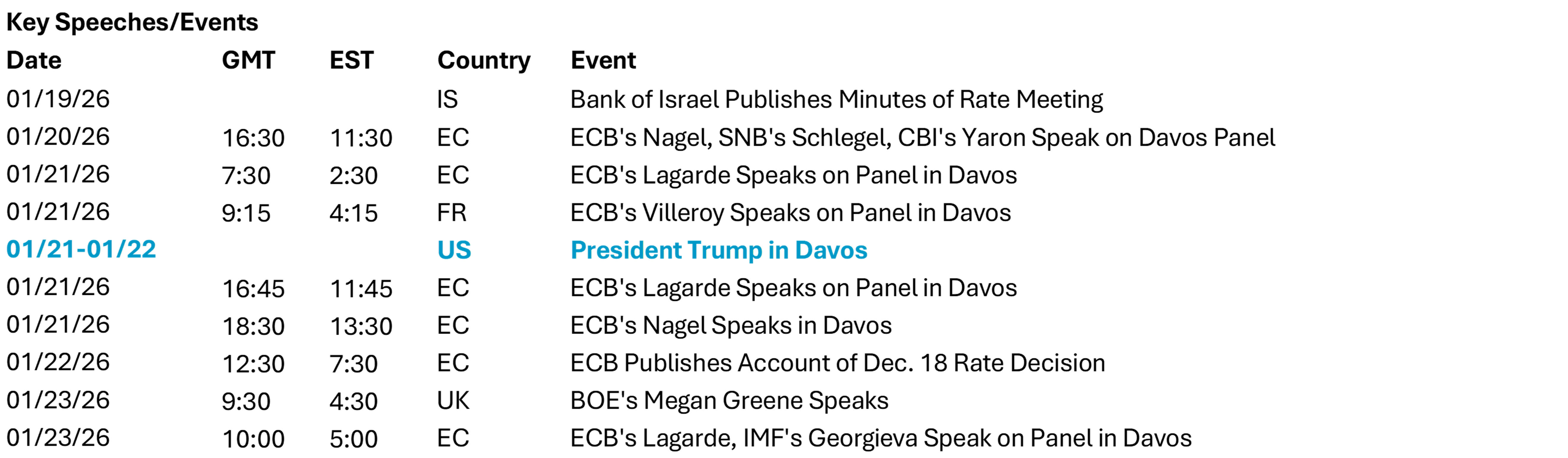

Crosscurrents and inflection points

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

“As January goes, so goes the year” has been less of a tailwind for investors than in previous years. There has been a notable lack of conviction, highlighted by the extremely negative correlation in our trend index from iFlow. Chasing momentum has not worked. There is no fear of missing out, but rather growing patience to buy the dip. The path to 10%-plus S&P 500 returns is widely expected to deliver more volatility than in 2025. U.S. midterm elections have become a key pivot point for potential policy shifts in H1 2026, as the Trump administration pushes all levers to run the economy hot. This has led to three notable trades:

1) The rise of small-cap shares and a clear rotation away from tech

2) Homebuilders and mortgage-backed securities (MBS) buying as affordability becomes essential

3) New record highs for industrial metals as supply and demand search for an equilibrium amid fragmentated supply chains

The following themes shaped last week’s market sentiment.

Supreme Court rulings: tariffs and Cook. Markets will be watching the hearings on Governor Lisa Cook and the justices’ mood. Markets are also awaiting a ruling on tariffs. Both remain part of the bond market event risk horizon, but how and when they are settled is unknown. Higher deficits and less accommodative Fed policy could drive bond yields higher, adding to the consensus curve steepening trade.

Geopolitics. The short list of places to watch includes Iran, Ukraine, Greenland and Mexico. The push to use U.S. military continues to rattle risk-takers. Trump’s success in Venezuela increases his appetite to take other geopolitical risks. As the Economist notes: “The world is being sped up by a hubristic, glory-seeking president who scorns detail. Mr. Trump may not grasp the risks he is running until it is too late.”

Rotations and Q4 earnings. This week, 10% of the S&P 500 reports, with key focus on Netflix, regional banks and Intel, along with some large consumer names like P&G and J&J. So far, Q4 EPS has moved from 8.3% to 8.8% with whispers that we end at 10% in mid-February. The biggest movers in the first two weeks of 2026 have been the rally in the Russell 2000 small-cap index versus the tech-heavy NASDAQ-100 – a rotation that has moved nearly 10% from mid-December lows. Fed rate cuts, ongoing valuation concerns and stronger economic data, combined with earnings season, form a key test for the broadening out of risk beyond the Magnificent 7 theme of the past three years.

AI and paying for it. 2026 will test the ability of hyperscalers to continue to invest in AI without leverage. The widening of Oracle credit default swaps in Q4 remains a cautionary signal for any tech company borrowing aggressively. Against this backdrop, we see four key forces supporting the AI narrative.

Affordability, housing and Trump’s Davos plan. Most investors see 30% as the threshold for fair housing costs. This includes rent or mortgage costs, insurance, taxes and utilities. One factor shocking consumers has been surging utility costs, averaging 7% y/y over the last five years, with heating and electricity leading the rise. In tweets and speeches ahead of the World Economic Forum, Trump has pushed MBS buying plans involving Freddie Mac and Fannie Mae – compressing mortgage spreads by 15bp. He has floated the idea of banning institutional buying of homes – hitting some private credit investors. He also has pressured the FOMC to cut rates further. The key to affordability is twofold: improving consumer incomes and building more supply – with three to four million new homes needed to make up for more than a decade of underbuying.

Japan and equities are center stage for risk reversals this week

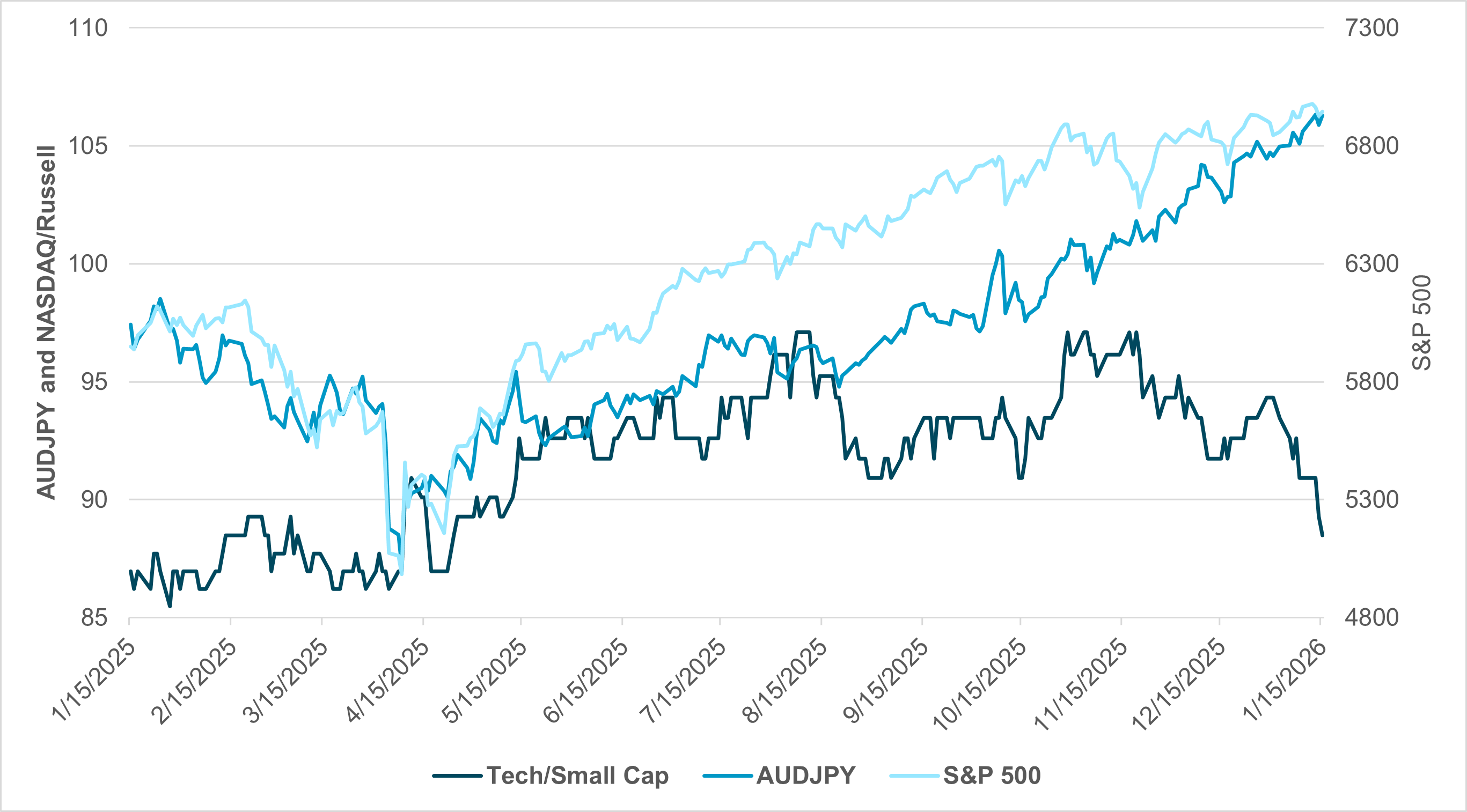

EXHIBIT #1: AUDJPY, THE S&P 500, AND THE ROTATION OF THE RUSSELL 2000 VS. THE NASDAQ

Source: BNY

Our take: The role of AUDJPY as a hedge against equity markets has come back into focus after last week. First, there is a risk of JPY intervention from Japan’s Ministry of Finance and potentially the U.S. Treasury. Second, U.S. investors have actively bought Japan bonds and equities but hedged the JPY, making this a clear vulnerability in the event of a position unwind.

Third, Metals – both precious and industrial – have reversed on back of China’s efforts to curb speculation. This hurts the commodity link to AUD buying. Similarly, the urgency for an RBA rate hike has stalled. Finally, the S&P 500’s ability to rotate from the Tech sector to the small caps without a sharp downturn hinges on Fed rate cuts and stronger Q4 earnings this week.

As we can see, the nearly 10% drop in the NASDAQ/Russell rotation index since December is the largest since April, and its correlation with the S&P 500 remains positive, suggesting some downside risks.

Forward look: The U.S. holiday-shortened week appears ripe for correction risks. The ongoing rally in U.S. equities, the USD and the relative stability of U.S. bonds will be tested by the week’s news cycle – from Japan’s snap election risks and the Bank of Japan (BoJ) decision, to the Fed policy debate and stronger U.S. economic data. The relative calm in FX and bond markets may begin to shift in the second half of January as investors reassess policy responses and market feedback loops.

Fed faces sticky inflation, and better economic data is key

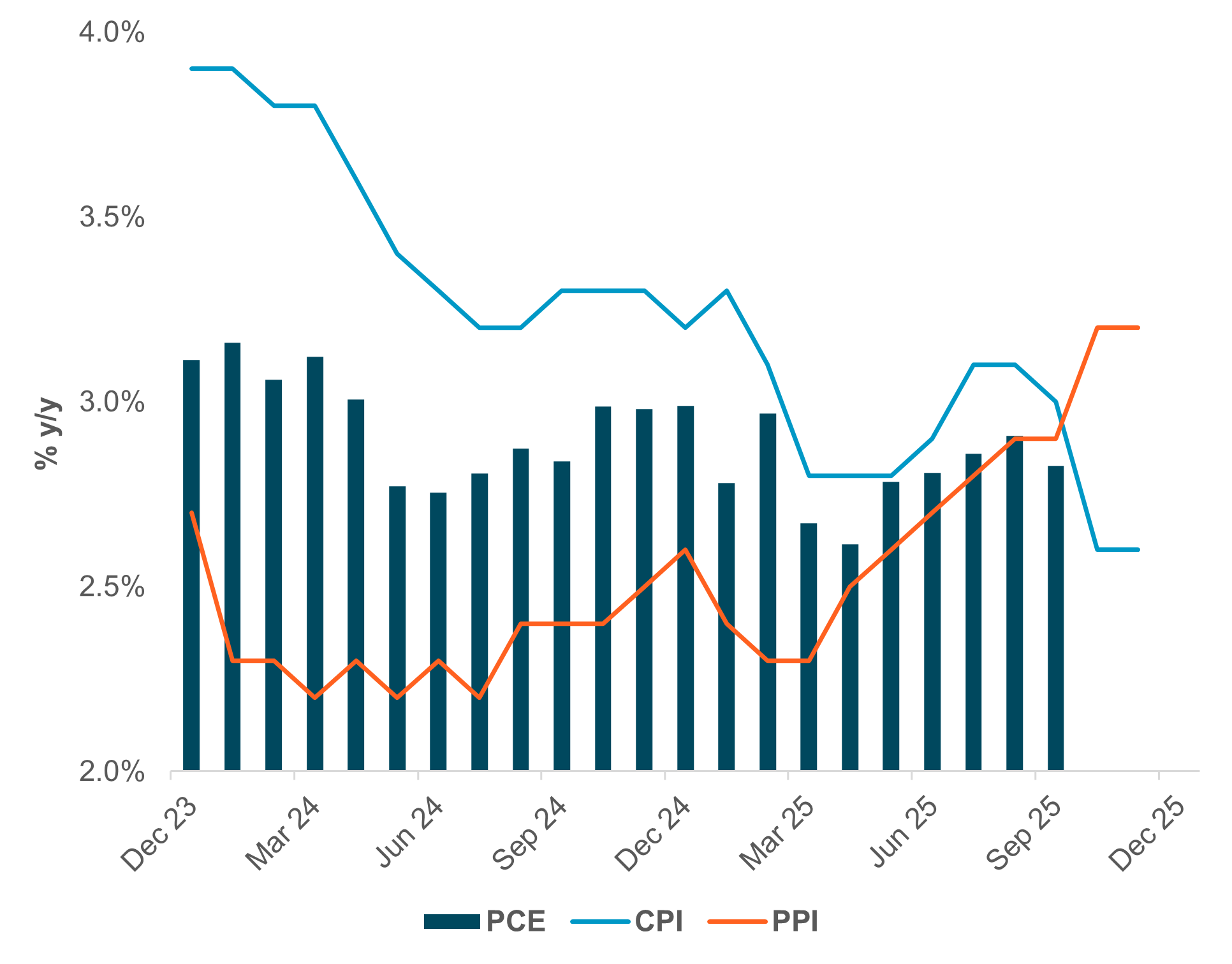

EXHIBIT #2: CORE INFLATION – PPI, CPI AND PCE

Source: BNY, Bloomberg

Our take: Last week, U.S. economic data generally surprised to the upside, reducing market expectations for rate cuts in the 2026 path. Initial claims were particularly encouraging, at least temporarily allaying our concerns about a faster deterioration in the labor market. The Fed’s Beige Book, on the other hand, was more downbeat, with firms reporting flat hiring and few new positions created.

Forward look: This week’s data calendar is somewhat lighter, and FOMC members are in their blackout period ahead of the January 28 meeting, where no rate move is expected. Construction and home sales data (Wednesday) could confirm last week’s signals about housing activity, and on Thursday, the third and final Q3 GDP report is due, which we expect to reinforce the growing prominence of AI-related investment across the economy. The personal consumption data for November will also be published Thursday. Based on earlier CPI and PPI series, a PCE print well above 2.5% is likely, helping provide the Fed with an additional argument not to cut rates at the end of the month.

EMEA: Damage control in Davos as PMIs confirm manufacturing contraction

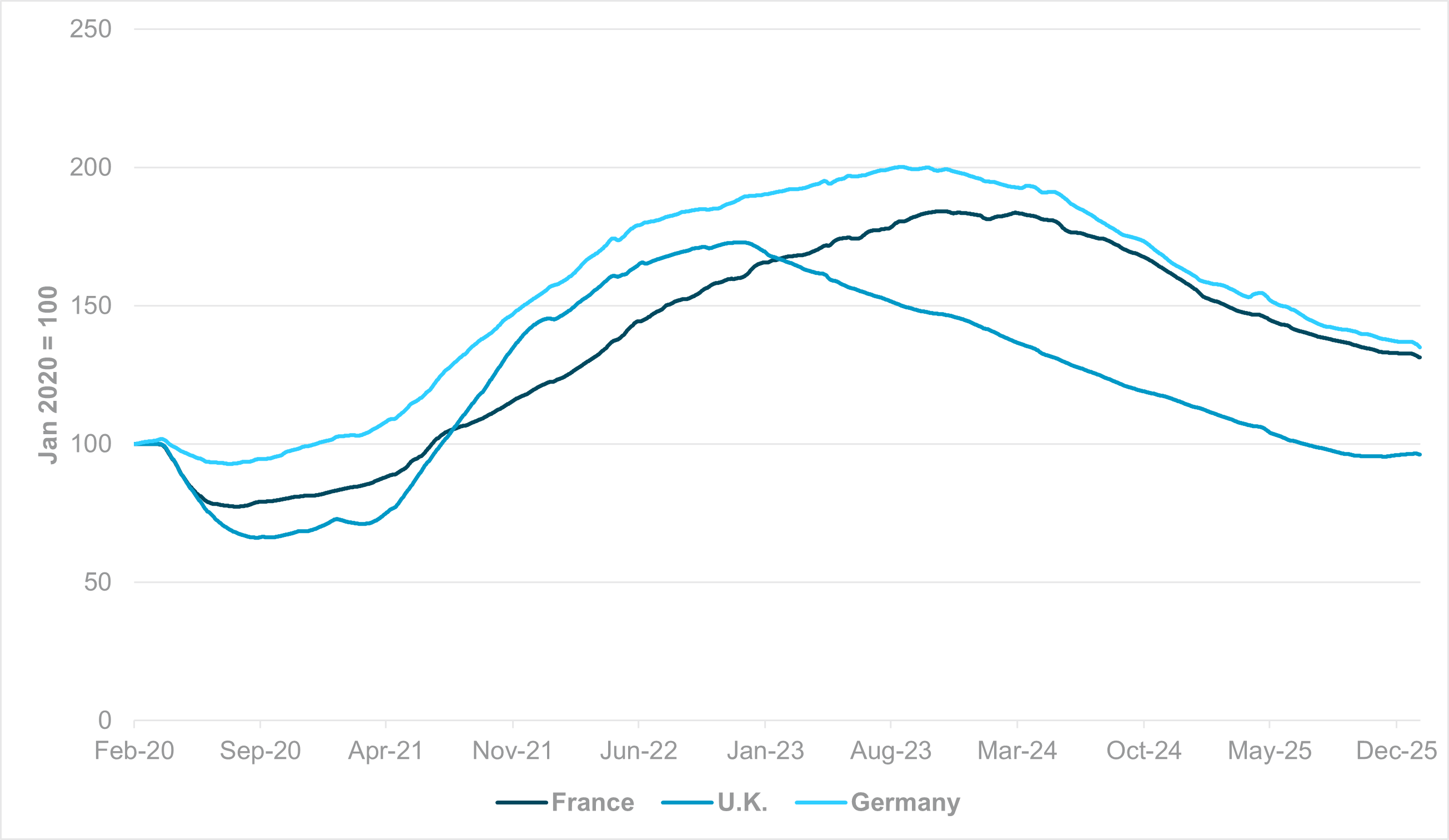

EXHIBIT #3: INDEED TOTAL JOB OPENINGS (SMOOTHED) – FRANCE, U.K. AND GERMANY

Source: BNY

Our take: EMEA remains heavily distracted by geopolitics. As global leaders gather in Davos, including President Trump, Brussels hopes for behind-the-scenes agreements on Ukraine and Greenland, allowing a pivot back to the domestic economy, which continues to face significant challenges. The European Commission’s recent decision to implement price floors with China has likely bought valuable time for European automotive manufacturers, while setting a template for other industries to manage competition with China in a non-confrontational manner. China’s lead trade negotiator, Vice Premier He Lifeng, will lead the delegation – an opportunity to consolidate recent progress.

Nonetheless, upcoming PMI releases will likely confirm that even a price floor cannot fundamentally alter the structural challenges facing European industry, with a knock-on effect on labor markets. Germany’s December PMI noted that “falling export sales … led to deeper cuts to employment, purchasing, and stocks of inputs.” In the coming months, from both a fiscal and monetary standpoint, the state of European labor markets will be critical to the outlook, with signs emerging that conditions may be worsening, despite robust wage growth. The latest high-frequency job openings data in Germany and France (Exhibit #3) continue to indicate a “slow bleed” in job creation.

The U.K. picture looks more problematic, with some dovish Bank of England (BoE) members, including Alan Taylor, already citing these trends as downside risks to the economy and policy. Public spending can only go so far, and the market’s appetite for fiscal dominance in Europe is limited – France’s budget impasse will soon move up the agenda.

We see a strong risk of Europe moving further toward a “more-fire, no-hire” economy given the current trend in openings, and both European Central Bank (ECB) and BoE settings will come under the microscope.

Forward look: Norges Bank and the Central Bank of the Republic of Turkey (TCMB) are the main decisions in the week ahead.

A key test for Norges will be whether it pivots away from further easing from its current 4% deposit rate. More cuts remain priced in and were part of previous policy guidance. NOK was a candidate, along with CAD and AUD, to benefit from any such pivot toward inflation monitoring, but ultimately only the RBA seemed inclined to rule out further cuts. The December inflation prints, which surprised to the upside, suggest that a pivot may still be in play, though domestic conditions point to a more complex picture. Like its larger Western European peers, Norway’s labor market is tight – the seasonally adjusted unemployment rate has fallen to 2.1% – but forward job creation remains a challenge. The country’s new vacancies rate for Q3 2025 has fallen to 2.6%, the second-lowest level since the pandemic, and new vacancies are at cycle lows. Norway can always afford additional fiscal support to cushion household demand, but such action would be stagflationary and not conducive to asset allocation. iFlow notes that NOK holdings have also fallen significantly from the highs, and valuations appear weak. Furthermore, oil prices and associated revenues have not fallen enough to turn Norges into a net FX seller.

TCMB remains a unique case in policy settings, but we estimate that TRY will limit losses and maintain carry interest by keeping real rates to around 5%, especially if the Fed maintains its current outlook. However, we are now closely monitoring the broader carry complex, as nearly high nominal-rate currency in LatAm and EMEA is overheld in iFlow, and conditions are ripe for an adjustment. TRY continues to benefit from real effective exchange rate (REER) strength rather than underlying nominal currency gains, which in turn means fixed income flows will take precedence.

The key data focus will be PMIs, with both Germany (consensus: 48.0) and European manufacturing (consensus: 49.1) expected to show continued contraction, though without clear signs of further deterioration. We remain concerned about the divergence between manufacturing and services, as the latter risks downside correction this year given labor market conditions.

APAC: China activities and investment, regional exports & CPI and BoJ in focus

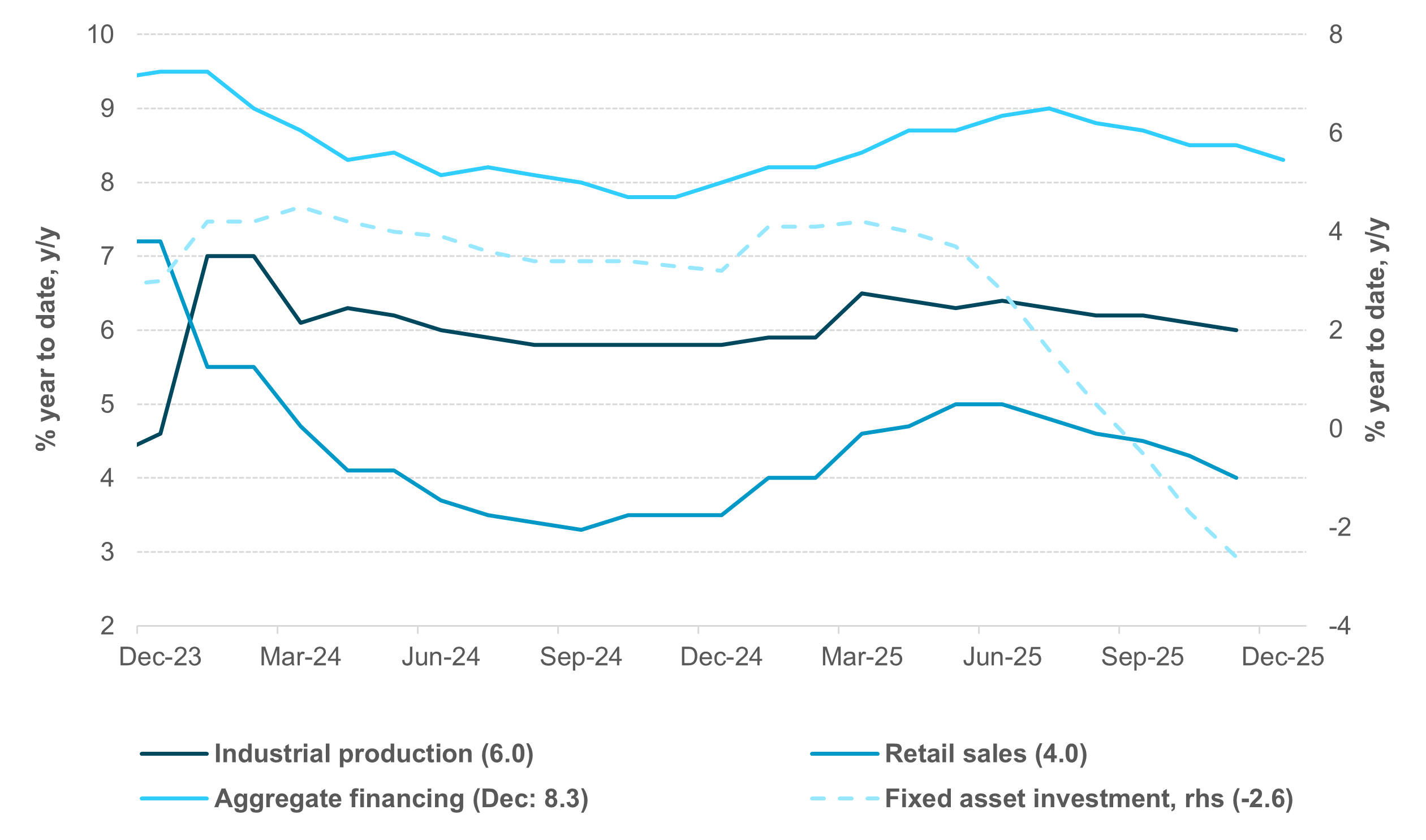

EXHIBIT #4: SLOWING CREDIT AND DETERIORATION OF INVESTMENT AND ACITIVITIES

Source: BNY

Our take: In APAC, attention this week will center on the BoJ policy decision, alongside China’s December activity and investment data, retail sales and home prices. December trade data are due from Taiwan, Malaysia and Japan, as well as South Korean export figures covering the first 1 to 20 days. Inflation figures will be reported by Malaysia, Singapore, New Zealand and Japan, while preliminary manufacturing PMI readings are expected from India, Australia and Japan. Additionally, Australia will release employment data and inflation expectations, while India will publish infrastructure industries growth data. The BoJ remains the focal point among central banking developments, with policy meetings also scheduled for Bank Indonesia (BI) and Bank Negara Malaysia (BNM).

China’s fixed asset investment in November continued to decline, registering –2.6% YTD y/y. Infrastructure investment within the tertiary industries further deteriorated to –1.1%, reaching its lowest level since June 2020. In contrast to traditional sectors, high-tech industries such as industrial robots (+20.6%), new energy vehicles (+17.0%) and integrated circuits (+15.6%) reported robust growth. Regarding domestic consumption, retail sales growth slowed considerably to 1.3% y/y, marking the lowest figure since December 2022, and stood at +4.0% on a YTD y/y basis. Sentiment in the real estate sector remained subdued, with property investment decreasing by –15.9% YTD y/y, close to the record decline of –16.3% YTD y/y observed in February 2020. December housing data are expected to reflect further weakness, with an accelerated decline in both new and existing home prices. In November, new home prices fell –0.39% m/m and –2.78% y/y, respectively, while used homes dropped –0.66% m/m and –5.7% y/y.

Regional exports are showing signs of improvement, supported by China’s stronger-than-expected December export growth of 6.6% y/y, or 5.5% for 2025. November export figures for Malaysia and Japan were 7.0% y/y and 6.1% y/y, respectively, while Taiwan’s export orders rose 39.5% y/y, bolstered by demand for semiconductors. South Korea’s exports for the first 1 to 20 days of the month are expected to return to positive territory, following a decline of –2.3% y/y during the first 1–10 days. Additionally, December CPI data for Singapore and New Zealand, along with Australian employment statistics, will be influential in shaping upcoming monetary policy decisions. The Reserve Bank of New Zealand’s November projections estimate that Q4 2025 CPI will decrease to 2.7%, compared to 3.0% in Q3.

The upcoming BoJ policy meeting will attract significant attention within the central banking sector. Markets will watch for both its customary statements on rate hikes tied to economic conditions and any signals about the timing of future policy adjustments amid ongoing currency and bond market volatility and prevailing political uncertainty. Additionally, BNM and BI are scheduled to meet, with both institutions anticipated to maintain current interest rates. Market participants are expected to closely monitor BI’s approach following the rupiah’s decline to historic lows last week.

Forward look: The positive risk-on sentiment experienced earlier was disrupted last week by increasing geopolitical uncertainties and a stronger USD, which offset the optimism surrounding the semiconductor and AI-related sectors. TSMC’s robust Q4 results, along with projections of near 30% sales growth by 2026 and capital expenditures estimated between $52bn and $56bn, show resilient and structural demand within the sector. We maintain a constructive outlook for the APAC market while recognizing ongoing market volatility.

The RMB continues to trade positively, despite minor disruptions following the elimination of margin trading. China implemented a 100% margin financing ratio on its stock exchanges, supported by readiness to deploy policy measures. Last week, China introduced several supportive initiatives effective January 19, including a 25bp reduction in interest rates on relending facilities (to 0.95% for three-month and 1.25% for 1y terms), a rediscount rate of 1.5%, a Pledged Supplementary Lending (PSL) rate of 1.75%, and rates of 1.25% on special structural monetary policy instruments. Additionally, relending quotas have been increased to support agriculture, small businesses, scientific and technological innovation, and the promotion of the green economy. Our constructive stance on the yuan remains unchanged.

Elsewhere in the region, performance has varied, with currencies from deficit-ridden countries or those facing fiscal concerns – such as PHP, KRW, INR and JPY –underperforming their peers. Close monitoring is advised for potential downside valuations in IDR, KRW and TWD compared to the elevated valuations in THB. Looking ahead, the India Union Budget (February 1) and Thailand general election (February 8) are immediate focal points, along with a possible election in Japan, prior to China’s 14th National People’s Congress (NPC) and the Chinese People’s Political Consultative Conference (CPPCC), which are scheduled for March 4 and 5.

As 2026 unfolds, markets are transitioning from momentum-driven certainty toward a more complex regime defined by rotation, policy risk, and uneven growth. Early-year signals point to declining investor conviction, with patience replacing FOMO and volatility becoming the price of prospective equity returns. The shift away from mega-cap technology toward small caps, housing-linked assets, and industrial inputs reflects both valuation discipline and expectations that policy levers – fiscal, monetary and regulatory – will be pulled aggressively ahead of the U.S. midterm elections.

Against this backdrop, macro risk is increasingly multi-dimensional. Central banks face sticky inflation and resilient activity, limiting their flexibility just as geopolitical tensions intensify across multiple regions. Currency and rates markets, which have remained relatively calm, appear vulnerable to feedback loops stemming from Japan policy risk, U.S. deficit concerns, and shifting global capital flows.

Meanwhile, AI remains a structural growth engine, but 2026 will test the sustainability of funding models, power costs, and talent constraints as deployment moves from hype to execution. Regionally, Europe grapples with structural labor and manufacturing headwinds, while APAC balances China stabilization efforts against currency and policy volatility. Taken together, the investment environment favors active risk management, relative-value positioning, and heightened sensitivity to policy transmission across assets.

Central bank decisions

Indonesia, Bank Indonesia (Wednesday, January 21): We expect that BI will leave its policy rate unchanged at 4.75%, maintaining an easing stance. The central focus should remain on improving the credit and interest rate transmission mechanism. Over the past month, average lending rates in Indonesia remained elevated above 14%. The central bank is expected to reinforce its “all-out pro-growth” messaging or signal it will assess further scope to lower interest rates, while continuing its triple intervention strategy – acting in spot FX, domestic DNDF, government bonds, and offshore IDR markets to stabilize FX.

Malaysia, Bank Negara Malaysia (Thursday, January 22): We expect BNM to keep rates unchanged at 2.75% and maintain an upbeat assessment for the year, supported by GDP growth momentum and a stable inflation profile. Our view is that BNM is done with easing measures and is unlikely to follow the Federal Reserve’s easing path.

Norway, Norges Bank (Thursday, January 22): No change is expected, but markets appear unwilling to fully price out further rate cuts, despite signs that inflation will not decline soon after upside surprises in the December prints. The labor market also remains relatively tight, with upside risks to wage growth. On the other hand, limited follow-through in the supposed ECB pivot has reduced the case for Norges to shift its bias, so we expect caution to prevail for now.

Turkey, Central Bank of the Republic of Turkey (Thursday, January 22): The market is looking for an additional 150bp in cuts from the TCMB as daylight is emerging between nominal rates and the inflation outlook. There is scope for TRY to hold on to real rates of about 5pp, and as the market remains in a relatively robust position with respect to carry trades, TRY flows will be well-anchored. The current inflation run-rate leaves sufficient space for slightly larger cuts. However, we do not expect cuts closer to 200bp, given that the dollar’s outlook is still not sufficiently dovish to support additions to carry interest.

Japan, Bank of Japan (Friday, January 23): The BoJ is not expected to change policy settings, and any key decisions will likely be on hold as the country gears up for a snap lower-house election. Parliament is expected to be dissolved on the same day, and the unification of the main opposition parties has also altered the country’s political landscape. Either way, the recent shift in language around Japanese lawmakers’ tolerance for JPY weakness suggests limits have been reached, and Governor Kazuo Ueda will need to elaborate on managing the associated risks.

Source: BNY

Source: BNY