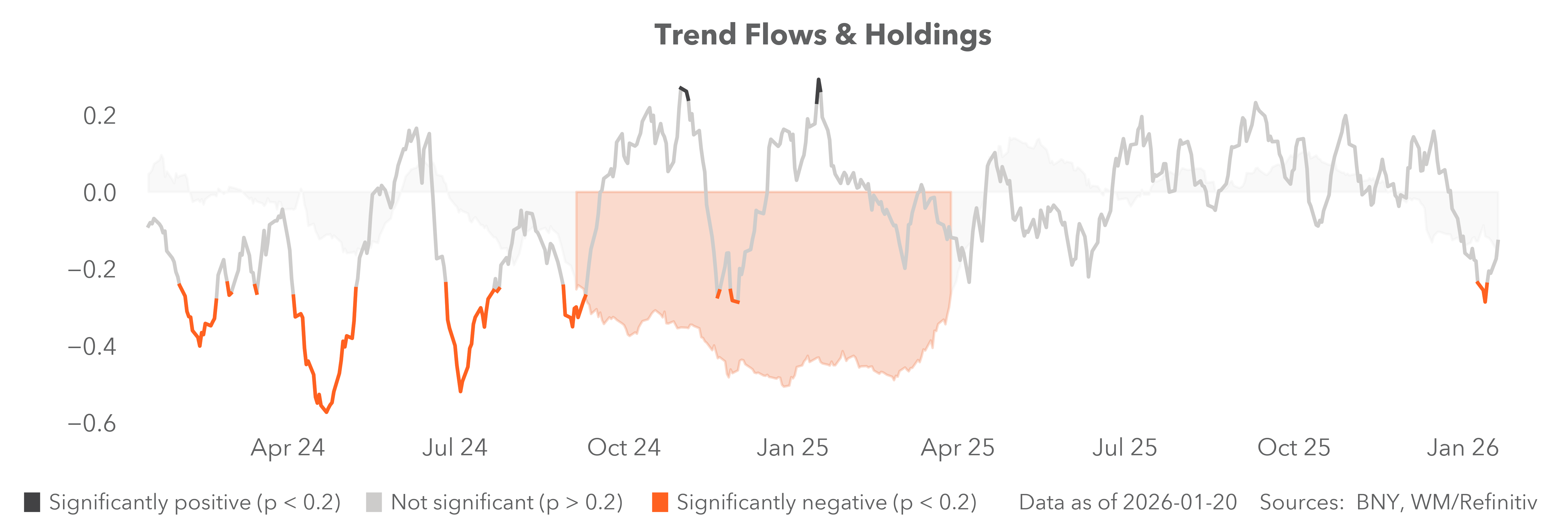

Carry exposures come into focus

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

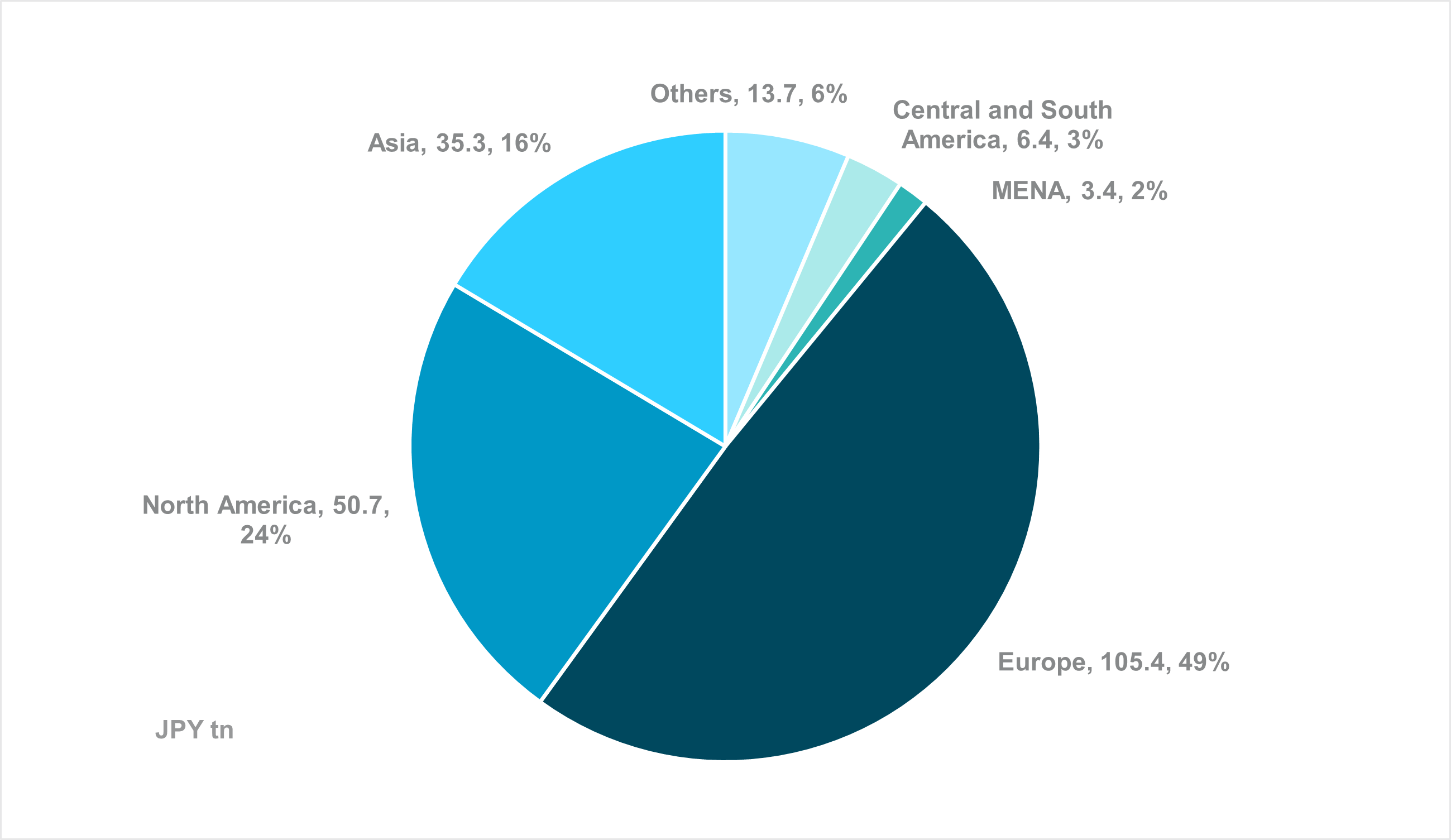

EXHIBIT #1: FOREIGN JGB OWNERSHIP BY REGION

Source: Ministry of Finance JGB Newsletter, June 2025, BNY

Our take

For all the talk this week of geopolitics driving steepening and rotation in global sovereign bond markets, the ongoing selloff in Japanese government bonds (JGB) likely takes precedence over other esoteric factors. Since the campaign period for the snap election is extremely short, most asset allocators with direct JGB exposures are likely to wait for a conclusive result and swift government formation. Only then will they consider adjusting positioning based on new fiscal policies. The current drivers are well-documented, and we would not rule out a wider shake-out in the event of an uncertain result or ongoing issues with fiscal credibility.

Beyond the implications for global sovereign curves, it is important to highlight the direct external exposures to JGBs, which will require swift risk management. Amid rising yields in recent years, foreign ownership of JGBs has steadily increased, reaching about 11.6% of total as of Q1 2025, according to Ministry of Finance (MoF) surveys – almost double the mid-single digits seen in 2010 and during Japan’s extended zero interest rate period. Including corporate bonds and local government bonds, these exposures peaked at ¥231.7tn in 2022. By the end of 2024, foreign holdings had declined to ¥214.9tn, with nearly 75% held by North American and European clients.

Forward Look

European investors account for roughly half of external ownership of Japanese fixed income, based on the MoF survey. While the ¥105.4tn, headline figure is large, outright duration exposure is likely more limited. As of Q2 2025, total foreign JGB ownership was heavily skewed toward T-bills over longer-dated securities (¥75tn vs. ¥63tn). The skey means significant curve steepening is unlikely to cause large losses that could trigger further unwinding. However, strong liquidity preference leaves foreign investors, especially in Europe, highly exposed to JPY movements instead. Repeated JPY weakness in recent months, despite multiple risk-aversion episodes, suggests even short-dated holdings present a greater risk. Consequently, while the U.S. has been much more vocal about APAC currency valuations, the ECB should also remain attuned to the risks posed by excessive JPY weakness. Beyond competitiveness concerns for European industry, financial stability may also matter.

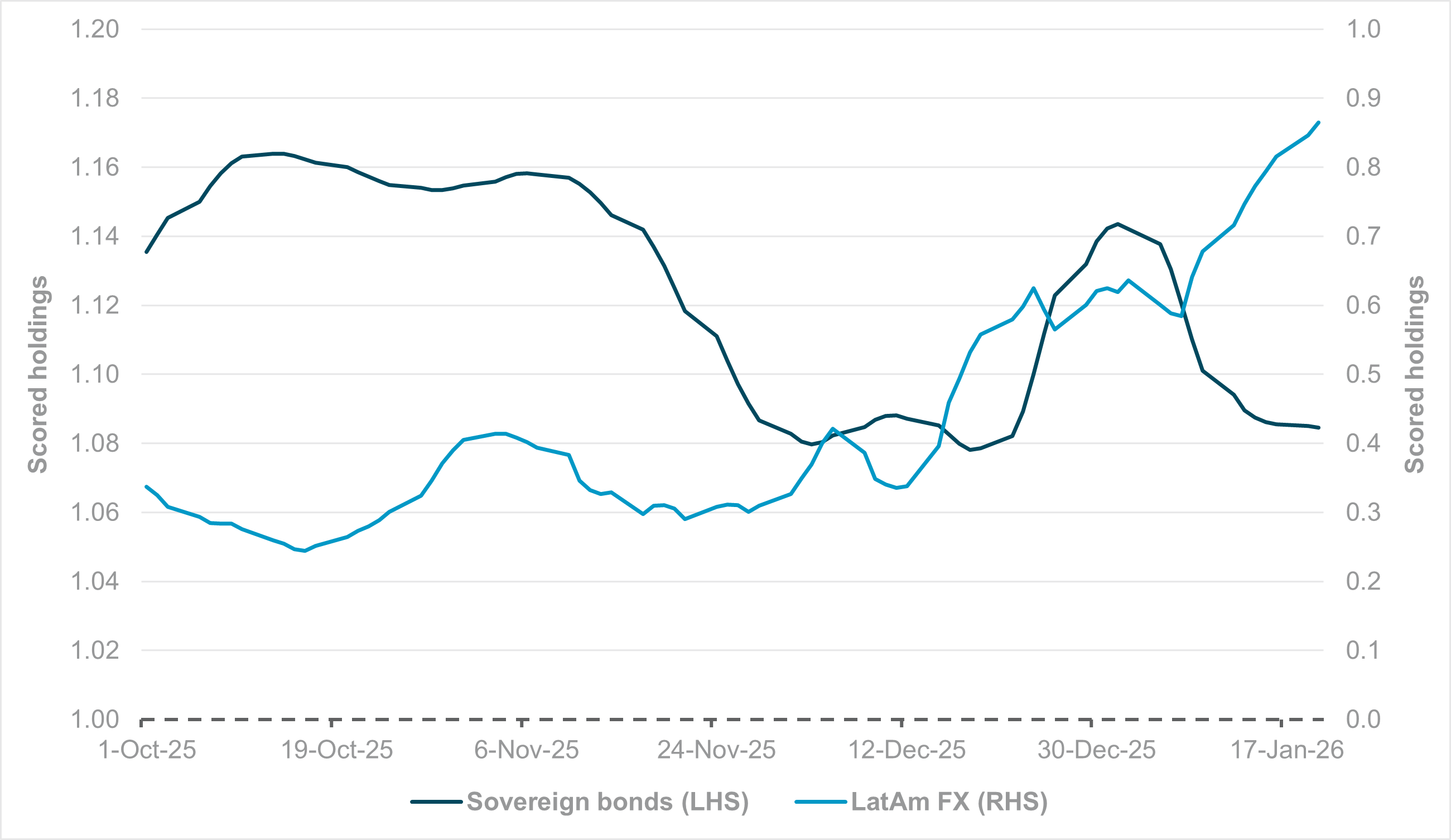

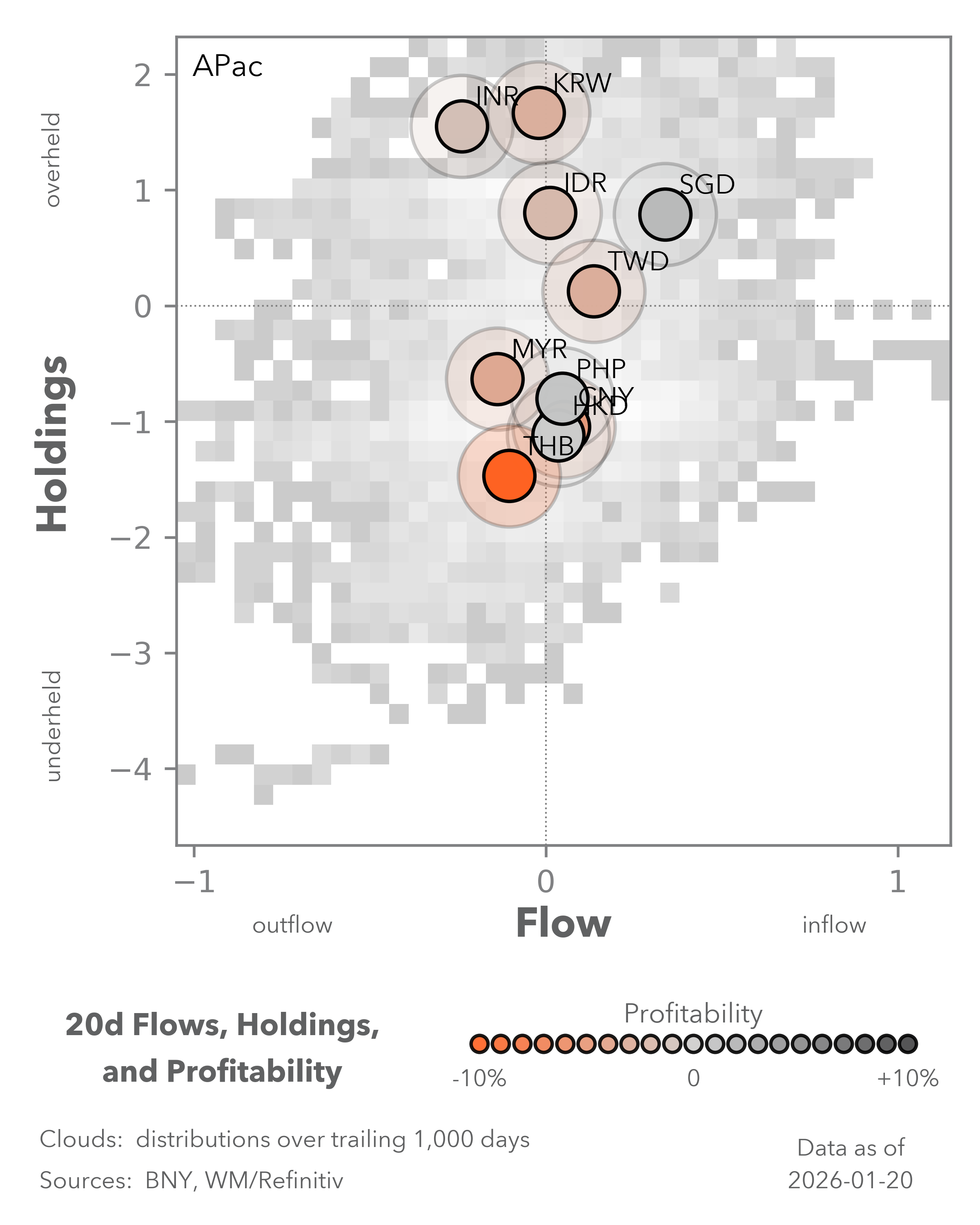

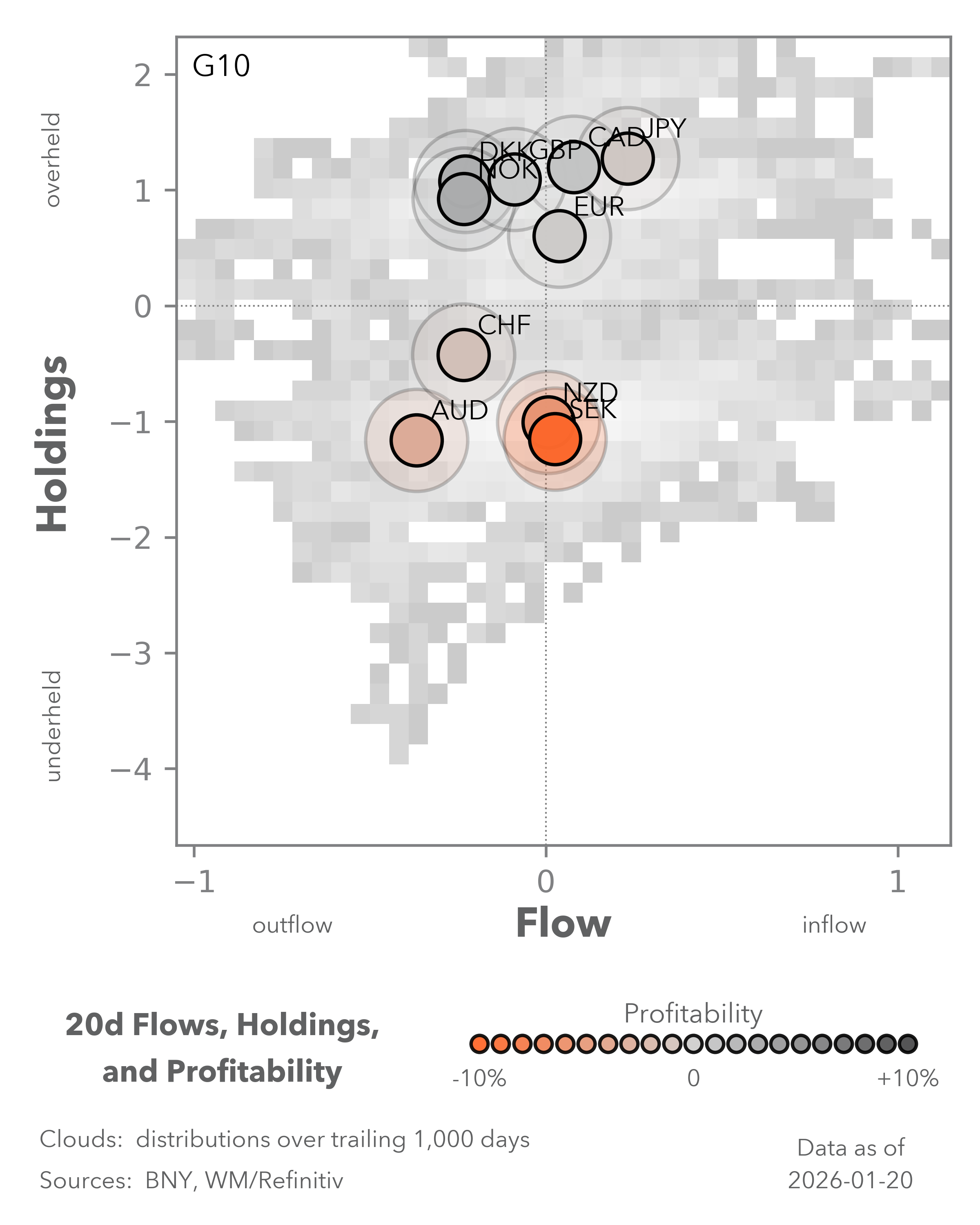

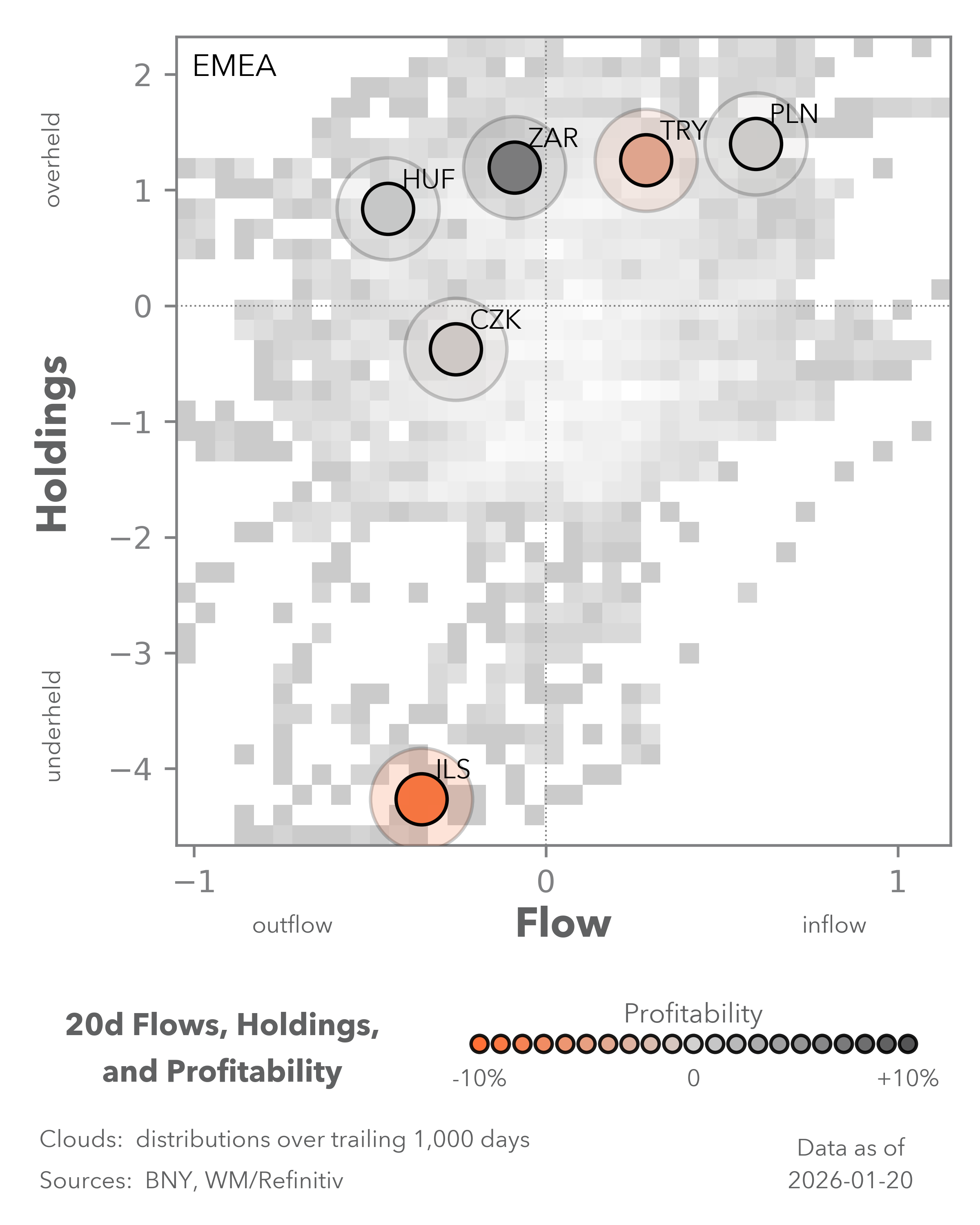

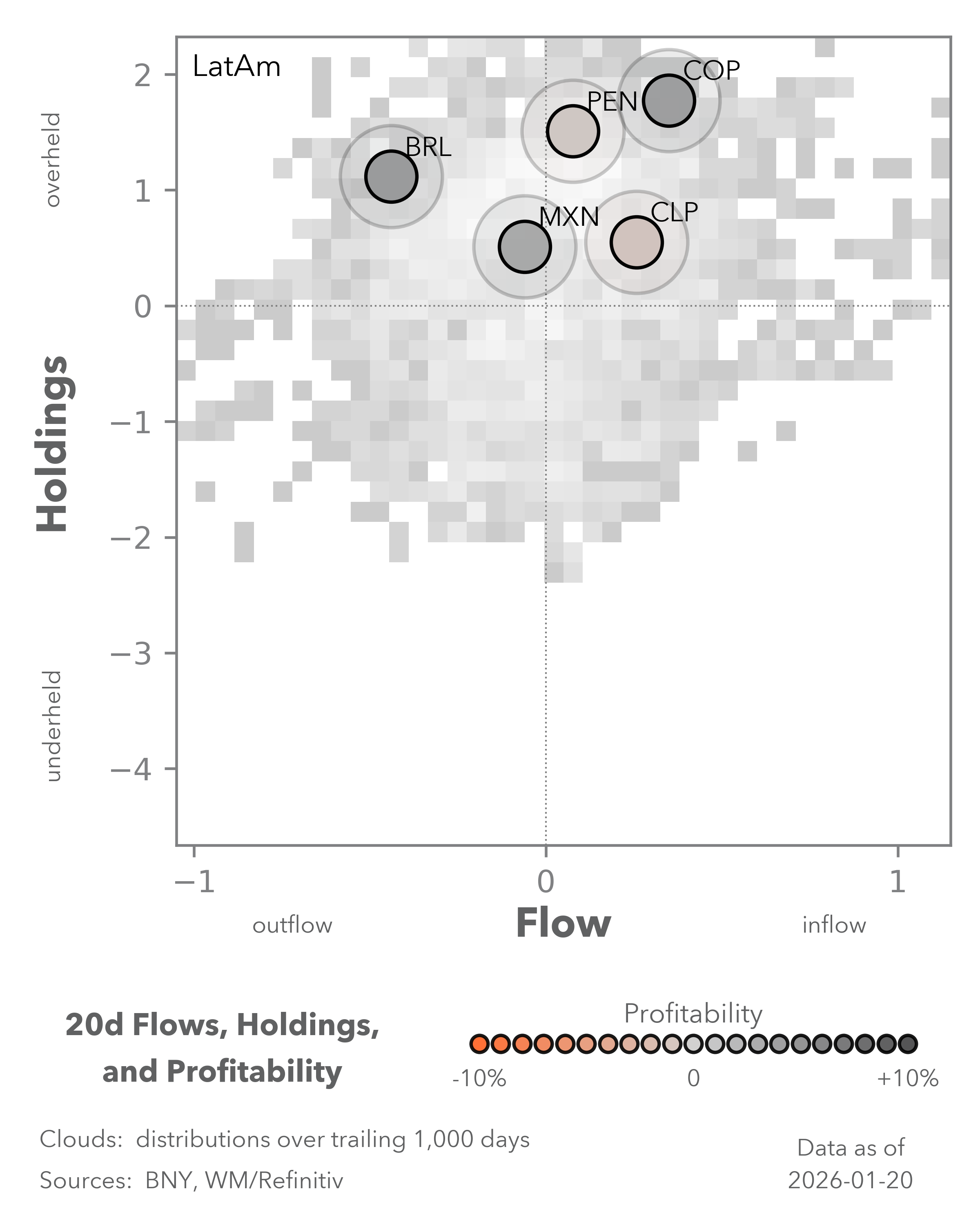

EXHIBIT #2: SCORED HOLDINGS IN EM AMERICAS BONDS AND LATAM FX

Source: BNY

Our take

Geopolitical concerns in recent sessions have dented stock markets, but we have not seen a stronger impact on carry positioning, which remains at the highs. We believe the funding base for carry trades is currently more diverse, which has rendered high-yielding currency holdings more resilient. Furthermore, the prospect that real rates will continue to hold firm is supportive. LatAm remains a key region anchoring carry trades, and current holdings have tripled since the beginning of December.

Surprisingly, bond holdings were unchanged over the past month, despite a late year-end surge. To reconcile this behavior, we believe that contrary to arguments against valuations, hedges in LaAm bond markets are now being removed. Investors are more willing to add to total return exposure and let FX do more of the work.

Forward look

Several LatAm central banks will make rate decisions next week. Colombia is expected to hike by 50bp, pushing its nominal lending rate back toward double digits and lifting the real rate near 5%.

Perhaps wary of steepening curves globally, asset allocators appear willing to shorten duration. Holding outright currency positions or reducing hedges can shift overall exposures if bond flows remain subdued. We expect the clear delineation in emerging market (EM) asset allocation to persist. FX and carry trades will dominate LatAm and EMEA, while APAC equities should continue to benefit. However, lower hedge ratios in some funding currencies are likely, given valuation extremes.

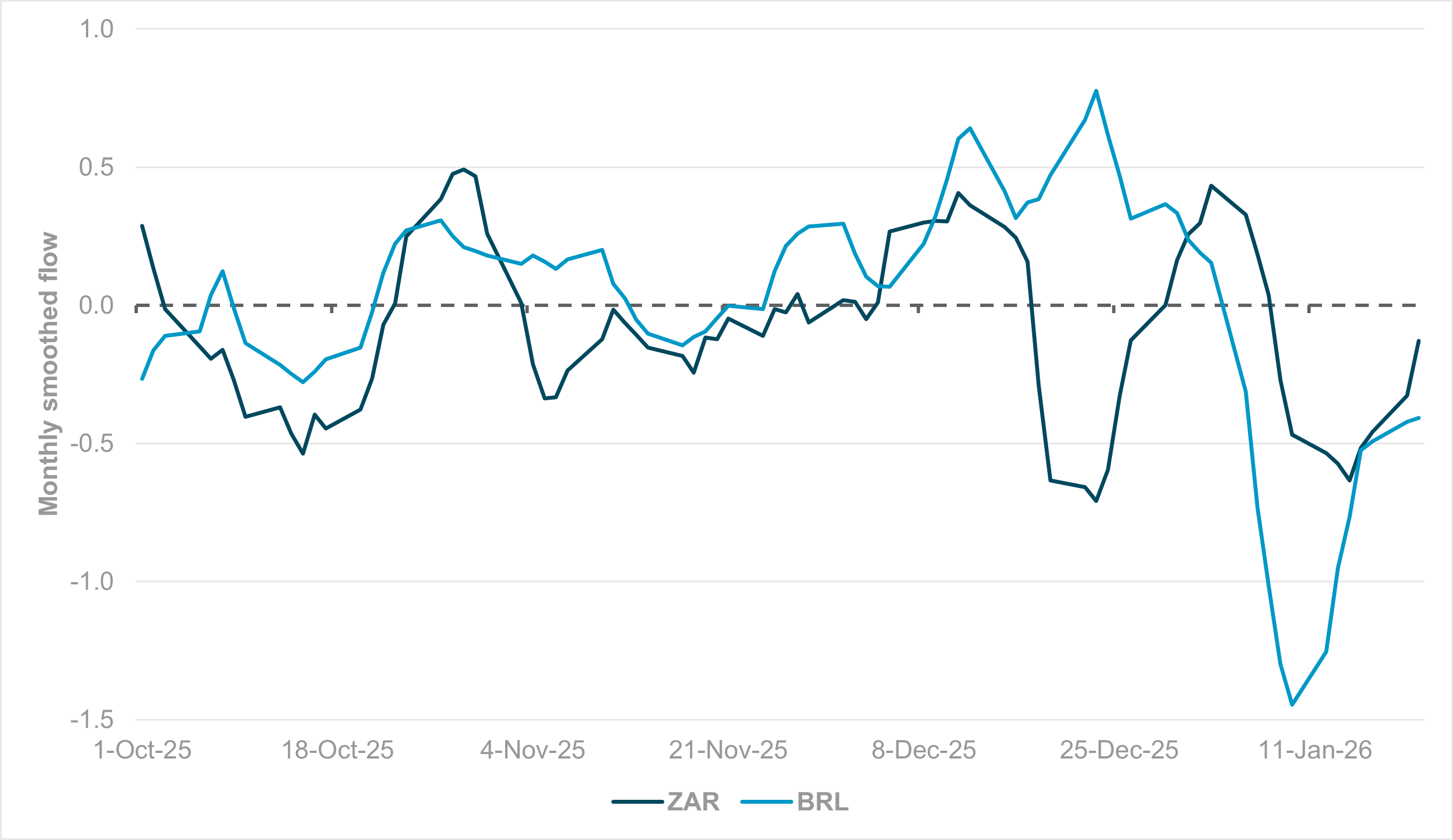

EXHIBIT #3: MONTHLY SMOOTHED FLOWS IN ZAR AND BRL

Source: BNY

Our take

The recovery in outright FX exposures – despite valuation concerns – is becoming clear in benchmark names such as ZAR and BRL, both of which will come under scrutiny next week as their central banks meet. BRL started the year weak and appeared at risk of significant geopolitical weakness due to ongoing tensions in its bilateral relationship with the U.S. Elections later this year will also be a factor that could impact positioning.

Meanwhile, ZAR has continued to perform well. Still, questions remain over the durability of the current commodity rally, which has likely driven valuations beyond what is justified by clear fiscal and governance improvements. Both currencies are comfortably overheld and profitable, and we expect any hawkish tilt to lead to further unwinding of current hedges and help push smoothed flow averages back into net positive.

Forward look

Assuming geopolitics takes a back seat as more central bank decisions loom, holdings levels of high-carry currencies will likely struggle to make new highs in the near term.

Month-end rebalancing, combined with growth risk from tight real-rate and currency-driven conditions, will exert a policy toll. The question is whether this trend will be uniform or if markets will begin to differentiate. For example, ZAR and BRL – despite differing commodity and growth exposures – have largely seen flows move in unison, aside from a brief divergence during the holiday period. Fed signaling has played a key role in this process, but as valuations hit cyclical extremes, we expect more scrutiny over the prospect of further re-rating. Only then can the current picture of “less selling” in well-held EM currencies shift into “more buying.”