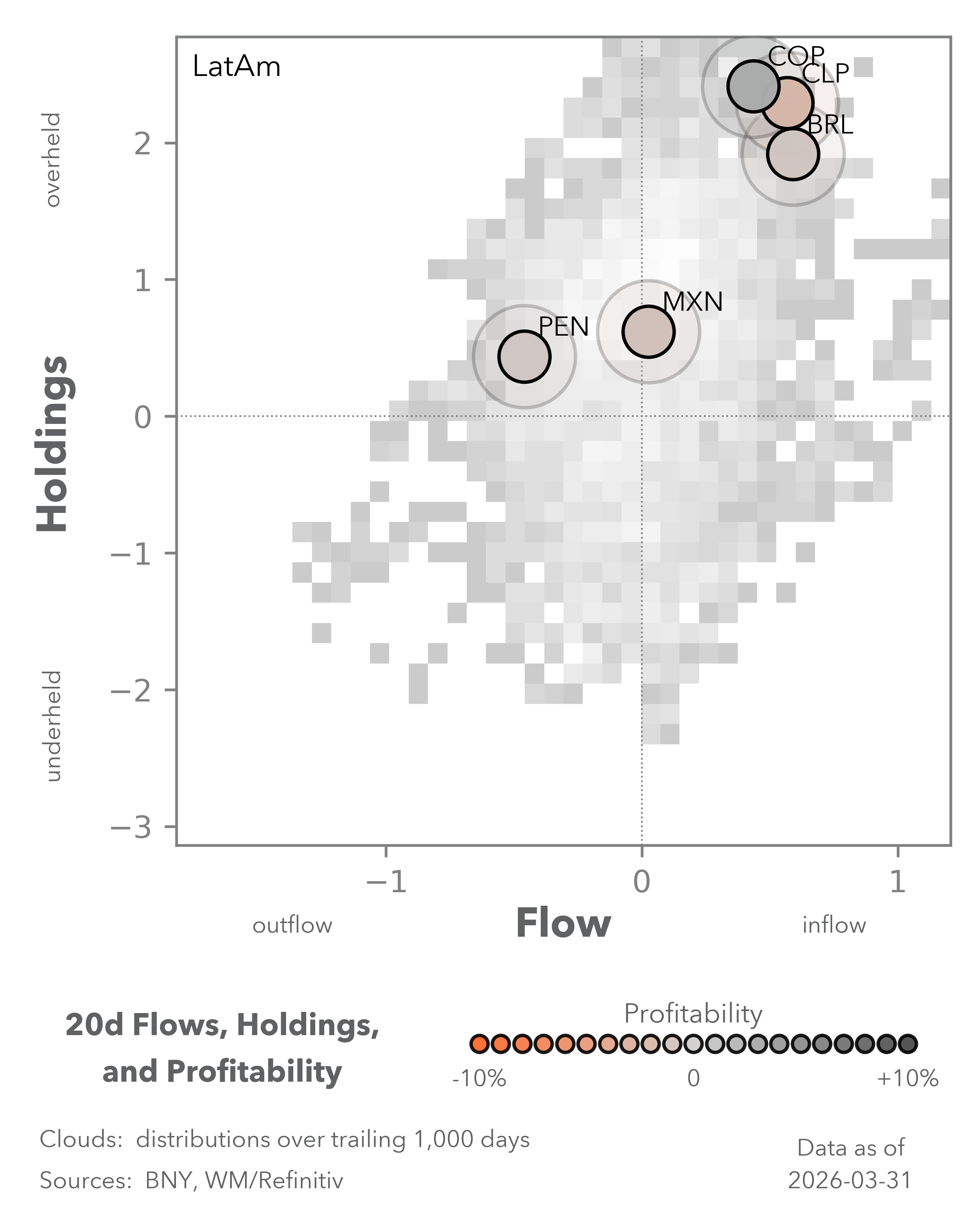

FX risk appetite

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

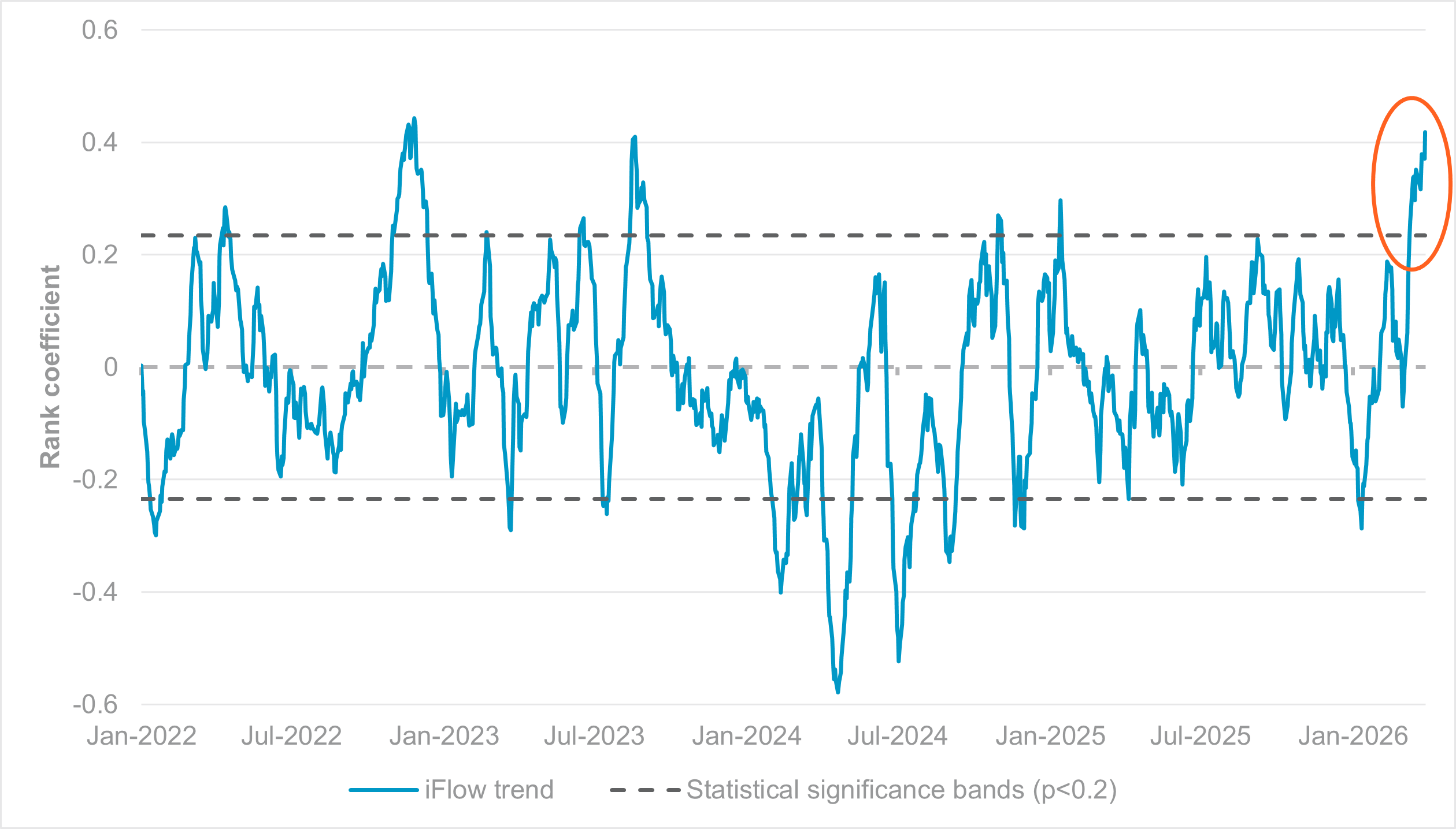

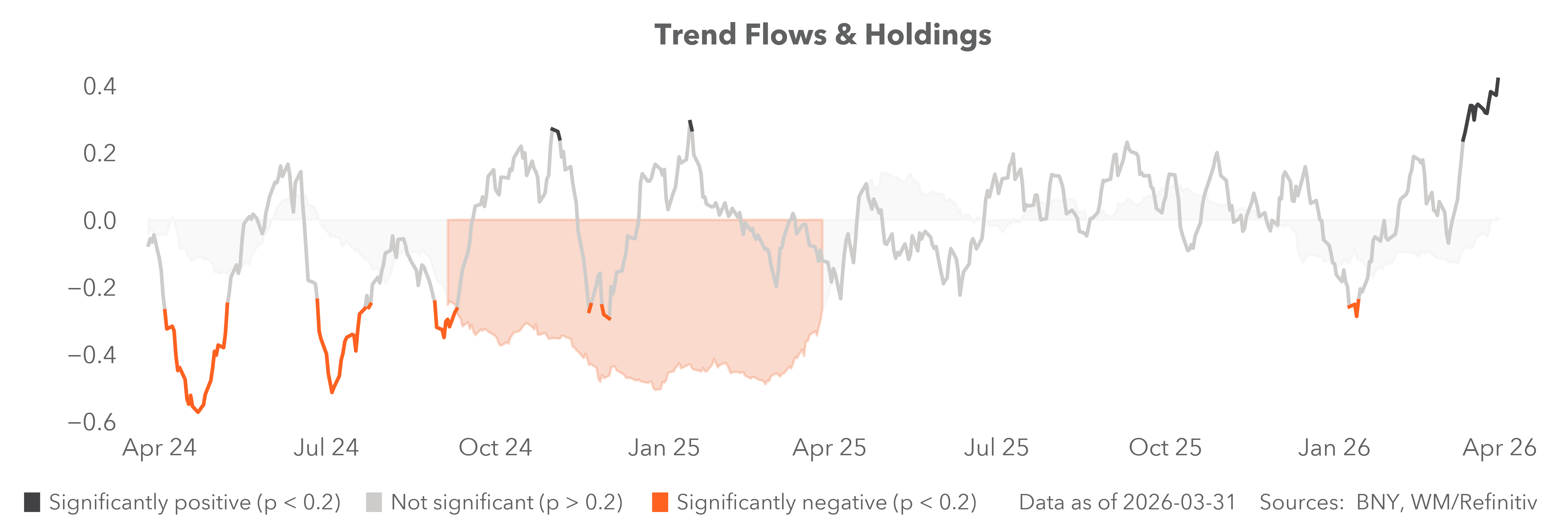

EXHIBIT #1: IFLOW TREND AT THREE-YEAR HIGHS, BUT NO SIGN OF MEAN REVERSION

Source: BNY

*iFlow trends tracks alignment (using a Spearman rank correlation) between currency flows (ranked by normalized monthly flow scores) against the same rankings of a currency’s spot trend performance, calculated by their standard 50-day vs. 200-day moving average, which is a standard momentum indicator.

Our take

Since mid-March, our iFlow Trend indicator has shifted into statistically significant positive territory. It‘s only the third time in the past two years this has happened, and in both prior cases, reversals were swift. Consequently, we highlighted that there would be opportunities in looking at fading momentum trades tactically, which largely entailed reversing some of the recent dollar strength against balance-of-payments-stressed currencies due to the supply shock. However, due to fears of escalation, iFlow Trend has only continued to accelerate and is now at its highest levels since H2 2022. We also establish that the 2022 episode led to swift mean reversion, pushing iFlow Trend deeply into negative territory. This means risk-reward to reverse momentum trades is even stronger now.

Forward Look

As the case for a de-escalation appears stronger this time, a “risk-on” theme is starting to emerge, even if FX is still slower to react in this respect. If we anchor currencies by their current flow situation and align them with momentum (measured by their respective dollar exchange rates), we have identified CLP, NOK and BRL as the currencies most at risk, while large reversals in IDR, INR, TRY and the EUR are also possible.

The drivers are clear. The first three are seen as high-yielders with strong positive terms-of-trade revisions from the current conflict. All three are in the top five in flow ranks and in the top ten by momentum ranking (see definitions in source). For the bottom-ranked flow names, stagflation and balance of payments are the clearest drivers, and EUR has been on the receiving end of the unwinding of the “hedge dollar” theme at the beginning of the year. All four are in the bottom five in current flow rankings, and their momentum scores are in or near the bottom five. As we highlighted in our asset allocation update this week, relative value is emerging for now. Fading momentum plays are another way to push for a risk-improvement narrative without taking dollar risk outright.

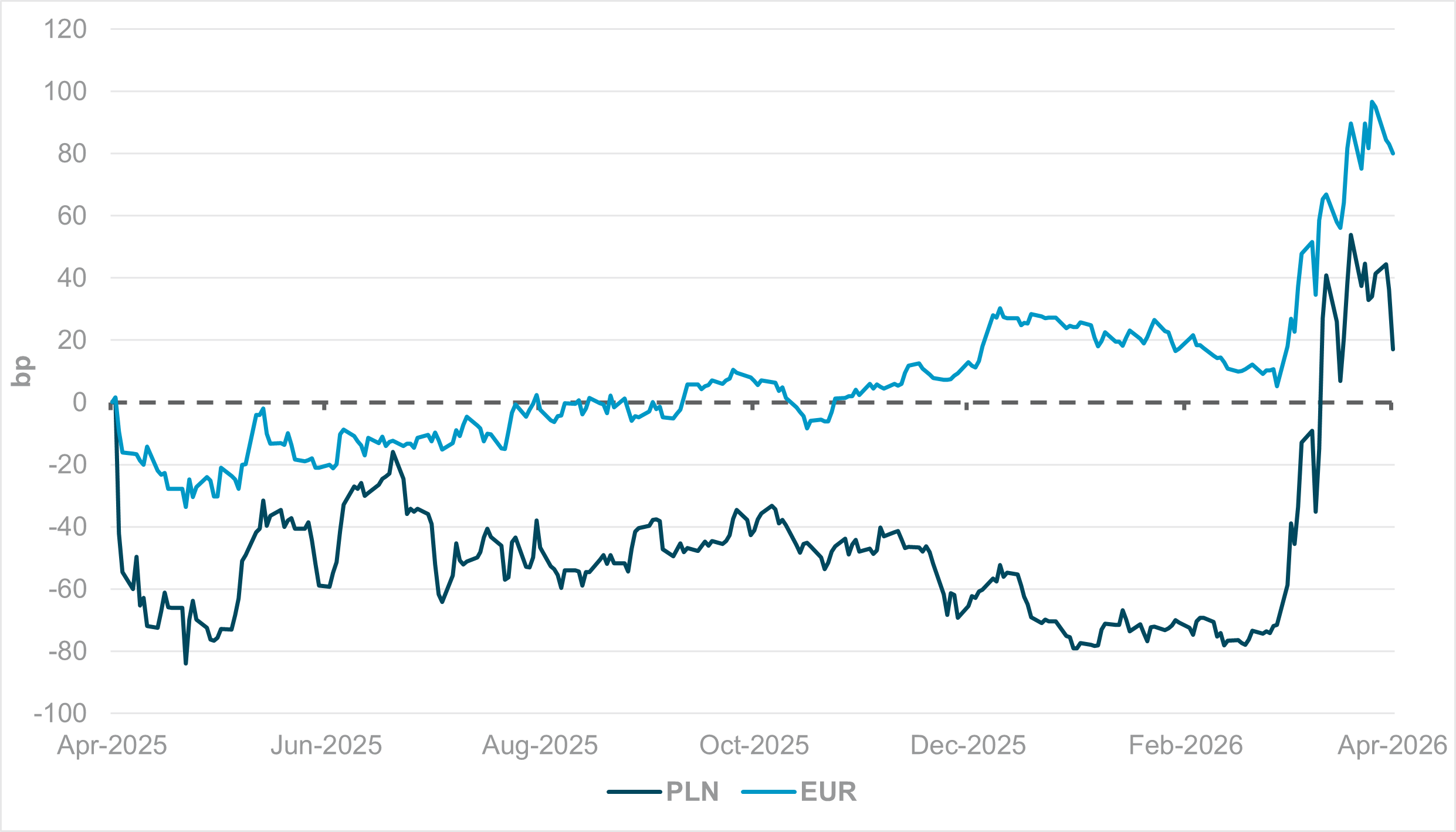

EXHIBIT #2: CHANGE IN 1Y/1Y FORWARD SWAP, LAST 12 MONTHS, PLN AND EUR

Source: BNY

Our take

The NBP decision in March was the first major European central bank decision at the beginning of the Iran conflict. Understandably, the consensus at the time saw a time-limited operation that was not expected to generate prolonged disruption to global energy markets or other inputs. The NBP press release didn’t even mention a conflict, only acknowledging that “changes in the global commodity prices and inflation, amid geopolitical tensions,” represented a risk factor for the country’s inflation outlook. Crucially, the Monetary Policy Council believed their inflation forecasts would hold and cut the reference rate by 0.25% to 3.75%.

Ultimately, it wasn’t long before global policy expectations were upended. Instead of further softening in CPI, Polish inflation jumped to 3% y/y in March, led by a 1.0% m/m sequential figure as input prices increased materially. Other central banks in the region have shifted their near-term outlook without pre-committing to any moves, and we believe the general inflation figures in CEE don’t warrant a strong reaction yet.

Poland’s m/m inflation print is lower than Germany’s, but across the region, protective measures are in place to limit the rise in energy costs. Other forms of subsidies will further pressure public finances. As an offset, short-term policy expectations must be firmly anchored to the hawkish side with all options on the table, as is being done by the European Central Bank (ECB) and the Bank of England (BoE).

Forward look

We remain of the view that current ECB and BoE pricing is excessive. Given the condition of the Eurozone and U.K. economies, there is very limited scope for aggressive tightening without triggering a material economic downturn, independent of a view on the direction of the conflict.

However, we find it surprising that CEE expectations have not moved even more aggressively, especially as fiscal impulse is far higher while labor markets are also tighter. For example, Polish forward rates are currently only 20bp higher on a 12-month basis, and less than 90bp compared to February 27 (the last trading day before the conflict began). In contrast, ECB rate pricing is now close to 80bp higher on a 12-month basis, and 75bp above February 27 levels. As a deeper easing path was in place for CEE central banks, the more recent moves are the most relevant, but even so, a 15bp premium over the ECB is somewhat defensive. We can see a bigger drop from the highs around mid-March. Such pricing is also insufficient to take pass-through risk into account should even half of the ECB’s current anticipated path materialize. Either way, we see strong upside risks to CEE policy pricing in the near term, beginning with the NBP, unless the market significantly changes its expectations for the ECB as well. The latter course is more in line with fundamentals, in our view, but rates markets currently believe otherwise.

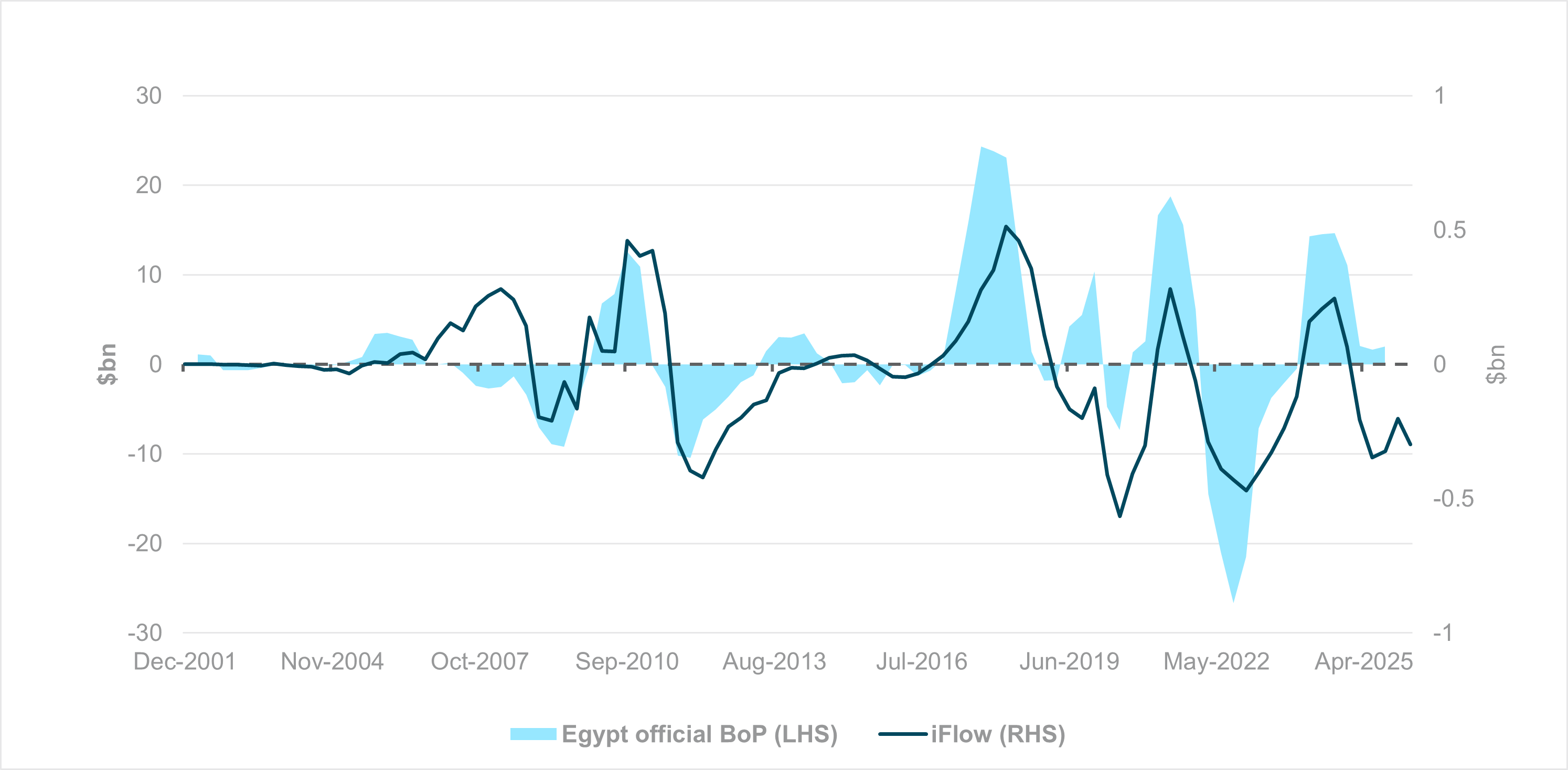

EXHIBIT #3: EGYPT INCURRENCE OF PORTFOLIO LIABILITIES, OFFICIAL DATA VS. IFLOW PROXY

Source: Bloomberg, BNY

Our take

Unsurprisingly, our custody data have flagged material outflows from Middle East and North African (MENA) markets. Outflows that generate risk aversion aside, the risk premium required to attract portfolio inflows is likely to be higher from a simple balance-of-payments perspective. For the oil-exporting economies, a sharp drop in export earnings for relevant products, in addition to services spend in the region, requires a significant near-term discount based on cashflows alone. These economies also lack a flexible exchange rate to compensate. For non-oil-based economies, higher import costs are a major factor. We’re also concerned that more downstream products will aggregate structural current account deficits.

Forward look

Despite current flow stress, we would avoid drawing comparisons with 2022-2023 for now. One key differentiator is that domestic demand – especially fiscal – has been retrenching for several quarters, which, on the margins, alleviates financial stress from a drop in funding. Furthermore, for Egypt, a key frontier market, reforms, including in exchange rate formation, have helped stabilize expectations and ensure a high starting point for real rates. Consequently, on a 12-month rolling basis, local asset markets have managed to generate a significant buffer to limit balance-of-payments risks for now. Our data are a relatively good proxy for trends in the Egyptian balance of payments. On a 12-month rolling basis, the combined outflows are still running at less than half the levels of 2022. For current account surplus economies with strongly positive external asset positions, the buffer is even larger. We expect funding gaps to remain large in the near term, but the levels are not insurmountable with the right fiscal and monetary policy execution.