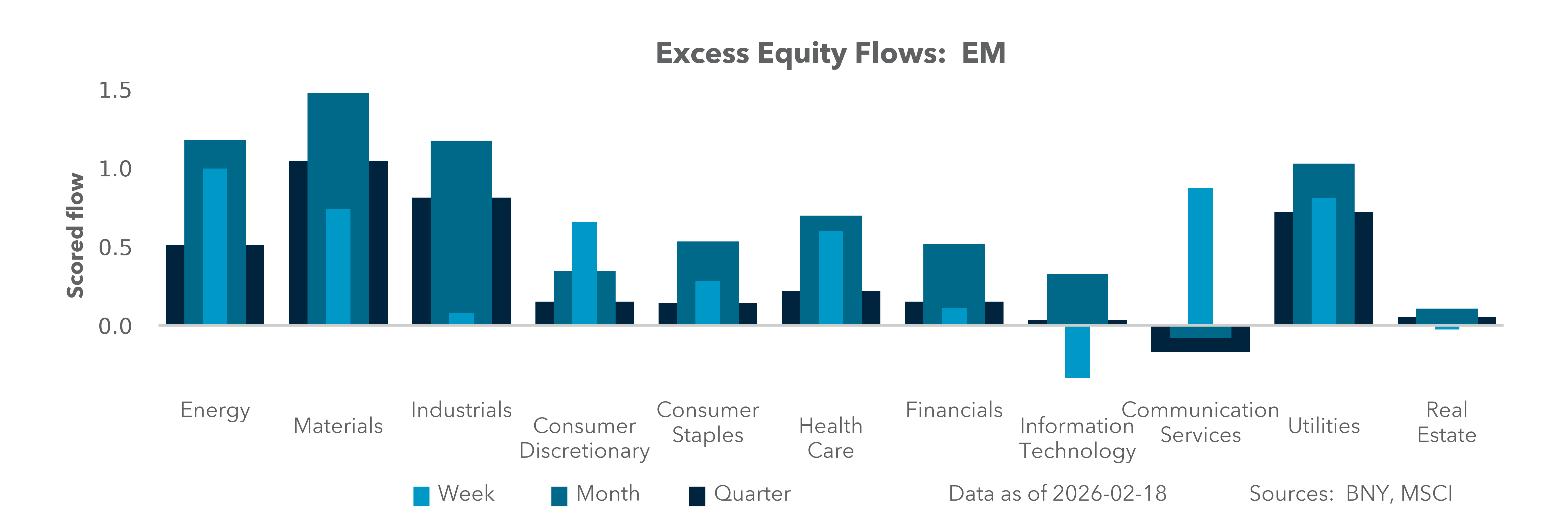

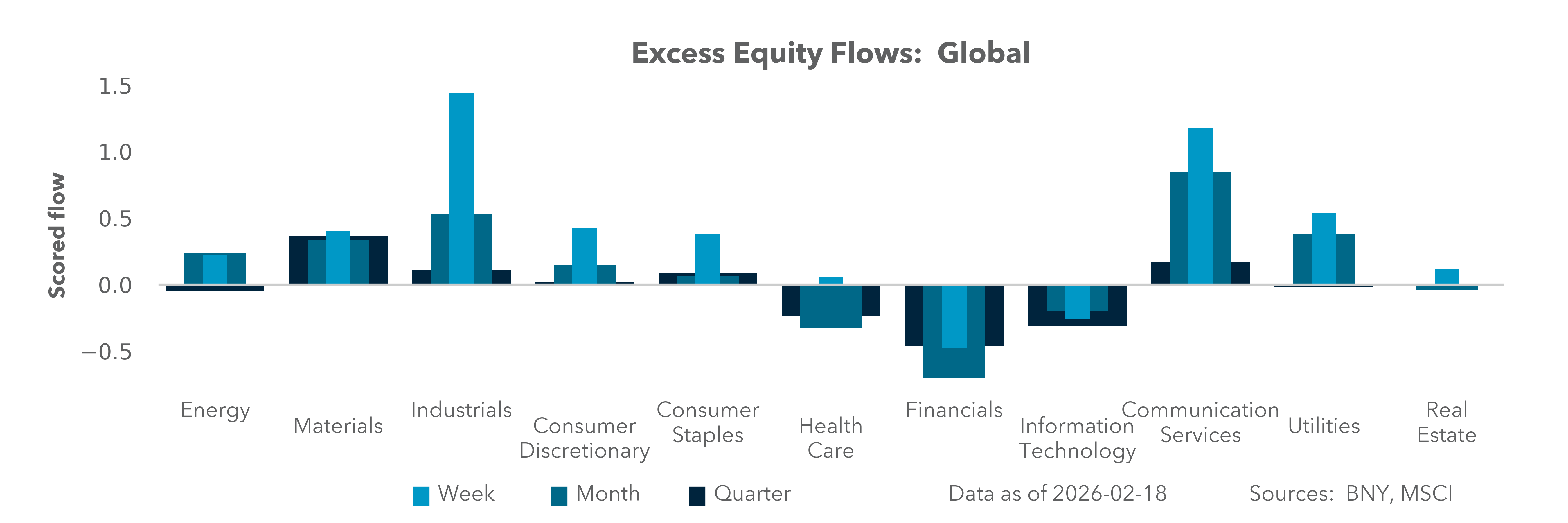

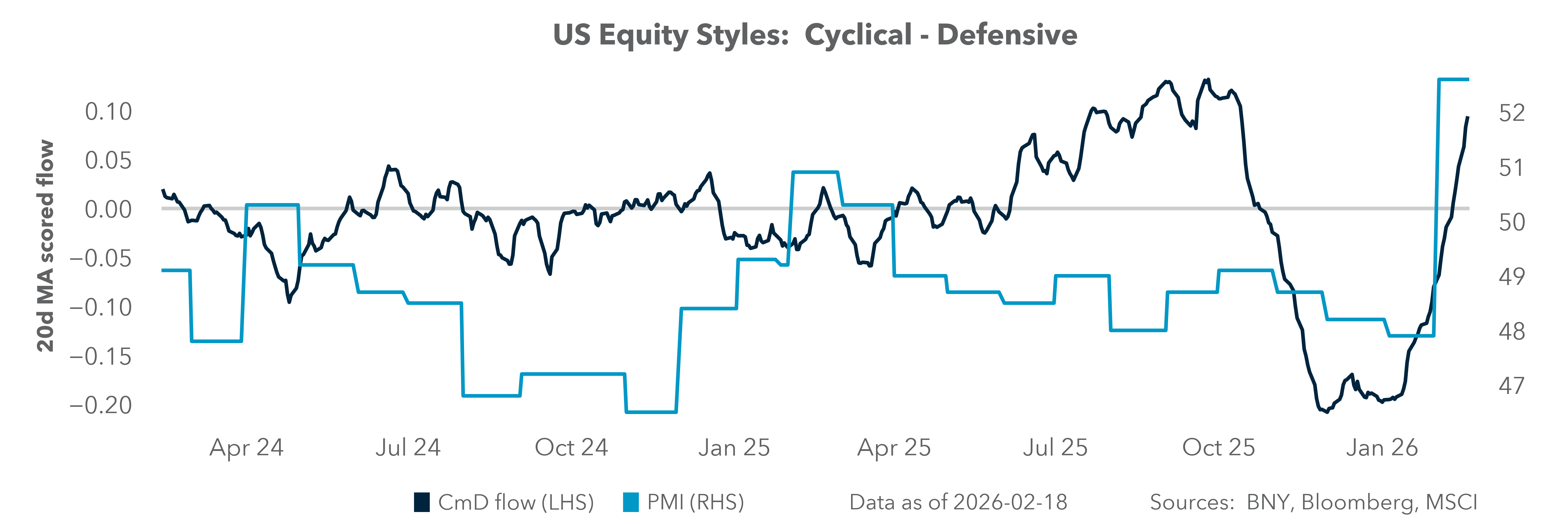

Follow the money

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 6 minutes

The ongoing bull and bear debate about equities in 2026 starts with AI and the $1tn in capex by large tech companies. Expectations are that Nvidia earnings will be the final word on returns and value, after a significant spate of volatility across global shares in February. The role of interest rates in setting the bar for returns has been key for equity valuations, and the drop in U.S. 10y yields from 4.31% to 4.01% in the last two weeks has created a circular reaction to equity moves lower. Much of the rate move has been linked to Fed Chair Nominee Kevin Warsh, who described AI as the “most productivity‑enhancing wave of our lifetimes” that would prove “structurally disinflationary,” like the expansion of the internet.

Generative AI and its effect on the U.S. labor market remain a key concern for investors and policy makers. AI investments and the wealth of the top 10% of the population drove U.S. growth in 2025 and likely will do the same in 2026. The K-shaped economy worries investors globally. The rise in asset prices has supported demand at the high-end, while the rest of the U.S. economy worries about affordability. February brought doubts about AI as a great equalizer and instead shifted concerns toward it being a killer competitor. This narrative changed again this week as investors look for value.

FOMC speeches about AI are important to consider here, as the role of policy in setting risk-free rates drives some of the bounce-back in technology shares this week.

The must-read Fed speech came from Governor Michael Barr. Here is the key point for the optimism of the moment: “Although new technologies often create winners and losers in the short run, history shows that in the longer run, innovation leads to broadly shared increases in productivity and living standards that tend to support economic growth and a healthy labor market.”

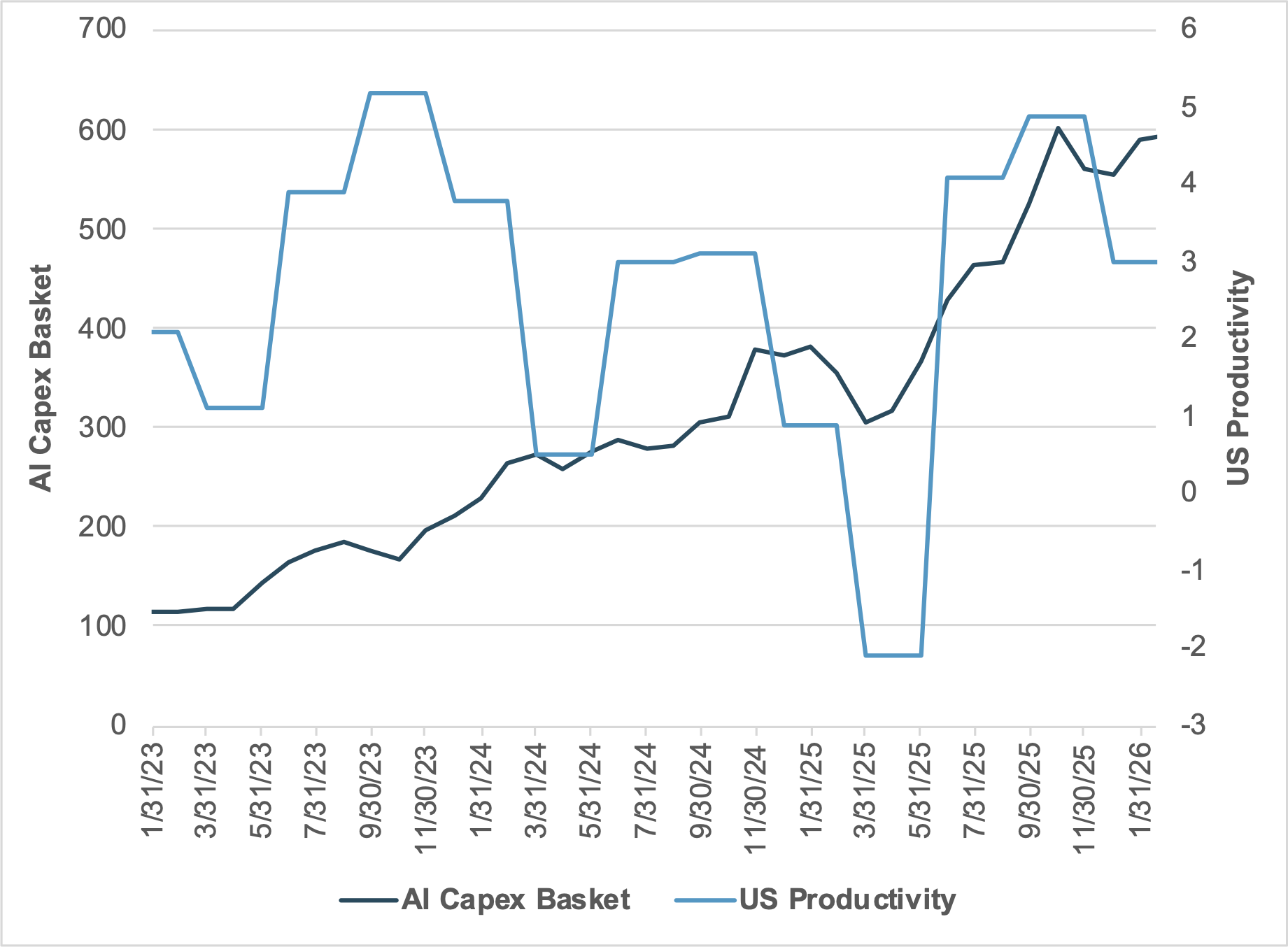

EXHIBIT #1: U.S. AI CAPEX BASKET VS. PRODUCTIVITY

Source: BNY, Bloomberg

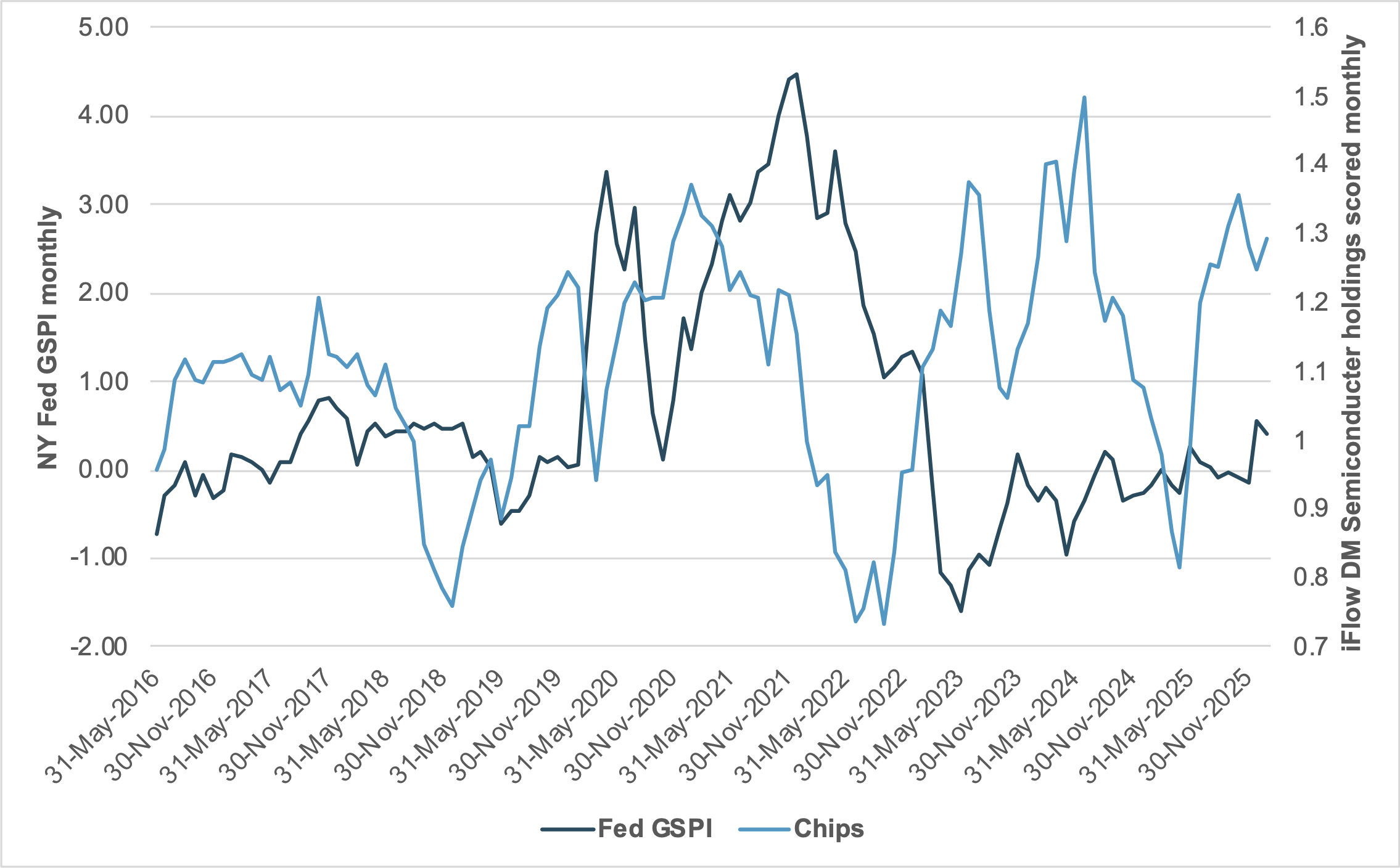

EXHIBIT #2: FED GLOBAL SUPPLY CHAIN INDEX VS. IFLOW CHIP HOLDINGS

Source: BNY, Federal Reserve Bank of New York

Our take

The U.S. productivity boom since COVID has been notable. Fear of missing out among hyperscalers with a winner-take-all mindset has driven investment into AI, with capex expected to double to $1tn in 2026. The link between AI investments and productivity is a bit more complicated.

AI investments have not slowed, while the notable drop in productivity into Q1 2026 is more about GDP growth. The slowdown last year was linked to policy uncertainty, trade drag from large imports ahead of tariffs, and Fed policy shifting from easing to holding. Current deregulation, shifts in tax code promoting immediate depreciation, and the investment push from the Trump administration are driving 2026 expectations.

Forward look

It is too early to argue that AI is driving U.S. productivity improvements. On the edges, most companies see some individual worker adaptation helping move work from mundane tasks to higher level decisions. Performance and output are not yet fully measurable. As such, any “deflation” fear from AI is more about 2027 and beyond. The implications for AI valuation are primarily linked to rapid investment into data centers driving up semiconductor, energy and land prices. That inflationary impact, mixed with longer-term fears about labor demand weakness, leaves investors watching for more clarity on the physical limitations to growth ahead.

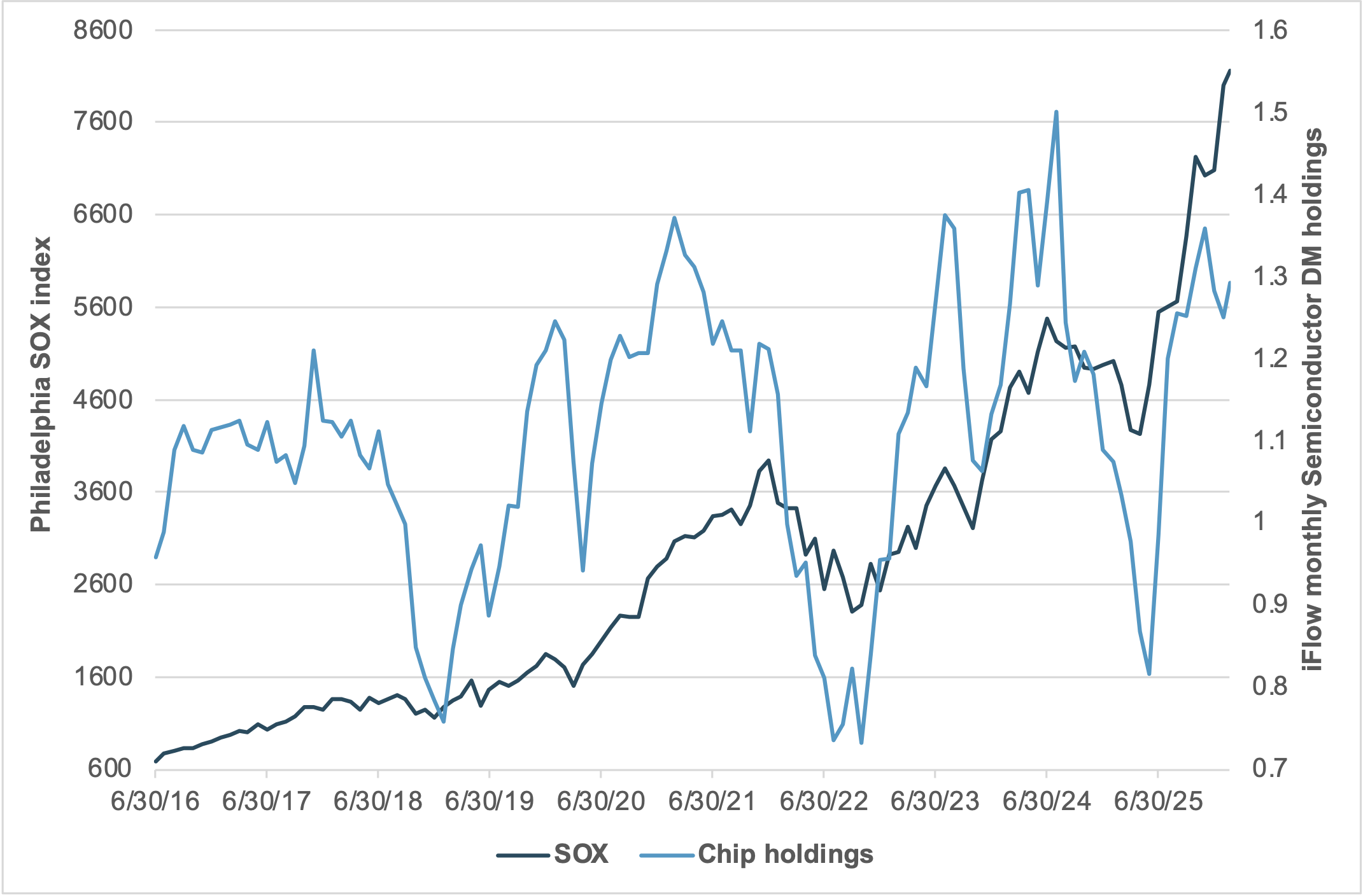

EXHIBIT #3: IFLOW HOLDINGS OF DM SEMICONDUCTORS VS. SOX

Source: BNY, Bloomberg

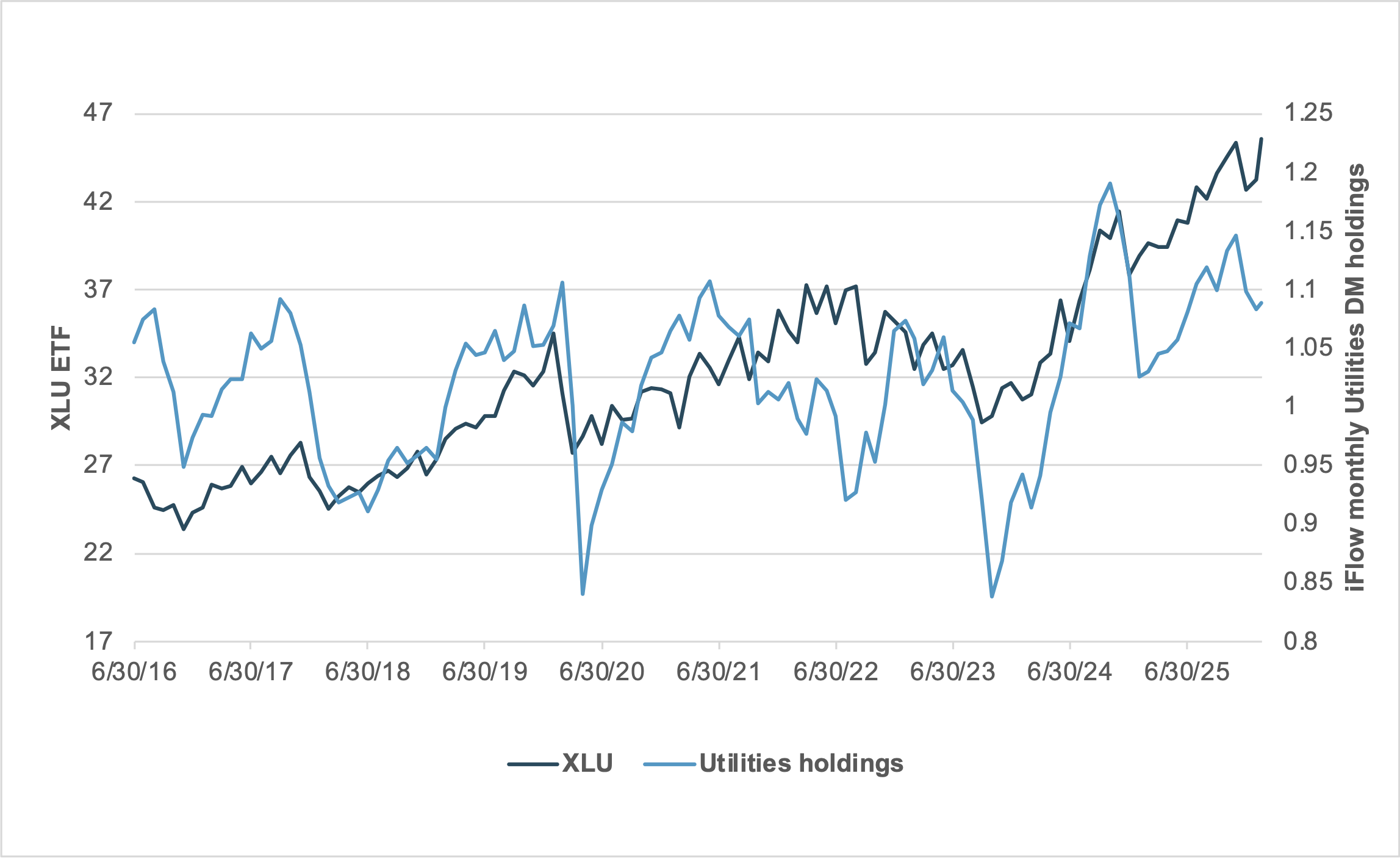

EXHIBIT #4: IFLOW HOLDINGS OF DM UTILITIES VS. XLU

Source: BNY, Bloomberg

Our take

The business cycle for chips and utility companies is reflected in their stock prices, and client holdings show the same pattern. The divergence between price and holdings over the last three months suggests something has changed.

The shift in utilities stands out, as investors watch political pressures on data centers to be independent of the public electrical grids. Rising demand for fixed income as a safe-haven and hedge to equity risks is also supporting utility shares, as they have steady cash flows similar to bond coupons.

However, investors are not chasing utility returns as they clearly see a dangerous correlation between big tech holdings (where positions remain over average) and utilities.

Forward look

The link between semiconductor prices and holdings is also diverging, but not as dramatically. Nvidia’s AI-specialized chips are part of this story, and this will become clearer during its Q4 earnings call on February 25. Markets expect another banner quarter for profits and robust outlooks, but the key will be where demand is and how much competition there is from other chipmakers.

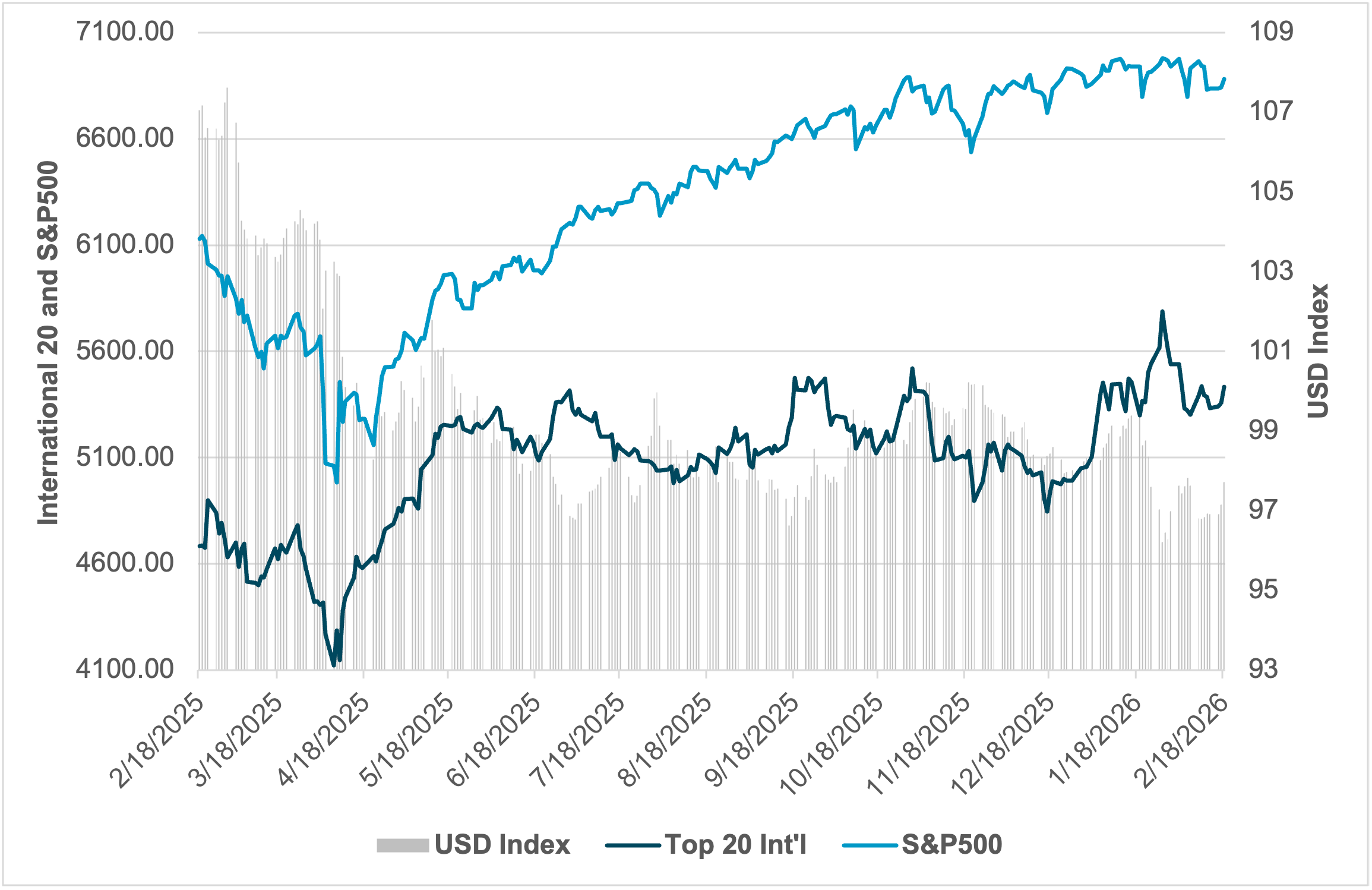

EXHIBIT #5: INTERNATIONAL TOP 20 MARKET CAP VS. S&P 500 AND USD INDEX

Source: BNY, Bloomberg

Market support for technology rests on whether revenue growth and operating leverage stabilize returns, and that path remains robust. Investor tolerance to any surprises from physical supply shocks – trade in chips, energy or materials – is limited. USD returns are also a significant factor for how investors see technology investments. U.S. hyperscalers continue to face hurdles abroad from regulations and new competitors. Home bias and the policy volatility add to concerns.

Our take

The last year saw a notable USD decline, but its rally in November and December mattered significantly to the performance of international shares. The selling in 2026 has lifted international shares back up, and their performance again beats the concentrated Magnificent 7 and the broader S&P 500. Year to date, the top 20 largest market-cap international basket has gained 7.55% compared with 0.5% for the S&P 500. The USD plays a role in returns, but it has lost just 0.5% year to date.

AI as a driver of the basket stands out, with Chinese tech, large energy and commodity companies, and APAC chipmakers all part of the composition.

Forward look

The growth and diversification of international companies will be a key driver for reallocation pressures in the coming week and month. Earnings from the S&P 500 have been strong in Q4, but the outlook for Q1 is downbeat, and there are ongoing doubts about Fed rate policy and the durability of the current U.S. soft landing.

As for EMEA, the Euro Stoxx 600 has underperformed in Q4 with 1% EPS blended – dragged down by materials and energy costs, along with worries about heavy concentration risks in defense and banks. This is shifting in Q1, as outlooks are robust, up 5% to 8% EPS.

APAC has seen solid AI-linked returns for South Korea and Taiwan, but China has been actively curtailing the exuberance risks in technology in its equity market. Outlooks for Q1 will link to China GDP targets and semiconductor prices. The Japanese election, stimulus from Takaichi’s new budget, and confidence from her landslide victory will be important as well.

The biggest risk for investors is in correlations. The link of AI investments in driving international returns matters to global financial conditions and policy responses.

Should investors continue to sell U.S. big tech companies, it could weigh on all stocks, forcing CEOs to slow spending, which could then weigh on GDP both in the U.S. and abroad. The convergence of risks and correlations dominates the wall of worry in 2026.

Looking ahead, the AI capex cycle is unlikely to resolve into a simple boom-or-bust outcome. For equity investors, the key variable is not the absolute level of spending but whether incremental investment translates into sustainable revenue growth, operating leverage and durable productivity gains. Physical constraints – chips, energy, grid capacity, and land – will shape the pace of deployment and introduce episodic volatility, particularly as policy and trade dynamics evolve. Valuation support will depend on evidence that hyperscaler spending is expanding end-demand rather than merely reinforcing competitive moats. International earnings momentum, USD direction and central bank policy will further influence cross-asset correlations. If AI investment broadens beyond a concentrated ecosystem and begins to lift aggregate productivity, the current skepticism may prove cyclical rather than structural. Until then, markets will trade on proof points – margins, order books and cash discipline – rather than narratives.