Market Movers: Excitement

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 7 minutes

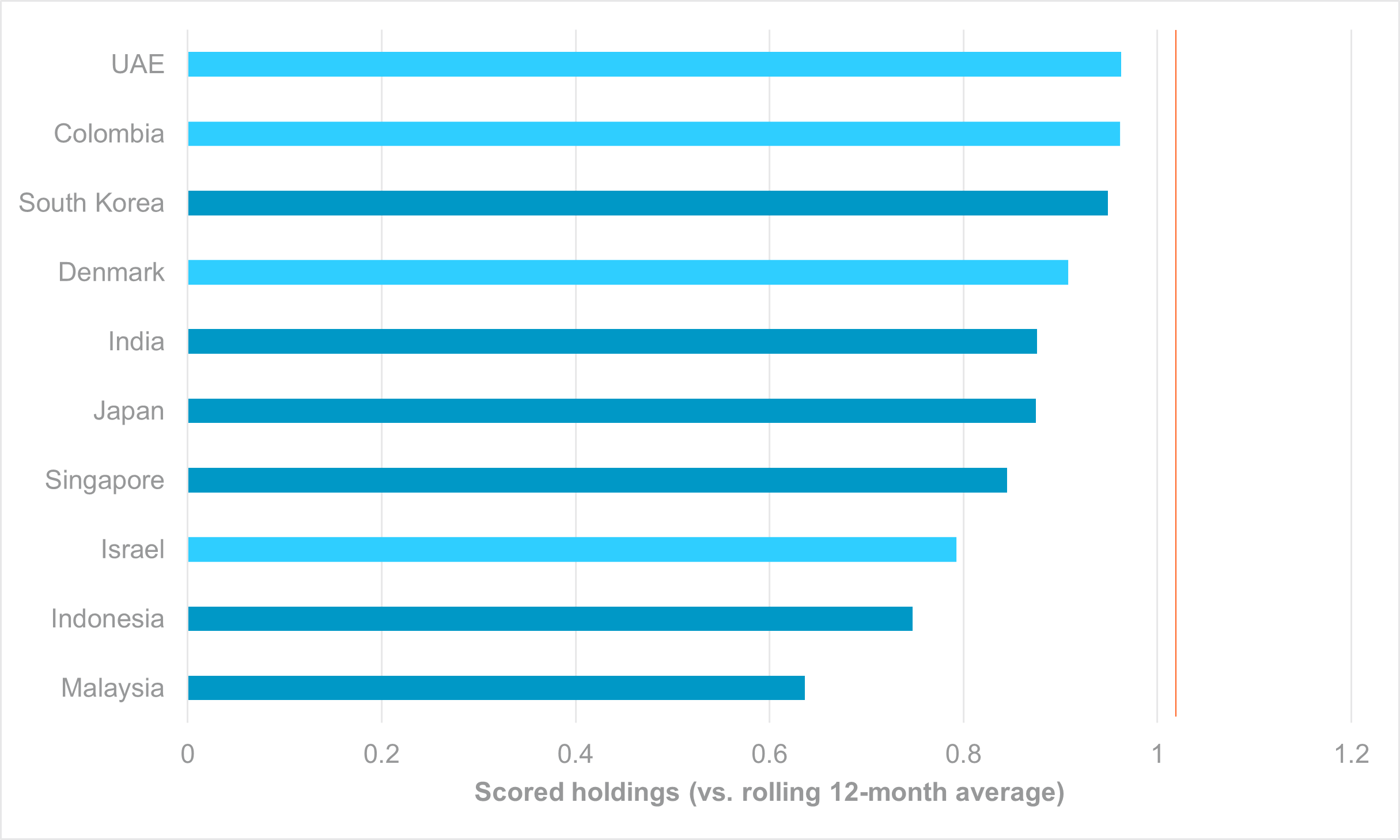

APAC names dominate worst-held bond markets

Source: BNY

Headlines remain mixed, but recent developments suggest the U.S. and Iran may be moving gradually toward some form of agreement, triggering a sharp decline in oil prices and an immediate improvement in equity sentiment. While elevated inflation is still likely to sustain a higher risk premium across global markets through reduced scope for policy easing, there is now greater potential for a relief rally in assets most exposed to the Gulf conflict. Markets currently appear focused on identifying the most vulnerable legacy positions, although secular themes such as AI and semiconductors would likely have continued attracting capital regardless of geopolitical developments. The larger rebound opportunity instead lies in the areas most heavily sold off on supply shock concerns.

Within FX, APAC remains the weakest-held regional complex. Economies with high sensitivity to balances of payments, such as IDR and INR, have shifted from overheld to underheld territory, while even savings-heavy economies have weakened due to import-driven inflation pressures. KRW, JPY and SGD remain the only overheld currencies in the region, though all face additional idiosyncratic headwinds. Fixed income positioning shows a similar pattern, with five of the six most underheld bond markets belonging to APAC net energy importers. Markets are continuing to price in a highly defensive outlook on real rates and fiscal risks, leaving these under-owned markets well-positioned for a strong recovery should energy prices continue to moderate.

Tech earnings surprising to the upside are no longer eliciting excitement. Instead, the story is one of new opportunities from tech and AI-driven IPOs, coupled with hopes that the U.S. and Iran are inching closer to a permanent settlement. Although markets are begrudgingly pricing in more sustained supply disruptions, the prospect of the Strait of Hormuz reopening soon and the removal of idiosyncratic supply factors are the most essential elements. The reaction in South Korean equities – with the KOSPI increasingly acting as a bellwether for sentiment through the day – is telling: the index rallied by 8.12% overnight, the single biggest daily gain since April 1. Relief through the crude import channel is essential for much of Asia in loosening financial conditions, and performance has been complemented by news of suspension of industrial action in the semiconductor industry. Nonetheless, price risks from the conflict, resource demands and secondary price effects from the AI investment boom (e.g., a 68th straight month of house price gains in Seoul) will continue to create challenges as policymakers and governments respond to embedded inflation expectations amid constraints to household disposable income.

Pakistan’s Army Chief Asim Munir is visiting Tehran today for meetings with senior Iranian officials as Islamabad steps up mediation efforts between Iran and the U.S. in the ongoing ceasefire and nuclear negotiations. The visit comes immediately after Pakistani Interior Minister Mohsin Naqvi’s second trip to Tehran in less than a week, highlighting Pakistan’s increasingly active diplomatic role in facilitating communication between the two sides. Iranian media has reported that Tehran is currently reviewing updated U.S. “viewpoints” following several rounds of indirect exchanges based on Iran’s earlier 14-point proposal. President Trump said negotiations are in their “final stages” but stressed there was no urgency to conclude an agreement. Washington has reportedly offered slightly improved incentives on frozen assets and sanctions relief, although no additional concessions have been made regarding Iran’s nuclear program, leaving key areas of disagreement unresolved despite the intensifying diplomatic activity. Brent +0.572% to 105.62, WTI +0.723% to 98.97, Omani crude -0.414% to 105.92, Dubai crude -1.921% to 103.314.

ADNOC CEO Sultan Ahmed Al Jaber has said the UAE is nearly halfway to completing a second oil pipeline designed to bypass the Strait of Hormuz, as Gulf producers accelerate efforts to reduce reliance on the waterway in the wake of the Iran conflict. Speaking at the Atlantic Council, Al Jaber said the new pipeline would double ADNOC’s export capacity through Fujairah on the Gulf of Oman and is expected to become operational in 2027. The project has been fast-tracked after Iran’s blockade of the strait disrupted regional energy exports and triggered what Al Jaber described as the most severe energy supply shock in history. He estimated that more than one billion barrels of oil exports have already been lost, with nearly 100 million additional barrels disrupted each week that the strait remains closed. He warned that even if the conflict were to end immediately, restoring oil flows to near-normal levels would take months, while U.S. Energy Secretary Chris Wright argued the crisis will ultimately accelerate investment in alternative export routes across the Gulf region.

ECB Governing Council member Olli Rehn has said the European Central Bank could raise interest rates in June to preserve credibility following the recent oil price shock. He also stressed, however, that there was still limited evidence that elevated inflation was becoming entrenched in the euro area. Speaking to Reuters, the Finnish central bank governor said medium and long-term inflation expectations remained anchored around the ECB’s 2% target, while wage growth continued to moderate despite short-term inflation pressures linked to disruptions in the Strait of Hormuz. Rehn warned that the euro area was moving closer to the ECB’s adverse scenario of weaker growth and higher inflation, with the June decision also dependent on updated staff projections and geopolitical developments involving Iran. He emphasized that the ECB would act independently of market pricing and highlighted risks of a prolonged energy supply shock for Europe, particularly for Germany, Italy and Central Europe. Euro Stoxx 50 -0.15% to 5967, EURUSD 0% to 1.1624, BBG AGG Euro Government High Grade EUR +2.5bp to 3.429%.

U.K. Chancellor Rachel Reeves is set to announce a package of cost-of-living measures aimed at cushioning households from the economic impact of the Iran conflict and higher energy prices, as the government seeks to avoid a broader inflation shock. Measures branded as “Great British Summer Savings” include free bus travel for children during August, potential cuts to agri-food tariffs on more than 100 imported products and an extension of the fuel duty freeze until year-end. Reeves said the priority was protecting households from rising costs while avoiding large-scale support measures that could worsen inflation or destabilize markets. The Treasury is resisting a repeat of the expansive energy bailout introduced after Russia’s invasion of Ukraine, preferring targeted interventions instead. Officials are also considering contingency plans ahead of a likely rise in the U.K. energy price cap in July, while concerns remain over the inflationary effects of supermarket price controls and prolonged disruption to energy supplies through the Strait of Hormuz. FTSE 100 -0.42% to 10389, GBPUSD +0.067% to 1.3444, 10y gilt -2.8bp to 4.96%.

U.S. initial jobless claims are expected at 210k vs. 211k.

U.S. May Philadelphia Fed Business Outlook is expected to ease to 17.6 points vs. 26.7.

U.S. April housing starts are expected to ease to 1.419 million vs. 1.502 million.

U.S. April preliminary building permits are expected to rise to 1.383 million vs. 1.363 million.

U.S. May preliminary S&P Manufacturing PMI is expected to ease to 53.8 vs. 54.5.

U.S. May preliminary S&P Services PMI is expected to rise to 51.1 vs. 51.0.

U.S. May Kansas City Fed Manufacturing Activity is expected at 8 vs. 10.0.

Central bank speakers: BoE rate-setter Alan Taylor delivers a speech at the Market News International event.

U.S. Treasury sells $100bn in 4-week bills, $95bn in 8-week bills and $19bn in a 10y TIPS reopening.

Mood: Risk-off sentiment is deepening: iFlow Mood fell to -0.245 as equity outflows accelerated, despite steady demand for core government bonds.

FX: Demand for G10 FX has returned with broad-based buying, except for JPY, DKK and CAD, which posted outflows. Elsewhere, positioning across EMEA, LatAm and APAC remained skewed to the sell side, led by SGD and TRY.

FI: Selling pressure in EMEA fixed income dominated flows, led by outflows from Hungary and Türkiye, alongside Brazilian, Peruvian and Japanese government bonds. In contrast, inflows were concentrated in Eurozone and Colombian government bonds, U.K. gilts and U.S. Treasurys.

Equities: Heavy selling persisted in South Korean, Japanese and Polish equities, followed by U.S. equities, while strong inflows were seen in China, Singapore and Thailand. Within DM EMEA, flows showed solid demand for the energy, industrials, consumer discretionary, healthcare and financials sectors.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” – Benjamin Graham

“The desire to perform all the time is usually a barrier to performing over time.” – Robert Olstein

Eurozone flash PMI data for May pointed to a deepening economic downturn, with the composite output index falling to 47.5 points from 48.8 in April, its weakest level in 31 months. The deterioration was driven primarily by the services sector, where activity declined to a 63-month low of 46.4, while manufacturing growth slowed sharply, with output barely remaining in expansion territory and the manufacturing PMI easing to 51.4. Businesses reported falling demand, worsening export orders and declining employment as higher energy costs and geopolitical uncertainty linked to the Middle East conflict weighed on activity. Input cost inflation accelerated to its highest level in three and a half years due to rising energy prices, supply shortages and severe supply chain disruptions, while selling price inflation also remained elevated. Employment fell for a fifth consecutive month and at the fastest pace since late 2020, with France and Germany both recording job losses. Business confidence weakened further, signaling increasing recession risks for the euro area economy in Q2. Euro Stoxx 50 -0.15% to 5967, EURUSD 0% to 1.1624, BBG AGG Euro Government High Grade EUR +2.5bp to 3.429%.

Germany’s flash PMI data for May indicated that private sector activity contracted for a second consecutive month, with the composite output index edging up only slightly to 48.6 points from 48.4 in April, remaining below the 50-point threshold that separates growth from contraction. The weakness continued to be driven by the services sector, where business activity fell to 47.8, while manufacturing momentum also faded sharply as output growth nearly stalled and the manufacturing PMI slipped back below neutral to 49.9. Firms reported weaker domestic and export demand amid heightened geopolitical uncertainty, rising energy costs and pressure on household spending power linked to the disruption in the Strait of Hormuz. Inflation pressures intensified further, with input cost inflation accelerating to its fastest pace in three and a half years due to higher commodity, transport and energy costs coupled with supply shortages. Despite elevated costs, businesses slowed the pace of output price increases, suggesting margin compression. Employment conditions deteriorated substantially, with job cuts accelerating to their fastest pace in more than 18 months, particularly in manufacturing. DAX -0.08% to 24719, EURUSD 0% to 1.1624, 10y Bund -2.4bp to 3.072%.

France’s flash PMI data for May signaled a sharp deterioration in private sector activity, with the composite output index falling to 43.5 from 47.6 in April, the weakest reading since November 2020. The decline reflected a broad-based slowdown across both services and manufacturing, as the services business activity index dropped to 42.9 while manufacturing output fell back into contraction territory at 46.4. The headline manufacturing PMI also slipped to 48.9. Firms widely cited the inflationary impact of the Middle East conflict, with higher fuel and energy costs weighing heavily on demand, output and confidence. New orders recorded their steepest fall since late 2020, particularly in services, while export demand also weakened sharply. At the same time, inflation pressures intensified, with input costs and selling prices rising at their fastest pace in at least three years, especially for energy, transport and metal-related inputs. Business expectations turned negative for the first time since late 2024, reflecting rising recession risks for the French economy. CAC 40 -0.18% to 8103, EURUSD 0% to 1.1624, 10y OAT -1.7bp to 3.701%.

Italy’s balance of payments data for March showed a continued improvement in the external position, with the 12-month rolling current account surplus rising to €31.6bn, equivalent to 1.4% of GDP, from €19.0bn a year earlier. The improvement was driven mainly by a stronger goods surplus, which increased to €53.0bn, and a recovery in primary income balances, while the services deficit widened only slightly. In March alone, the current account posted a surplus of €1.7bn. On the financial account side, Italy recorded net acquisitions of foreign assets worth €34.7bn over the previous 12 months, supported primarily by direct investment outflows and other investment flows, partly offset by portfolio investment outflows. During March, Italian residents increased their foreign asset holdings by €25.3bn, largely through portfolio and direct investment abroad, while foreign liabilities rose €28.8bn, mainly due to other investment inflows despite net foreign sales of Italian government bonds. FTSE MIB -0.11% to 49126, EURUSD 0% to 1.1624, 10y BTP -1.9bp to 3.808%.

U.K. flash PMI data for May indicated that private sector activity contracted for the first time in over a year, with the composite output index falling sharply to 48.5 points from 52.6 in April. The downturn was driven by a steep deterioration in the services sector, where business activity dropped to 47.9, its weakest level since early 2021, as firms cited weaker consumer spending, subdued investment sentiment and heightened uncertainty linked to the Middle East conflict and domestic politics. In contrast, manufacturing output strengthened modestly, supported by precautionary stock building and customer front-loading ahead of expected price increases and supply disruptions, leaving the manufacturing PMI unchanged at 53.7. Inflation pressures remained elevated, with firms reporting higher fuel, transport, energy and raw material costs, while supply chain disruptions intensified further. Employment declined for a 20th consecutive month, led by service sector job cuts, and business confidence weakened to its lowest level since April 2025, pointing to growing recession risks alongside persistent inflationary pressure. FTSE 100 -0.42% to 10389, GBPUSD +0.067% to 1.3444, 10y gilt -2.8bp to 4.96%.

Swiss industrial production contracted sharply in Q1, with overall industrial output falling 7.1% y/y after a 0.4% decline in the previous quarter, highlighting broad weakness across manufacturing. Production in the wider secondary sector, covering industry and construction, declined 6.1%. Manufacturing output dropped 7.2%, driven by a steep 20.4% fall in pharmaceutical production, which heavily weighed on the aggregate result. Other weak areas included chemicals, rubber and plastics, and wood and paper products. In contrast, several export-oriented segments remained resilient, with metal products rising by 8.8%, electronics by 6.6% and electrical equipment by 6.3%. Construction activity was still positive overall, supported by gains in building construction and civil engineering, while electricity supply contracted by 6.9% y/y. SMI +0.04% to 13405, EURCHF -0.061% to 0.91434, 10y Swiss GB +2bp to 0.547%.

Swedish labor market data for April pointed to continued weakness, with unemployment remaining elevated despite some improvement in seasonally adjusted figures. The number of employed people aged 15 to 74 was 5.226 million on a non-seasonally adjusted basis, while the unemployment rate was 8.7%, equivalent to 500,000 unemployed individuals. Seasonally adjusted and smoothed data showed the unemployment rate easing to 8.6% and the employment rate at 69.2%. Statistics Sweden noted that technical collection problems during the Labor Force Survey may have led to an underestimation of employment and permanent staff numbers, warranting caution around the estimates. Permanent employment fell by 88,000 y/y to 4.086 million, while temporary employment has increased in recent months. Youth unemployment remained particularly high at 26.5%, and the unused labor supply corresponded to 565,000 full-time jobs. OMX -0.03% to 3099, EURSEK +0.117% to 10.8672, 10y Swedish GB -5.1bp to 2.852%.

Poland’s construction and assembly production increased by 4.5% y/y in constant prices in April, rebounding from weak earlier trends and rising 9.7% compared with March. Seasonally adjusted output was up 3.1% y/y and 3.4% m/m, indicating a modest improvement in underlying activity. Growth was recorded across all major construction segments, led by building construction at 5.2% and followed by specialized construction activities at 4.4% and civil engineering at 3.9%. Investment-related construction work remained the key source of strength, rising 13.0% y/y, while restoration work fell 15.4%. Despite the stronger April reading, cumulative construction output for January to April was still down 5.8% compared with the same period last year, reflecting continued weakness in restoration activity and broader softness earlier in the year. Civil engineering output also posted a sharp 25.3% m/m increase in April, highlighting improving momentum in infrastructure-related projects. WIG -0.44% to 133095, EURPLN +0.038% to 4.2475, 10y PGB -0.5bp to 5.923%.

Poland’s industrial production rose 3.1% y/y in April, accelerating from a 1.2% increase a year earlier, although output fell 7.4% vs. March, due largely to base effects. Seasonally adjusted industrial production increased by 2.5% y/y but declined by 2.6% m/m, indicating softer underlying momentum. Growth was driven primarily by intermediate goods production, which rose 7.3% y/y, alongside gains in energy output and capital goods production. By sector, the strongest increases were recorded in coal and lignite mining, other transport equipment, waste management activities, machinery and equipment, and basic metals production. Weakness remained concentrated in durable consumer goods, which fell 7.9% y/y, while falls were also recorded in furniture, beverages and motor vehicle production. For the January-April period, industrial production was up 3.0% compared with the same period in 2025, suggesting manufacturing activity remained resilient overall despite monthly volatility and uneven performances across sectors.

Poland’s enterprise sector employment remained broadly stagnant in April, while wage growth continued to moderate. Average paid employment stood at 6.386 million full-time equivalents, unchanged from March but 0.9% lower than a year earlier, extending the gradual softening trend in labor demand. Meanwhile, average monthly gross wages and salaries rose 5.4% y/y to PLN 9,530.74, although they were down 1.3% vs. March as bonus and award payments returned to normal following elevated first-quarter payouts. Statistics Poland noted that the earlier increase in the statutory minimum wage to PLN 4,806 in January continued to influence wage dynamics. For the January-April period, average employment was down 1.0% y/y, while average wages increased by 5.9% y/y. The data suggest that while labor market conditions remain relatively stable, hiring momentum continues to weaken and wage pressures are gradually easing from their previous high levels.

Japanese trade statistics for April showed total exports at ¥10.51tn, up 14.8% y/y (March: 11.7% y/y), and imports at ¥10.21tn, up 9.7% y/y (March: 10.9% y/y). The trade balance came in at a surplus of ¥302bn, reversing from a deficit of ¥150bn in April 2025 and a surplus of ¥667bn in March. Key export destinations included Asia (+16.1% y/y), led by China (+15.5%) and Taiwan (+27.6%), alongside North America (+12.9%), Western Europe (+22.4%) and ASEAN (+19.9%), while Middle East-bound exports declined by 55.5%. Major export sectors were electrical machinery (+28.6%), transport equipment (+6.0%) and machinery (+12.5%). Imports saw declines in mineral fuels (-19.3%), driven by petroleum (-49.9%) and LNG (-20.2%), while electrical machinery (+30.3%) and machinery (+22.8%) imports rose sharply. Nikkei +3.14% to 61684, USDJPY -0.032% to 159.05, 10y JGB -0.7bp to 2.776%.

Japanese private sector growth slowed to a five-month low in May, with the S&P Global Flash Composite PMI Output Index falling to 51.1 points (April: 52.2). Manufacturing drove modest expansion (PMI 54.5 vs. 55.1), while services stagnated at 50.0 after 13 months of growth. Input costs surged at the fastest pace since October 2022, largely due to Middle East conflict-related supply disruptions, leading to the sharpest rise in selling prices on record. New business growth softened, especially in services, and export orders rose slightly. Job creation continued but at a seven-month low. Business confidence remained subdued amid geopolitical uncertainty.

Japan’s total machinery orders rose 4.3% m/m (seasonally adjusted) in March, with a 10.3% q/q increase in January-March. Private sector orders, excluding the volatile shipbuilding and electric power sectors, fell 9.4% m/m but grew 6.4% q/q. On a y/y basis, core private machinery orders increased by 5.9% in March. Manufacturing orders declined by 14.2% m/m but rose 11.5% y/y, while non-manufacturing orders were down 6.0% m/m but up 4.8% y/y. Foreign orders surged by 31.0% m/m and 86.8% y/y. For April-June, total machinery orders are forecast to fall by 1.8%, with private sector orders expected to rise 0.3% q/q.

In April, new condominium launches in the Tokyo metropolitan area (Tokyo, Kanagawa, Saitama, Chiba) rose 15.6% to 1,163 units (April 2025: 1,006 units). The average price was ¥87.36mn, up 24.8% y/y but below ¥100mn for the first time in three months. The price per square meter increased for the 12th consecutive month to ¥1.306mn. The initial contract rate fell to 62.3%, down 4.0 percentage points y/y. Inventory decreased slightly to 6,313 units. Tokyo’s share was 40.8%, with the six central wards averaging ¥224.26mn per unit. May launches are forecast at around 1,500 units.

Japanese portfolio investment update for the week to May 15: The standout trend over the past week was the continued strong foreign demand for Japanese equities, marking the seventh consecutive week of net inflows. Foreign investors bought ¥950bn of Japanese equities, bringing cumulative YTD inflows to a record ¥10.744tn. In contrast, foreigners remained net sellers of Japanese bonds (-¥1.033tn), though flows continue to lack a clear directional trend. Japanese investors continued to buy foreign bonds amid higher UST yields, albeit at a slower pace, while flows into foreign equities remained broadly neutral.

Australia’s seasonally adjusted unemployment rate rose to 4.5% in April from 4.3% in March, with employment falling by 18,600 (-0.1% m/m vs 23.3k in March). The unemployment count increased by 33,000, driven by rises in both full-time and part-time jobseekers. The underemployment rate slightly decreased to 5.8%. Despite lower employment, total hours worked rose by 0.8% m/m, with hours worked per person up 0.9%. Trend unemployment remained steady at 4.3%, with trend employment growing 0.2% m/m. The participation and underemployment rates remained unchanged at 66.7% and 5.9%, respectively. ASX -0.42% to 5575, AUDUSD -0.155% to 0.7114, 10y ACGB -10.5bp to 4.965%.

The Australian private sector contracted in May, with the S&P Global Flash Australia Composite PMI Output Index falling to 47.8 points (April: 50.4). Services activity declined to 47.7 (April: 50.7), while manufacturing output remained subdued at 48.5 (April: 48.5). New business dropped at the fastest pace since September 2021, driven by market uncertainty linked to the Middle East conflict. Employment fell for the first time since late 2024, with job losses in both services and manufacturing. Inflationary pressures persisted, in particular from fuel, raw materials and transportation costs, though input price inflation eased slightly from prior months.

New Zealand goods exports rose 12% y/y to $8.6bn in April, led by milk powder, butter and cheese (+7% y/y to $2.3bn). Exports to China increased by 3.9% y/y, driven by dairy, meat and seafood, while Australia (+27% y/y), the U.S. (+19% y/y) and the EU (+30% y/y) saw substantial export growth. Exports to Japan fell 9.8% y/y. Imports rose 3.4% y/y to $6.7bn, with significant increases from China (+13%) and the EU (+17%), but declines from the U.S. (-39%) and Australia (-1.9%). The trade surplus hit new record highs at $1.9bn in April. NZX 50 +0.92% to 12878, NZDUSD +0.172% to 0.5855, 10y NZGB -9.2bp to 4.711%.

South Korean exports rose 65% y/y in the first 20 days of May, reaching $52.7bn, the highest ever for this period. Semiconductor exports surged 202% to $21.9bn, accounting for 41.7% of total exports, while petroleum product exports increased by 46.3% to $3.23bn. Automobile exports fell 10.1% to $2.76bn. Imports rose 29.3% to $41.6bn, resulting in an $11bn trade surplus. Key export destinations saw significant growth: China (+96.5%), the U.S. (+79.3%), Vietnam (+70.2%) and the EU (+21.7%). Cumulative exports reached $359.1bn, up 43.9% y/y. KOSPI +8.42% to 7816, USDKRW -0.608% to 1506.15, 10y KTB -1bp to 4.195%.

Seoul apartment prices rose 0.31% in the week to May 18 – the fastest weekly increase since January 26 and the 68th consecutive week of appreciation. Nationwide, apartment prices were up 0.07%. Despite government measures to curb speculative demand, strong demand in redevelopment areas is supporting price growth. Rising property prices and inflationary pressures from the Middle East conflict pose challenges for the BoK’s policy outlook, with a rate hike expected by year-end after it held rates at 2.5% in April.

South Korea’s producer price index rose by 2.5% m/m and 6.9% y/y in April (from 1.7% m/m and 4.1% y/y in March). This is the sharpest m/m increase since February 1998, when the index also rose 2.5% amid a global financial crisis. Manufacturing products led with a 4.4% m/m increase, while agricultural, forestry and marine products declined by 1.0% m/m. The domestic supply price index surged 5.2% m/m and 9.9% y/y, driven by a 28.5% m/m rise in raw materials. The total output price index increased by 3.9% m/m and 13.8% y/y. These preliminary figures indicate broad-based price pressures across production stages, especially in manufacturing and raw materials.

The RBI is considering measures to stabilize the rupee, including a potential interest rate hike at its June 5 meeting, raising dollars from overseas investors via a deposit scheme for non-resident Indians and issuing sovereign dollar bonds. The RBI has also initiated a $5bn currency swap auction to boost liquidity and dollar reserves. These steps are aimed at curbing the rupee’s recent sharp depreciation: it has hit nearly 97 to the dollar. Policymakers emphasize India’s strong economic fundamentals despite the currency weakness. Inflation pressures and foreign fund outflows are factors in support of tightening monetary policy soon. JCI -3.34% to 6107, USDIDR -0.419% to 17679, 10y IDGB -3bp to 6.791%.

Indian private sector growth slowed slightly in May, with the HSBC Flash India Composite PMI Output Index at 58.1 (April: 58.2). Services outperformed manufacturing, with the services PMI at 58.9 (April: 58.8) and manufacturing PMI at 54.3 (April: 54.7). New orders, exports, employment and business activity growth softened, with export orders rising at the weakest pace in 19 months. Input price inflation accelerated, driven by higher costs for energy, food, fuel and materials, but output price increases were more cautious. Business confidence remained positive, supporting job creation and inventory build-up despite competitive pressures and geopolitical challenges.