Balance sheet reduction moves to the fore

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 4 minutes

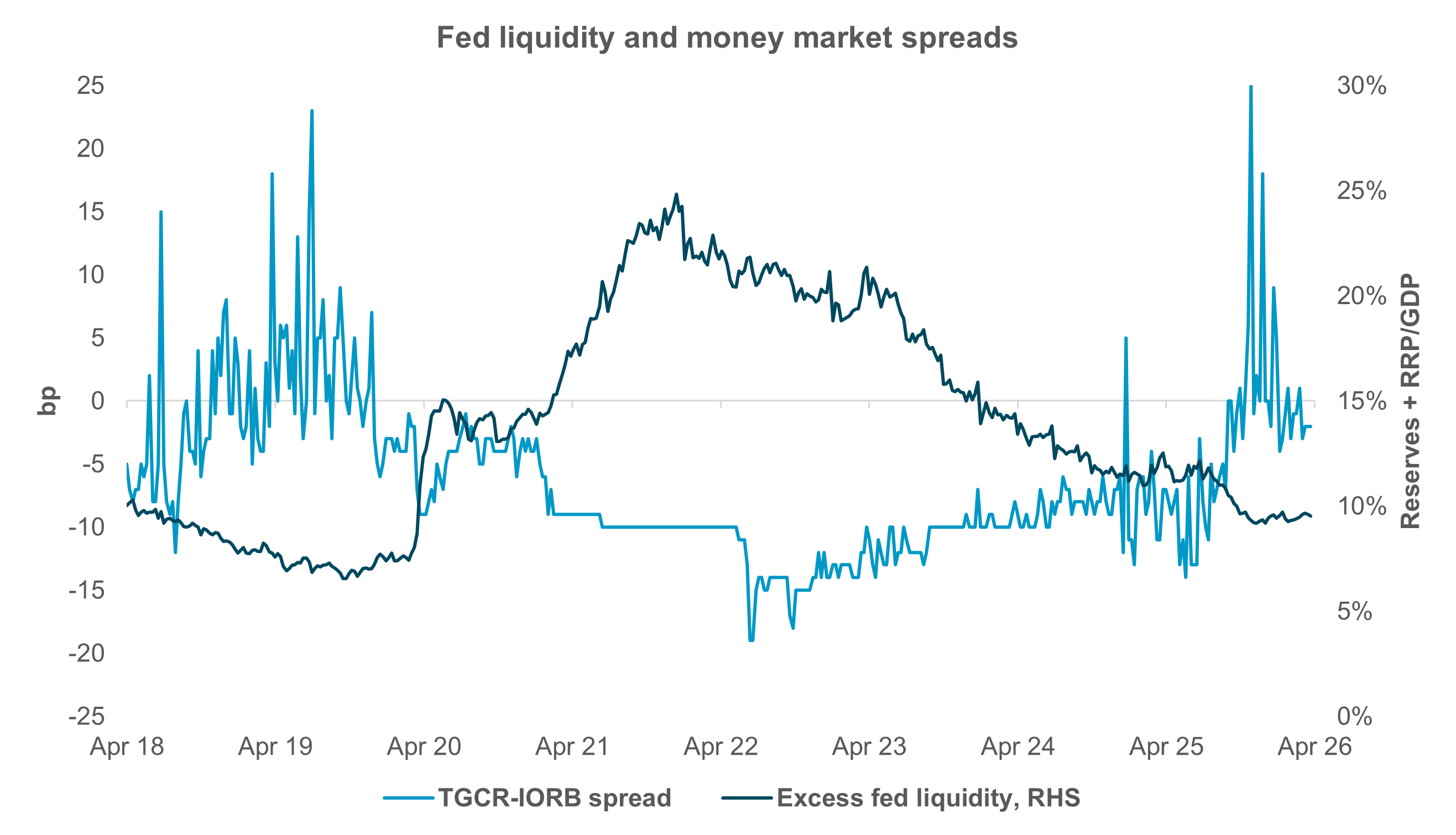

EXHIBIT #1: SMALLER FED BALANCE SHEET, TIGHTER MONEY MARKETS

Source: BNY Markets, Federal Reserve Board of Governors, Bloomberg

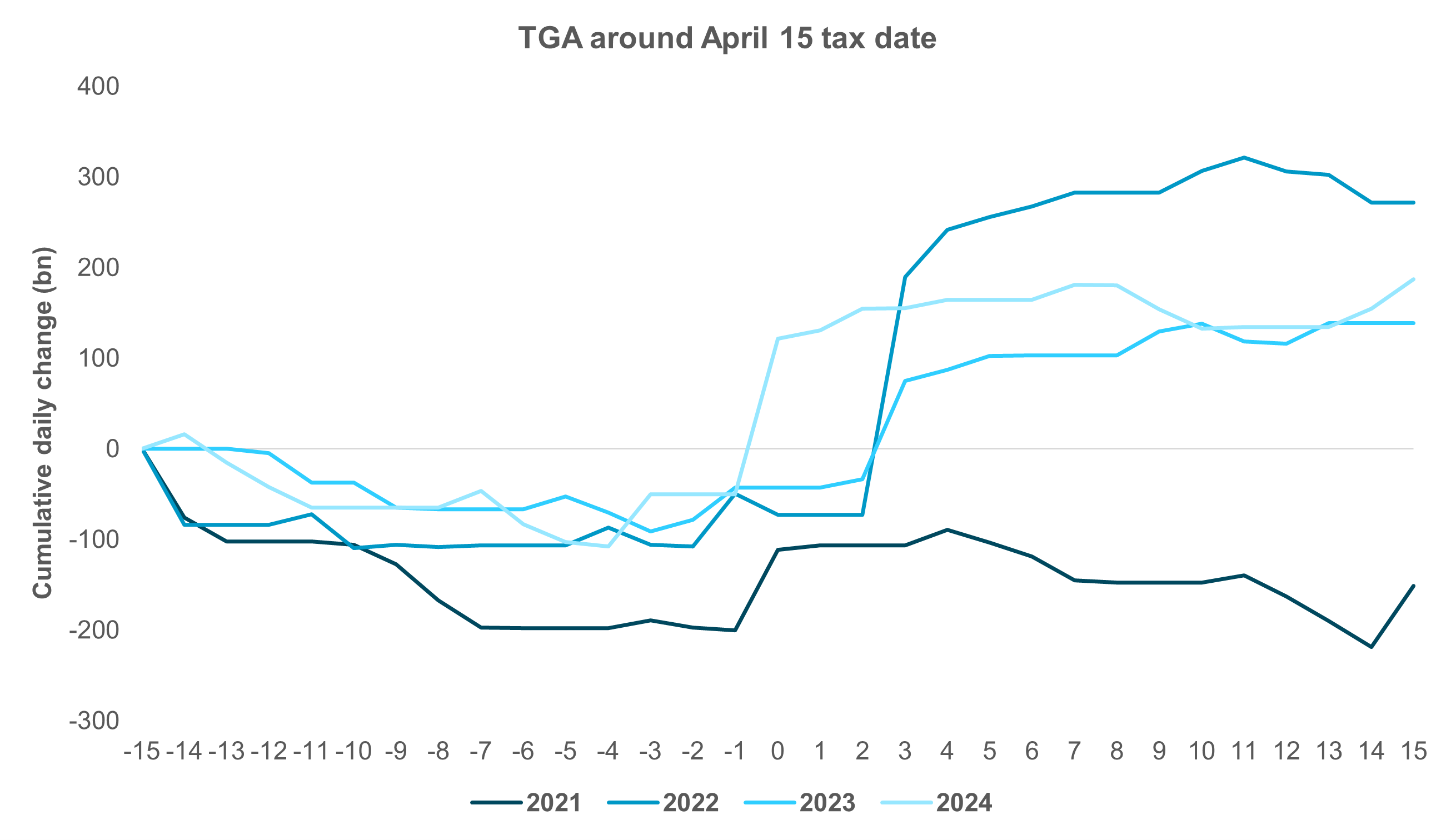

EXHIBIT #2: TAX DATES RELIABLY SWELL THE TGA

Source: BNY Markets, U.S. Treasury Department

The Fed’s balance sheet remains a hot topic that will only grow more so in the coming months. We have written frequently on both balance sheet dynamics and the level of reserves. Both issues, of course, are connected – given that the largest liability on the Fed’s balance sheet is reserves, exceeding even currency in circulation. Many Fed officials, including Fed chair nominee Kevin Warsh, have indicated a desire to reduce the size of the balance sheet in coming years. This would primarily be accomplished by reducing the supply of reserves in the system. However, lower reserves typically correlate to tighter money markets, hence shrinking the balance sheet could be problematic in this sense. Exhibit #1 shows the relationship between funding spreads and reserve dynamics.

Last week, the New York Fed’s System Open Market Account (SOMA) manager Roberto Perli delivered remarks related to balance sheet and plumbing issues, including the Fed’s recent experience with reserve management purchases (RMPs) aimed at keeping funding markets stable while reserves remain in an ample state. Governor Stephen Miran, also a proponent of a smaller balance sheet, delivered remarks alongside the release of a comprehensive Fed working paper addressing potential mechanisms available to achieve this goal. At a Brookings Institute conference, Stanford Professor Darrell Duffie discussed a similar topic alongside his own paper. Today, we put these remarks and papers into perspective.

The Fed currently judges reserves to be ample, meaning that in general, short-term money market rates should not exhibit excessive volatility, except on so-called “high pressure” days such as month and quarter end, and days that feature large UST settlements. Perli’s speech, entitled “Reflections on the Early Days of Reserve Management Purchases and the Maintenance of Ample Reserves,” summarized developments in this space. He argued (convincingly, to us) that RMPs and standing repo (SRP) operations have helped ease the transition of the balance sheet from an abundant reserves regime to a merely ample one, without significant funding market stress. Since December, the NY Fed has been purchasing around $40bn per month in T-bill buying, and the SRP has seen occasional use, especially on these high-pressure days.

Perli also noted that once tax season has come and gone, RMPs can be scaled back from $40bn per month, though he stopped short of specifying a target. Tax dates bring significant funds into the federal government’s coffers (formally called the Treasury General Account or TGA), which, in turn – other things being equal – reduces reserves, potentially creating short-term risks to liquidity in funding markets. Exhibit #2 shows how the TGA typically jumps at and just after April 15. This is why the rather hefty RMPs will stay that way through April.

The Fed’s concept of the balance sheet “trilemma” implies that a central bank can achieve a smaller balance sheet only if it either tolerates high money market volatility or engages in frequent open market operations to keep rates stable. Both Perli and Miran argue that another option, outside the trilemma, would be to reduce banks’ structural demand for reserves, allowing for a smaller balance sheet without stoking rate volatility.

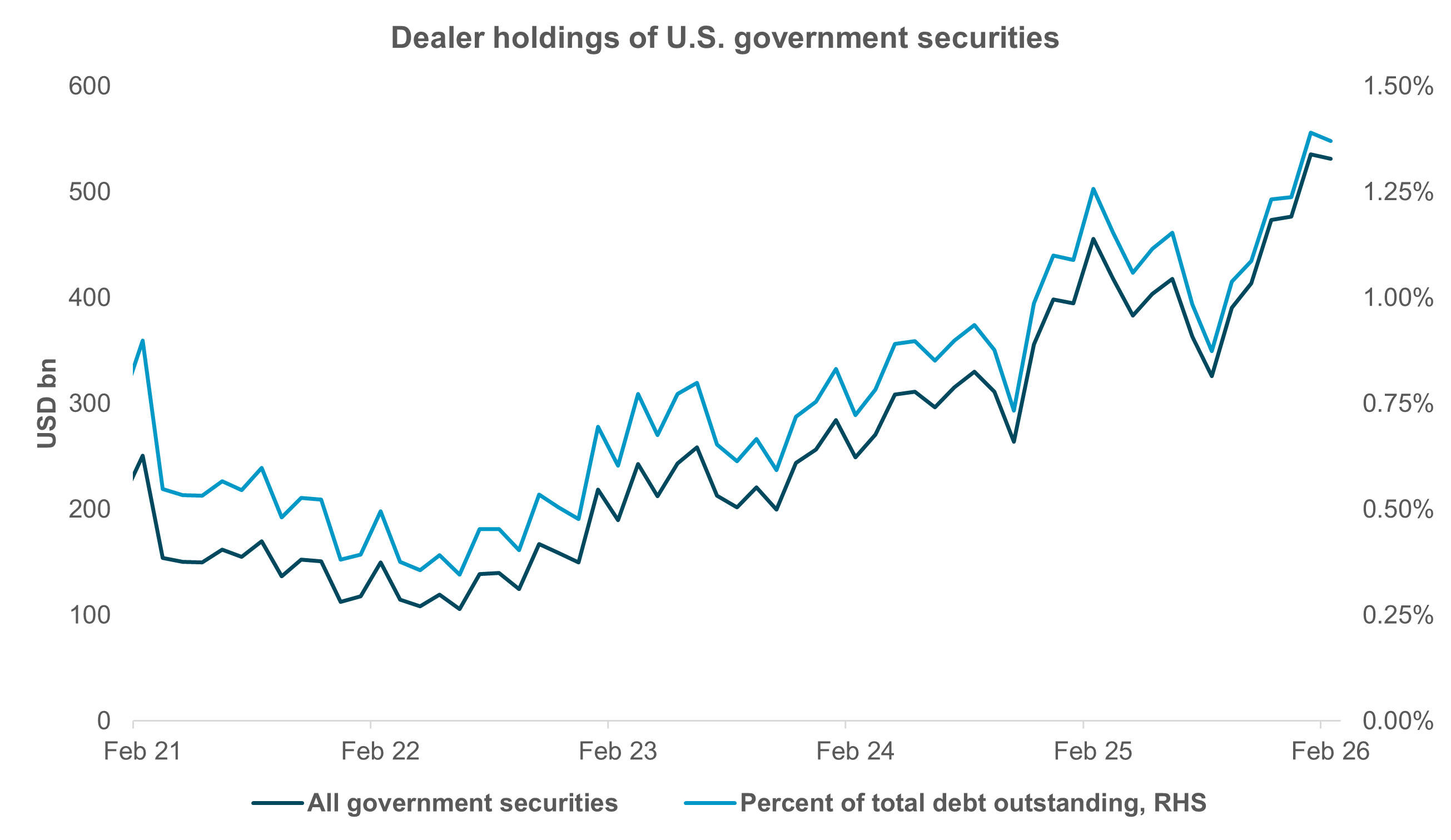

EXHIBIT #3: DEALER HOLDINGS AT ALL-TIME HIGHS

Source: BNY Markets, Bloomberg, U.S. Treasury Department

Governor Miran delivered his speech the same day his co-authored working paper, “A User’s Guide to Reducing the Federal Reserve’s Balance Sheet,” was released. The speech was relatively short. The paper is long and detailed – more than we can cover here, but the key arguments are worth distilling. Both argue that policy changes, particularly regulatory tweaks, could achieve as much as $2.1tn in balance sheet shrinkage, though the timeline could likely stretch well over a year. The idea, as noted above, is to shift the demand curve for reserves to the left, achieving lower reserve levels at the same clearing price (i.e., interest rate) for funding.

Miran identified 15 specific policies to achieve this. These broadly fall into three buckets: (1) regulatory reform to reduce banks’ appetite for reserves by lowering required capital and liquidity buffers; (2) administrative tweaks to make holding reserves less attractive; and (3) changes to Fed liquidity facilities that would give market participants easier access to short-term funding on high pressure days. In simulations (not shown), Miran and his coauthors find that the reserve supply needed to meet demand can fall by $1.15tn to $2.1tn. As a point of reference, reserves are currently around $3tn, or about 9% of U.S. nominal GDP. For further reference, in September 2019 when the funding markets seized up, reserves were just 7% of GDP at the time.

Professor Duffie’s paper covers much the same ground but with a more cautionary tone. Because smooth interbank payments depend on sufficient intraday liquidity, any changes –regulatory, rate-related or otherwise, including the tricky question of tiering interest on reserves – should be phased in gradually and closely coordinated with money market participants.

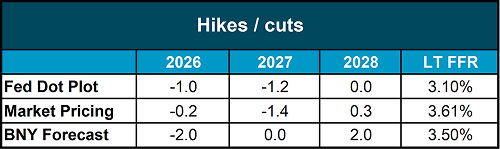

We maintain that the Fed will cut interest rates in H2 2026, although the market remains skeptical. On Monday, rate markets appeared to have “flipped” somewhat. Markets have shifted from pricing in a small probability of hikes – where they sat earlier in the Middle East conflict – toward pricing cuts in the second half, much more in line with our view, which we advocated here in recent weeks.

To reiterate: under the (admittedly bold) assumption the conflict ebbs by midyear, and energy and other crucial input prices follow, we see a path to rate cuts. We don’t expect prices to return to pre-conflict levels, nor does our outlook require this. As long as prices have peaked, inflation – crucially short-term inflation – expectations will ease as well, but our view is that the labor market will deteriorate to the point that the Fed can start to cut rates.

This week’s data will be telling – several key labor market indicators, including the March NFP report, are due. A weaker employment outlook would reinforce our case.