Validation vs. rotation

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

Q4 earnings are now underway, with investor attention sharply focused on AI-related growth prospects and the associated risk of valuation excess. This debate was prominent at the World Economic Forum, where CEOs of major technology platforms emphasized the importance of broad-based global AI adoption to drive productivity gains and improve economic outcomes. Nvidia’s commentary, including its multi-layer infrastructure framework, underscored the scale and duration of the current investment cycle. While the strategic case for AI as a catalyst for wider economic benefits is increasingly well understood, confirmation will depend on whether non-technology sectors can translate AI investment into tangible improvements in growth and margins over the coming year.

Markets are entering a critical “validation” phase in which earnings must demonstrate that demand for technology leaders remains strong and that their revenue and cash flow profiles are sufficient to underpin consensus expectations for U.S. growth and earnings through 2026. At the same time, rotation dynamics have persisted, with Materials, Energy, and more recently Consumer Staples attracting incremental flows.

This backdrop raises three key questions for investors:

Does the capital cycle drive positioning shifts?

Do valuations better predict future returns or margin outcomes?

Can sector rotation occur without becoming a zero-sum trade?

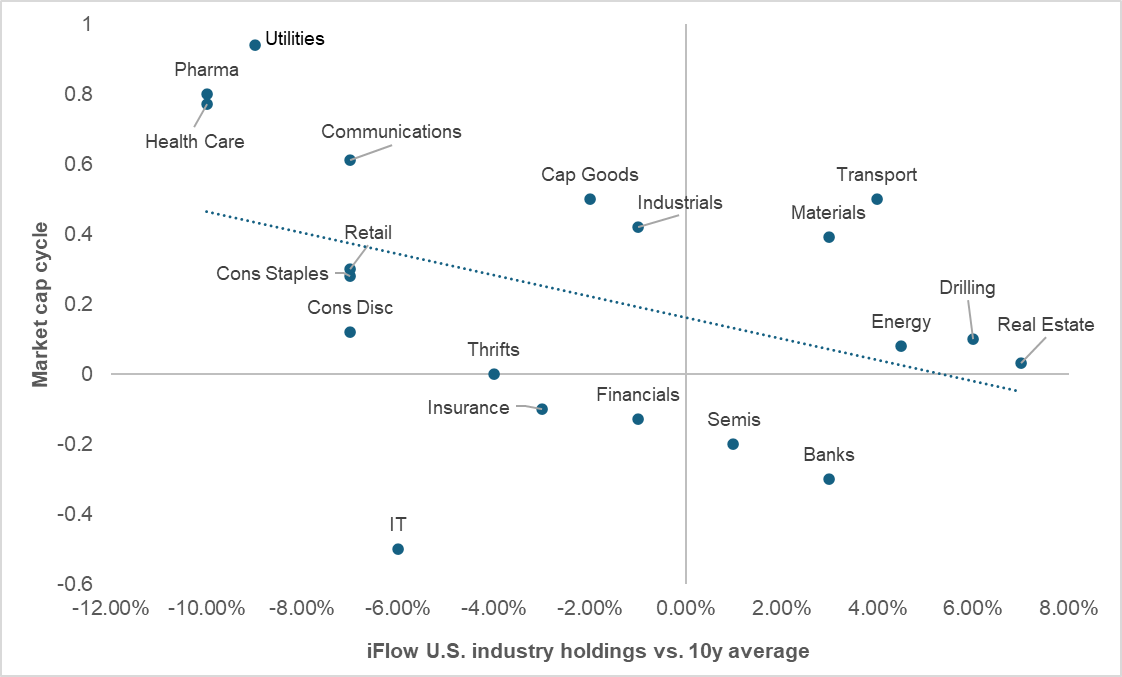

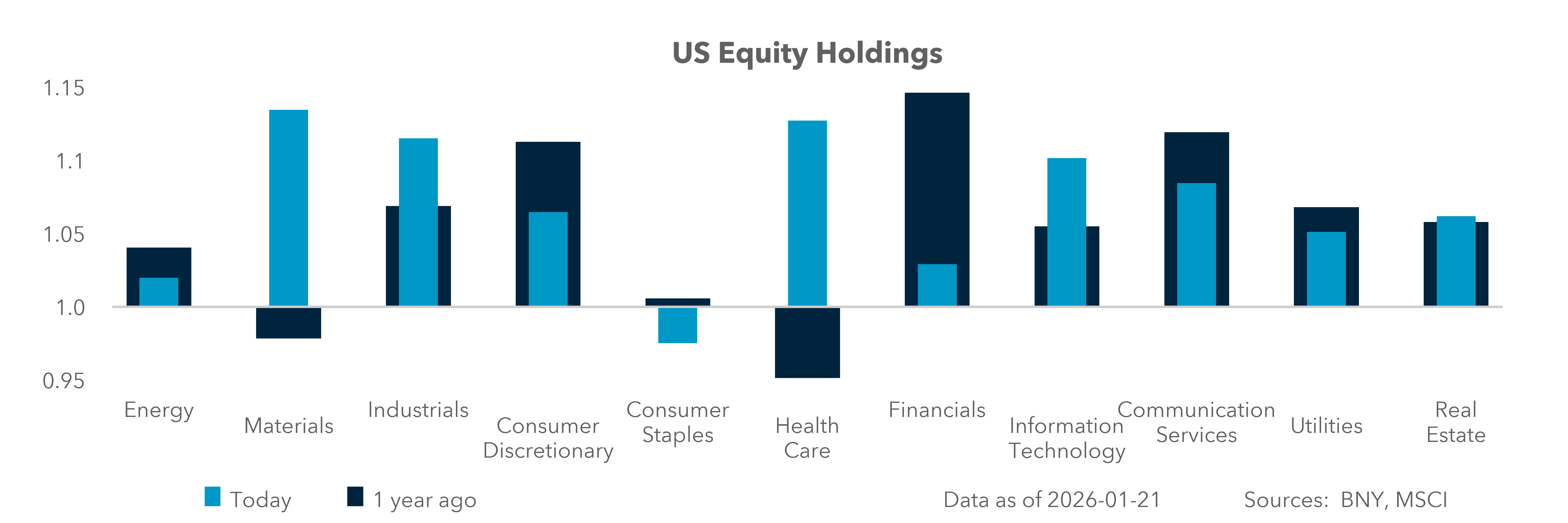

EXHIBIT #1: DOES THE CAPITAL CYCLE LEAD POSITIONING?

Source: BNY, Bloomberg

Our take

We frame the market capital cycle by comparing each sector’s current share of the S&P 500 with its historical peak-to-trough range over the past decade. On this basis, only two of the 11 sectors remain in a downcycle, while the majority are entering the initial stages of an upcycle.

This reinforces evidence of an ongoing rotation away from the Magnificent 7 toward the broader 493 constituents. Positioning data into Q4 earnings similarly indicate reduced exposure to mega-cap technology and increased allocations to lower-valuation sectors and industries. Energy, Real Estate and Materials have been the primary beneficiaries of this shift. More notable, however, are the two largest sectors – Financials and Information Technology – that remain in a capital downcycle and are under-owned relative to their 10y averages.

The capital cycle remains a critical lens for assessing how much further sector-level selling can occur without undermining the broader S&P 500 uptrend. As shown in Exhibit #1, the resilience of consumer-driven earnings will be central to maintaining market stability through any continued rotation.

Forward look

The principal risk in any sustained handoff in market leadership away from technology is the capacity of other sectors to absorb incremental capital without developing valuation excesses of their own. Over the next three weeks, the key drivers for the S&P 500 will be margin performance in the Consumer Staples and Consumer Discretionary sectors, alongside evidence that these industries are successfully deploying AI to enhance productivity and offset cost pressures.

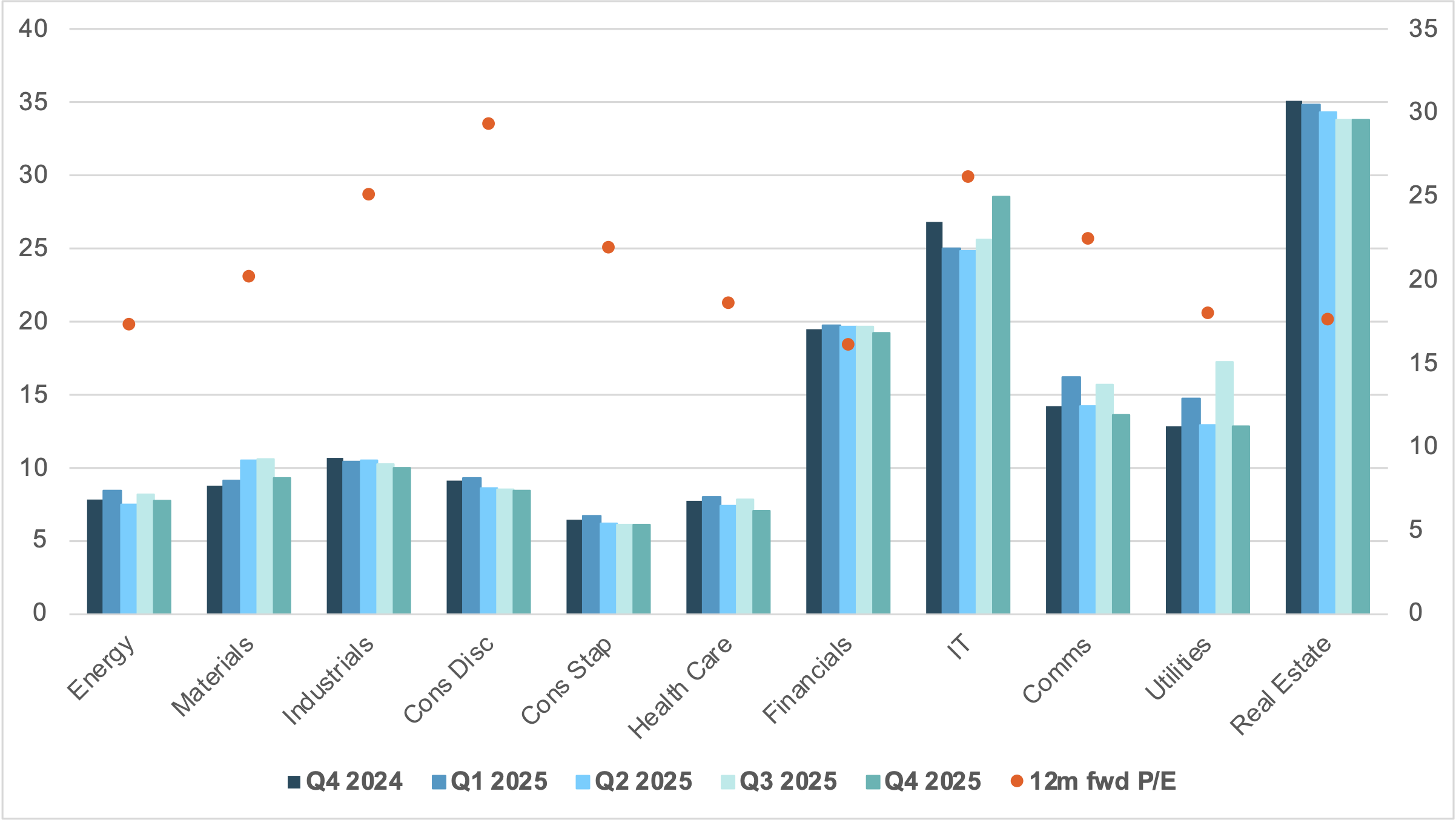

EXHIBIT #2: U.S. EQUITY SECTOR MARGINS AND FORWARD P/E

Source: BNY, FactSet

Our take

Margin expectations for Q4 remain muted, with only the IT sector anticipated to show any improvement. At the index level, S&P 500 margins are trending modestly lower, declining from 13.1% to 12.8%. While still above the five-year average of 12.7%, this does not yet signal a renewed upward trajectory following the gains seen into 2024.

Notably, margin levels and forward P/E multiples remain poorly correlated: Consumer Discretionary screens as the most expensive sector in P/E, while Real Estate delivers the highest margins.

Forward look

Over longer horizons, elevated P/E multiples have historically raised concerns around prospective returns, but margin compression has proven the more material source of downside risk.

Falling margins typically reflect a slowing growth backdrop, rising inflation, or a combination of both. Current market assumptions for 2026 point to stable inflation alongside firmer growth. Historically, this configuration has been associated with positive supply-side dynamics – such as global trade expansion in the 1990s or excess capacity following the 2001 recession. For this outlook to be sustained, AI-related investment will need to translate into tangible productivity gains capable of supporting a comparable macro environment.

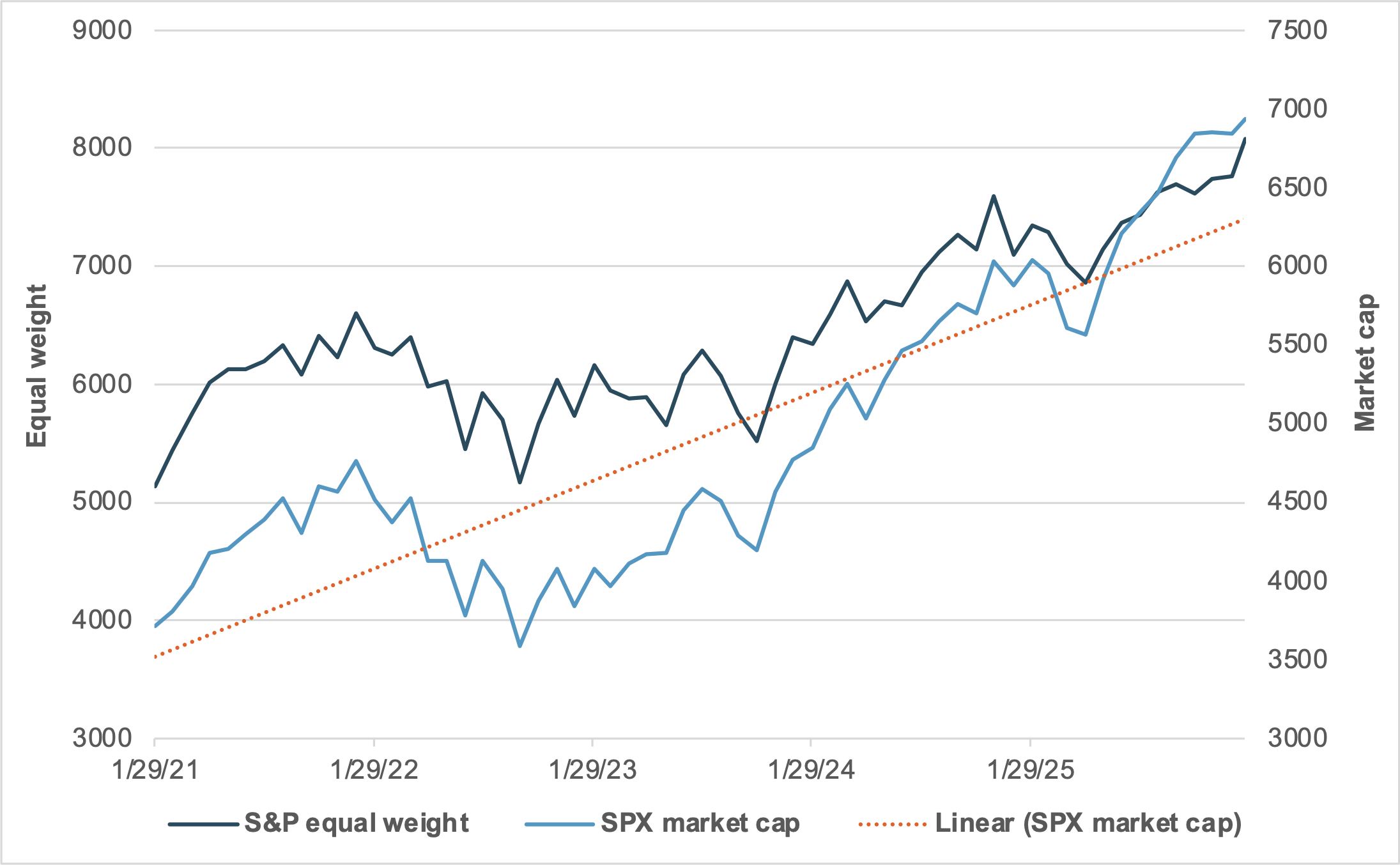

EXHIBIT #3: U.S. S&P 500 EQUAL WEIGHT VS. MARKET CAP INDEX

Source: BNY, Bloomberg

Our take

Technology’s outperformance over the past decade has been the defining investment narrative for the S&P 500. While the period has included several notable corrections, the persistence of this near 17-year bull market (excluding the COVID disruption) has increasingly raised concerns around valuation excesses.

What has been more striking over the past eight weeks is the effectiveness of the rotation out of technology and into other sectors within the U.S. equity market. Relative performance between the NASDAQ and Russell 2000 has shifted by more than 10% over this period, with the Russell 2000 advancing 15%.

Forward look

The primary risk heading into Q4 earnings is whether the rotation trade can be substantiated by improved earnings delivery from currently over-owned sectors such as Materials, Transportation, Energy and Real Estate. For investors, the challenge lies in diversifying exposure toward smaller-capitalization segments without materially inflating valuations.

Factor dynamics – particularly value and size – tend to be decisive during rotation phases, placing greater emphasis on Communications, Consumer and Health Care as potential leaders. The binding constraint may be political rather than economic: efforts by the Trump administration to accelerate U.S. growth while containing inflation leave limited scope for margin expansion, particularly in sectors exposed to consumer affordability pressures.

As Q4 earnings unfold, the market sits at a critical inflection point between validation and rotation. Leadership can continue to broaden without derailing the S&P 500, but only if earnings can deliver more than expected returns and robust outlooks. Focus is on both earnings per share and margins as they confirm that capital is being redeployed productively rather than defensively. The next phase will hinge on whether AI investment translates into measurable productivity gains across consumer-facing and cyclical sectors, supporting margins amid tighter affordability constraints. Absent that validation, rotation risks becoming a source of index-level volatility rather than a healthy rebalancing of market leadership.