Ceasefire gives growth another chance

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 10 minutes

Last week’s 13 central bank decisions, the signing of an MOU for a 60-day ceasefire and path toward a U.S.–Iran peace deal, and the continued rally in risk assets globally defined a week in which the G7 focused on geopolitical issues from Iran, Russia and China to AI governance. This was a week that shifted the narrative from fears of an energy shock to one of investment and growth. AI valuations and credit spreads returned to the top of investors’ list of concerns.

In focus this week:

For a global macro portfolio, the most important question next week is whether markets continue rotating from the war/inflation narrative back toward the growth/AI narrative, which should support higher equities, tighter credit spreads, and cyclical assets over defensive positioning. Much of this is already priced into risk assets, but given the list above, copper, oil, gold, USD and the U.S. rate curve all bear watching – each could shift quickly under the rebalancing pressure of month- and quarter-end.

What else could matter in the week ahead?

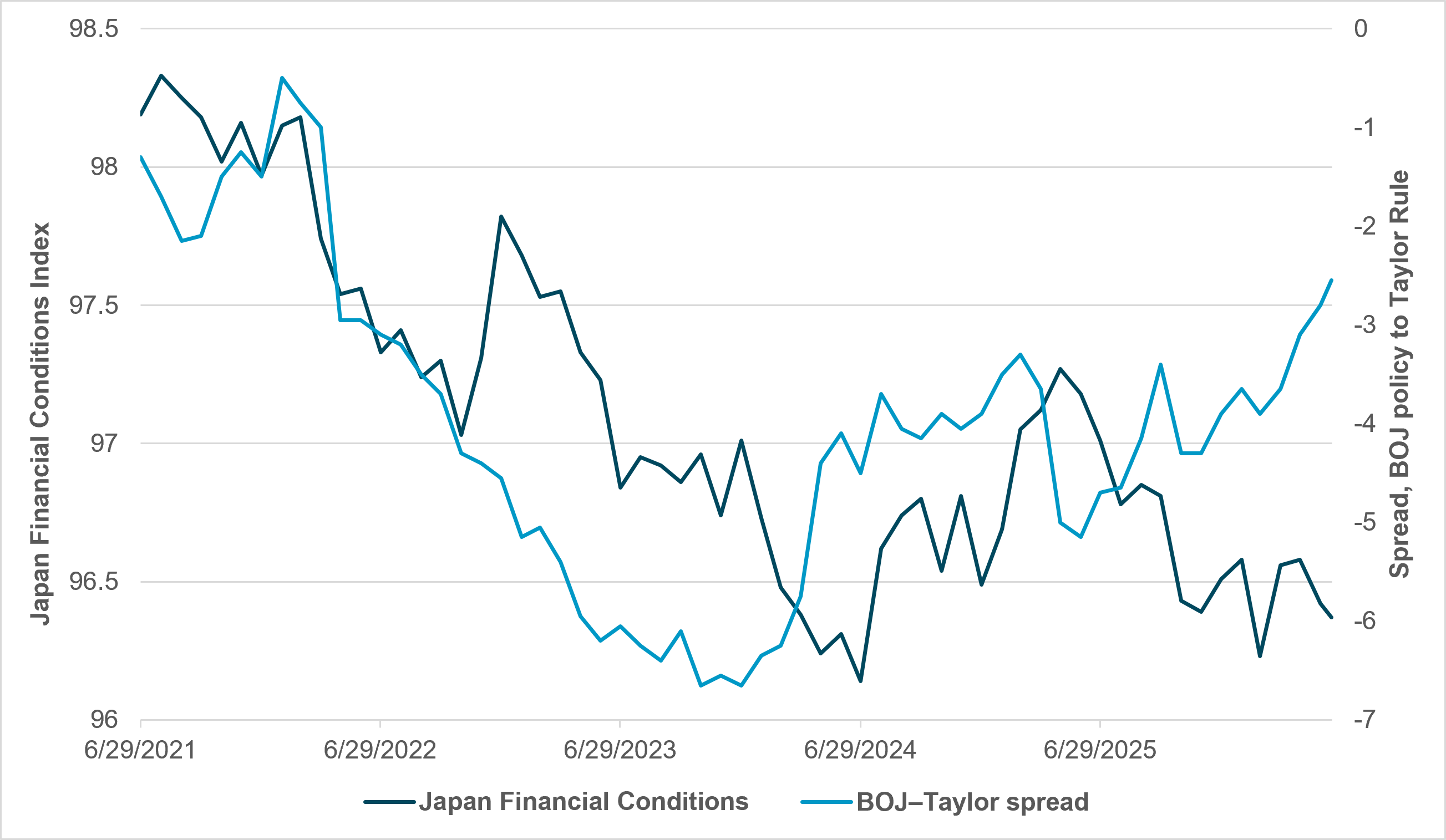

EXHIBIT #1: BOJ POLICY AND TIGHTENING FINANCIAL CONDITIONS

Source: BNY, Bloomberg

Our take: The Bank of Japan (BOJ) is still behind the Taylor model in rate normalization. The key Tokyo CPI data this week will be watched closely for signals on how urgent the BOJ’s rate hiking cycle needs to be. The last meeting was not hawkish enough to keep the JGB curve from steepening, with 10y rates at 2.59% and 2y rates nearly flat at 1.24%. The risk-reward for investors remains: long Nikkei, flat bonds and weak JPY. Japan’s financial conditions appear to matter more to the rest of the world than they do in Japan itself.

Forward look: JGB yields have been shifting their role as a global benchmark for rates since 2025. Japan could see more volatility in rates and in FX. The government’s plans to cut consumption taxes on food from 8% to 1% will be a key test for markets this week and will likely add to focus on rates globally. Strained government budgets are not unique to Japan, but bringing money home to fill the funding gap is. Japan is likely to export tighter financial conditions and may have to intervene in JPY to cap further inflation risks.

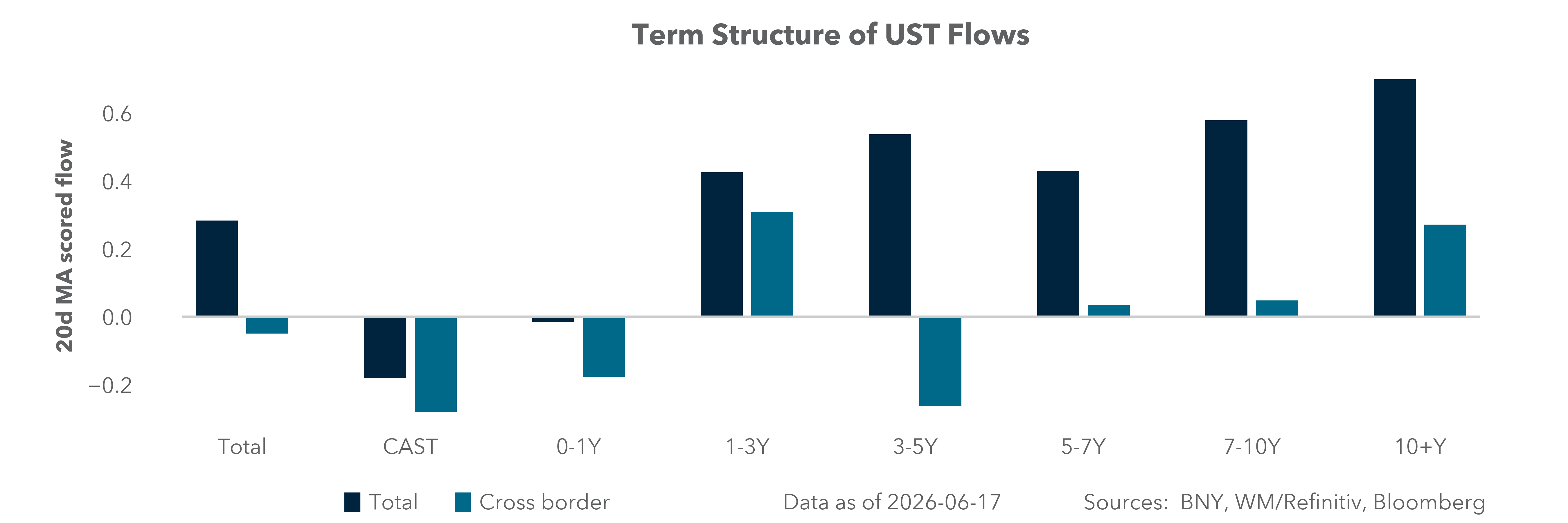

North America: Inflation data after hawkish Fed tilt

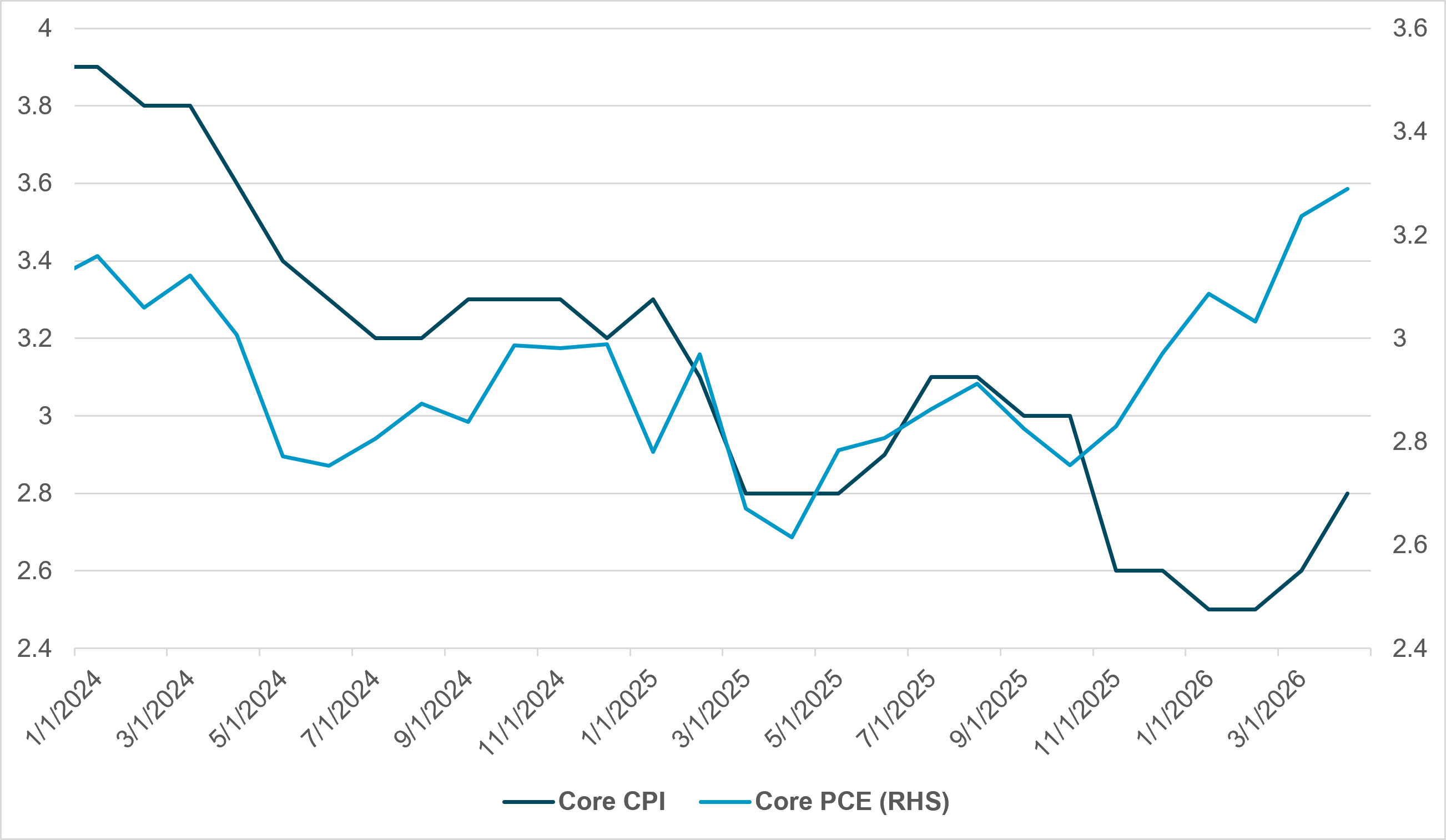

EXHIBIT #2: U.S. Y/Y INFLATION’S UPWARD TRAJECTORY

Source: BNY, Bloomberg

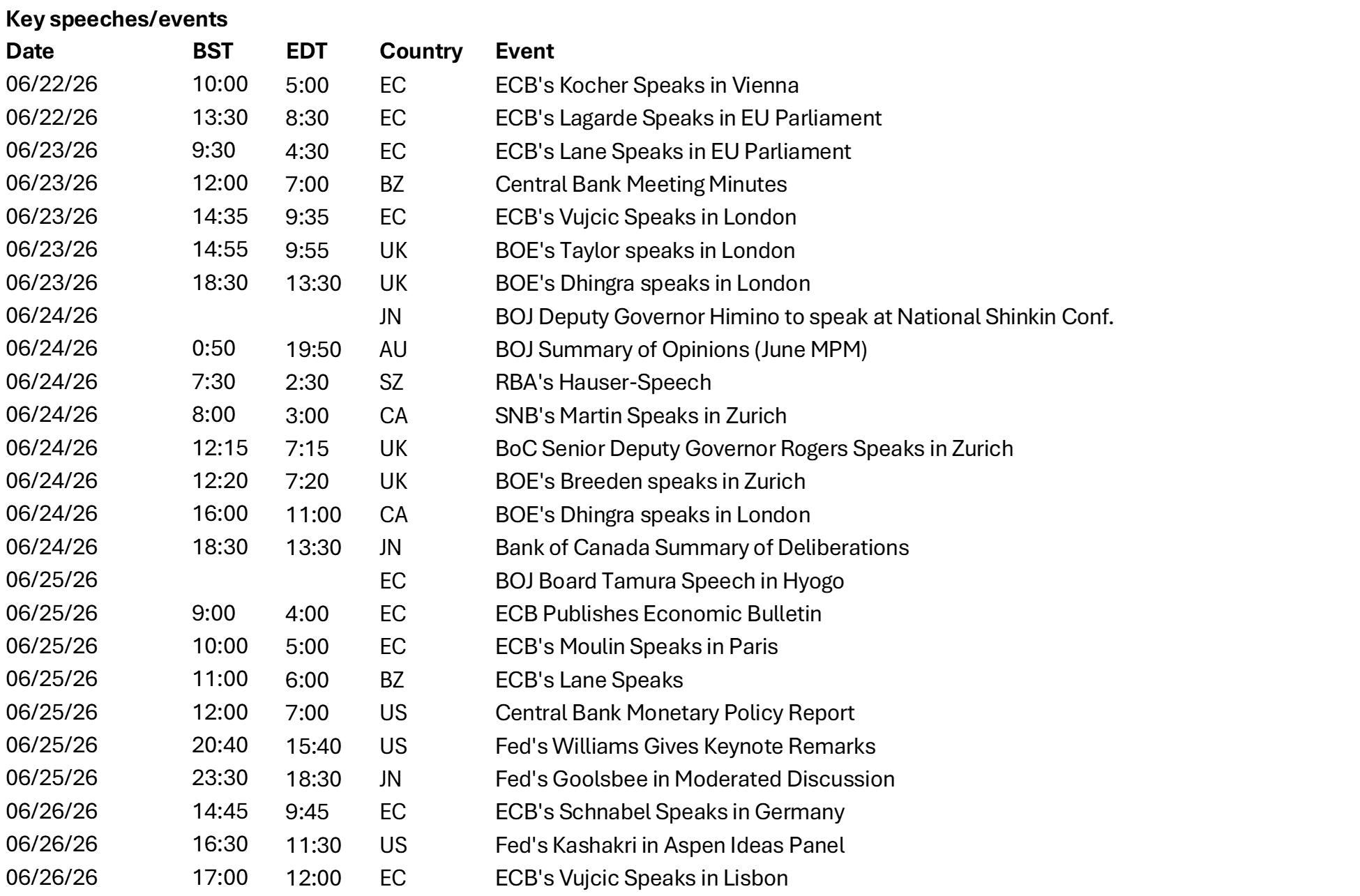

Our take: Markets read Chair Kevin Warsh’s first FOMC meeting last week as hawkish, focusing on both the tone of the statement and the early signs of a more active reform agenda, including the announcement of five task forces. This week’s calendar should help determine whether that repricing has more room to run.

In the U.S., Thursday’s PCE is the clear focal point, with consensus looking for a hot 0.5% m/m headline print versus 0.4% last month and an expected 0.3% core print versus 0.2% last month. GDP and the University of Michigan Consumer Sentiment survey will round out the week, while Fed speakers John Williams, Austan Goolsbee and Neel Kashkari are likely to be watched closely for a read-through on the meeting, commentary on the task forces or broader institutional changes.

Canada’s CPI comes out on Monday, with consensus expectations at 3.0% y/y versus 2.8% last month, alongside appearances by Bank of Canada (BOC) Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers.

Forward look: The most important data point is Thursday’s U.S. PCE, since a stronger-than-expected print would reinforce the market’s hawkish interpretation of Warsh’s first meeting and keep upward pressure on front-end yields and the dollar. With the market already sensitive to signs of more persistent inflation, a 0.3% m/m gain in core would likely be treated as confirmation of near-term hiking expectations already priced in by the market. GDP and University of Michigan are secondary, but together they will help frame the resilience of demand and the consumer’s inflation outlook.

In Canada, a 3.0% y/y CPI would be enough to keep the BOC on alert, especially if Macklem and Rogers strike a cautious tone.

Banco de México is expected to keep rates on hold at 6.50%, though a hawkish lean may be necessary to offset the effects of the Fed result.

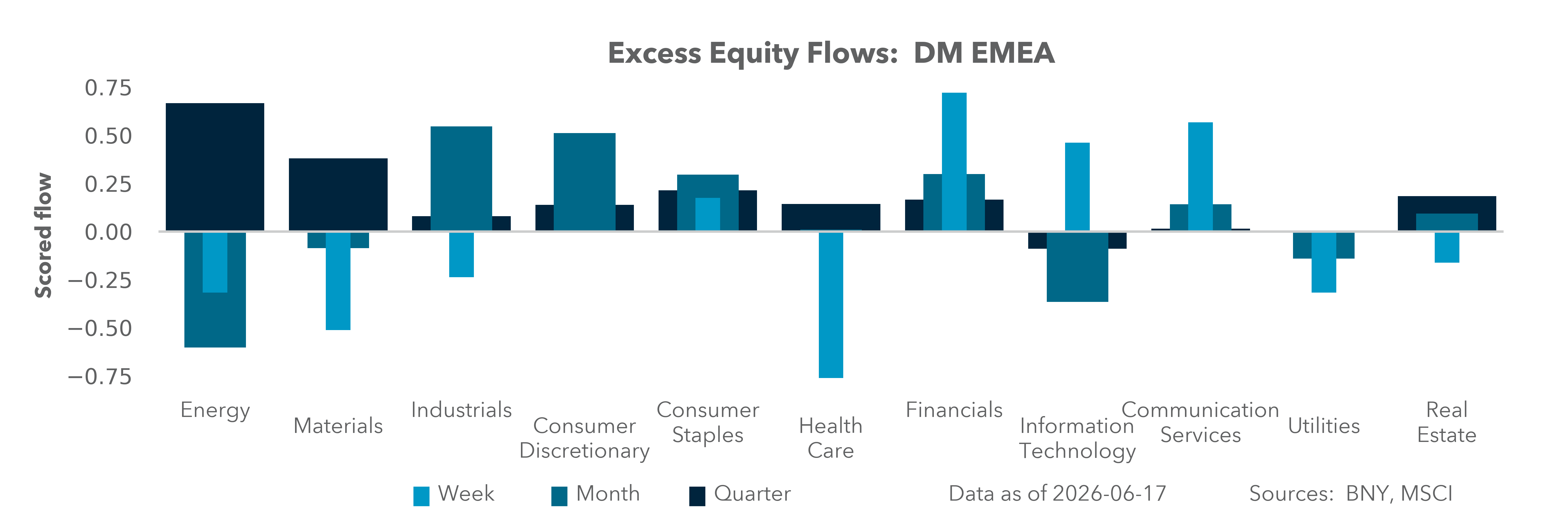

EMEA: Politics and trade distracting from growth

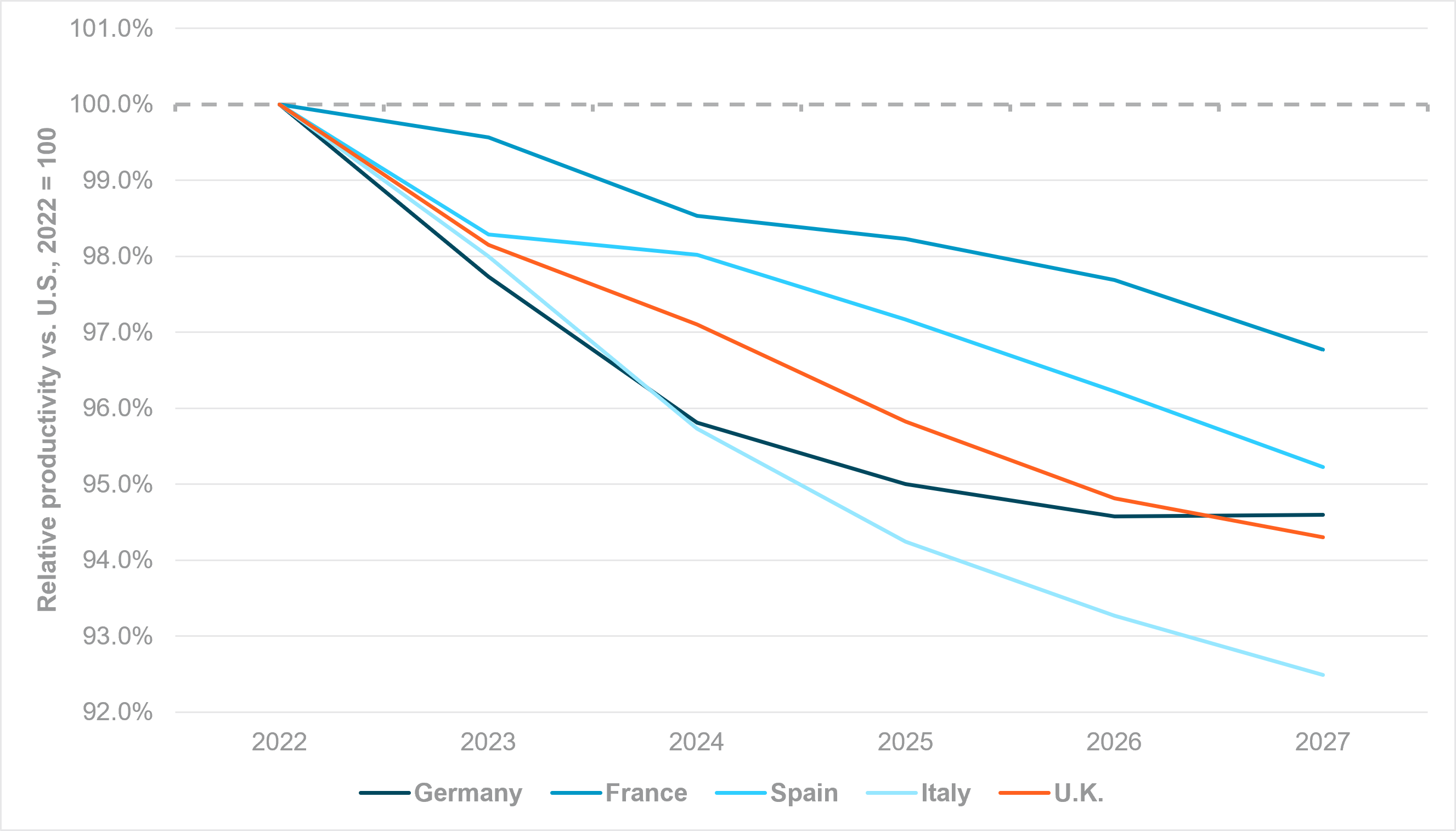

EXHIBIT #3: RELATIVE LABOR PRODUCTIVITY VS. U.S., OECD ECONOMIC OUTLOOK

Source: BNY, OECD

Our take: Not a single major central bank in Western Europe followed the ECB in hiking rates. Although the decisions were in-line with expectations, the policy narratives were nowhere near as hawkish as the Governing Council’s stance. Policymakers in Europe are happy to incorporate hikes or the risk of a move in their outlook, but there is no inclination to act preemptively. For example, Bank of England (BOE) hawk Catherine Mann clearly expressed her preference for a hike, but advocated waiting for data to fully confirm that wages were moving in a way that could risk price stability. She stressed that if the BOE were to hike, transmission into the economy would be rapid and effective – making an “activist” hike in a supply-constrained environment a powerful tool that should only be deployed once risks to price stability are clear and a growth offset is warranted.

The Riksbank and Norges Bank have similarly embedded additional tightening through their forecast horizon to signal such intent, but both are also content to wait for confirmation. The bottom line is the ECB is foregoing optionality through its strict adherence to price stability.

Assuming the supply shock has peaked, Europe will need to return to the growth narrative without delay. ECB President Christine Lagarde made this point at her press conference, highlighting that structural reforms were still needed to manage the trade-off between inflation and growth. Such messages are being delivered on a regular basis by Governing Council members but competitiveness continues to deteriorate (Exhibit 3). The latest challenge to European financial conditions may lie in the form of asset rotation back into the U.S. due to stock listings and other funding rounds for the AI/tech theme. Yet, the immediate challenge Brussels has chosen is to strengthen its response to the surge in Chinese imports, in order to protect European industry. Limiting external competition does not make an economy more competitive globally, and we fear Brussels continues to delay the domestic reform agenda.

Forward look: The only rate decision in Europe in the week ahead is in Hungary, where a cut is highly likely given surprisingly weak inflation. The confirmation of the ceasefire has bought additional space for the Magyar Nemzeti Bank, and real rates remain high enough to support both duration and the currency, though we believe the impending decline in energy prices will dampen pass-through risk even if a cut weighs on HUF.

Otherwise, politics will dominate as markets assess the EU summit conclusions and political developments in the U.K. We also expect European NATO members to announce participation in operations to support shipping recovery through the Strait of Hormuz, which would benefit transatlantic relations.

APAC: Post-ceasefire relief meets hawkish Fed headwinds

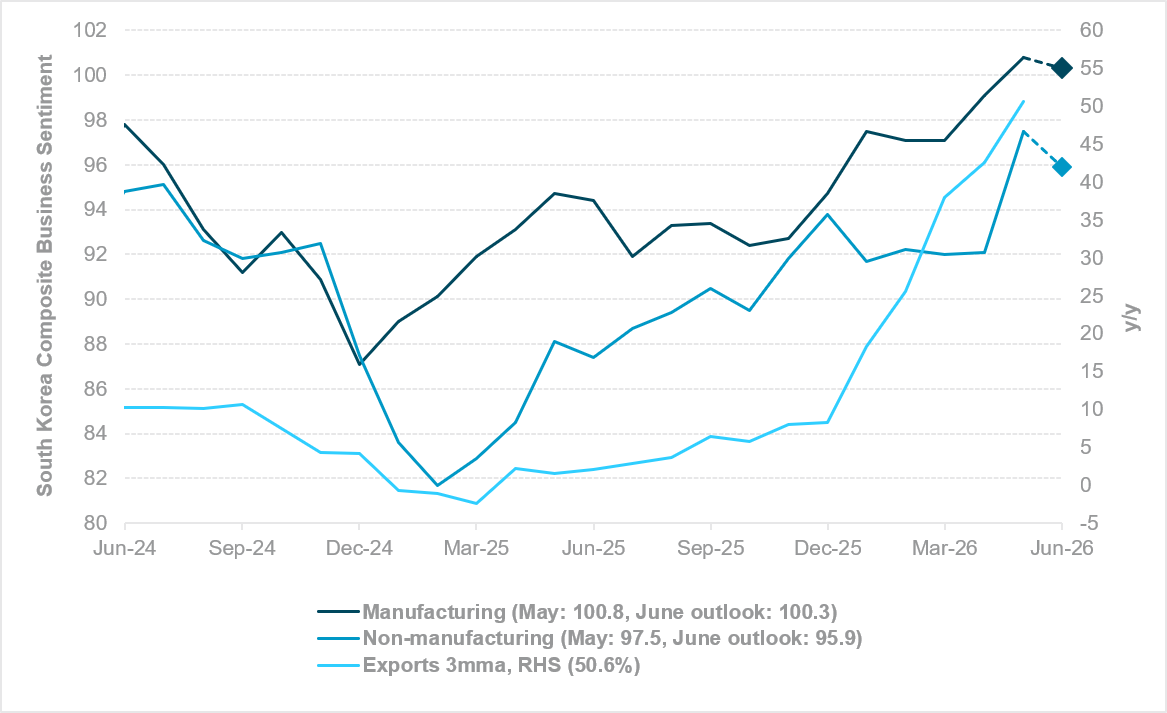

EXHIBIT #4: SOUTH KOREA COMPOSITIVE BUSINESS SENTIMENT INDEX

Source: BNY, Bloomberg

Our take: APAC’s macro calendar is led by Australia’s May CPI and labor market report, which will be key to assessing the durability of inflation pressures and the RBA’s policy outlook. The June Tokyo CPI – a closely watched lead indicator for nationwide inflation – will be in focus alongside Japan’s June PMI and services PPI. Singapore releases May CPI and industrial production, providing another important gauge of regional price dynamics. China’s Loan Prime Rate fixings and Thailand’s policy rates are both expected to be unchanged.

Elsewhere, activity indicators dominate the calendar. South Korea releases June exports (1–20 days), consumer confidence, retail sales and the Composite Business Survey Index, offering a timely read on domestic and external demand. Taiwan’s export orders and industrial production will provide further insight into the technology cycle, while India’s June PMI, infrastructure output and FX reserves will help gauge growth momentum. Regional PMI surveys round out a week focused on growth resilience, inflation trends and the implications for regional FX and rates markets.

The negative sentiment data may be overlooked following the signing of the U.S.–Iran peace deal, which called for reopening the Strait of Hormuz and extending the ceasefire another 60 days.

Forward look: The de-escalation of Middle East geopolitical tensions and the decline in oil prices have provided meaningful relief across Asia, particularly for net oil-importing economies and their currencies. However, the hawkish outcome of the latest Fed meeting introduced renewed headwinds through a stronger U.S. dollar and tighter global financial conditions. Overall market sentiment remains fragile.

Regional central banks have stayed highly vigilant in containing currency depreciation through a combination of macroprudential measures, higher money market rates, more attractive hedging conditions for foreign investors, active FX smoothing operations, and, in some cases, monetary tightening. Both Bank Indonesia and the Bangko Sentral ng Pilipinas raised policy rates by 25bp last week, to 5.75% and 4.75% respectively, while signaling the possibility of further tightening if needed to support currency stability.

While the worst of the recent market stress may be behind APAC, the recovery path is likely to be gradual as policymakers continue to address fiscal vulnerabilities, external financing needs, and broader deficit concerns.

The week ahead should provide a clearer read on whether the global macro backdrop remains one of resilient growth and manageable inflation, or whether recent signs of divergence become more pronounced. While the Fed has reinforced a hawkish bias, policymakers across Europe and much of Asia should find room to refocus on growth and competitiveness, rather than managing FX risk, capital outflows and financial stability concerns. Nonetheless, the policy landscape remains uneven and there will be opportunities in relative value positions.

Against this backdrop, incoming inflation and activity data will be watched closely, with U.S. PCE likely to set the global tone by testing whether recent Fed repricing has further room to run. More broadly, markets will be looking for evidence that growth can regain momentum outside the U.S. without reigniting price pressures, or whether policy divergence remains the defining theme for the global outlook. We argue that this is also highly desirable for asset allocation, as diversification interest is rebounding given the heavy concentration in the “U.S. exceptionalism” theme.

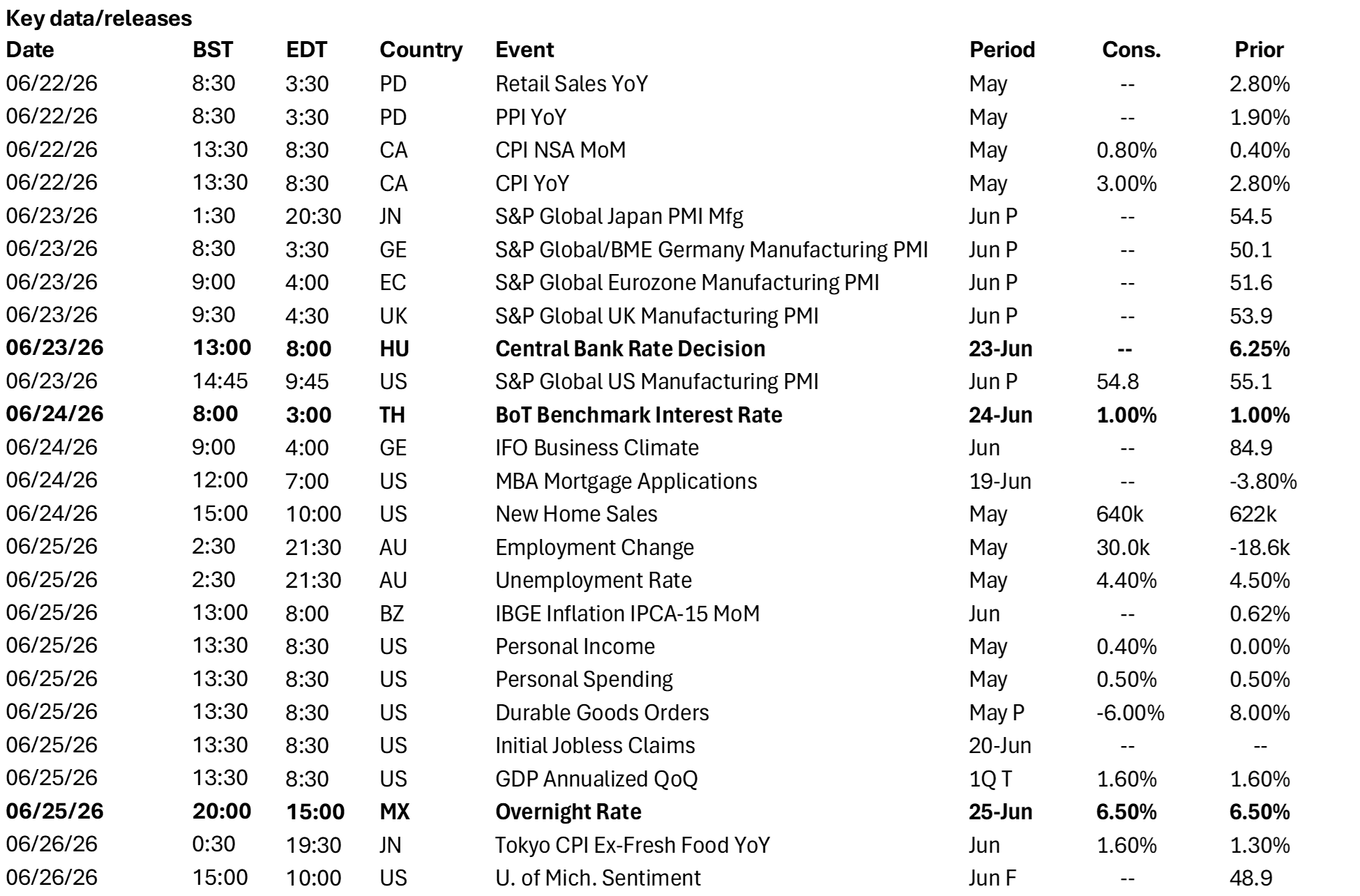

Central bank decisions

Hungary, Magyar Nemzeti Bank (Tuesday, June 23): The MNB is likely to cut rates to 6.00%. Inflation continues to behave as if there were no supply issues globally. Sequential inflation has fallen back to zero and the annualized rate has returned below 2%. The fiscal consolidation pledged by the government is clearly starting to exert pressure on domestic demand, marking a significant turnaround in inflation expectations. The government has also signaled tolerance for currency weakness as long as bond yields continue to fall. The MNB has sufficient space to keep real rates high enough to limit pass-through risk, even as its divergence from the ECB warrants monitoring.

Thailand, Bank of Thailand (Wednesday, June 24): We expect the BOT to keep the policy rate unchanged at 1.00%. Although headline CPI reached 2.79% y/y in May – up sharply over the past two months and likely to rise further – and exports and tourism are improving, we see little urgency for the BOT to tighten. Growth remains uneven, and maintaining negative real interest rates could provide additional support for domestic demand. Market focus will be on the BOT’s updated macroeconomic projections and its assessment of the balance between rising inflation pressures and growth risks.

Mexico, Banco de Mexico (Thursday, June 25): Banxico is expected to keep rates on hold at 6.50% but if the market continues to push for Fed hawkishness, the transmission into financial conditions for Mexico is perhaps among the fastest and most consequential globally. While this doesn’t mean that Banxico will need to match the FOMC one-for-one, the market will probably have a lower tolerance for divergence compared to other central banks in the high-yield group. Current inflation is manageable, but a 200–250bp real rate level is low by regional standards.

Source: BNY

Source: BNY