Market Movers: Two-sided

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 6 minutes

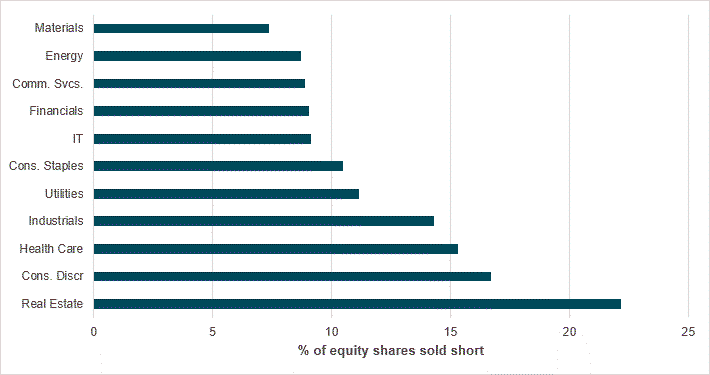

Short utilization points to growing margin and cost pressures

Source: BNY

Despite the lack of progress in the Iran talks, the U.S. equity performance stands out; however, the associated concentration risk in energy and IT-related themes is also well-established.

Meanwhile, based on our short utilization figures, the stress points in the U.S. economy are starting to show as well. These are related in particular to the current supply pressures and to a potential tightening in financial conditions if the Fed cannot realize interest rate cuts.

For example, real estate is facing significant gains in short utilization, and this is one of the sectors that is most sensitive to interest rates. Consumer discretionary is also facing additional stress and is now the sector with the second-highest short utilization in North America. Note, however, that it already had the highest short utilization before the war began, indicating that investor concern over spending capacity has been present throughout the year. Healthcare has been facing cost-related uncertainty for a while, and industrials are contending with additional input costs. However, we stress that these four sectors started the year with the highest levels of short utilization – thematically, cost and margin pressures have always featured, although the conflict has likely exacerbated adverse conditions. Meanwhile, energy, IT and communication services are showing very limited short utilization. Clearly, current earnings-driven performance in these sectors will be painful for any short positions.

Today is about the two-sided forces in play across markets, with the May 4 holiday in the U.K. adding to liquidity constraints. The fear factors of energy prices and supply shocks continue to leave open debates about policy – compare the push by the ECB’s François Villeroy de Galhau to wait for more data against his colleague Peter Kažimír’s near-certainty on a June rate hike. USD is higher despite EUR holding above 1.1700 on the index because of JPY and local holidays. Stocks are a mixed bag, with Asia higher, Europe lower and U.S. futures uneven.

Bottom line: U.S. markets may have the Monday blues, as April’s come-from-behind rally in U.S. shares looks to have lost its momentum in May. The role of the USD as a brake to the bulls could be a factor today. Similarly, the only weekend news from Iran was two-sided, with the U.S. plan helpful but insufficient to convince markets that a solution to the energy supply impasse has been found. This leaves U.S. data today again being interpreted in the context of oil prices. The Fed Senior Loan Officer survey will also be seen in that light, with a focus on what squeezed business and consumers mean for bank lending. The week ahead brings a host of labor data and robust expectations, making today’s result important as investors shift from momentum to value.

Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria and Oman have met virtually to review global oil market conditions. They agreed to implement a production adjustment of 188,000 barrels per day in June 2026, reducing the additional voluntary cuts announced in April 2023. The countries emphasized a cautious approach, retaining flexibility to adjust production levels, including reversing previous cuts from November 2023. They reaffirmed their commitment to market stability, full conformity with the Declaration of Cooperation and compensating for any overproduction since January 2024. Brent +0.657% to 108.88, WTI +0.736% to 102.69, Omani crude -3.917% to 102.06, Dubai crude -3.429% to 100.855.

Japanese Prime Minister Sanae Takaichi and Australian Prime Minister Anthony Albanese have agreed to enhance cooperation to secure stable supplies of critical minerals, energy and essentials amid China’s rare earth dominance and Middle East conflicts. They issued five outcome documents, including a joint declaration on economic security focusing on resilient supply chains for rare earth minerals, energy and food. Both countries also committed to deepening defense and cybersecurity collaboration. This cooperation addresses Japan’s reliance on China for rare earth minerals and energy challenges due to disrupted crude oil transport. The visit marks the 50th anniversary of their friendship treaty. Japan closed. USDJPY +0.083% to 156.88.

President Trump has announced an increase in U.S. tariffs on cars and trucks imported from the EU to 25%, citing the bloc’s failure to comply with a trade agreement. The tariffs will not apply to vehicles manufactured in U.S. plants. This move escalates trade tensions with the EU and may impact companies such as Stellantis NV, which imports European models. The trade deal, agreed in July, has faced ratification delays and disputes over metals tariffs. Both sides have expressed interest in finalizing the agreement despite ongoing challenges. S&P Mini +0.17% to 7270, DXY +0.029% to 98.184, 10y UST -0.1bp to 4.37%.

China has directed its companies to defy U.S. sanctions on private refiners linked to Iranian oil, including Hengli Petrochemical, marking an unprecedented challenge to U.S. policy. This move signals a more aggressive stance ahead of the Xi-Trump summit and may escalate tensions if the U.S. extends secondary sanctions to Chinese banks or state entities. Beijing’s blocking measure aims to nullify the sanctions’ legal effect domestically, reflecting its opposition to unilateral U.S. sanctions lacking UN authorization. The decision tests the U.S. sanctions system and highlights China’s expanding use of economic tools, as U.S.-China relations remain strained. China closed. USDCNY +0.181% to 6.8281.

China’s People’s Bank and General Administration of Customs is easing gold import and export licensing rules to promote trade and improve the business environment, effective June 1, 2026. The validity of multi-use permits for gold trade will be extended from six to nine months, with no limit on the number of customs declarations within the permit’s quota. Fifteen additional customs ports, including Beijing, Shanghai and Guangzhou, will be authorized for bullion clearance. This replaces previous regulations from 2016 and 2017, streamlining procedures for frequent gold trading entities.

RBNZ policy member Prasanna Gai has stated that the Strait of Hormuz supply shock does not justify automatic rate hikes, advocating a conventional look-through approach to supply shocks. He emphasized that pre-emptive tightening is only warranted when economic synchronization is high and coordination mechanisms are active, and that these conditions are not currently met. However, Gai acknowledged that the shock has raised the neutral interest rate, implying a higher baseline for future policy normalization. His dovish stance contrasts with hawkish signals from other central banks, reflecting New Zealand’s fragile economy and prior aggressive rate cuts throughout 2025. NZX 50 +0.45% to 13098, NZDUSD +0.17% to 0.5909, 10y NZGB -2.7bp to 4.656%.

Final U.S. March durable goods expected to rise by 0.8%, ex-transportation up 0.9%.

U.S. factory orders for March expected to grow by 0.5%, with ex-transportation orders up 1.4%.

U.S. Treasury sells $89bn in 13-week bills and $77bn in 26-week bills.

Central bank speakers: The Fed’s John Williams delivers keynote remarks at the Cynosure Group Spring Symposium Yale Club. ECB Governing Council member Joachim Nagel speaks on Europe’s economy in Frankfurt. The Governor of the Bank of Canada, Tiff Macklem, will appear before the House of Commons Standing Committee on Finance.

Mood: Remains in risk-neutral territory at 0.045, softening from a risk-on stance despite generally firm inflows into global equities. An underlying liquidity preference is likely picking up due to high energy prices.

FX: AUD and CHF underperformed into month-end, with the former assuming a defensive stance ahead of the upcoming RBA decision

FI: EUR and GBP continued to lead G10 fixed income due to high real rates, likely justified by the cautious central bank decisions last week. Meanwhile, large outflows were seen in Chinese government bonds.

Equities: Most G10 markets continued to perform well, led by the U.S., which is once again driving the global tech theme. Chinese equities fared well in APAC, hinting at some rotation taking place.

“Unless both sides win, no agreement can be permanent.” – Jimmy Carter

“To love and be loved is to feel the sun from both sides.” – David Viscott

The Eurozone Sentix Economic Sentiment Index for May climbed 2.7 points to -16.4, reflecting cautious investor optimism despite ongoing inflation concerns and the Iran conflict. However, the index for Germany declined by 3.2 points, as its third consecutive drop took it to its lowest level since January 2025 amid a government crisis and economic difficulties. By contrast, the U.S. and Asia ex-Japan regions showed strong improvements, with indices rising by 7.6 and 8.4 points, respectively, contributing to a 6.5-point increase in the global economic sentiment index. Euro Stoxx 50 -0.1% to 5876, EURUSD -0.077% to 1.1712, BBG AGG Euro Government High Grade EUR 0bp to 3.313%.

The Q2 ECB Survey of Professional Forecasters for Q2 showed upward revisions in near-term headline HICP inflation to 2.7% (2026) and 2.1% (2027), with 2.0% expected for 2028, unchanged from Q1. Core HICP inflation was also revised up to 2.2% for 2026-27 and 2.1% for 2028. Real GDP growth forecasts were lowered to 1.0% for 2026 and 1.3% for 2027, unchanged for 2028, mainly due to higher energy prices linked to the Middle East conflict. Unemployment rate expectations remain steady at 6.3% (2026), 6.2% (2027) and 6.1% (2028).

The Eurozone manufacturing PMI for April rose to 52.2 points (March: 51.6), setting a 47-month high and indicating stronger manufacturing growth. This was driven by increased new orders and front-loaded purchasing amid expected price rises. Output and new export orders expanded, the latter for the first time in over four years. Input price inflation surged to a 46-month peak, pushing output price inflation to a 39-month high. Supply chain delays worsened due to bulk ordering and geopolitical tensions. Employment fell for the 36th consecutive month despite rising backlogs. Business optimism fell to its lowest ebb since November 2024.

Germany’s manufacturing sector saw continued growth in output and new orders in April, with the S&P Global Manufacturing PMI at 51.4, slightly down from March’s 52.2. However, business confidence turned negative for the first time in 18 months due to concerns over rising inflation, supply chain disruptions and uncertainty linked to the Middle East war. Input costs rose sharply to their highest level since September 2022, driving factory gate charges up. Supply delays worsened to the most severe since mid-2022. Employment declined, but workloads remained stable amid modest purchasing growth and inventory reductions. DAX +0.43% to 24396, EURUSD -0.077% to 1.1712, 10y Bund +1.8bp to 3.055%.

France’s manufacturing sector showed solid growth in April 2026, with the S&P Global Manufacturing PMI rising to 52.8 from 50.0 in March, the highest reading since May 2022. New orders and output increased at the fastest rates since early 2022, driven by advanced client stockpiling motivated by supply chain pressures linked to the Middle East conflict. Export orders declined, while domestic demand surged. Input price inflation hit a near-four-year high, outpacing selling price increases, indicating cost absorption. Employment fell for the third consecutive month. Business confidence improved slightly but remained subdued because of geopolitical concerns. CAC 40 -0.23% to 8096, EURUSD -0.077% to 1.1712, 10y OAT +1.6bp to 3.709%.

Italy’s manufacturing PMI rose to 52.1 points in April, up from 51.3 in March – the highest level in four years. Output growth was the strongest in over three years despite softer demand and a modest drop in total order volumes. Export sales saw a slight increase. Purchasing activity hit a four-year record, driven by stock concerns and anticipated price rises. Employment growth was the highest since September 2024. Supply chain disruptions worsened due to the Middle East conflict, causing the longest delivery delays since mid-2022 and pushing cost inflation to a nearly four-year high. Selling price inflation was also substantial, despite softening. FTSE MIB -0.02% to 48237, EURUSD -0.077% to 1.1712, 10y BTP +1.5bp to 3.874%.

Dutch manufacturing PMI rose to 54.4 points in April from 52.0 in March. This was the highest reading since July 2022 and the eleventh consecutive month of improvement. Demand strengthened as supply chain disruptions linked to the Middle East war prompted customers to front-load orders: new international orders grew at the fastest pace in nine months, notably from Asia and the U.S. Output increased at the steepest rate in seven months, while employment declined slightly for the second successive month due to labor shortages and cost-saving measures. Supply delays worsened, leading to increased input purchasing and stockpiling. Input cost inflation hit a near-four-year high, driven by energy, fuel, transport and raw materials. AEX +0.21% to 1016, EURUSD -0.077% to 1.1712, 10y NGB +1.3bp to 3.182%.

Spain’s manufacturing sector expanded modestly in April, with the S&P Global Manufacturing PMI rising to 51.7 from 48.7 in March – its first improvement since November. Output and new orders increased as clients sought to build stock amid supply chain disruptions caused by the Middle East war. Inflation surged, with factory gate and input prices rising at the fastest rates since late 2022, driven by higher energy, fuel and transportation costs. Despite rising workloads, employment fell for the eighth consecutive month. Export orders fell for an eighth month, though the rate of decline eased compared with March, reflecting ongoing uncertainty. IBEX 35 -0.24% to 17743, EURUSD -0.077% to 1.1712, 10y Bono +1.8bp to 3.516%.

Switzerland’s manufacturing PMI rose to 54.5 points in April, up from 53.3 in March, indicating expansion in the sector. Key subindices showed increases in output (52.3 vs. 50.6), backlog of orders (56.1 vs. 54.2) and quantity of purchases (54.4 vs. 48.3). Purchase prices surged to 82.8 from 71.3, while suppliers’ delivery times slightly lengthened to 64.1 from 63.6. Employment in manufacturing remained below 50, at 48.5. The services PMI dropped to 54.8 from 57.2 but still signaled growth, with business activity at 58.4 and new orders at 54.8. SMI +0.16% to 13157, EURCHF -0.257% to 0.91735, 10y Swiss GB +1.1bp to 0.415%.

Sweden’s Swedbank Manufacturing PMI rose to 57.2 points in April, up from 56.2 in March, indicating stronger manufacturing sector expansion. Key components showed orders increasing to 59.4 (54.2 in March), production slightly down to 57.6 (58.4) and employment easing to 55.1 (57.9). Delivery times lengthened significantly to 64.3 (59.6), while stocks rose to 57.0 (51.8). Export orders increased modestly to 53.0 (52.4), and domestic orders strengthened to 57.9 (54.4). Raw material prices surged to 81.3 (69.8), reflecting rising input costs. Overall, the data signal robust manufacturing growth with rising demand and cost pressures in April. OMX +0.45% to 3074, EURSEK -0.32% to 10.8382, 10y Swedish GB -0.8bp to 2.878%.

Hungary’s industrial producer prices rose by 1.2% y/y and 3.9% m/m in March. Domestic output prices increased by 1.2% y/y, driven by a 1.6% rise in manufacturing but a 0.1% decline in energy. Energy and intermediate producer branches rose by 1.7% and consumer goods producers by 1.1%, while capital goods remained unchanged. Non-domestic output prices rose 1.3% y/y, with manufacturing down 0.8% but energy prices up 20.2%. Q1 domestic and non-domestic output prices fell by 1.5% and 1.7% y/y, respectively. Budapest SI +1.07% to 135221, EURHUF -0.009% to 363.36, 10y HGB 0bp to 6.03%.

Türkiye’s April CPI was up 32.37% y/y and 4.18% m/m. Key contributors to the y/y increase included housing, water, electricity, gas and other fuels (+46.60%), transportation (+35.06%) and food and non-alcoholic beverages (+34.55%). M/m increases were led by housing (+7.99%), transportation (+4.29%) and food (+3.70%). Core CPI, excluding unprocessed food, energy, alcohol, tobacco and gold, rose 30.51% y/y and 3.42% m/m. Elsewhere, the April Domestic Producer Price Index (D-PPI) rose by 28.59% y/y and 3.17% m/m. By sector, y/y increases were 40.42% in mining and quarrying, 30.36% in manufacturing, 7.19% in electricity and gas, and 38.26% in water supply. M/m changes included a 9.84% rise in mining, a 3.59% gain for manufacturing and a 4.96% decline in electricity and gas. Key industrial groups saw y/y growth rates of between 24.70% and 33.15%. BI 100 -0.12% to 14425, USDTRY -0.041% to 45.1995, 10y TGB +35bp to 34.24%.

Australian total dwelling approvals fell 10.5% in March to 17,300 units (after a 31.0% rise in February), driven by a 26.0% drop in private sector dwellings excluding houses to 6,632 units (February: 101.1% rise). Private sector house approvals rose 0.9% to 10,194, the highest since November 2021, led by a 9.5% increase in New South Wales. Residential building value declined 15.8% to $10.77bn, while non-residential building value fell 25.3% to $5.97bn. Elsewhere, the Melbourne Institute Monthly Inflation Gauge recorded another m/m jump in inflation for April. This was primarily influenced by higher recreation-related prices, attributable largely to airfares. In y/y terms, headline inflation was 4.3%. The monthly cost of living also increased in April, particularly for employees and self-funded retirees. ASX -0.09% to 5558, AUDUSD -0.056% to 0.7198, 10y ACGB -4bp to 4.98%.

Asia manufacturing PMI for April showed divergent rates, but input cost inflation surged across the region: North Asia (Taiwan 55.3, South Korea 53.6, Malaysia 51.6) remained in expansion, while Indonesia (49.1) and the Philippines (48.3) contracted. North Asia’s growth was supported by output, new orders and inventory building amid supply concerns, with resilient export demand, especially in Taiwan. ASEAN weakness stemmed from declines in output and exports, notably in the Philippines. Input cost inflation surged region-wide due to energy, raw materials and freight disruptions linked to the Middle East conflict, causing higher output prices and longer supplier delivery times. Business confidence softened except in the Philippines. MSCI Asia +0.13% to 257, USD vs. APAC FX Index +0.027% to 104.2591, BBG AGG APAC Government High Grade USD 0bp to 4.729%.

South Korea’s manufacturing sector saw record-high input price and output charge inflation in April as the Middle East conflict drove raw material supply disruptions. The S&P Global Manufacturing PMI rose to 53.6 points (March: 52.6), marking the strongest expansion since February 2022. Production and new orders increased, partly from clients building safety stocks amid rising costs and shipping delays. Export orders grew modestly, aided by easing U.S. tariff disruptions. Despite higher costs and supply delays, employment rose for the second successive month. Business confidence fell to a five-month low amid uncertainty over the conflict’s duration. KOSPI +5.12% to 6937, USDKRW +0.631% to 1467.6, 10y KTB +7.3bp to 3.915%.

Taiwan’s manufacturing sector grew strongly in April. The S&P Global Taiwan Manufacturing PMI rose to 55.3 points from 53.3 in March, in its strongest improvement since December 2021. Production and new orders increased sharply, driven by stockpiling amid supply chain concerns linked to the Middle East war. New export business expanded substantially across the U.S., Europe, China, Japan and Southeast Asia. Input price inflation hit a near-five-year high due to material shortages and shipping disruptions, causing the steepest rise in selling prices since late 2021. Supplier lead times lengthened significantly, while employment decreased marginally. TAIEX +4.57% to 40705, USDTWD +0.089% to 31.62, 10y TGB -2.5bp to 1.486%.

Hong Kong’s Exchange Fund recorded its smallest quarterly gain in five quarters in Q1. It put on HK$34.5bn, down 56% from HK$79.2bn a year earlier, as the Middle East crisis triggered a stock market slump. Hong Kong stocks lost HK$5bn (vs. a HK$16.4bn gain a year earlier) in Q1. Overseas stocks slid HK$11bn, triple the prior year’s loss. Bond gains were 39% lower at HK$24.6bn. Despite the uncertainties, the local economy and capital markets remain resilient. The fund’s total assets had risen to HK$4.34tn as of end-March. Hang Seng +1.28% to 26107, USDHKD +0.016% to 7.8335, 10y HKGB -1.2bp to 1.417%

The Indonesian manufacturing sector contracted in April, with its PMI falling to 49.1 points from 50.1 in March, marking the first decline in nine months. Production volumes decreased at the fastest pace since May 2025, despite a slight rise in new orders driven by domestic demand. Inflationary pressures intensified, with input cost inflation reaching a four-year high due to the Middle East conflict, leading to the steepest rise in selling prices since 2013. Employment fell modestly, and supplier delivery times lengthened for the seventh consecutive month. Business confidence eased to a five-month low amid concerns over prolonged geopolitical tensions. Elsewhere, Indonesia reported y/y inflation of 2.42% in April, with the m/m rate at 0.13% and the YTD measure at 1.06%. Key contributors included food, beverages and tobacco (+3.06%), transport (+1.61%) and personal care (+11.43%). Core inflation was 2.44% y/y, 0.23% m/m and 1.16% YTD. JCI +0.18% to 6969, USDIDR -0.156% to 17380, 10y IDGB -5.2bp to 6.801%.

Indonesian exports rose by 0.34% y/y to $66.85bn in January-March, driven by a 0.98% increase in non-oil and gas exports to $63.60bn, while oil and gas exports fell 10.58%. Exports declined by 3.10% y/y to $22.53bn in March, with non-oil and gas down 2.52%. Key non-oil export gains included nickel (+60.6%) and animal/vegetable fats and oils (+7.95%), while mineral fuels dropped 8.35%. The top destinations were China ($16.50bn), the U.S. ($7.29bn) and India ($4.50bn), which together accounted for 44.48% of non-oil exports. Manufacturing exports grew by 3.96%, but agriculture and mining exports fell sharply.

Malaysia’s manufacturing sector saw a moderate improvement in April, with the S&P Global Malaysia Manufacturing PMI rising to 51.6 points from 50.7 in March. This represented the fastest output growth since December 2021. Production and new orders increased, driven by stockpiling amid Middle East war-related uncertainties. Export orders declined for the second month in a row, impacted by weaker international demand. Input delivery times lengthened to a near-four-year high, while input cost inflation hit a 45-month peak, pushing charge inflation to a record high. Employment rose modestly, but backlogs increased due to material shortages. Business confidence weakened to an eight-month low. KLCI +0.81% to 1736, USDMYR +0.364% to 3.9573, 10y MGB +2bp to 3.566%.

India’s manufacturing PMI rose to 54.7 points in April from 53.9 in March, marking the second-slowest output growth since October 2022. New orders and production increased but remained among the slowest in over three years. Export orders surged to a seven-month high, driven by demand from Australia, France, Japan, Kenya, China, Saudi Arabia, the UAE and the U.K. Input prices rose at the steepest rate since August 2022, pushing output charges up at the fastest pace in six months, largely due to the Middle East conflict. Employment growth was the strongest in ten months, while input inventories expanded at the slowest pace in nearly five years. SENSEX +0.41% to 77230, USDINR -0.123% to 95.0363, 10y INGB +0.7bp to 7.022%.

The Philippines’ manufacturing PMI fell to 48.3 points in April from 51.3 in March, signaling a moderate contraction – the first since November. New orders declined sharply, including export orders; the fall, which was attributed to trade route closures, was the steepest since mid-2020. Production stagnated (50.0) and input costs rose rapidly, driven by higher energy and shipping expenses linked to the Middle East conflict. Selling prices increased at the fastest pace in 41 months. Inventory levels and staffing were reduced, in the first job cuts in 2026. Despite challenges, business confidence hit a 17-month high, supported by expectations of improved demand. PSEi +1.86% to 5942, USDPHP -0.148% to 61.572, 10y PHGB +5.6bp to 6.897%.

Vietnam’s manufacturing sector saw a decline in new orders in April, the first drop in eight months, as inflation hit a 15-year high on rising fuel and oil costs. The S&P Global Vietnam Manufacturing PMI fell to 50.5 points (from 51.2 in March), which represents a seven-month low. Output growth continued but slowed to a ten-month low. Export orders decreased for the second month, impacted by higher transportation costs. Input and output prices rose sharply, at the fastest pace since April 2011. Employment and purchasing activity were reduced, while supplier delivery times lengthened significantly. Business sentiment weakened to a seven-month low due to Middle East conflict concerns. VN-I -0.02% to 1854, USDVND +0.05% to 26343,10y VGB -0.1bp to 4.226%.

Vietnamese CPI rose by 0.84% m/m in April, 3.31% since December 2025 and 5.46% y/y. For the first four months, CPI increased by an average of 3.99% y/y, with core inflation at 3.89%. The gold price index fell 6.71% m/m in April but rose 10.83% since December 2025 and 54.24% y/y, averaging a 75.13% y/y increase in the first four months. The U.S. dollar price index increased by 0.17% m/m in April, up 1.44% y/y but down 0.31% since December 2025, and averaged a 2.29% y/y rise in the first four months of 2026.

Vietnam’s Index of Industrial Production (IIP) for April rose by 3.0% m/m and 9.9% y/y. Manufacturing and processing grew by 10.0% y/y, mining by 7.6%, water supply and waste management by 7.1% and electricity production and distribution by 10.9%. By region, growth was recorded in Da Nang (+44.2% m/m), Vinh Long (+9.7%), Ho Chi Minh City (+8.2%), Quang Ngai (+4.2%), Dong Nai (+3.6%), Can Tho (+2.0%), Hai Phong (+1.3%) and Bac Ninh (+0.5%), while Quang Ninh declined by 4.1%.