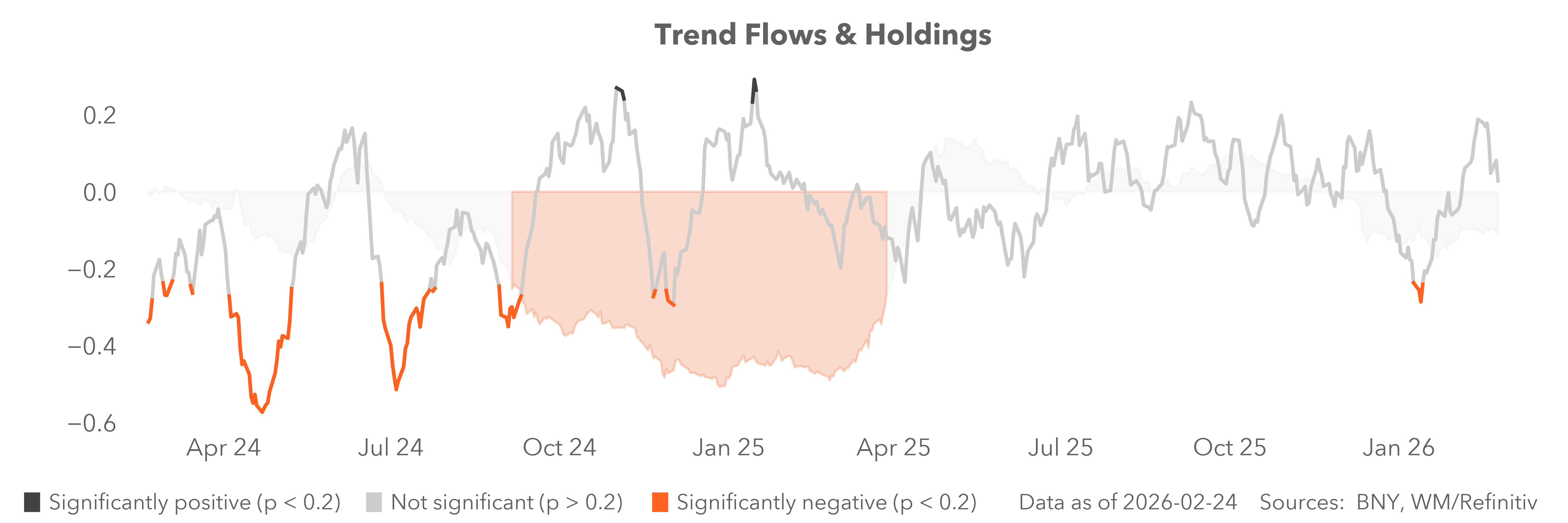

Structural pressures beneath the noise

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

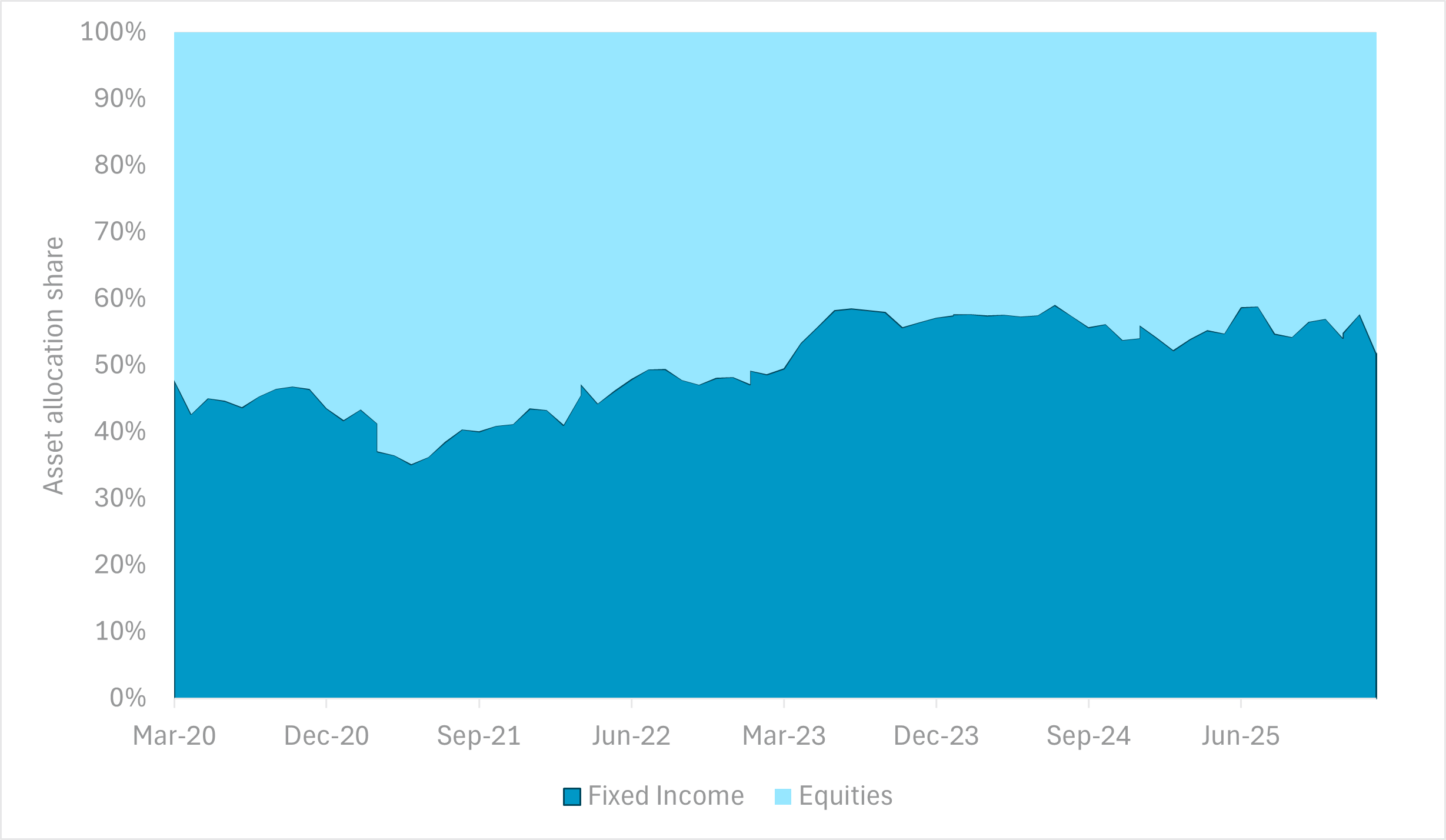

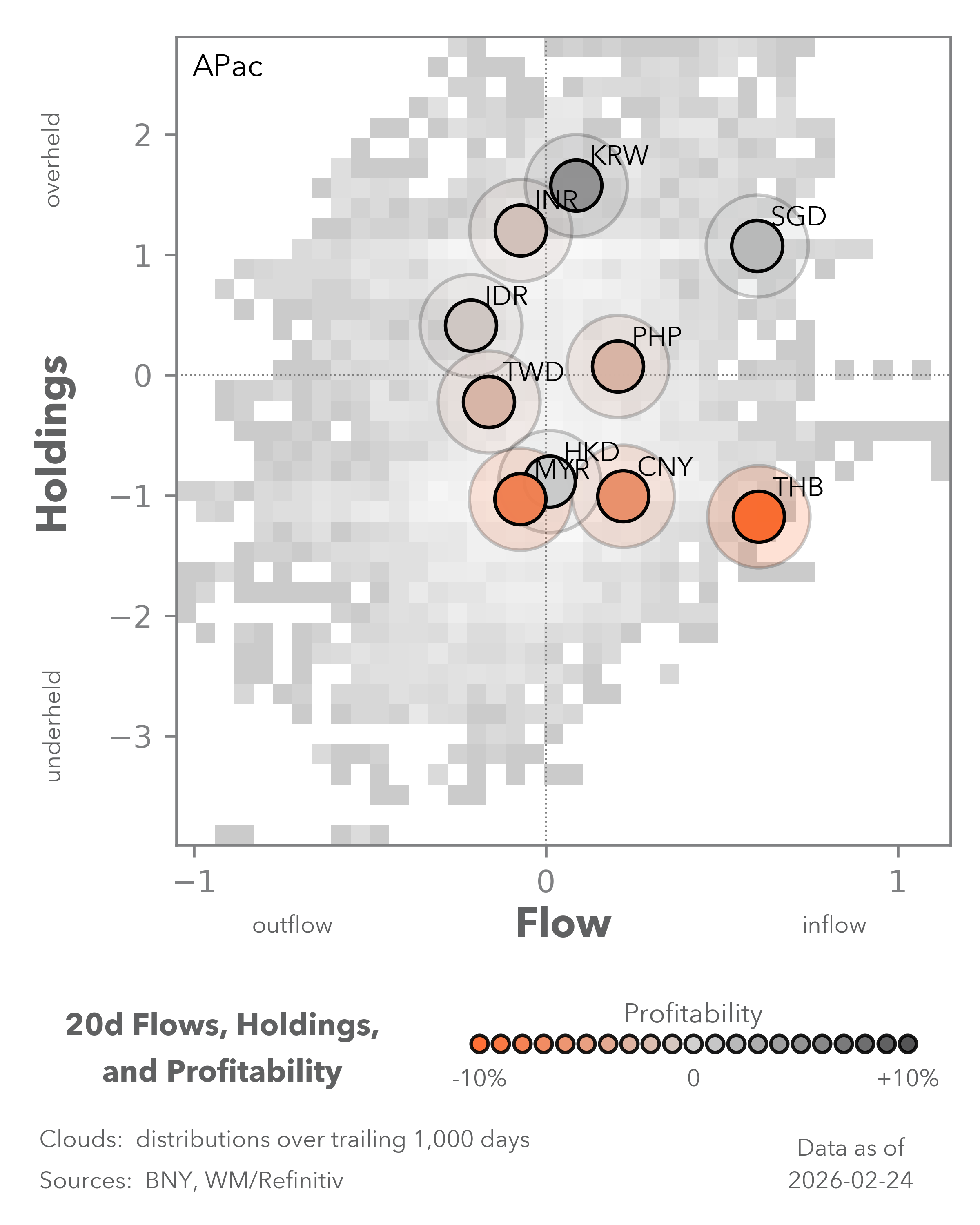

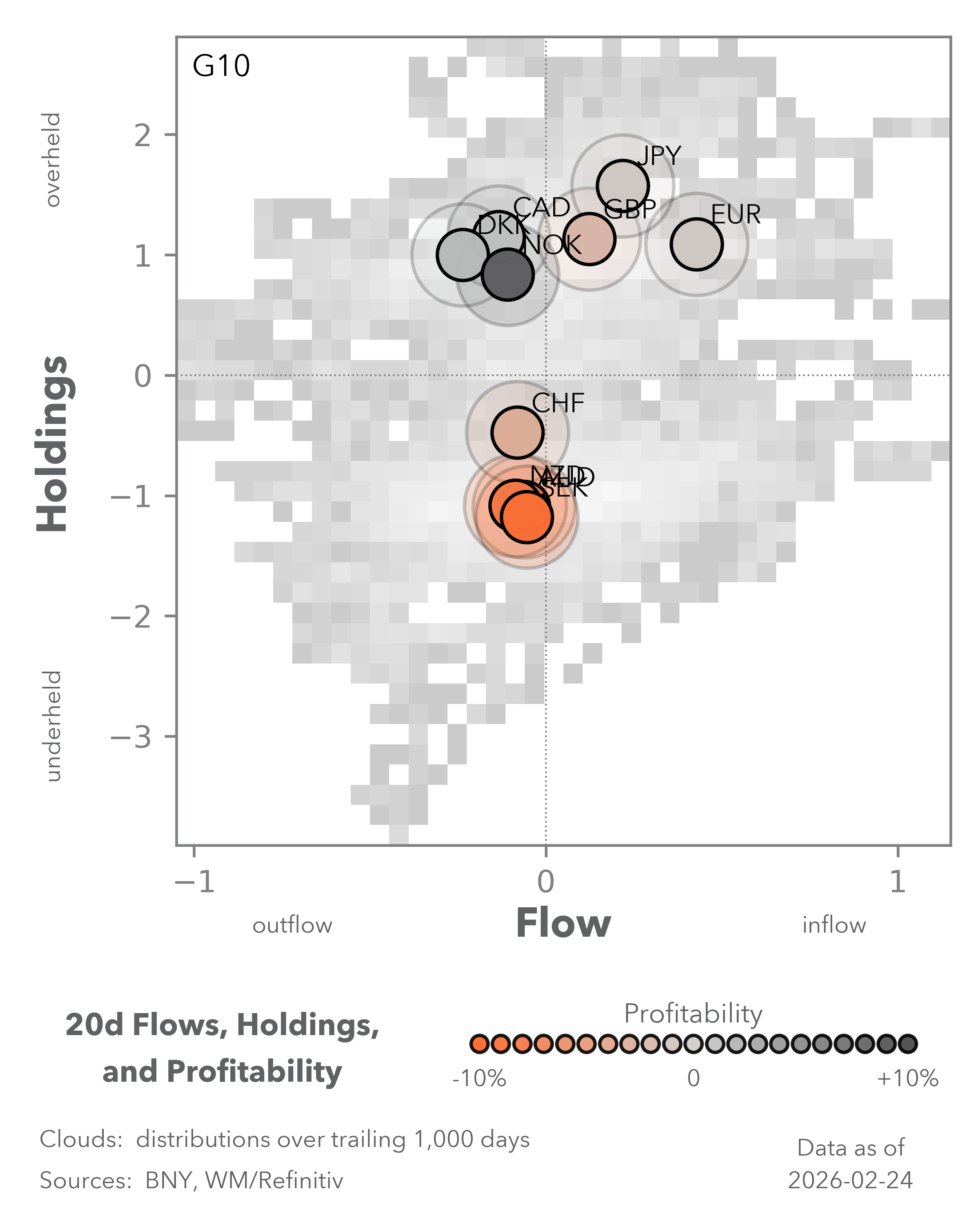

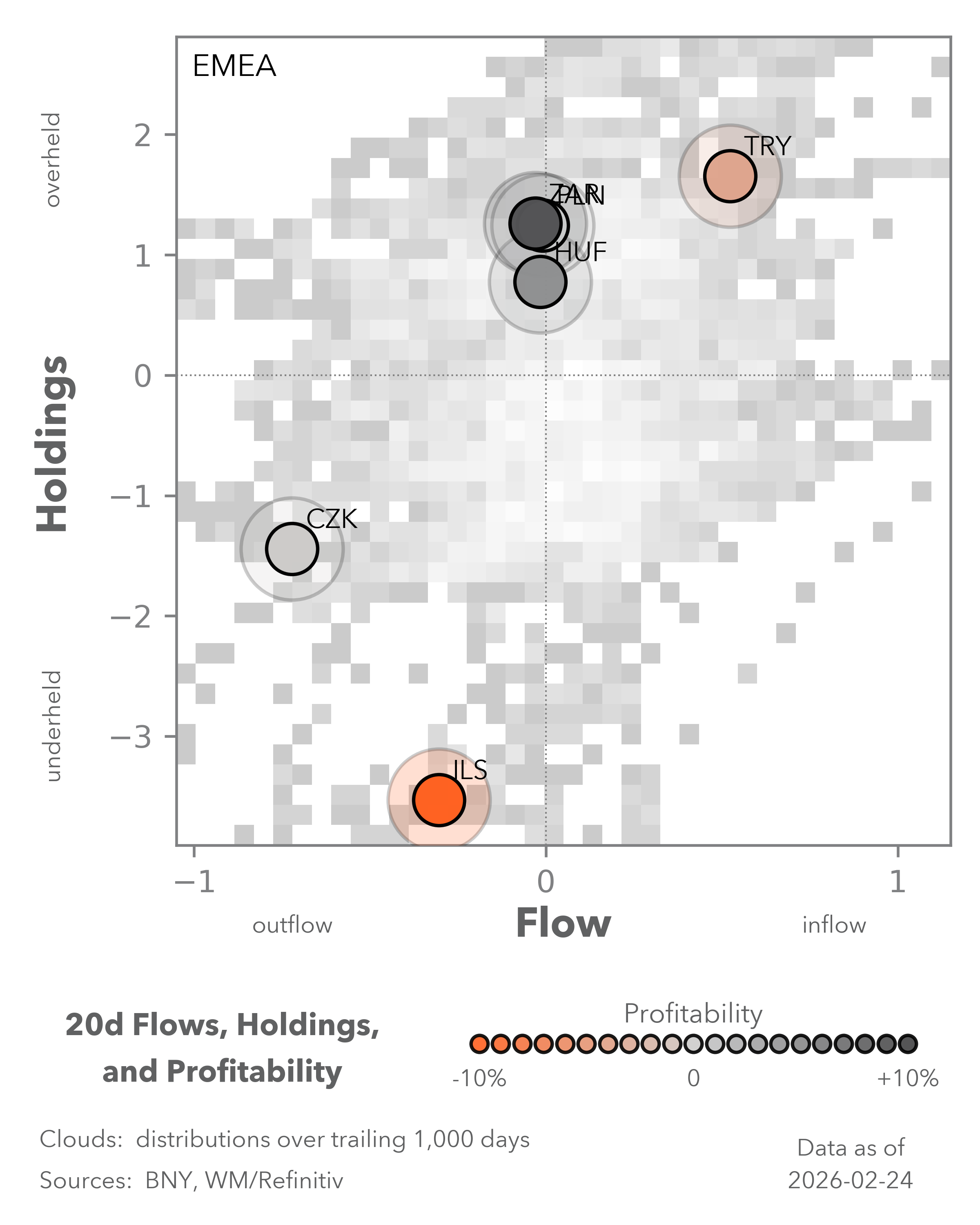

EXHIBIT #1:. ASSET ALLOCATION – CROSS-BORDER INVESTORS

Source: BNY

Our take

The result of today’s Gorton and Denton by-election is expected to mark the beginning of a significant period of uncertainty in U.K. politics, culminating in local elections in May. Polling suggests a three-way race between the ruling Labour Party and the Reform and Green Parties. Any significant underperformance by Labour would likely lead to renewed questions about Sir Keir Starmer’s leadership and trigger an immediate reaction in gilt markets. There is a general perception that any “populist” result, whether from the left or right, would lead to a further tilt toward fiscal expansion by the U.K. government, bringing fiscal dominance concerns back into play.

Political noise has become a recurring feature of U.K. politics over the past decade. While acknowledging the short-term impact on gilt holdings, the status of U.K. government paper has never been in serious doubt – even during the 2022 mini-budget crisis. The broader institutional framework remains supportive. GBP will also face stress, but it is unlikely to be prolonged. Our new asset allocation indicator shows that for cross-border investors, gilt holdings as a share of their U.K. assets have been remarkably stable over the past three years. This highlights a bigger challenge: The U.K. equity market is no longer seen as a growth story. There is little interest in adding exposure. The decline of the London Stock Exchange as a major market for IPOs has been well-documented, but successive governments have been unable to turn matters around.

Forward Look

We have long maintained a defensive view on GBP due to structural factors. The latest survey data point to continued household demand weakness. Bank of England (BoE) Governor Andrew Bailey, who retains the swing vote on the Monetary Policy Committee (MPC), recently said he will enter upcoming meetings “asking if a cut is justified,” That clearly signals the direction of travel. However, the very structural factors that have supported bond holdings are starting to turn around. Bailey is perhaps the first BoE governor willing to express a more positive outlook on U.K. productivity growth, which has been largely absent since the Global Financial Crisis. In time, if this does translate into higher trend growth and real incomes, the U.K. equity outlook will change completely and encourage more cross-border flow.

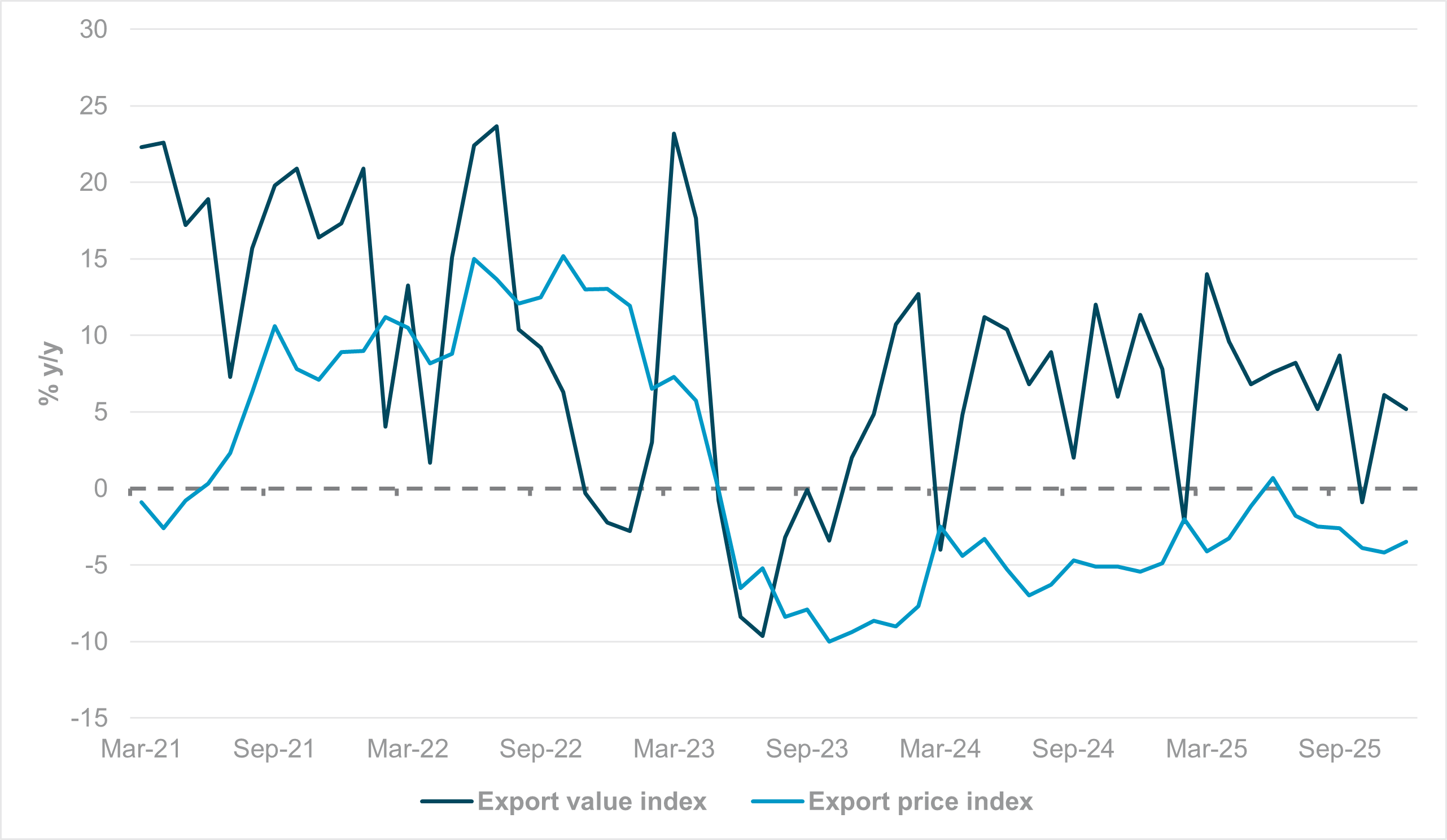

EXHIBIT #2: CHINESE EXPORT VALUE AND PRICE INDICES

Source: BNY

Our take

Despite domestic and EU-wide pressure for a harder line on Chinese exports to Europe, German Chancellor Friedrich Merz was diplomatic during his meetings in Beijing with Chinese President Xi Jinping, stating that despite being aware of “differences on a number of issues … we realize that we can cooperate in many areas. That will need patience and above all dialogue.” Larger orders for European-made aircraft will help make a small dent in trade imbalances. However, we suspect that China’s business leaders are likely to stress that they are equally, if not more, concerned about pricing pressures and disinflationary outcomes. Even as the renminbi strengthens, export prices have been contracting for nearly three years. Growth in export values has also struggled to match levels seen before the end of COVID. Any undershooting of already-low export price growth could put the brakes on CNY appreciation earlier than expected.

Meanwhile, CPI is expected to remain below 1% for a fourth consecutive year. Domestic patience for reflation to materialize – which would suit Europe’s needs – is wearing thin. Only seven of mainland China’s 31 first-level subdivisions expect local government revenue growth above 4%. Sustained household demand, the only source of genuine nominal demand growth, will need to come from central fiscal impulse.

Forward look

Consequently, the annual National People’s Congress, which opens next week, is perhaps the last chance to reset expectations for the year. The rhetoric in favor of supporting household demand remains strong, and the budget deficit target is unlikely to fall below 4%. Nonetheless, we maintain the view that quality is more important than quantity, as one-off injections cannot generate a permanent shift in household expectations. Nothing has come close to the comprehensive relief in 2019, which directly impacted incomes. We would continue to manage expectations on this front.

In the near term, enforcing regulations against “involution” to address overcapacity will serve everyone’s purposes and continue attracting rotation into local equity markets. This is already a relatively consensus view, so we doubt there will be a large marginal impact on domestic asset performance.

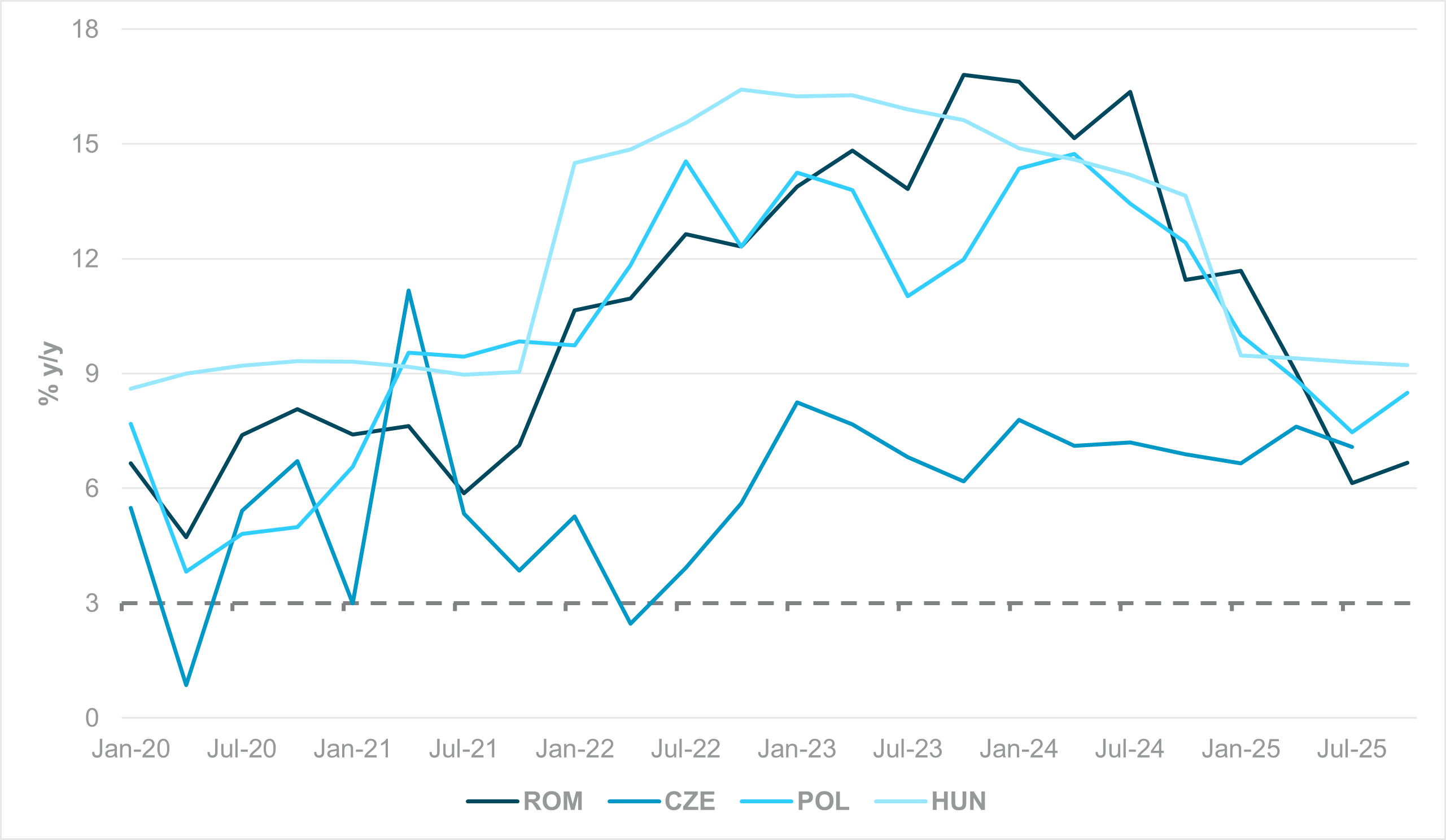

EXHIBIT #3: CEE WAGE GROWTH

Source: Bloomberg, BNY

Our take

The National Bank of Poland is expected to follow Hungary with a rate cut next week, alongside similar guidance.

Even with sufficient policy space, emerging market central banks do not wish to signal a sustained easing cycle in a soft global risk environment. Elevated currency valuations are also not seen as overly problematic.

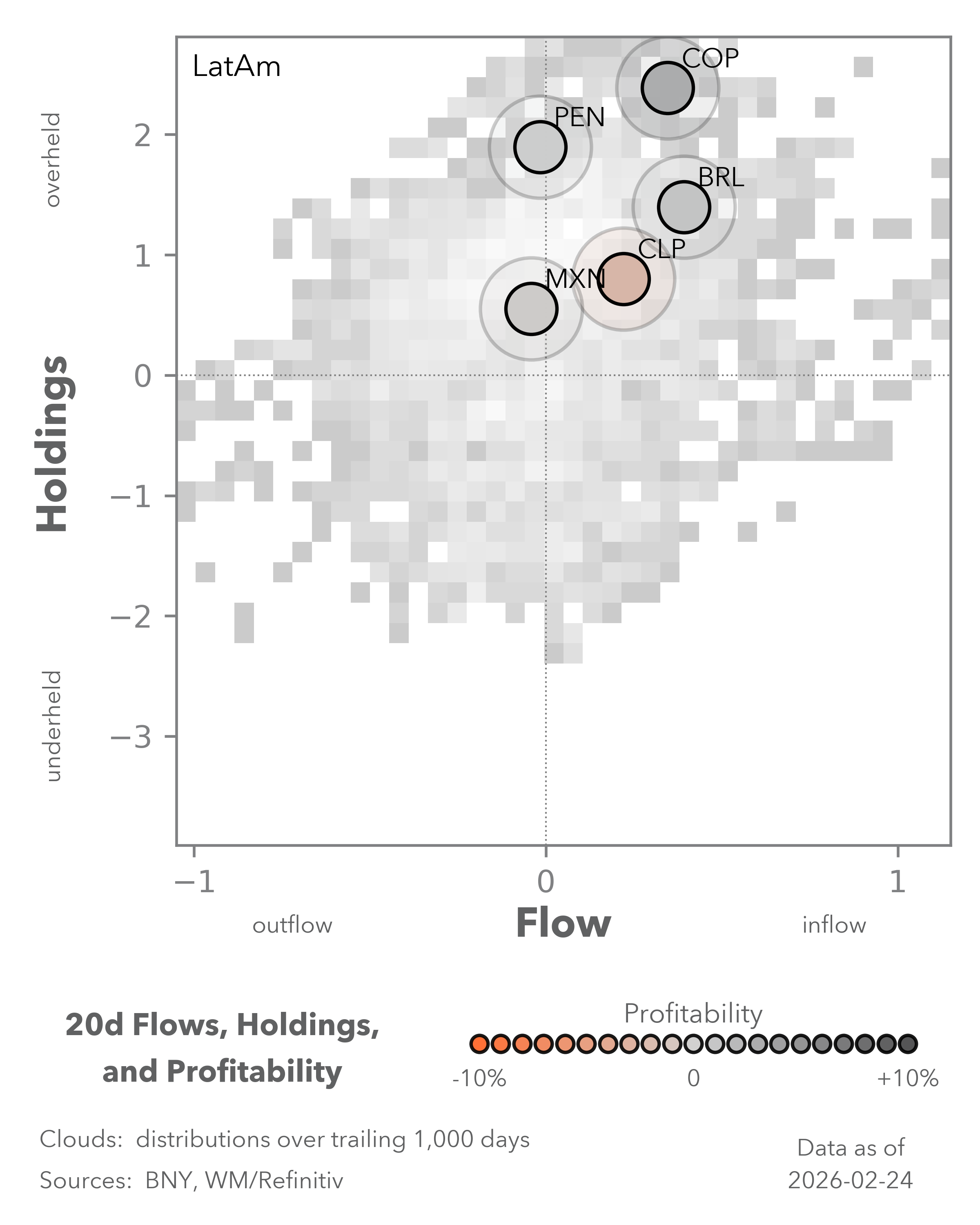

We believe the reason for “benign neglect” toward Latin American and European “carry” currencies is clear. Fiscal impulse remains excessive, making non-tradables inflation the key driver – rather than tradables pass-through or export earnings volatility seen in previous cycles. However, the marginal impact of fiscal support is fading. Export earnings are waning amid soft external demand and elevated currency valuations. That is translating into lower income expectations and softer wage growth. Central and Eastern Europe (CEE) has struggled with extremely high wage pressures over the past three years, mostly due to supply issues. The downtrend is now clear, and Hungary has shown that transmission into non-tradables inflation can be swift. There is clearly more room to ease across the region if wage growth continues to normalize.

Forward look

ven if Poland and CEE peers or the broader EMEA region signal an accelerated cycle, carry trades may not unwind quickly.

iFlow indicates that holdings of Latin American and EMEA high-yielders have peaked. However, there is little conviction behind sales, as lower nominal rates do not necessarily mean lower real rates. National Bank of Hungary (MNB) Governor Mihály Varga stated that even with additional cuts, the MNB “will ensure positive real interest rates.”

Poland and South Africa, the other popular carry trades in the region, will likely follow the same approach, with South Africa now anchored by a lower inflation target. The South African budget announcement this week has even pledged to introduce fiscal rules, which will further strengthen fiscal credibility and the real rate outlook.

The only outlier at present is Romania, where inflation is swiftly approaching double digits but without the rate hikes to match. It is no surprise that it is currently the most strongly sold currency in iFlow’s suite of high-yielders.