Chasing spirit animals

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 9 minutes

Markets have been chasing spirit animals as June opens with the familiar tension between inflation and growth. Beyond bulls and bears, the hope for geopolitical solutions – whether an Iran deal and a Strait of Hormuz reopening or an end to the four-year Russia–Ukraine war – has been pushed aside in light of the grim economic data on growth, from Canada’s technical recession to the risk of one in Europe. Stronger U.S. data – from ISM to jobs – and a hawkish tilt from Fed speakers leave higher growth and higher rates as the driver of U.S. exceptionalism. USD hedging and H1 2026 rebalancing will both face a reckoning. The AI-drives-everything narrative frayed last week. The SpaceX IPO and Alphabet equity offering raise a harder question: will markets make room through rotation, cash drain, or something else entirely?

In focus for the week:

What else could matter in the week ahead?

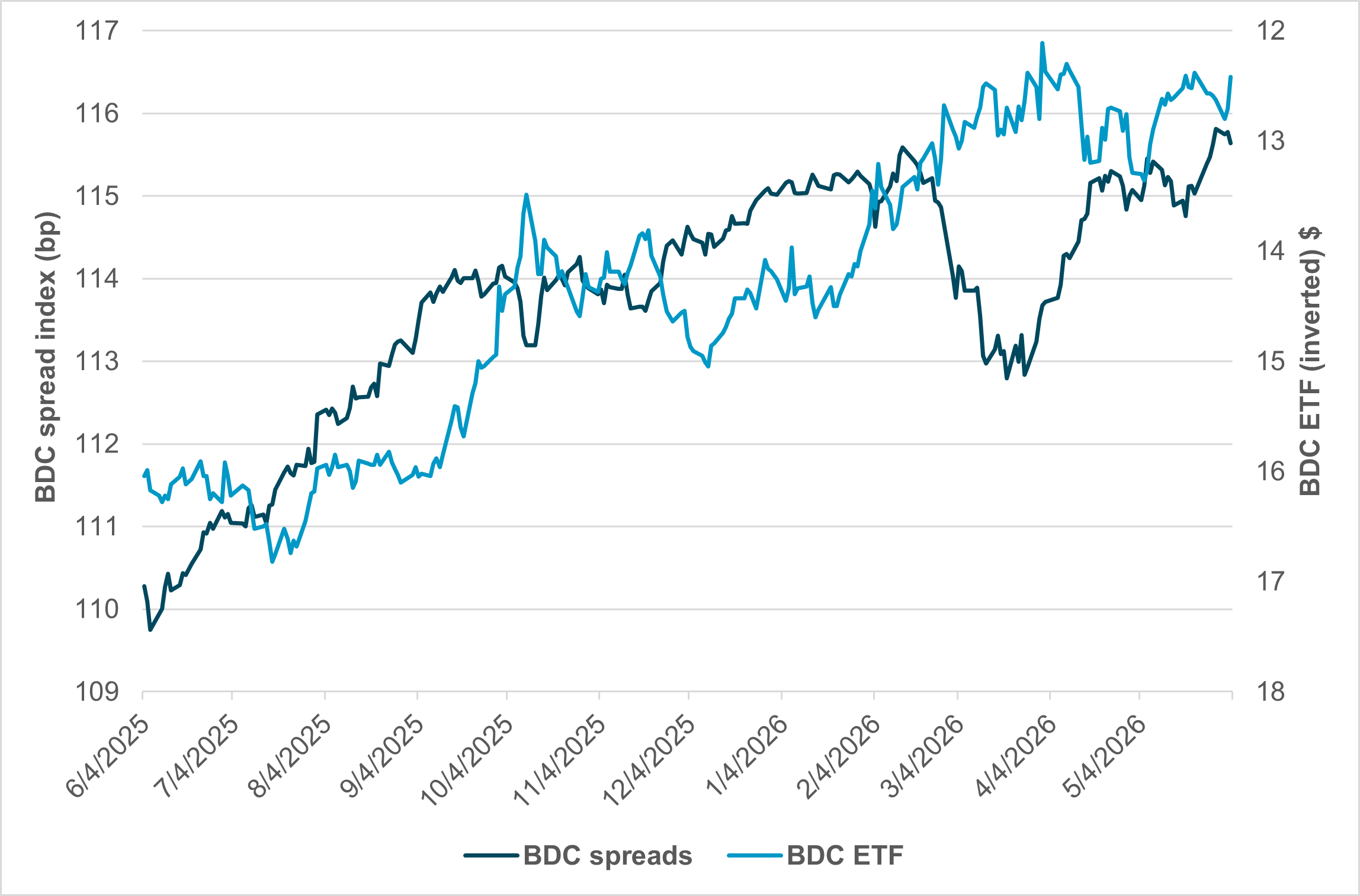

EXHIBIT #1: PRIVATE CREDIT SPREADS VS. BDC EQUITY

Source: BNY, Bloomberg

Our take: The return of private credit concerns in the last week came with Partners Group and gating of redemptions. This concern coupled with higher interest rates globally stands out as a driver for using credit spreads as a barometer for risk. Pressure on private credit firms (BDC ETF) and their credit spreads tend to move together, but there are moments of divergence – typically around larger risk-on or risk-off episodes, as we saw at the peak of the U.S.–Iran conflict. The moves from last week are different and reflect a shift in Fed policy outlooks.

Forward look: The last week saw over $50bn in IG issuance. We also saw two large IPO plans come to market – SpaceX and plans for Anthropic. Liquidity needs for borrowing money will be an important part of the week ahead as it plays against asset allocation and rotation pressures for investors as they think about rebalancing. The role of private equity and IPOs will add to the focus on Fed policy. As we shift from oil and the USD as the risk barometer for markets, credit spreads in BDC and AI will likely return to focus similar to October 2025.

North America: Inflation not growth

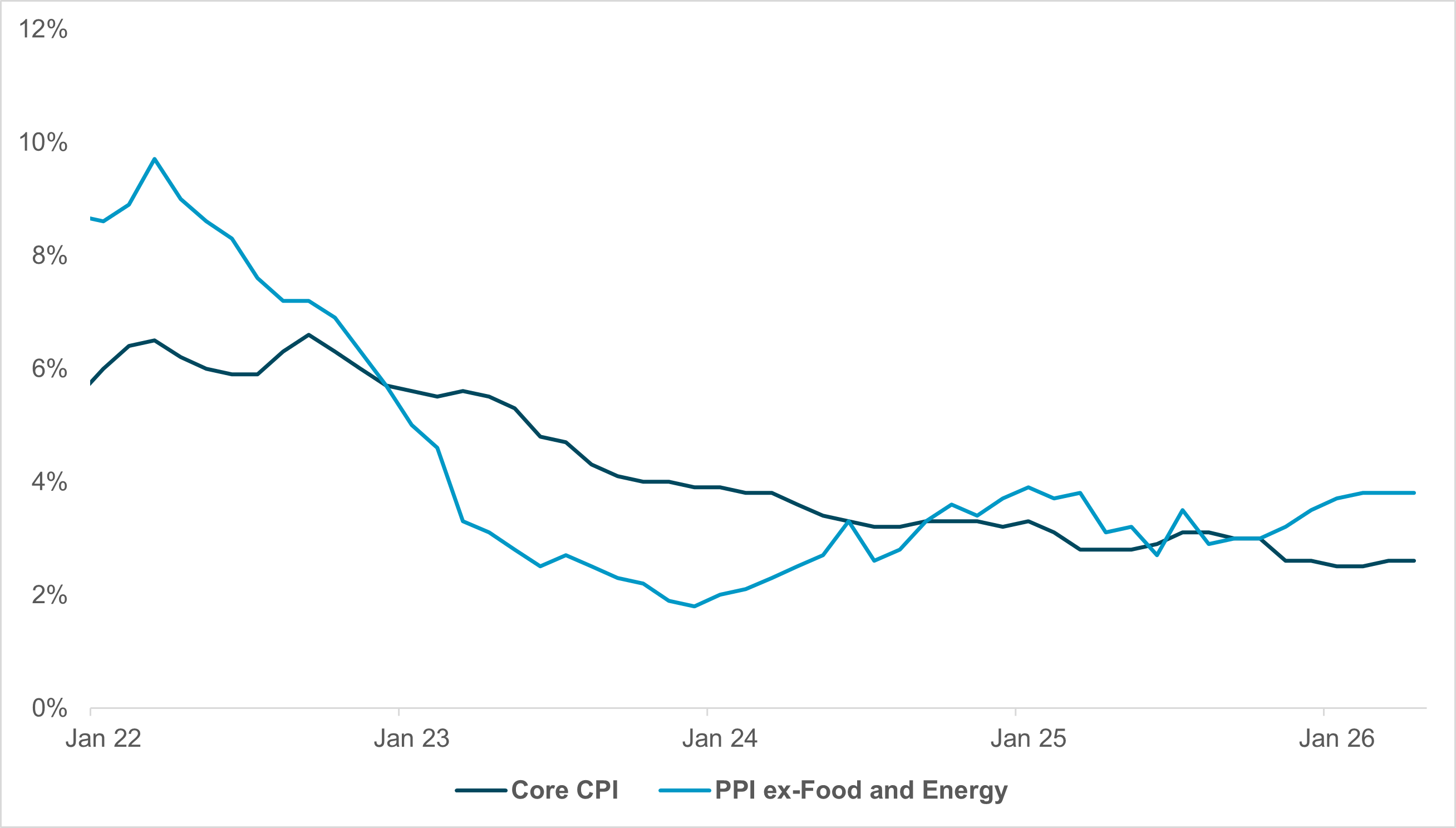

EXHIBIT #2: U.S. CPI CORE VS. PPI CORE

Source: BNY, Bloomberg

Our take: Last week’s data painted a picture of a resilient U.S. economy with the standout being a blowout nonfarm payrolls report that pushed markets to fully price in a Fed rate hike by year end. The 172,000 m/m growth in payrolls beat the consensus estimate of 88,000, while unemployment remained steady.

All this leaves inflation as the key macro variable to watch this week. To that end, U.S. CPI on Wednesday will dominate market attention, followed by PPI on Thursday and the University of Michigan sentiment survey on Friday. The Fed is in its communications blackout, so there should be little in the way of fresh policy guidance from officials.

The BOC meets on Wednesday against a softer growth backdrop, with the economy now in a technical recession notwithstanding the strong labor report, making the policy decision more noteworthy than usual.

Forward look: Of the week’s releases, CPI is clearly the most important for rates markets and Fed pricing. After last week’s strong labor data, another upside surprise on inflation would reinforce the view that growth remains resilient enough to force the Fed’s hand. PPI will matter mainly insofar as it confirms or challenges the CPI signal, while Michigan sentiment will be a useful read on consumer resilience rather than a primary market driver.

The BOC is widely expected to remain on hold, but the tone of the statement and any discussion of recession risks will matter for the CAD and Canadian rates. Canada’s labor report also beat expectations. For markets, the key question is whether CPI confirms the recent hawkish repricing or creates room for some reversal.

EMEA: Don’t forget growth

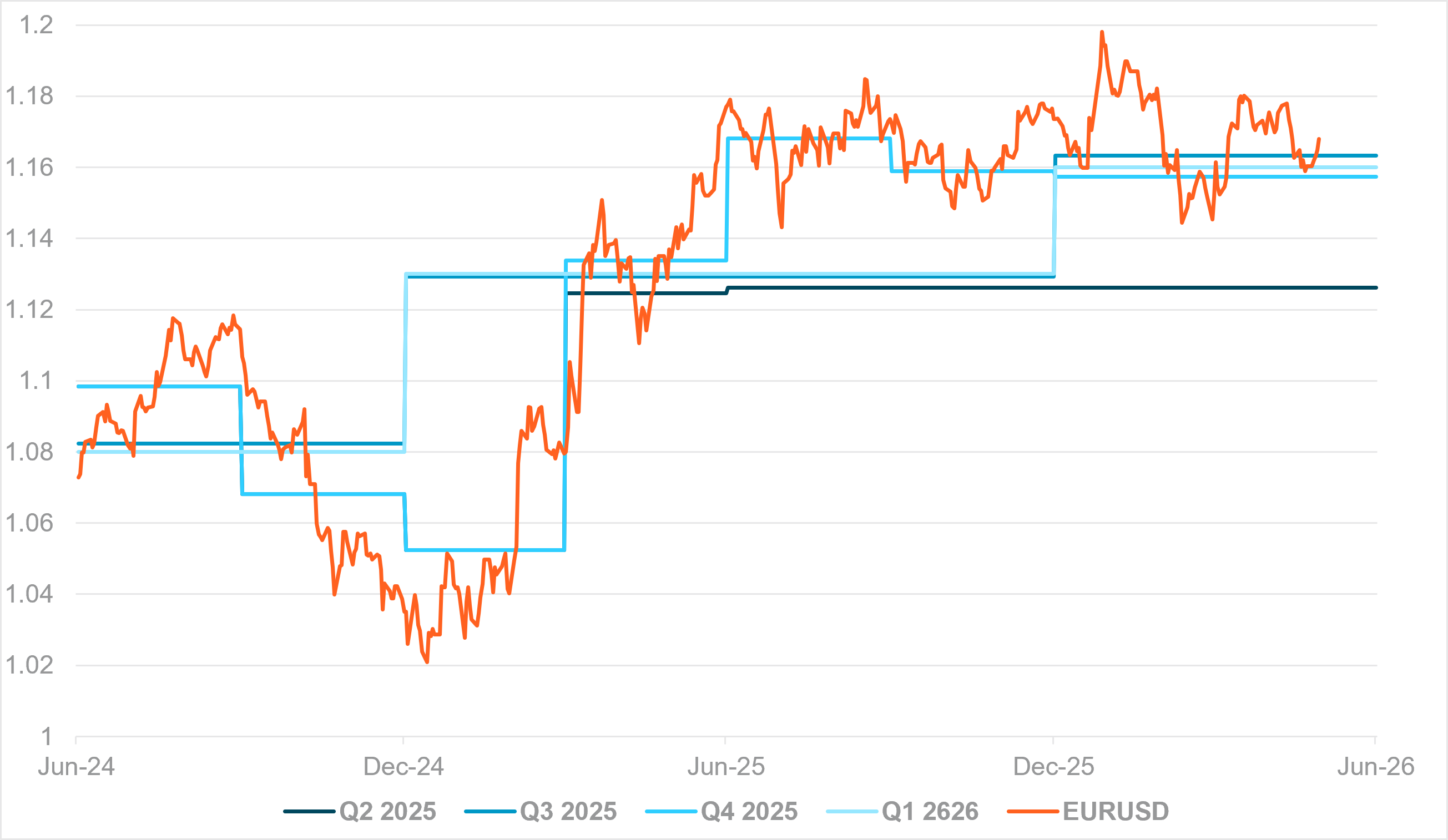

EXHIBIT #3: EURUSD HAS STOPPED UNDERPERFORMING THE ECB’S PROJECTIONS

Source: BNY

Our take: An ECB hike on Thursday is considered a foregone conclusion but uncertainty remains regarding what happens next. For now, we believe the “don’t forget growth” message is strong enough (at least behind closed doors) such that the Governing Council will not be able to commit to a prolonged cycle for now, and that would already risk some downside risk in the euro: any increase in exposures which solely responded to the wide gap between ECB expectations versus peers would require some moderation.

For communication clarity, we believe the ECB will need to state where the economy stands relative to its scenario analysis and whether policy will be reactive or pre-emptive. We expect President Christine Lagarde to stress policy “uncertainty.” But if the gap between current conditions and the “severe scenario” – which would have pushed HICP through 6% – proves insufficient to justify restraint, markets may begin to price out further hikes. At present, it’s doubtful whether the 4% peak in both HICP and wage growth in the “adverse scenario” is attainable, which argues against overreaction. Hawkish members should not cite euro support as the justification for further hikes. Compared to 2025, we note that the ECB is no longer playing “catch-up” to the EUR’s performance, as the currency is now trading around the levels anticipated in its past three Staff Projections (Exhibit 3). This means negligible impact either way, and the ECB should note that the recent surge in hawkish pricing has not supported the currency, both in terms of levels and also positioning – the currency remains underheld in iFlow.

Tightening pre-emptively to restrain the economy is sufficient, and FX dynamics for the Eurozone in the context of financial conditions is very different compared to the situation in economies like India and Indonesia. If anything, a modestly weaker EUR is probably desirable to help exporters.

Forward look: European inflation prints feature prominently, and we expect confirmation that most of the sequential prints for Western European economies showed no incremental growth in prices in May. Given expectations for immediate pass-through in prices were relatively high beforehand, this is a surprisingly mild outcome and supports our view that demand restraint is taking hold in Europe. The ultimate determinant for second-round effects remains in core inflation and, crucially, wages. Based on the U.K.’s latest decision-making panel survey, 24% of companies expect some pass-through into wages as a direct consequence of the conflict, but headline wage growth is not expected to rebound strongly as there’s still an offset in the form of a loosening labor market. If similar trends arise in the Eurozone, it will also dampen calls for more proactive tightening as well. Otherwise, it’s a relatively quiet week for event risk aside from the ECB decision, though we’re monitoring the Russian response to Ukrainian President Volodymyr Zelenskyy’s call for direct peace talks. An EU-led push for direct contact is underway, and any breakthrough would meaningfully compress risk premia in Europe.

APAC: China activity, South Korea exports and regional sentiment

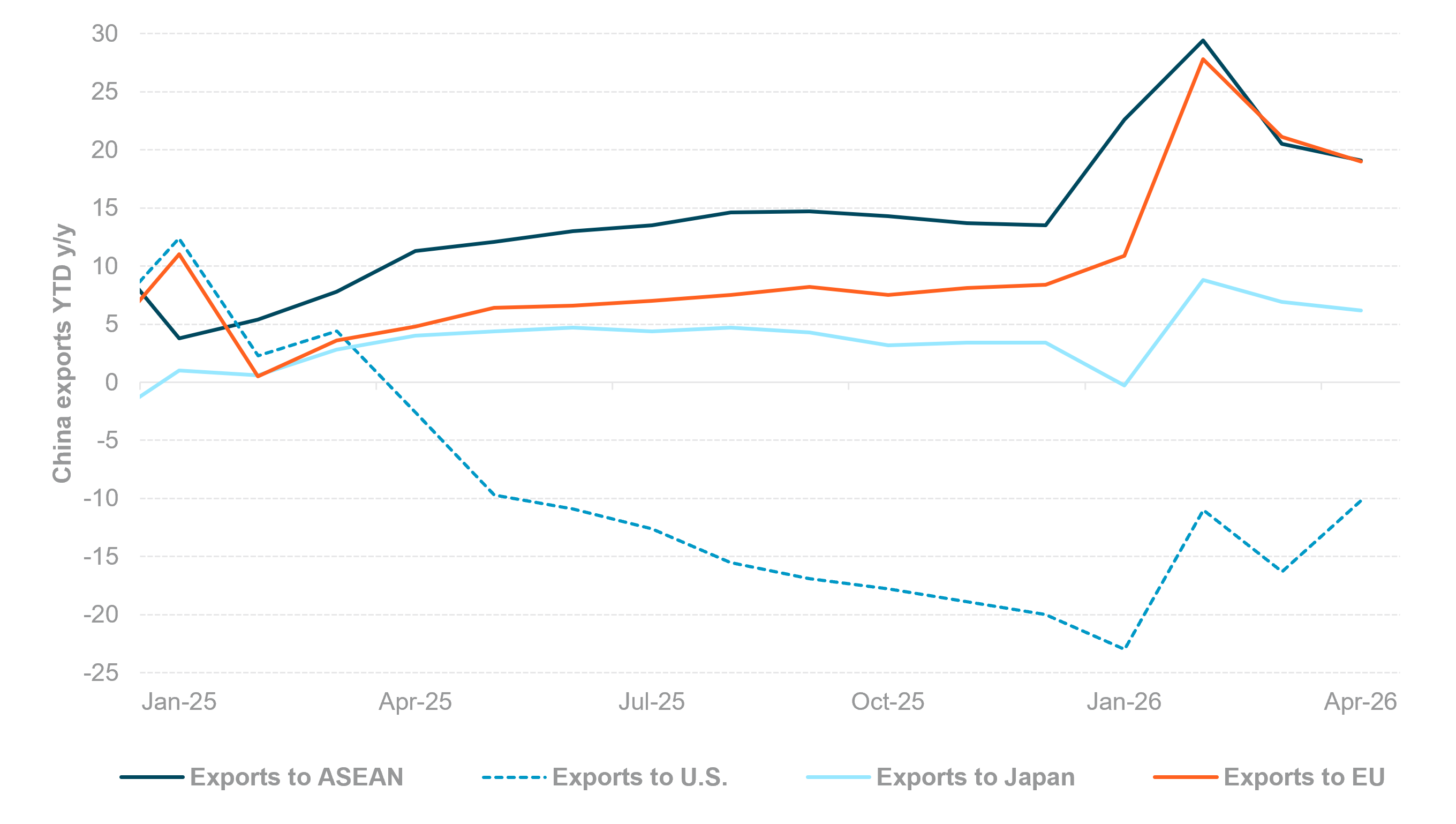

EXHIBIT #4: CHINA EXPORTS TO U.S. LAGGED THE REST OF THE WORLD

Source: BNY, Bloomberg

Our take: Asia’s macro calendar will be led by China’s May activity and price data, with exports, CPI/PPI and credit aggregates (new yuan loans, aggregate financing and M2) providing the clearest read on the balance between external demand, domestic activity and policy transmission. Trade data will be closely watched given ongoing tariff uncertainty and export front-loading dynamics, while inflation and credit figures will help gauge whether recent policy support is gaining traction. India’s May CPI and April current account balance will also be key for rates and FX markets, while Taiwan’s export data will offer another timely signal on global technology demand.

Elsewhere, attention will turn to growth and trade indicators across the region. South Korea releases Q1 GDP, labor market data, bank lending figures and the first 10 days of June exports, providing an early snapshot of external demand momentum. Japan’s final Q1 GDP, PPI, bank lending, Eco Watchers survey and the Q2 Business Sentiment Survey will be important for assessing the domestic recovery and BOJ normalization prospects.

In Southeast Asia, Malaysia’s industrial production, the Philippines’ unemployment rate, Thailand’s consumer confidence, Indonesia’s consumer confidence, and Singapore’s foreign reserves will help round out the regional picture.

Markets will also focus on Australian consumer and business sentiment indicators alongside inflation expectations, while New Zealand’s Q1 manufacturing volume and May PMI will provide an update on the pace of economic recovery.

Forward look: Sentiment across Asia deteriorated sharply, led by aggressive selloffs in South Korean and Indonesian assets. The KOSPI fell 3.7% w/w, while USDKRW broke through the key 1,500 resistance level and closed at 1538 (+2.2% w/w). In Indonesia, the JCI plunged 9% and USDIDR breached the psychologically important 18,000 level, driven by sustained foreign equity outflows and a collapse in confidence amid renewed concerns over Bank Indonesia’s independence.

In contrast, the Indian rupee and Philippine peso outperformed on idiosyncratic factors. The rupee was supported by a series of financial reforms, including further liberalization of foreign investment into India government bonds and equities, alongside tax exemptions on interest income from government securities and capital gains. The peso remained supported by aggressive FX smoothing operations and official warnings against speculative positioning, helping to cap USDPHP near 61.75. While these measures have proved effective in the near term, their durability is less certain against a backdrop of weakening regional market confidence.

With little sign of relief from a stronger U.S. dollar or elevated crude oil prices, risks are rising that depreciation expectations become unanchored, triggering further capitulation in ASEAN equity and FX markets. The Chinese yuan has remained remarkably stable and continues to serve as a regional anchor. We will be closely monitoring whether the RMB’s divergence from regional peers persists beyond key support around 6.713. Any meaningful RMB correction could amplify pressure across Asian currencies and risk assets. With no APAC central bank meetings this week, attention is already turning to next week’s policy decisions, particularly in Indonesia and the Philippines.

Looking ahead, markets appear poised for a critical transition from geopolitical headline trading toward a more fundamental assessment of inflation persistence, liquidity conditions, and growth resilience. The upcoming U.S. CPI report may prove decisive in determining whether investors continue to price a more hawkish Federal Reserve or begin to reassess the probability of further tightening. In Europe, the ECB’s expected rate hike will be less important than guidance around future policy actions and the balance between inflation control and weakening growth. Across Asia, investor confidence remains fragile as currency pressures intensify and concerns about capital outflows persist, particularly in Indonesia and South Korea.

The AI-driven equity rally faces its own test. Large IPOs, equity offerings, and private credit stresses compete for scarce liquidity. Collectively, these developments suggest markets may remain volatile through the remainder of June, with inflation data, credit spreads, and liquidity indicators emerging as the most important signals for asset allocation decisions.

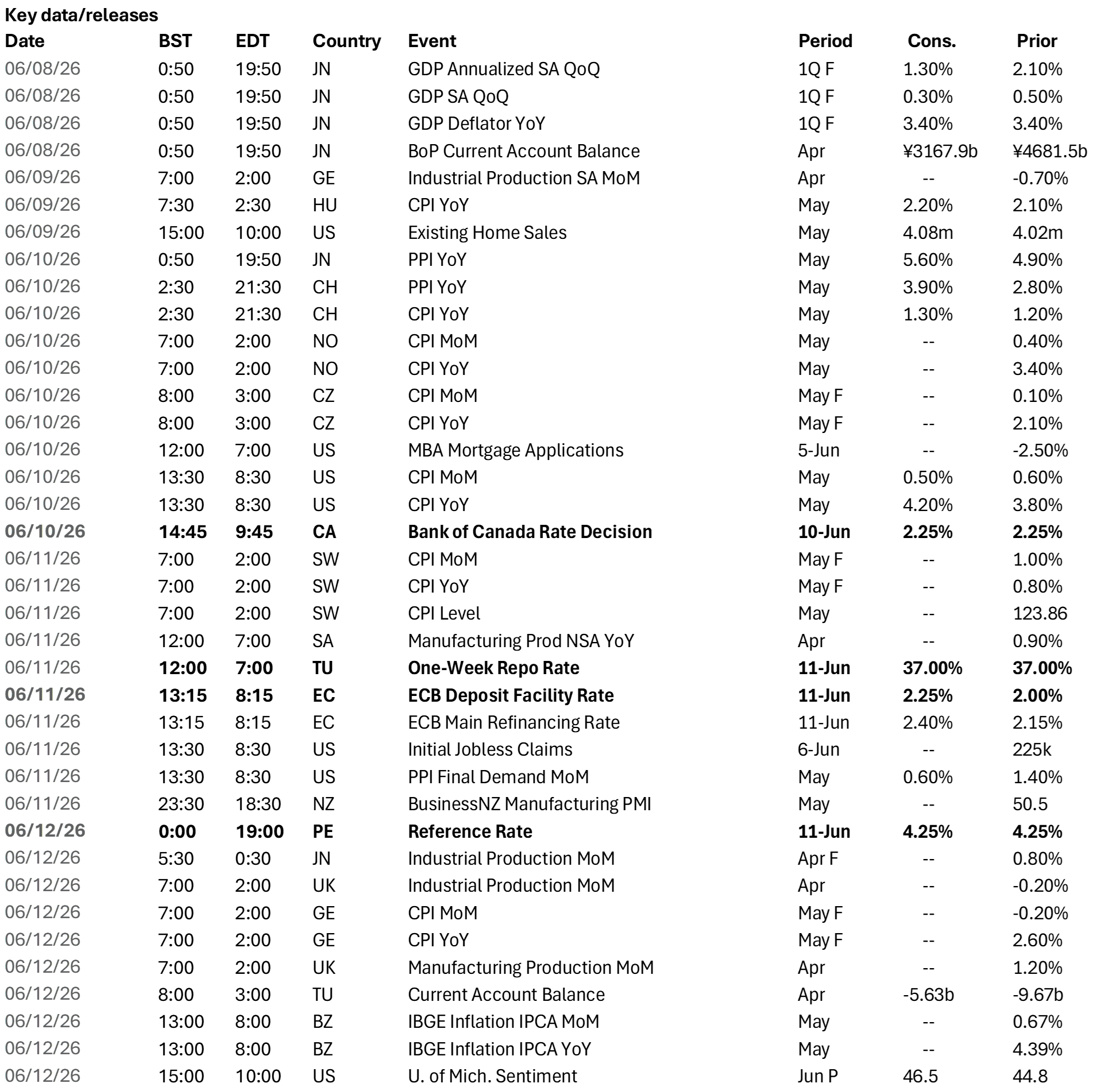

Central bank decisions

Canada, Bank of Canada (Wednesday, June 10): The BOC is expected to hold rates at 2.25%, and prospects for a rate hike in the near term are minimal with the country in a technical recession. The current run of downside data surprises should temper hawkish expectations, a point the Governor will likely address at the post-decision press conference. With Fed pricing potentially moving in the opposite direction and difficult trade negotiations looming, the CAD will likely remain under pressure.

Turkey, Türkiye Cumhuriyet Merkez Bankası (Thursday, June 11): The TCMB is expected to keep rates unchanged at 37%, which may leave many parts of the market disappointed given the current pressure on the currency and broader balance of payments. iFlow points to material weakness in the financial account, and the currency will likely be one of the leading high yielders to shift into underheld territory. Domestic factors aside, pushing up real rates will help address outflows and reserve liquidation.

Eurozone, European Central Bank (Thursday, June 11): The ECB is widely expected to hike rates to 2.25% to address rising inflation expectations, even though we believe that the risks to growth from such a move are perhaps underappreciated. A key point of contention that President Lagarde will need to address at her press conference is whether the hike is precautionary or marks the beginning of a new cycle. The scale of dissent will also shape market pricing for the rest of the year.

Peru, Banco Central de Reserva del Perú (Thursday, June 11): No change is expected by the BCRP, but market scrutiny over the sustainability of current policy positions across LatAm is also growing as supply pressures begin to spread. Since the decision follows the second round of the presidential election, flows will likely focus on future policy direction rather than immediate factors, especially with sequential inflation manageable for now.

Source: BNY

Source: BNY