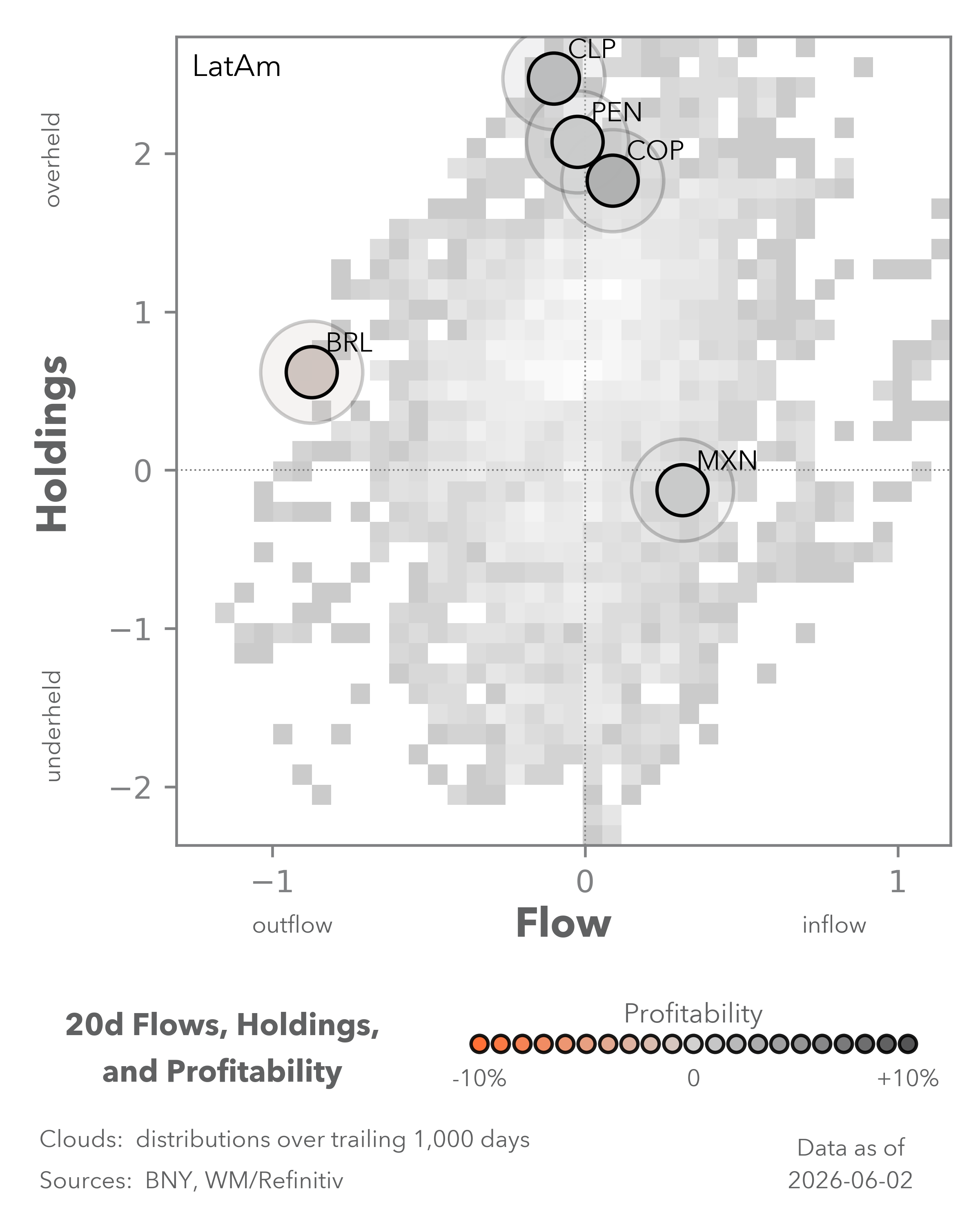

Drawing the right lessons from inflation expectations

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

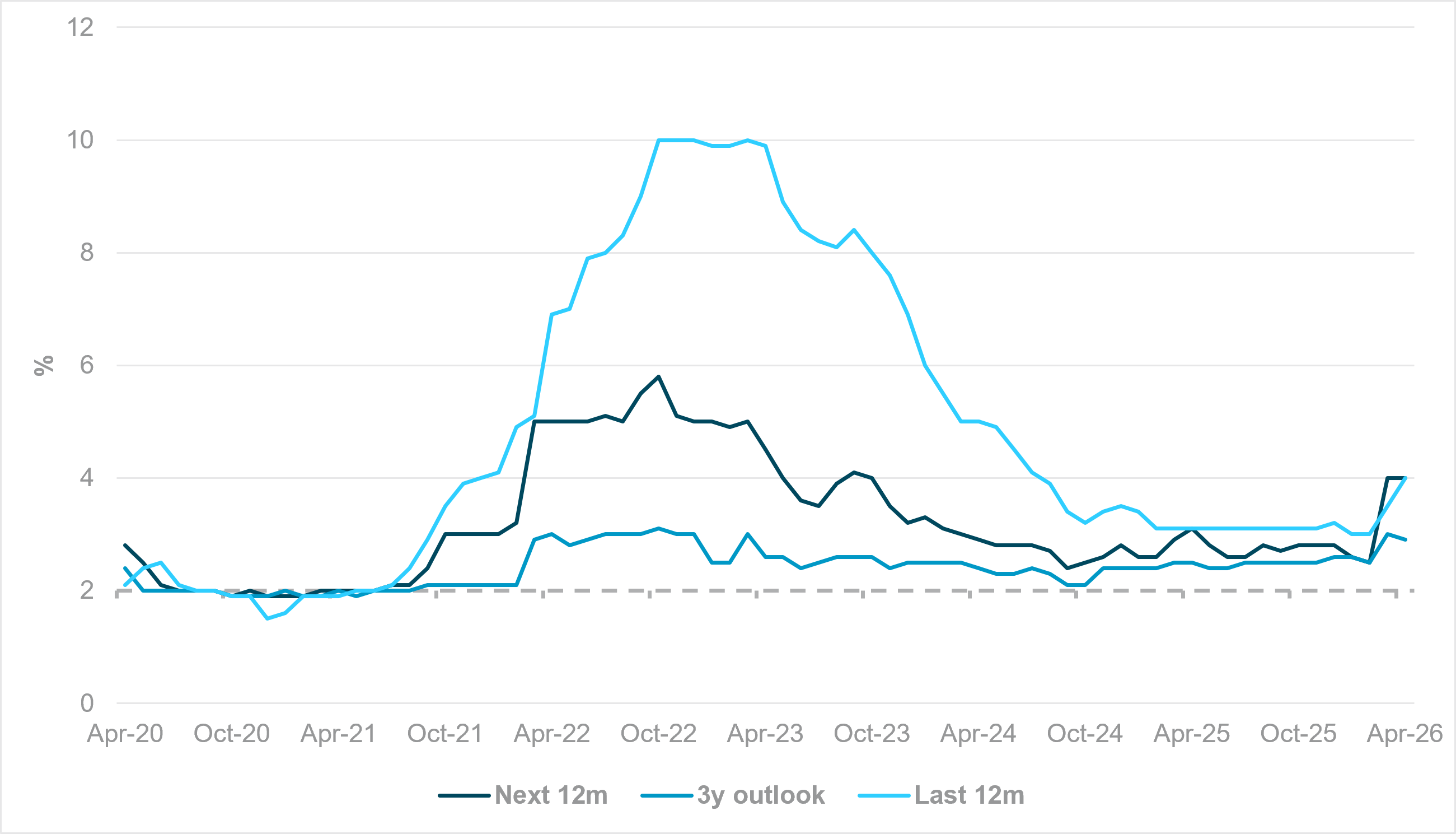

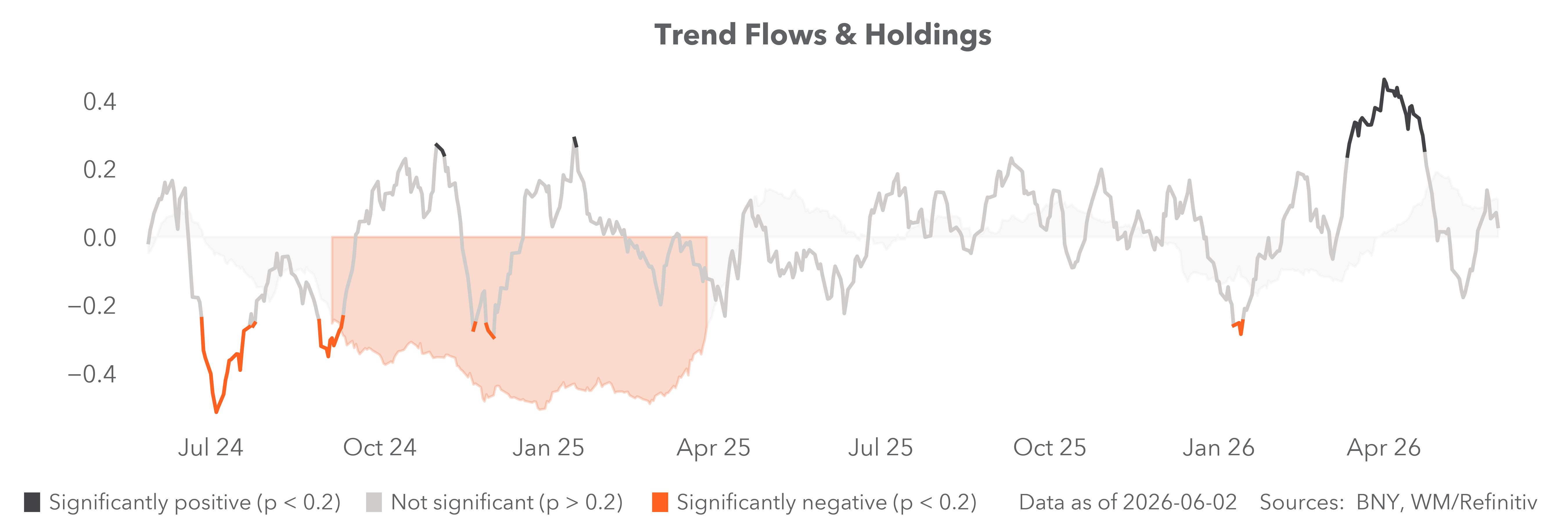

EXHIBIT #1: EUROZONE CONSUMER SURVEY, INFLATION EXPECTATIONS RESULTS

Source: BNY, Bloomberg LP

Our take

The ECB enters its pre-decision blackout period today. Given that anchoring inflation expectations is central to the Governing Council’s mandate, a hike on Thursday is all but confirmed. The April Consumer Survey – which saw another print above 3% in the 12-month forward inflation expectations figures – seals the deal, with households anticipating 4% again for the second month running. Nonetheless, we believe the Governing Council should not automatically see this as a repeat of 2022, and any attempt to draw immediate parallels risks further policy error. Forward inflation expectations began moving in Q3 2021 and stabilized at a high level six months later.

The onset of the Ukraine conflict then amplified expectations and notably, began to move the three-year inflation view as households realized the shock would have structural implications. Crucially, the ECB did not hike until July 2022, after two supply shocks had already taken place. We concede that the first shock in late 2021 was not accompanied by a move in three-year inflation expectations so an immediate move can happen in a “precautionary” context, but there is time to observe changes in medium-term expectations.

Forward Look

A key point of debate – which is already happening for the Bank of England – is whether the tightening already priced in has helped tighten financial conditions and “bought” central banks some time as household expectations shifted. The latest round of services PMIs confirms this view, with almost every single Eurozone economy showing a contraction, indicating a sharp decline in household demand as cost-of-living pressures weigh. Again, this is totally distinct from the last cycle, where demand was already expanding rapidly in 2021 with the first post-lockdown re-openings of individual economies, sowing the seeds for the prolonged period of supply pressures for the rest of the cycle. The ECB should recognize that households have long memories and are also doing some of the tightening for the Governing Council.

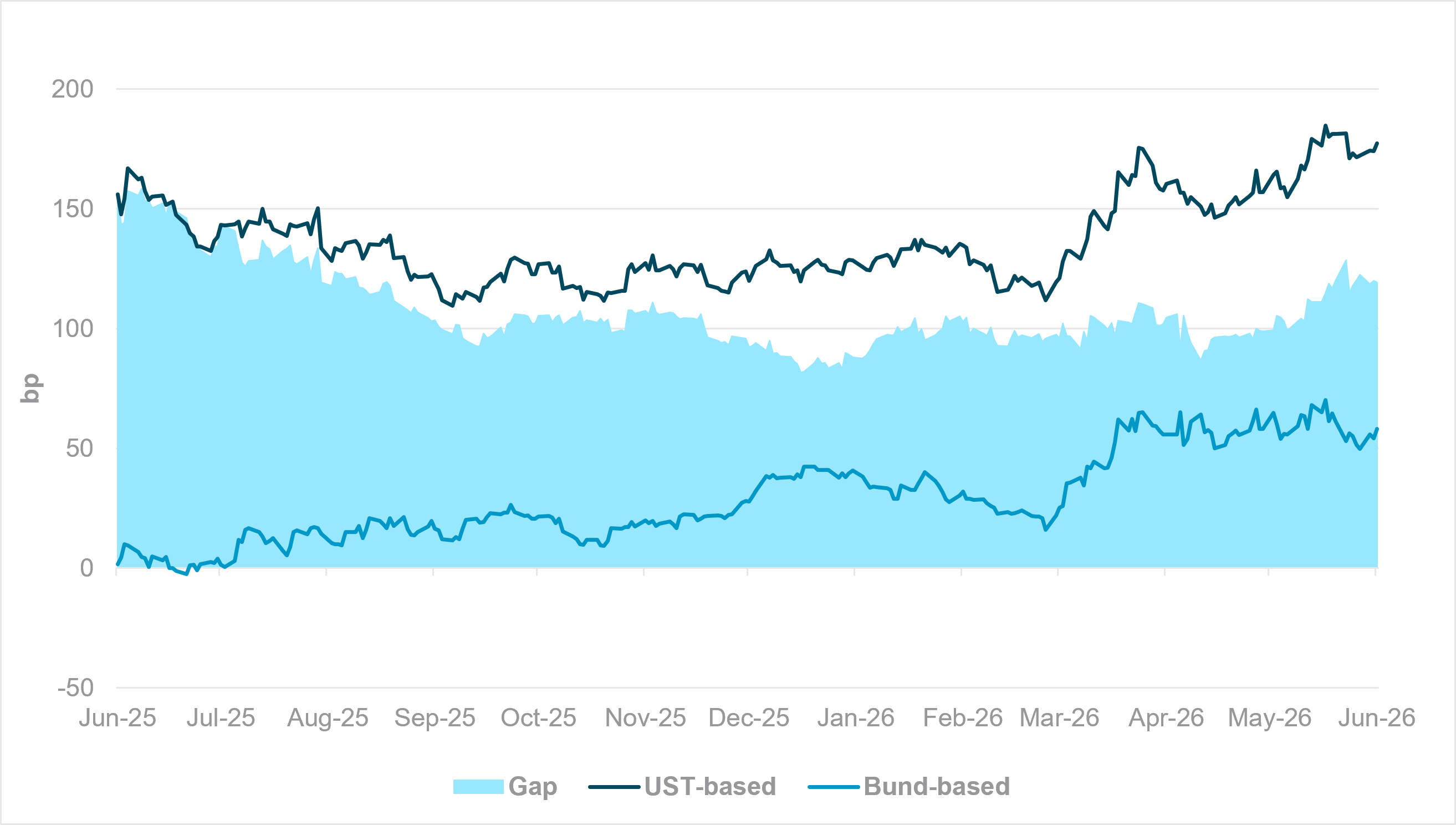

EXHIBIT #2: EUR CAN’T COUNT ON PASS-THROUGH DISINFLATION EVEN AFTER A HIKE

Source: BNY, Bloomberg LP

Our take

Current pricing for the ECB remains well ahead of the Fed and peers, but the EUR is struggling to benefit. As with any carry model, real rates are now driving the marginal changes in currency performance, and current developments do not favor the currency. Firstly, if the net cost to Eurozone growth from a hike proves stronger than anticipated, the market will price in forward easing swiftly, with some dampening in risk-free yields such as Bunds. Breakeven inflation, as seen in the U.S., may not have increased markedly, but the lack of further gains in Bund yields due to growth concerns will undermine performance, in the same way that the drop in equity holdings is already impacting the euro through asset rotation.

Secondly, the market is still far from pricing in a Fed hike this year (if at all), but commensurate steepening in Treasurys is already taking hold. From a growth perspective, data are even holding up to support higher yields. The pricing out of Fed cuts and better energy resilience has also limited moves in U.S. breakeven inflation, while inflation will find better anchoring through gradual adjustments in the Fed’s stance. Consequently, USD’s five-year real rate advantage over the EUR’s is now at its strongest in over three quarters.

Forward Look

We continue to question the view that ECB hawkishness will benefit the euro. On the margins, some increased hedging may be necessary, but iFlow figures indicate the EUR is now losing ground in holdings across the board, largely driven by domestic investors adding hedges on overseas investments, especially in the Eurozone. Even the Swiss franc has moved into net overheld for the first time since June 2022. The EU itself has long called for improved competitiveness to boost trend growth, which in turn will help real rates, but the market is increasingly losing confidence that the Eurozone economy can return to this track in the near future.

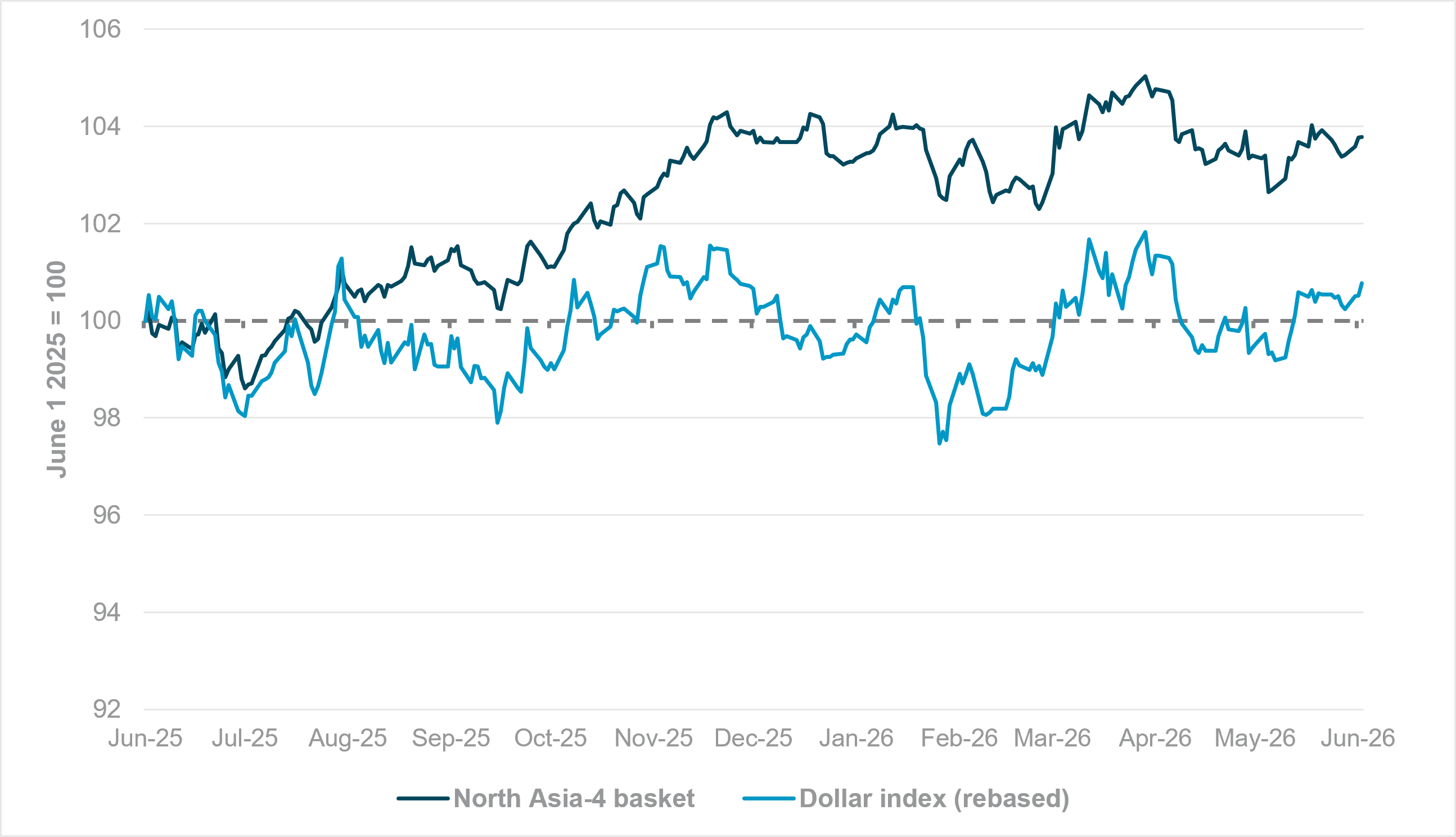

EXHIBIT #3: USD PERFORMANCE IN THE LAST 12 MONTHS – DXY VS. IMPORT-WEIGHTED NORTH ASIA BASKET

Source: BNY, Bloomberg LP

Our take

Japanese PM Sanae Takaichi’s comments on Wednesday as USDJPY approaches 160.00 have once again raised the specter of intervention. Given she hinted that anything would be done in “cooperation” (or even coordination) with the U.S., it is clear that the U.S. sees the JPY as undervalued. Although U.S. Treasury Secretary Scott Bessent refrained from directly commenting on the JPY during his recent trip to Japan, his linking Japan’s “strong fundamentals” to “excessive FX volatility” is perhaps a nod toward fair-value adjustment.

Similar comments are applicable to all North Asian exporters. Despite running ever-higher surpluses against the U.S., the dollar appears to be trending back to the high end of its recent range against this group. This matters for U.S. inflation, too, since the U.S. runs trade deficits against all of them; weighted by their year-to-date U.S. import shares, the USD vs. North Asia basket (CNY, JPY, TWD and KRW) is up near 4% this year. In contrast, the broader dollar index, which reflects USD performance against traditional names, is also up 1%.

Forward look

There is a strong case for USD to outperform the latter group due to growth and policy differentials. However, in terms of balance-of-payments adjustments, North Asian exporter currencies are not reflecting the changes in their respective terms of trade. Ironically, only CNY is strengthening against USD, but its current account surplus is the lowest of the group at 3.7% of GDP as of Q1. The other three economies are all running surpluses of 5% of GDP or higher – over 22% in Taiwan’s case. Even traditional concerns about market share are difficult to justify at present, especially for South Korea and Taiwan, as very large technical and regulatory barriers make it unlikely they’d lose their chip leadership. Demand restraint is gradually easing across the region, and that will help real effective exchange rates recover. At the same time, we expect the U.S. to strengthen calls for those currencies to reflect “strong fundamentals” of the economies. Doing so would also help the Fed avoid a USD valuations overshoot, which would complicate monetary policy.