Uneven recovery in FX risk appetite expected

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

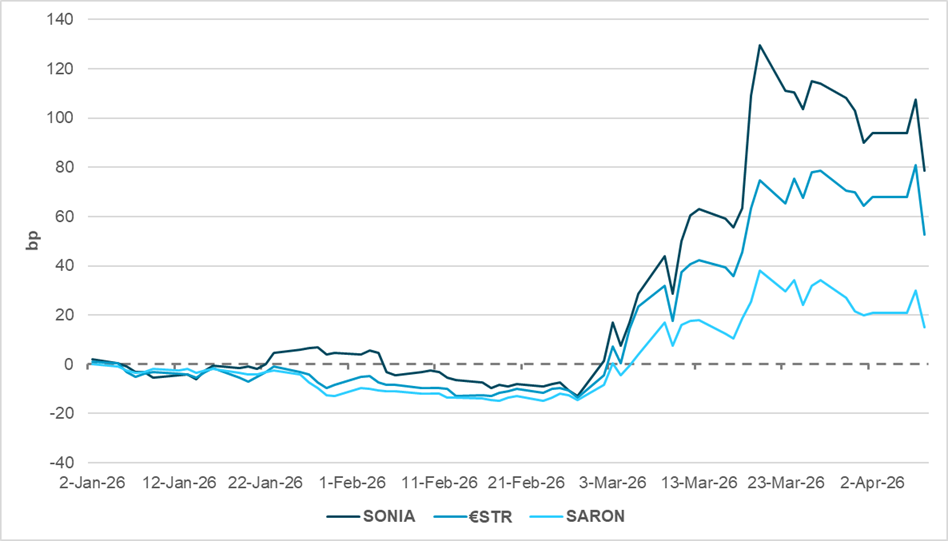

EXHIBIT #1: CHANGE IN EUROPEAN INTEREST RATE FUTURES, YEAR TO DATE

Source: BNY, Bloomberg

Our take

Risk sentiment is rallying strongly as the U.S. and Iran reach a temporary ceasefire, but not all asset classes are responding equally. If we characterize improvement in risk sentiment as an easing in financial conditions, then the usual manifestations should be stronger equities, lower yields and a drop in policy rate expectations. As European markets opened, pricing (via December 2026 futures) for the European Central Bank (ECB), Bank of England (BoE) and Swiss National Bank (SNB) (see Exhibit #1) reacted as expected, reducing targets for year-end benchmark rates as energy prices dropped sharply.

However, current pricing remains well above levels at the beginning of the year, including up to 80bp for the BoE and over 50bp for the ECB. Swiss rates are still expected to move above zero by year-end. By all accounts, we believe pricing is far removed from policy objectives.

Forward Look

There are already major differences between the European central banks in their reaction function to the conflict. For the Bank of England, skepticism about the need to hike at all has been strong, especially as U.K. households are in a very different place compared to 2022‒2023. Even hawks such as Megan Greene have stated that the conflict has led to “greater downside risk to demand, given the starting point” and didn’t see a reason to hike in March. If natural gas prices can fall further ahead of the period during which U.K. regulators set the Q3 price cap for energy bills, inflation expectations can be managed further.

The ECB is quite split, with some members warning that the central bank would need to act even before second-round effects came through. Consequently, it is striking that BoE and ECB rate pricing dropped by almost the same amount as ceasefire news filtered through, given how different policy stances are.

Finally, we question why any hikes are priced into the SNB curve at all: the currency is sufficiently strong to help generate negative pass-through, and the central bank has shown clear tolerance in this regard. With inflation struggling to maintain a positive footing based on the SNB’s conditional forecasts, hikes would further threaten price stability to the downside through their forecast horizon. Pushing out hikes and even factoring back cuts to reflect the growth shock continue to offer strong risk-reward, in our view.

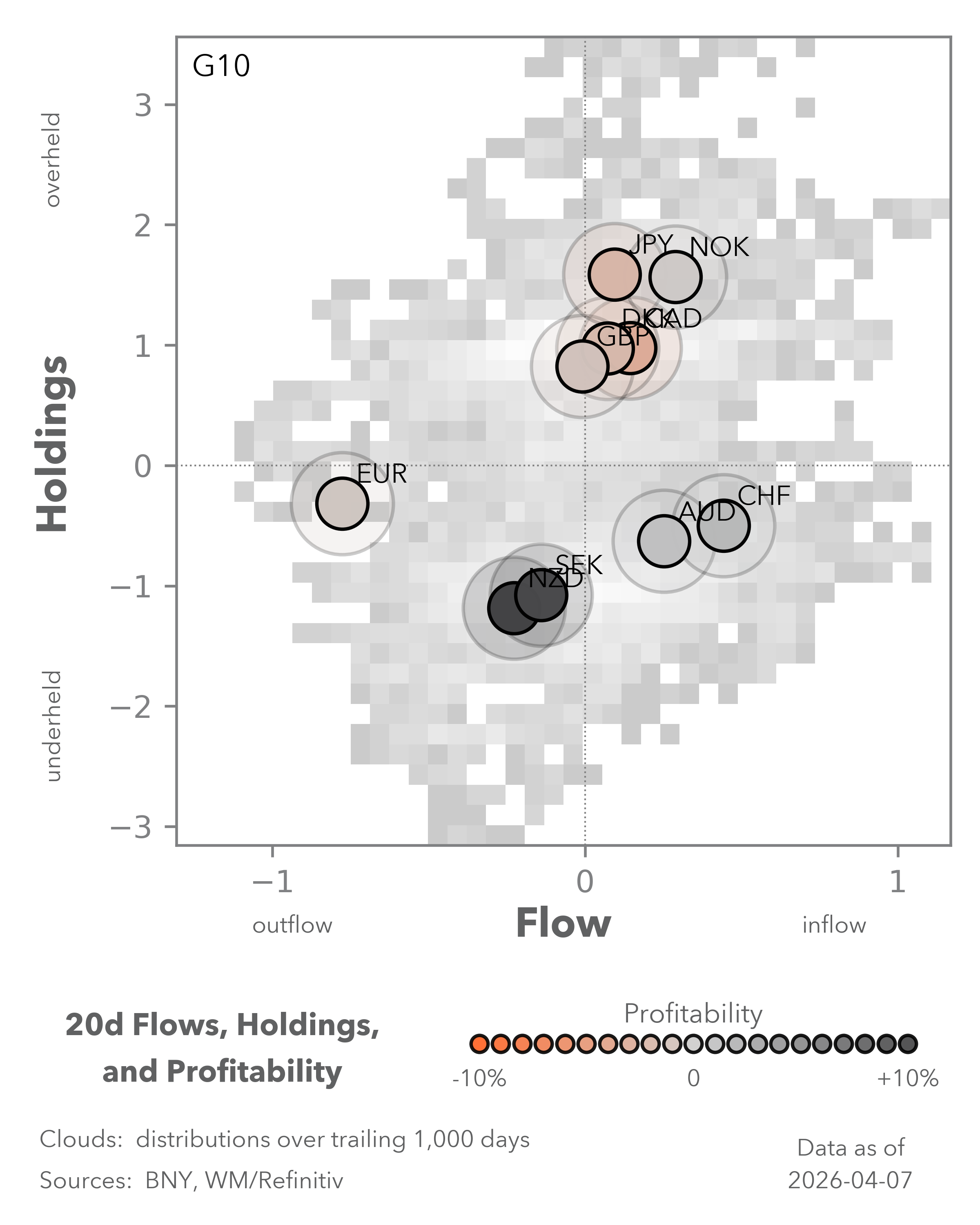

EXHIBIT #2: SMOOTHED MONTHLY FLOW AVERAGE, EUR AND NOK

Source: BNY

Our take

Assuming the ceasefire holds over the next two weeks, the “easiest” FX flows to realize would be mean reversion of the “extreme” moves since the beginning of the conflict. On the outflow side, emerging market currencies facing balance of payments stress and developed market currencies exposed to stagflation were hit hardest. At the other end, energy- and commodity-linked currencies with clear policy space were bid. The EUR and NOK currently occupy both ends of the spectrum (Exhibit #2) and perfectly encapsulate this view: the Eurozone is seen as struggling with stagflation as energy costs bite, while Norway will see a strongly positive terms-of-trade shock, and Norges Bank has largely pre-committed to a hike – the only developed central bank in Europe to do so.

Forward look

The EUR remains the most affected by the unwind of the ‘hedge the dollar’ theme exhibited before the conflict. The process is now fully complete, to the extent that the EUR is now net underheld on an aggregate basis. From a domestic asset allocation perspective, given the year-to-date performance of U.S. equities remains manageable, we can only surmise that forward buying of EUR for hedging purposes has been taken off in size – which is striking given rate expectations have moved in a direction which would normally necessitate the opposite behavior. Regardless, now that the EUR is net underheld, the bar for reversing flows is now much lower.

In contrast, NOK’s gains may halt for now if energy prices peak. Even if energy prices remain elevated, we believe receipts will be large enough to meet government financing requirements such that the Norges Bank may shift toward FX purchases again, representing an additional layer of resistance against positive NOK flows, and NOK holdings remain by far the strongest among European currencies.

EXHIBIT #3: SMOOTHED MONTHLY FLOWS, CNY AND CGBS

Source: Bloomberg, BNY

Our take

During the first week of the conflict, CNY was the best-performing currency, prompting us to explore whether it could serve as a secondary safe haven (after the dollar). Compared to savings-heavy APAC peers, its energy resilience was stronger, and currency volatility was heavily managed. However, our flows indicated that the period of CNY purchases was fully aligned with large outflows from Chinese government bonds. The CNY-CGB inverse relationship has been consistent for most of the year so far, so the CNY purchases reflected unwinding of CGB holdings, likely driven by fears of higher inflation pushing down real rates.

CGB interest returned toward month-end, and we saw CNY flows also shift back into net selling as hedging likely picked up. However, early Q2 flows point to a change in behavior, with CNY and CGBs now both being net bought (Exhibit #3). This could be an early indication that markets are seeking greater CNY exposure outright – with CGBs now being bought at lower hedge ratios.

Forward look

Low interest rates relative to the U.S. remain a stumbling block for much of APAC. As long as the JPY, KRW and TWD also struggle to generate a change in behavior, it is understandable that markets would not want to be over-exposed to the CNY. The People’s Bank of China would push back heavily against any significant real effective exchange rate (REER) appreciation. On the other hand, there is also the possibility that for the first time since the post-pandemic re-opening, there is genuine reflation taking place in China, and the market may be misjudging the outlook for front-end yields. Coupled with expectations of an easing-inclined Fed (even before the ceasefire was announced), keeping the same hedging dynamics on any Chinese asset may not have the same risk-reward as in previous years. The main challenge remains the lack of movement in longer-dated CGB yields, and the burden of proof will remain on Beijing to push for more forceful stimulus and durably lift inflation expectations.