Market Movers: No Change

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

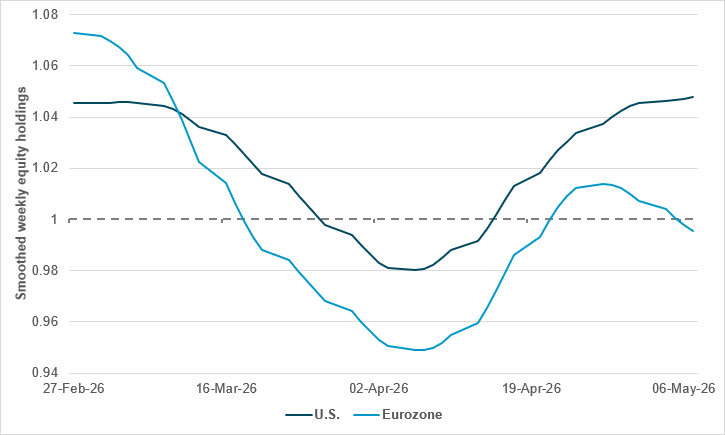

European equity holdings faltering as U.S. recovery continues

Source: BNY

Back in April, when markets rallied upon news of the first ceasefire, we began tracking the state of holdings recovery. We wanted to ascertain whether the improvement in equity and fixed income indices corresponded to asset allocations pushing flows back into the market. There is a longstanding narrative that institutional investors have lagged retail flows, and that divergence appears to have become even more acute of late: institutional investors appear far more concerned about the medium to long-term impact of the conflict on supply chains and feel that risk sentiment is overlooking some of the outstanding risks.

Progress is also uneven across regions. For example, total institutional holdings in the U.S. have largely normalized, while the situation in DM EMEA is very different. Toward the final week of April, only around half of the losses incurred in European holdings since the beginning of the conflict had been recovered. The last two weeks have seen holdings scaled back again given the deterioration in levels, and the gap versus the U.S. is beginning to widen.

While European equities may have started the year on a strong footing, the perception that supply chain issues will damage the region far more is proving difficult to shake off. This is being compounded by a more hawkish push by the region’s central banks: Norges’ hike was a surprise last week, and the market has a June ECB hike as its base case. We expect divergence to continue if these factors remain dominant.

The status quo cannot last, and yet markets remain mixed on risk assets. The rejection of the Iranian peace proposal has pushed oil prices higher, with Brent up 2.5% after testing $105 again. Bond yields globally climbed 1.5-3bp (10y) in response, while within equities China was up 1.6%, with Sweden down 0.4%, Germany flat, Italy up 0.3% and U.S. futures down 0.1%. USD was flat, with CNY at three-year highs and JPY dropping back to 157, while NOK gained ground and India lagged against USD. Drivers beyond the Iran conflict are inflation, including Norges Bank’s hawkish stance, plus U.K. political drama following the local elections, hopes of a Ukraine truce hitting defense shares across Europe, and South Korean trade and Chinese economic data driving equities.

Bottom line: The focus on actual and expected inflation will dominate the week ahead, as investors await the U.S. release tomorrow. The U.S. Treasury sale of $58bn in 3y notes will serve as a guide to measuring nerves. The overnight newsflow highlights the risks associated with the ongoing conflict and the lack of progress over the weekend on resolving it. The silver lining is in the ongoing push from AI that is countering the worst effects from the Iran conflict, leaving mixed equity momentum. Meanwhile, politics and the push for belt-tightening are in evidence in India, where reductions in gold and fuel purchases are the focus. The question today is about the breadth and depth of demand everywhere, with AI shares and oil clearly leading.

U.S.-Iranian tensions remain elevated, after President Trump rejected Tehran’s response to a proposed peace framework aimed at ending the conflict and reopening the Strait of Hormuz, calling it unacceptable. Iranian officials, including Foreign Ministry spokesman Esmail Baghaei, defended their position, demanding sanctions relief, an end to the U.S. naval blockade and a ceasefire across theaters in the region, including Lebanon. The disagreement highlights a significant gap between Washington and Tehran, with Iran also resisting constraints on its nuclear infrastructure while signaling limited concessions. The impasse leaves a fragile ceasefire in place and keeps Hormuz effectively disrupted, prolonging global energy market uncertainty. The dispute is also expected to feature in upcoming U.S.-China discussions, underscoring the broader geopolitical stakes surrounding the conflict. Brent +2.232% to 103.55, WTI +1.981% to 97.31, Omani crude +1.556% to 97.94, Dubai crude +1.473% to 97.585.

Indian Prime Minister Narendra Modi has urged citizens to avoid purchasing gold for at least a year, directly appealing to households to curb demand in order to protect the country’s foreign exchange reserves. Speaking publicly, Modi linked the request to rising external pressures from the Middle East conflict, which has driven up energy costs and widened India’s trade deficit while weakening the rupee. He also called for reductions in fuel consumption and non-essential overseas travel, framing the measures as necessary national adjustments. The intervention is significant given gold’s central role in Indian savings and cultural practices and prompted an immediate market response, with shares in major jewelry companies falling sharply following his comments. Gold -0.811% to 4677.04, silver +0.306% to 80.5842, platinum -1.029% to 2037.5.

The U.K. government aims to attract £99bn in Australian pension fund investment over the next decade for major projects in clean energy, infrastructure, housing and innovation. Investment Minister Lord Stockwood is touring Australia, Malaysia and Singapore to promote the U.K. as a stable and trusted investment destination. Australian pension funds currently hold around £41bn in U.K. assets. The government’s new “Supers Unit” will facilitate increased investment, building on a modern industrial strategy that has secured £360bn in private investment and supported 120,000 jobs. Bilateral trade between the two countries has risen 22% to £24bn since their trade agreement. FTSE 100 +0.14% to 10248, GBPUSD -0.133% to 1.3613, 10y gilt +4.1bp to 4.953%.

The head of the Bank for International Settlements, Pablo Hernandez de Cos, has said countries should keep fiscal spending targeted and temporary to avoid increasing inflationary risks that could force central banks to raise interest rates. He warned that prolonged Middle East disruptions pose risks to global financial stability, especially with rising public debt increasingly held by non-bank financial institutions. While central banks can “look through” temporary supply shocks, persistent shocks may trigger harmful inflation effects, requiring policy action. De Cos highlighted the need for careful monitoring amid market optimism and high volatility. MSCI World 0.21% to 1106, DXY +0.065% to 97.963, BBG Global Aggregate 0bp to 3.757%.

ECB policymaker Martin Kocher has warned that the ECB may soon be forced to raise interest rates if energy prices do not ease, explicitly linking the policy outlook to ongoing geopolitical tensions and their impact on inflation. In his remarks, Kocher emphasized that while euro area growth and labor markets remain relatively resilient, the persistence of elevated energy costs could heighten stagflation risks and trigger broader second-round price pressures. He framed the ECB’s previous decision to delay tightening as appropriate given only moderate inflation dynamics at the time, but signaled a clear shift toward readiness to act in the near term. His comments underscore increasing concern within the ECB about inflation persistence and the need for timely policy intervention if conditions do not improve. Euro Stoxx 50 -0.36% to 5890, EURUSD -0.06% to 1.178, BBG AGG Euro Government High Grade EUR 0bp to 3.254%.

U.S. April existing home sales are forecast to rise 2.0% m/m, 4.05 million vs. -3.6% m/m, 3.98 million.

Canada Bloomberg Nanos Confidence is expected at 49 vs. 50.0.

U.S. Treasury sells $89bn in 13-week bills, $77bn in 26-week bills and $58bn in 3y notes.

Mood: Risk sentiment has continued to deteriorate, with further equity outflows alongside sustained demand for core government bonds. iFlow Mood: -0.036.

FX: Strong USD inflows, against broad-based selling across the iFlow universe. EUR, GBP, COP, MXN and SGD saw the heaviest outflows.

FI: Widespread buying in government bonds, led by the Eurozone, Sweden, Mexico, Hungary and the U.K., followed by U.S. Treasurys. Selective selling in Australia, Indonesia, China and Malaysia.

Equities: Selling pressure was concentrated in EMEA, South Korean, Swedish and broader European/U.K. equities, while the U.S., China and Thailand saw sizable inflows.

“Although there is no progress without change, not all change is progress.” – John Wooden

“When we are no longer able to change a situation, we are challenged to change ourselves.” – Viktor Frankl

The U.K. KPMG and REC Report on Jobs for April shows permanent staff appointments fell at the fastest pace since January, driven by heightened uncertainty from the Iran war and rising business costs. Despite this, the decline was slower than typical 2025 levels. Temporary billings rose slightly for the first time in three months as firms favored flexible staffing. Overall demand for workers continued to contract for a 30th consecutive month, but at the softest rate in nearly a year. Candidate availability increased markedly due to redundancies and lower demand. Pay growth for permanent and temporary roles remained weak but improved modestly from March. FTSE 100 +0.14% to 10248, GBPUSD -0.133% to 1.3613, 10y gilt +4.1bp to 4.953%.

Norway’s headline CPI rose 3.4% y/y in April, down 0.2 percentage points from March, reflecting lower energy prices. A decline in fuel and electricity costs, including tax cuts on petrol and diesel, was the primary driver dampening overall inflation, with fuel prices falling sharply m/m. Electricity prices also contributed to the softer y/y reading. In contrast, core inflation as measured by CPI excluding energy and tax changes rose to 3.2% y/y, up 0.2 percentage points from March. This increase was largely driven by food prices, which jumped 6.1% y/y, reversing earlier promotional effects. Monthly CPI rose 0.4%, with cheaper airfares and household goods partially offsetting broader price pressures. OSE +0.18% to 1974, EURNOK -0.148% to 10.8417, 10y NGB +3.9bp to 4.411%.

Norway’s producer price index recorded a 7.4% y/y rise in April, driven primarily by strong price gains in export-oriented industries. Export prices rose sharply (+7.2% m/m), reflecting renewed volatility in global commodity markets, particularly for metals and refined petroleum products. Prices for refined petroleum surged by 47.3% in April, following earlier increases in crude oil and natural gas, while export metal prices rebounded by 7.6% after a prior decline. On a y/y basis, export prices increased by 8.2%, with particularly strong gains in food manufacturing at 13.8% and metals at 10.6%. Chemical industry prices remained comparatively weak despite a modest monthly uptick, highlighting uneven dynamics across different sectors of Norwegian industry.

Czech retail sales were up 4.9% y/y and 1.2% m/m in real terms in March, indicating continued consumer demand strength. Growth was broad-based, with y/y rises of 5.5% for non-food sales, 4.8% for food sales and 2.6% for automotive fuel. On a m/m basis, food sales led gains at 1.8%, followed by non-food goods at 1.0%. E-commerce remained a key driver, with internet and mail order sales surging 13.4% y/y, while non-specialized stores also contributed strongly. Sector performances were mixed, with falls in clothing and footwear offset by gains in cosmetics and pharmaceuticals. Motor vehicle sales were comparatively subdued, rising 2.0% y/y and remaining flat m/m. Prague SE -0.8% to 2515, EURCZK +0.029% to 24.317, 10y CZGB +5.5bp to 4.85%.

Türkiye’s trade sales volume index showed total trade sales rising 1.7% y/y in March, while retail sales volume surged 21.2% y/y, highlighting strong consumer demand. In contrast, motor vehicle trade and repair contracted by 10.3% y/y and wholesale trade by 3.5%, indicating divergence across sectors. On a m/m basis, total trade sales increased by 1.9%, driven by a 2.6% rise in retail and a 2.4% increase in wholesale activity, while motor vehicle sales fell 2.9%. The data suggest retail strength is the primary growth driver, offsetting weakness in autos and wholesale segments, with momentum remaining positive into the end of Q1. BI 100 +0.17% to 15088, USDTRY +0.056% to 45.3822, 10y TGB +11bp to 33.71%.

Türkiye’s total turnover rose 34.6% y/y in March, reflecting strong nominal activity across sectors, and was up 4.4% m/m. The y/y expansion was broad-based, led by services at 36.5% and trade at 35.9%, with industrial turnover up 33.2% and construction a somewhat softer 22.0%. On a m/m basis, growth was driven by industry, which rose 5.7%, and trade at 4.9%, while services increased by 2.8%. Construction turnover declined by 0.9% m/m, indicating some softness in the sector. Overall, the data point to continued strong nominal demand conditions, with services and trade acting as key growth engines despite mixed short-term momentum across sectors.

China’s CPI rose 0.3% m/m, 1.2% y/y, 0.9% YTD y/y in April (March: -0.7% m/m, +1.0% y/y, +0.9% YTD y/y). Services items and consumables inflation both rose by 0.1 percentage points to 0.9% and 1.4% y/y, respectively. Core inflation came in at 0.2% m/m, 1.2% y/y, 1.2% YTD y/y (March: -0.7% m/m, +1.1% y/y, +1.2% YTD y/y). Food prices fell 1.6% y/y and m/m, mainly due to y/y falls of 15.2% for pork and 6.7% y/y for livestock meat, while non-food prices rose 1.8% y/y. Services increased by 0.9% y/y. On a m/m basis, CPI rose 0.3%, driven by a 0.7% rise in non-food prices despite a 1.6% fall in food prices. Key contributors to inflation included transportation (+4.6% y/y) and healthcare (+2.2% y/y), while housing costs came down slightly (-0.2% y/y). CSI 300 +1.64% to 4952, USDCNY +0.071% to 6.7957, 10y CGB -0.4bp to 1.756%.

China’s PPI rose 1.7% m/m, 2.8% y/y, 0.2% YTD y/y in April vs. 1.0% m/m, 0.5% y/y, -0.6% YTD y/y. This is the first positive YTD y/y reading since December 2022. The rise was driven by higher prices in mining (+10.6% y/y), raw materials (+7.1%) and chemical products, supported by international oil price increases and stronger domestic demand in sectors such as electric machinery and computing. Conversely, prices for consumer goods such as food (-1.9% y/y) and clothing (-1.1% y/y) fell. Input prices also climbed 2.1% m/m, 3.5% y/y and 0.5% YTD y/y, with substantial rises for non-ferrous metals (+21.3% y/y) and chemical raw materials (+5.9% y/y).

China’s trade balance for April was $84.82bn, up from $51.13bn in March. Exports rose 14.1% y/y to $359.44bn (March: 2.5%, April 14.5% YTD y/y), while imports increased by 25.3% y/y to $274.62bn (March: 27.8%, April 23.6% YTD y/y). Key export destinations included the U.S. (-10% YTD y/y, trade surplus: $23.07bn), Hong Kong (41.1% YTD y/y, $33.60bn), ASEAN (19.1% YTD y/y, $26.85bn) and the EU (19% YTD y/y, $30.04bn). Imports of crude oil fell 23% m/m to 38.47 million tons, while soybean imports surged 110.9% m/m to 8.48 million tons. Export volumes of steel and refined oil products declined, whereas fertilizer and rare earth exports increased.

In Hong Kong, special asset bankers are intensifying efforts to resolve a HK$200bn bad debt pile, driven largely by losses in commercial real estate. The city’s distressed loan ratio reached 2.01% at end-2025, the highest figure since 2004. Several banks, including Bank of East Asia and United Overseas Bank, have expanded their special asset teams to accelerate collateral sales and borrower liquidations. Despite a recovering residential market, commercial property vacancies remain elevated at 16.8% (March 2025). The shift reflects a move from patience to decisive action to cut losses and free up capital in the context of an economic rally and looming infrastructure projects. Hang Seng +0.03% to 26401, USDHKD +0.012% to 7.8285, 10y HKGB -1.2bp to 1.417%.

South Korean exports in the first ten days of May surged 43.7% y/y to $18.4bn, driven by a semiconductor boom with shipments up 149.8% y/y to $8.5bn – a record high for May. Semiconductor exports accounted for 46.3% of total exports, up 19.6 percentage points. Exports to key destinations rose sharply: China (+81.8%), Vietnam (+89.3%), the U.S. (+17.9%), Taiwan (+96.7%) and the EU (+11.3%). Imports increased by 14.9% to $16.7bn, led by semiconductors, crude oil and petroleum products. The trade surplus for May 1-10, 2026, was $1.7bn. KOSPI +4.32% to 7822, USDKRW -0.683% to 1472.15, 10y KTB +2.8bp to 3.904%.

South Korea has reinstated a heavier capital gains tax on multiple-homeowners from this month, ending a four-year suspension. The surtax adds 20 percentage points for owners of two homes and 30 points for those with three or more, on top of the basic 6% capital gains tax and 10% local income tax, pushing the top effective rate to about 82.5%. The suspension, in place since May 2022 to boost property transactions, has now expired. Exceptions apply for sellers with firm plans or completed transfers by May 9. New transaction deadlines apply in 33 regulated districts, including tighter rules in Seoul’s prime areas.

Bank Indonesia’s April Consumer Confidence Survey shows consumer confidence edged up to 123.0 points from 122.9 in March, remaining in optimistic territory (index >100). The current economic condition index rose to 116.5 (115.4 in March), supported by improvements in employment and durable goods purchase indices. However, the consumer expectations index edged down to 129.6 from 130.4. Current income expectations and business activity outlooks also softened slightly. Overall, the data indicate sustained consumer optimism regarding Indonesia’s economy in April. JCI -0.39% to 6942, USDIDR -0.247% to 17416, 10y IDGB +1.3bp to 6.616%.

Former RBI Governor Duvvuri Subbarao has advised the Reserve Bank of India to reduce currency intervention and allow the rupee to weaken, enabling proper price signals amid rising import costs and foreign outflows. He emphasized that market participants must adapt to two-way rupee movements for India to develop economically. Subbarao suggested that interest rate hikes should be a last resort, given India’s current robust growth and low inflation. He also recommended a gradual approach to capital account liberalization, warning against aggressive measures that could destabilize markets. The rupee has weakened by about 5% this year due to energy import vulnerabilities. SENSEX -1.15% to 76442, USDINR -0.709% to 95.1575, 10y INGB +4.7bp to 7.028%.