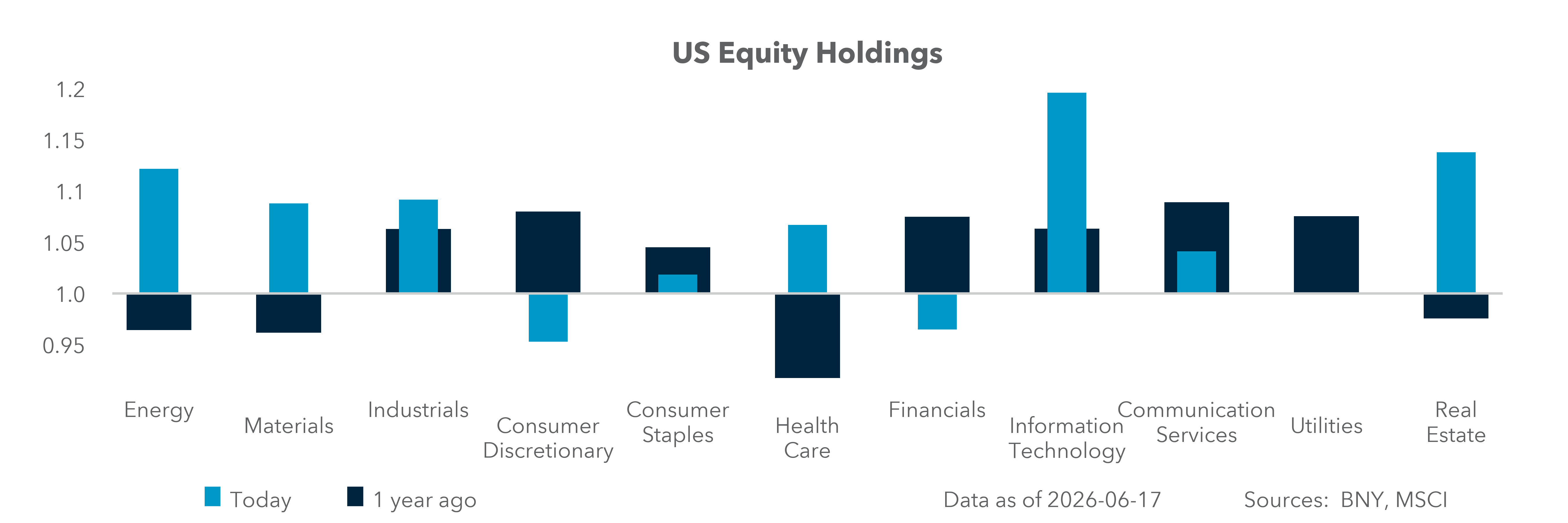

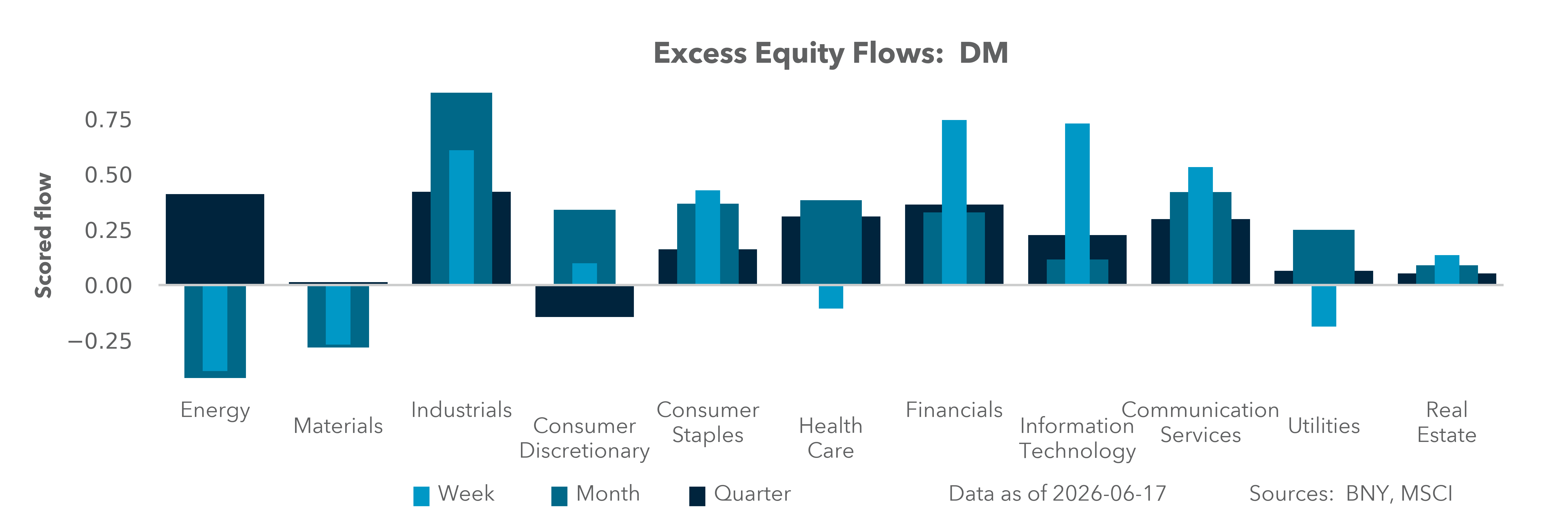

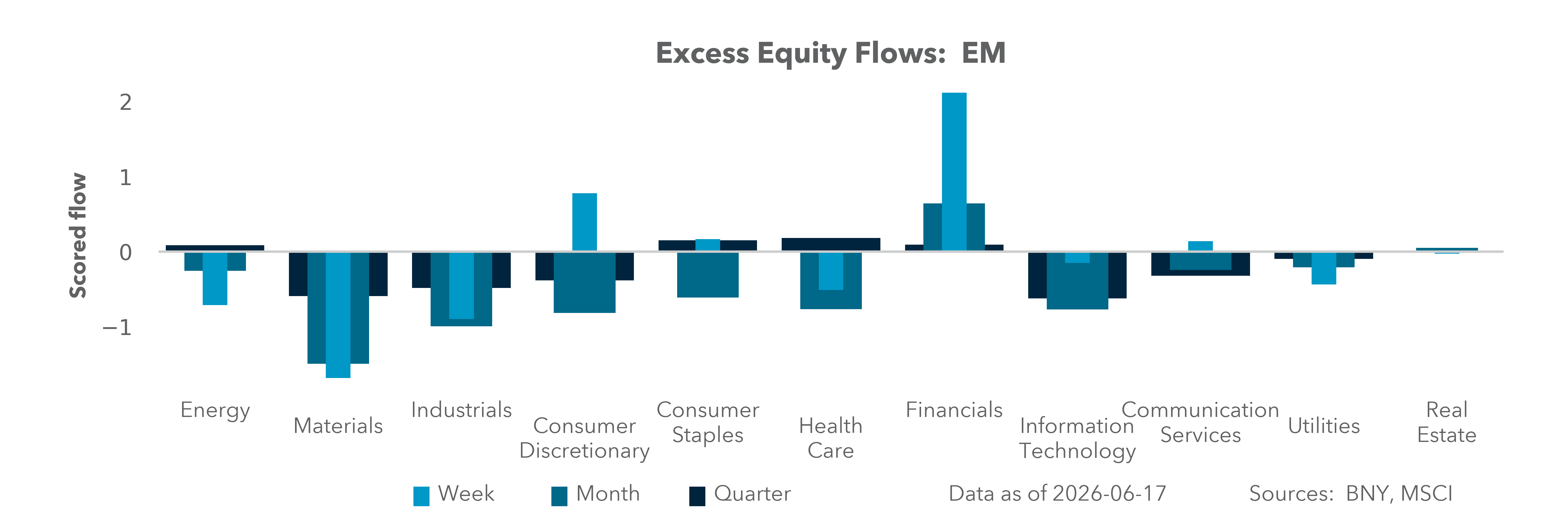

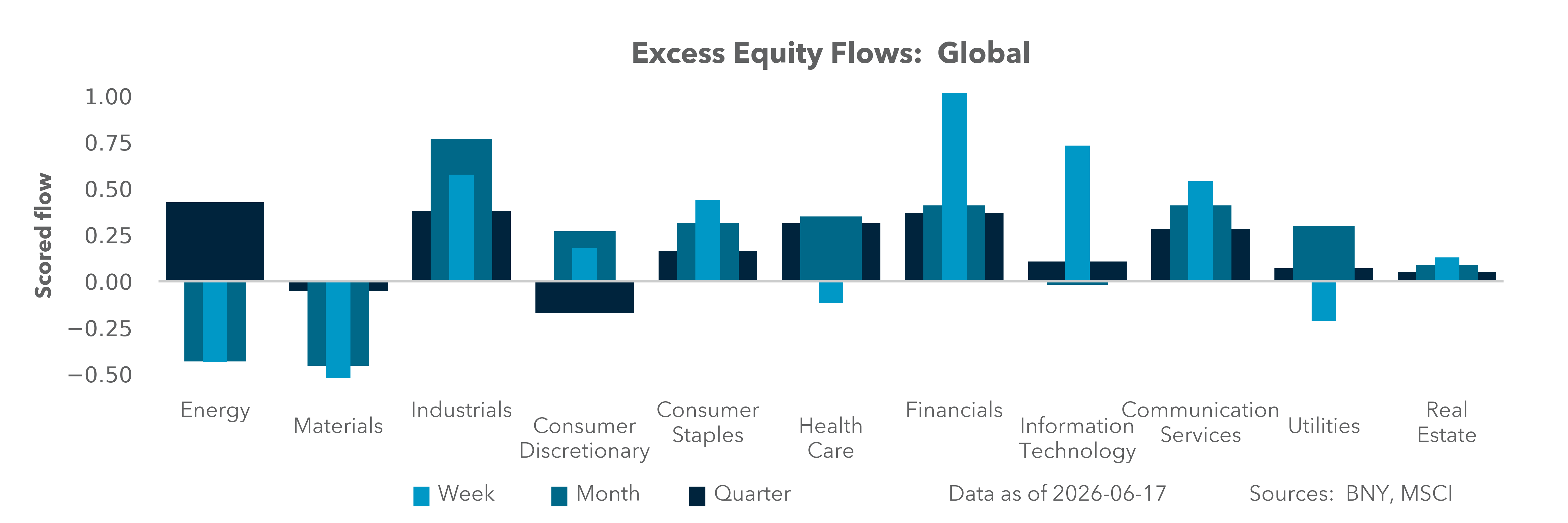

Iran conflict unwind: Energy and tech

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

Energy and technology were the biggest winners globally over the last three months. Some of this traced to the Strait of Hormuz closure and tighter energy supply. However, the squeeze in semiconductors and the ongoing race for AI data center dominance looks different. Mixing AI costs with war shocks has complicated demand-supply forecasting. While correlation is not causality, the urgency to build excess GPU capacity and the data centers to house it may ease, given lower AI token fees, higher rates, and upcoming IPOs from Anthropic and OpenAI. Valuations for both are under scrutiny, with SpaceX now providing a benchmark that defines success on different terms than a traditional IPO.

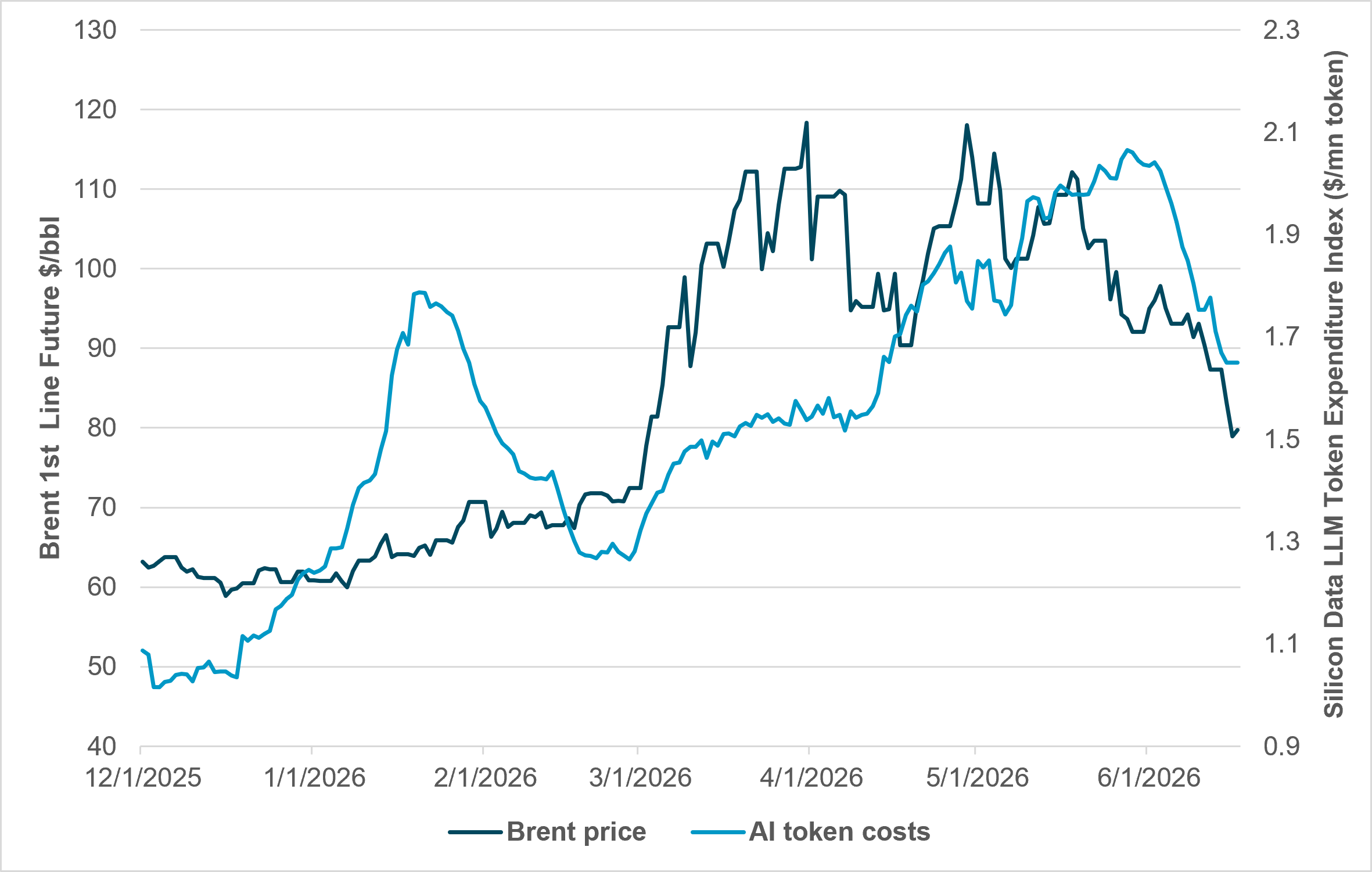

EXHIBIT #1: BRENT OIL PRICE VS. LLM TOKEN EXPENDITURE INDEX

Source: BNY, Bloomberg

Our take

AI token costs and energy prices have only recently moved together. January’s squeeze traced to semiconductor shortages from U.S./China trade friction and renewed data center investment spending. February’s pullback was idiosyncratic – LLM model rollouts stalled amid government pushback on new releases. The war then added energy as another input to token costs, breaking the prior logic. The reversal in oil and token costs will now shape AI adoption economics going forward.

Forward look

GCC supply disruptions hit semiconductors on a second front: helium and petrochemicals critical to chip production also tightened. Even so, LLM token costs and chip costs don't move in lockstep. Rather, the AI rollout across the U.S. economy and the focus on token costs and agentic solutions make the supply-demand equilibrium harder to model. A year ago, a typical AI interaction might have involved a single prompt and response, perhaps 2,000 tokens in total. Today, agentic AI workflows have fundamentally changed that arithmetic. A single task executed by a multi-agent system (researching a topic, drafting a document, validating it against internal policies, then iterating based on feedback) can burn through 50,000 to 500,000 tokens before producing a final output. The evidence of this shift is visible in the data. TechCrunch has reported on a phenomenon known as "tokenmaxxing," in which power users consume extraordinary amounts of compute, driving providers to introduce new pricing schemes. This has led to new price schemes from LLMs and others.

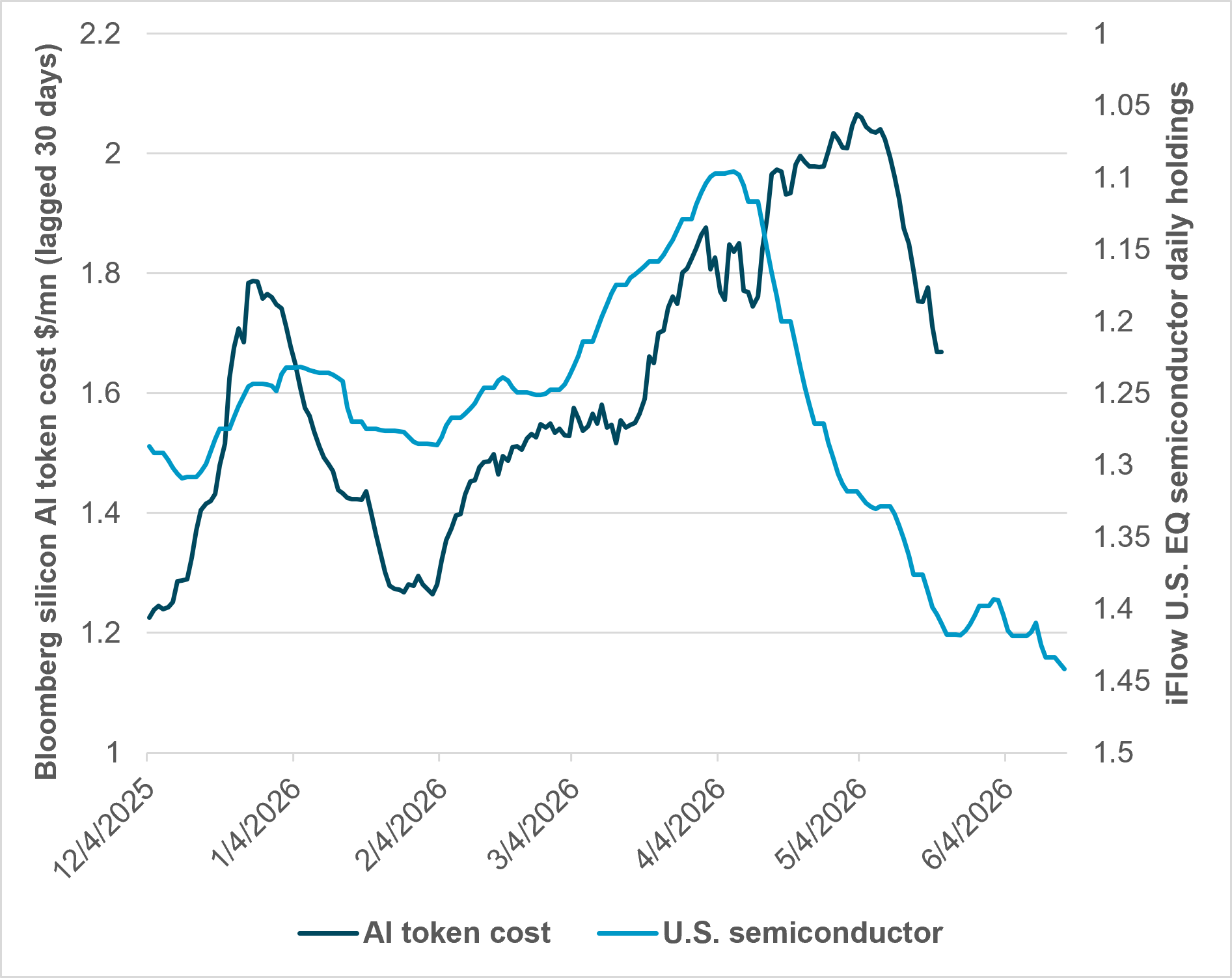

EXHIBIT #2: AI TOKEN COSTS (LAGGED 30-DAYS) VS. U.S. SEMICONDUCTOR HOLDINGS

Source: BNY, Bloomberg

Our take

Semiconductor holdings correlate negatively with AI token cost. Explaining that relationship matters for gauging whether the energy unwind matters to markets. Some analysts argue that agentic adoption is still early-stage, and that falling costs will drive the next demand leg, though there’s too little data on AI token costs to fully gauge investor weighting them. The equity relief rally from lower oil prices also points to a more benign inflation read, with rates more likely to hold steady than rise further.

Forward look

How investors read the Warsh Fed’s approach – looking through inflation and keeping rates balanced – will likely weaken the equity-to-token-cost correlation. For semiconductors, the risk is in curtailed supply chains, new chip costs, and shortening hardware lifespans. A nascent market for GPU chip exchanges – forwards and repos, linked to Silicon Data and the CME – is emerging. Hyperscalers will be watching closely to see whether it delivers real cost stability.

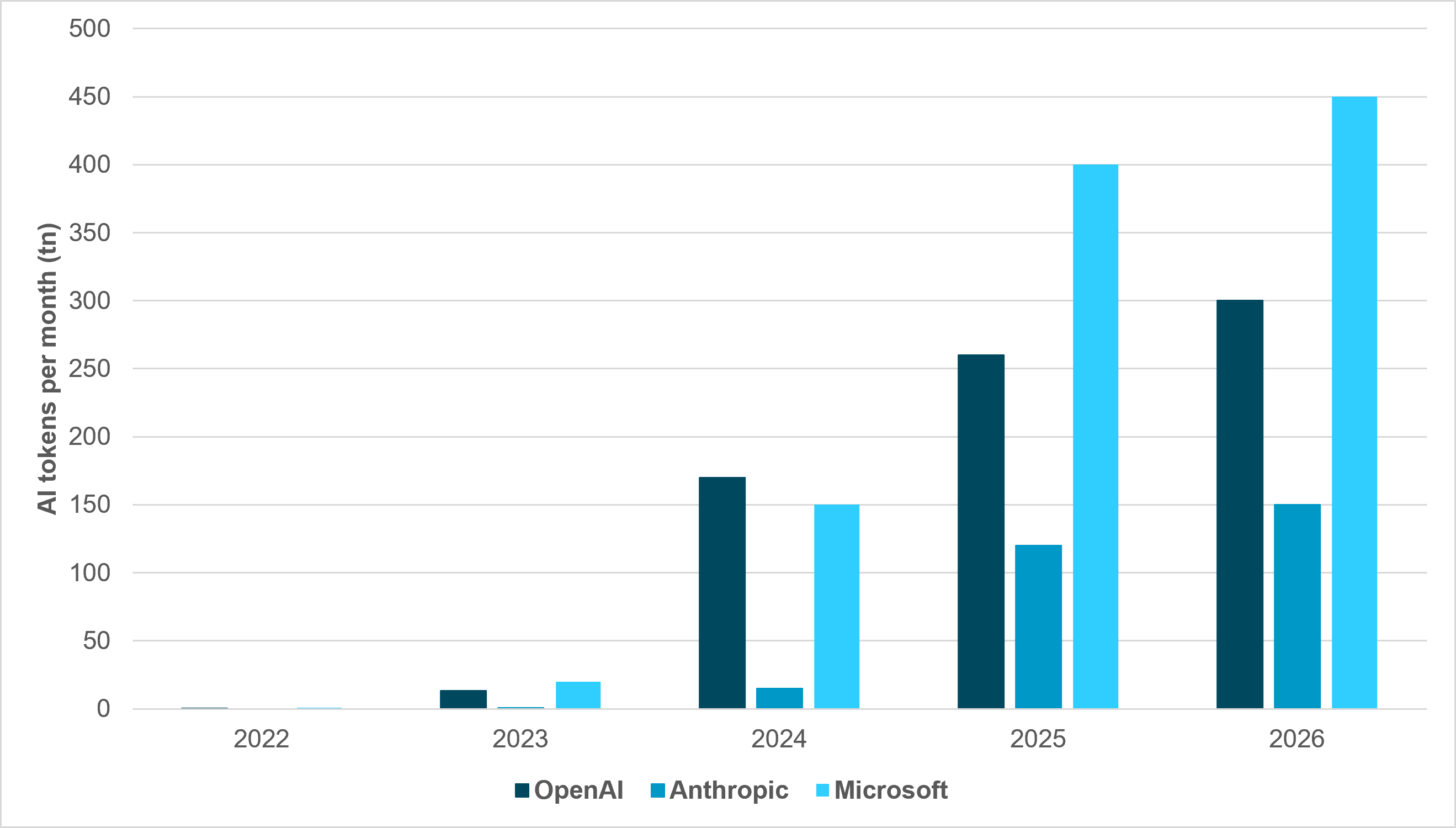

EXHIBIT #3: AI TOKEN GROWTH FOR BIG THREE LLM PROVIDERS

Source: BNY, Bloomberg

Our take

Token volume on LLMs doesn’t map directly to revenue. Anthropic runs the smallest token count but generates the most revenue. Microsoft’s token use is spread across multiple models and yields the least per token. The mix has also shifted: chatbot prompting has given way to agentic solutions, and agents now consume more tokens than humans do. Corporate platforms using AI for web scraping and database indexing account for the largest share, with autonomous “reasoning loop” workflows the heaviest users of input vs. output tokens. Pressure to allocate model capacity more efficiently across the spectrum will likely accelerate this further.

Forward look

The wide dispersion of AI use across businesses shows up in the recent Ramp Study: the median monthly spend per business in April was $2,246, while the average monthly spend was $140,842. That gap reflects how AI spending actually distributes – most companies are in early or moderate adoption, but a single team or automated workflow running unchecked can move you from the median into the average range. IBM’s Global AI Adoption Index found that 33–42% of organizations cite lack of AI skills as a top barrier to adoption, depending on the survey year. Deloitte’s State of AI in the Enterprise report (7th edition, surveying 3,235 senior leaders) found that 84% of organizations are increasing their AI investments, and 78% of leaders reported greater confidence in the technology. Across business, AI demand looks durable regardless of costs.

For equity investors, the central question is shifting from whether AI demand exists to how efficiently that demand translates into sustainable returns across the technology value chain. Recent market performance reflects both cyclical influences, including energy price volatility and geopolitical disruptions, and structural forces tied to AI adoption. While lower token costs may create periodic concerns around pricing power, they are also expanding the addressable market for AI applications and accelerating enterprise deployment.

Agentic AI suggests computing demand could remain well above historical expectations even as model efficiency improves. Supply-side risks remain: semiconductor bottlenecks, GPU replacement cycles, and the still-developing secondary market for AI hardware capacity. The next investment cycle will likely be defined less by model launches than by utilization rates, monetization efficiency, and capital discipline – and companies that convert growing AI usage into durable cash flows are best positioned to command premium valuations.