Pockets of disinflation, still uneven

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

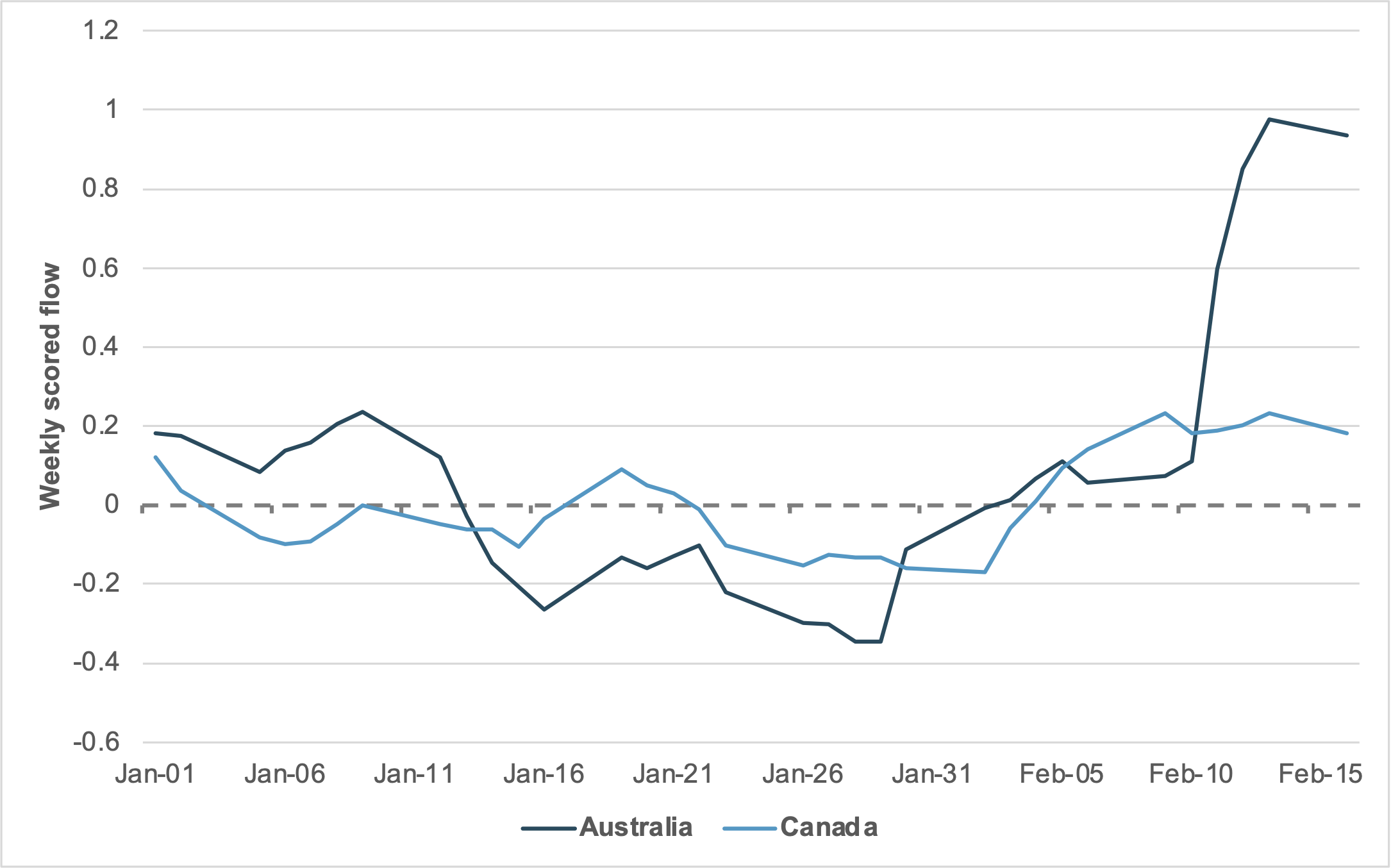

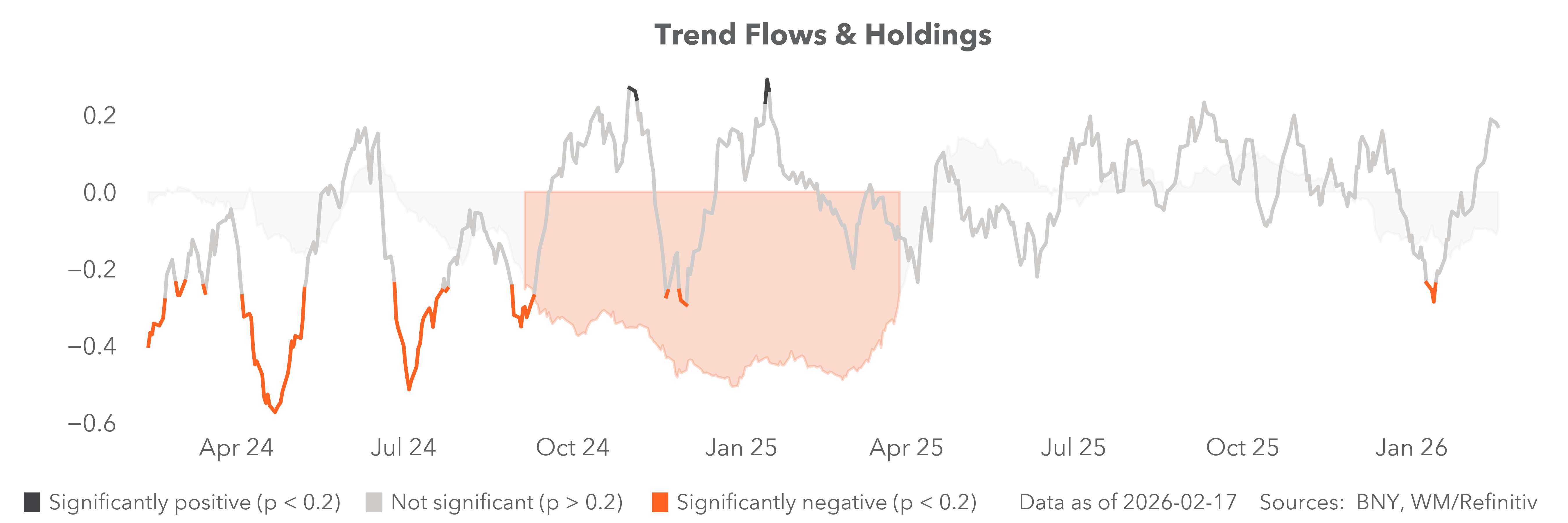

EXHIBIT #1: YTD CASH AND SHORT-TERM FLOWS, AUSTRALIA AND CANADA

Source: BNY

Our take

Despite ongoing challenges for risk sentiment, rates and FX markets are showing little reluctance to price in policy pivots where justified by inflation. Flows are even more forceful when hawkish expectations are endorsed by the relevant policymakers. Presently, Australia is the clearest case of G10 tightening, with Governor Michele Bullock has repeatedly emphasized in recent weeks that the Reserve Bank of Australia (RBA) will not hesitate to move if justified by data. Her warning that the country may be prone to structurally high inflation also suggests hikes will not be tactical and may serve as a clear anchor for carry-seeking flows, if the risk environment allows.

AUD’s overall flow picture has improved, but the more notable development of late has been a surge into cash and short-term instruments (CAST). Year to date, flows have been unimpressive, but after Governor Bullock’s recent speeches and testimony, Australia’s cash and cash equivalents market appears to have received the message on interest rates. Any asset hitting a flow magnitude of 1.0 or higher on a weekly basis is rare. When it happens, it is either due to event risk or some form of structural re-rating.

Forward Look

CAST flows tend to be highly sensitive to G10 rate differentials. We have identified several candidates already, but only Australia is responding forcefully, fully in line with a relatively simple set of fundamental assumptions. First, there needs to be data justification. Second, a central bank needs to be seen as credible in its response. Japan is also expected to hike rates this year, but questions remain regarding the Bank of Japan’s ability to respond in kind. Meanwhile, Canada’s pricing volatility persists, reflecting the uncertain economic environment surrounding trade. Finally, New Zealand is also a strong candidate, but we do not have sufficient density for the country’s cash market, which underscores the importance of liquidity.

CAST also tends to benefit during periods of risk-off as equities are sold, but if the relevant market’s rates are sufficiently high, cross-border investors will rotate into cash rather than repatriate. Extending duration in a steepening environment also offers poor risk-reward. We see equity-to-cash rotation as a factor behind the surge, as Australia’s mining sector faces downside risks to elevated levels of global developed market metals and miners’ equity holdings. With high ratings, good liquidity and yields, a stronger liquidity preference for the AUD is no surprise at all.

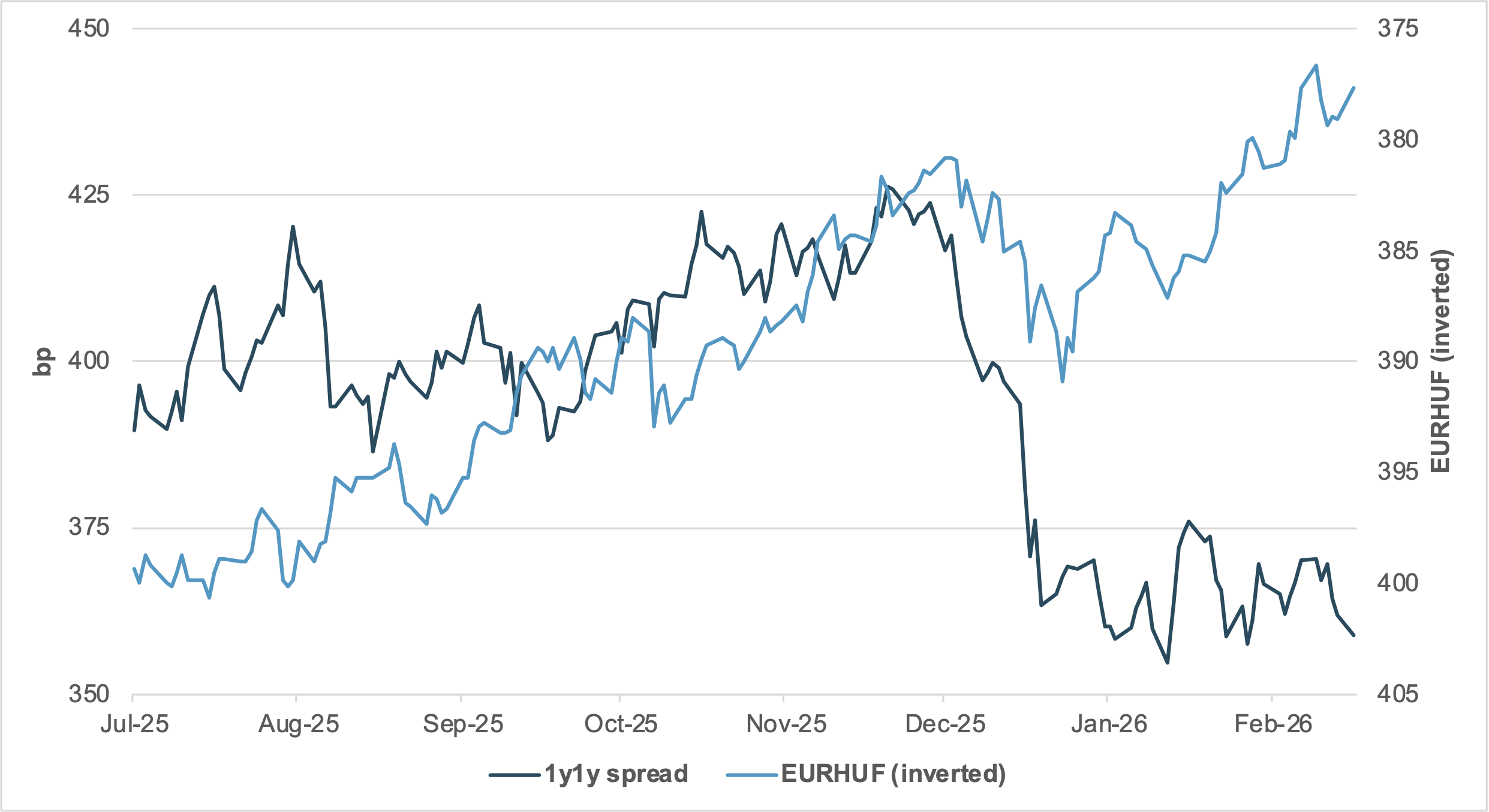

EXHIBIT #2: EUR–HUF 1Y1Y FORWARD SWAP SPREAD VS. EURHUF

Source: BNY

Our take

Amid the clamor for upside inflation surprises and associated policy pivots, some asymmetry remains in markets’ reaction to price data. Downside inflation surprises are seen as “more of the same” and, at this point in the cycle, are not eventful. There was one major exception recently: Hungary’s soft inflation print for January has upended policy expectations, including our own. The sharp drop from 3.3% y/y in December to 2.1% y/y in January – the lowest annualized level in seven years – has put additional easing next week by the Magyar Nemzeti Bank (MNB) firmly back on the radar. Given Hungary has been one of the clearest examples of fiscal dominance in emerging markets (EM), the pricing shift will heavily impact assets – including the carry trade where HUF was one of the best-held CEE/EMEA carry names over the past two quarters.

Forward look

It is tempting to see the January print as a one-off, but there have been some underlying disinflationary trends, such as softer services inflation (albeit still at a very high level) and goods’ price growth staying anchored. Meanwhile, HUF’s strong performance must have also played a small but key role in generating disinflation via exchange-rate pass-through (ERPT). While acknowledging carry trade strength, we believe EURHUF has detached from fundamentals for some time. Forward spreads have been pricing in weaker price growth and carry gains in Hungary despite the fiscal outlook, but EURHUF has just been on a one-way street. The European Central Bank’s pivot back to disinflation and euro monitoring has been far more evident in FX trades than rates. This is not sustainable, and we expect EURHUF to converge toward rate differentials, even if only on a tactical basis ahead of the election, is our favored view.

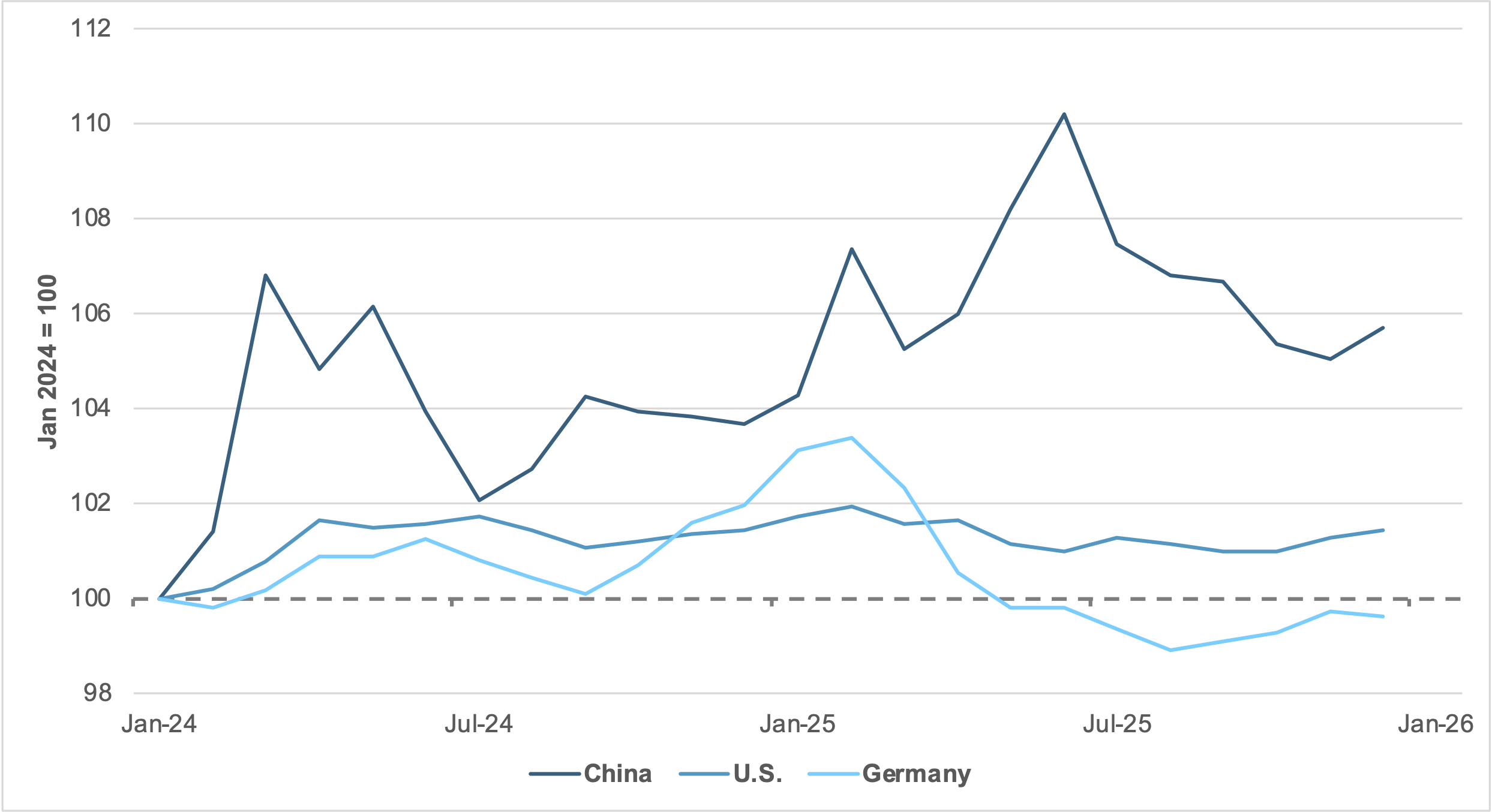

EXHIBIT #3: IMPORT PPI, CHINA, GERMANY AND THE U.S.

Source: Bloomberg, BNY

Our take

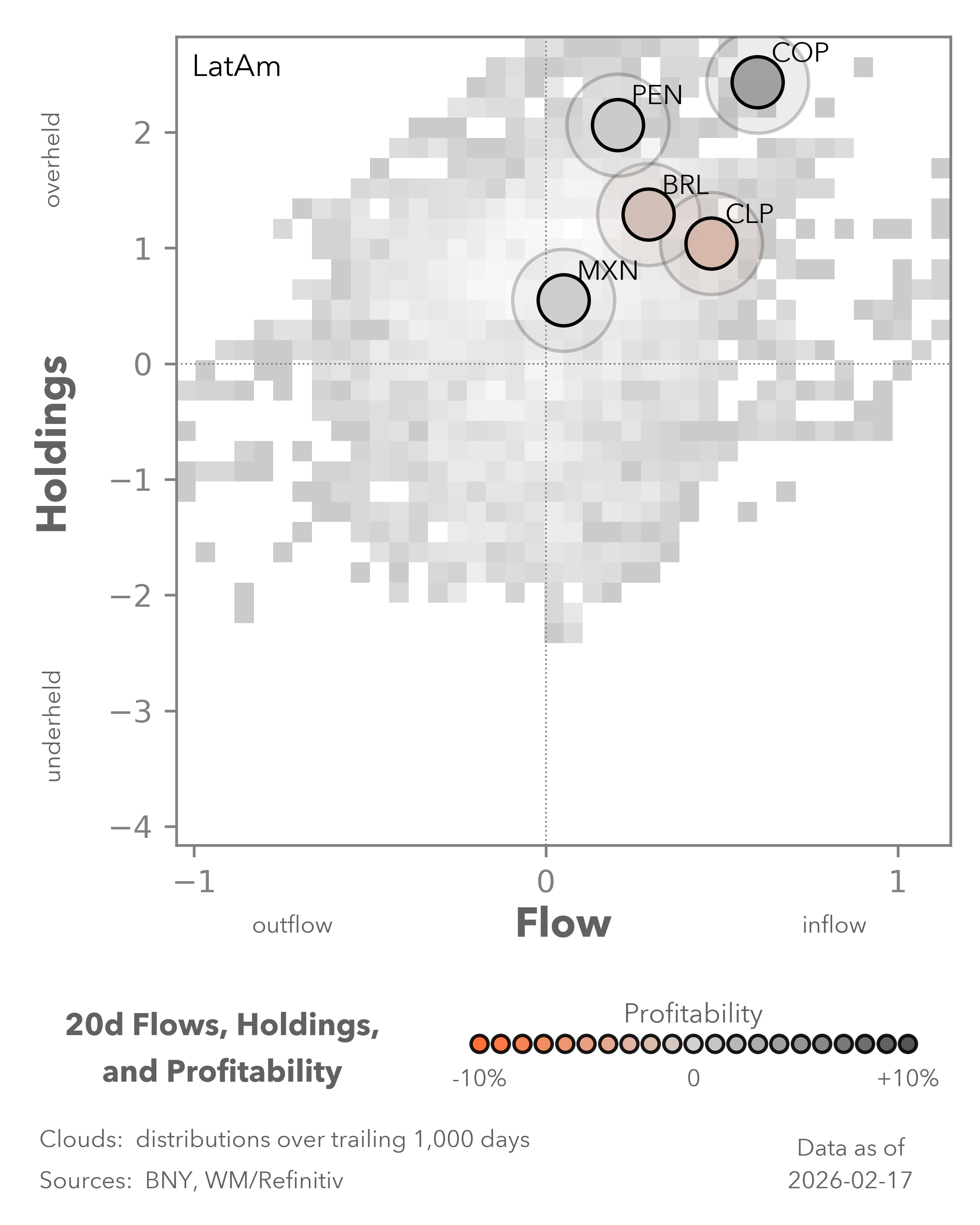

Metals markets have struggled to recover their early-year highs, and we don’t expect macro data to support a rebound in the near future. Underlying demand for industrial metals has long dragged on prices and futures curves, and there is very little sign that improvement is imminent. Furthermore, the recent price surge doesn’t even appear to be impacting import prices, which underscores the level of the demand drag. In absolute terms, import prices in the U.S., China and Germany are all lower on an annualized basis (Exhibit #3), with broader Chinese producer price figures (PPI) expected to remain negative for the remainder of the year. The recent decision by Indonesia to cut nickel ore quotas at its largest mine underscores the downside risks to base metals and the lengths to which exposed governments are willing to go to preserve favorable terms of trade. Such headwinds are likely to affect commodity markets in the near term.

Forward look

The current state of global import prices may also suggest that “involution” is now taking place globally, albeit not as actively as in China. Producers of finished and intermediate goods, worried about domestic production and market share, seem reluctant to raise export prices in the face of tariffs, helping holding down import costs. This is another reason why the impact of U.S. tariffs on inflation has been weaker than originally feared. Entrenchment of such practices is a big risk factor for the global economy but underscores that where inflation is persistent, wages and services inputs are the strongest factor. Policymakers may attempt to react forcefully to supply pressures, but we doubt the transmission will be seen as satisfactory. Meanwhile, we fully expect ongoing downside risk to flow and holdings in metals-exposed currencies. This means that the need to maintain tighter financial conditions remains imperative across much of EM.