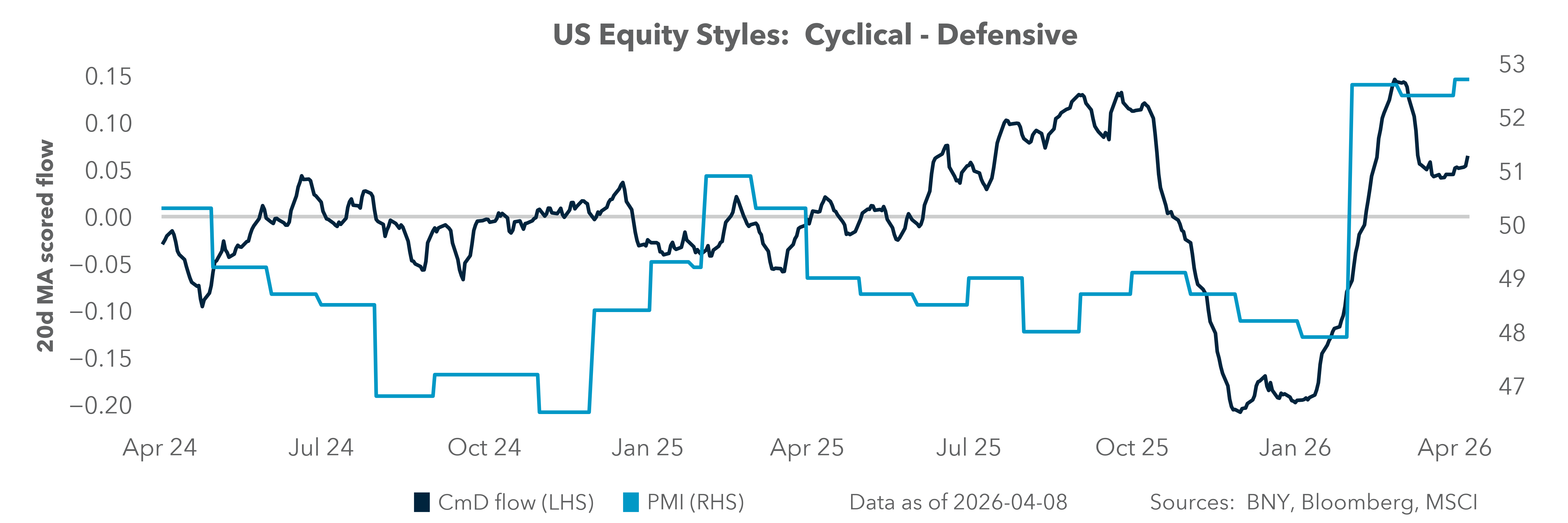

Earnings season outlook shifts

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

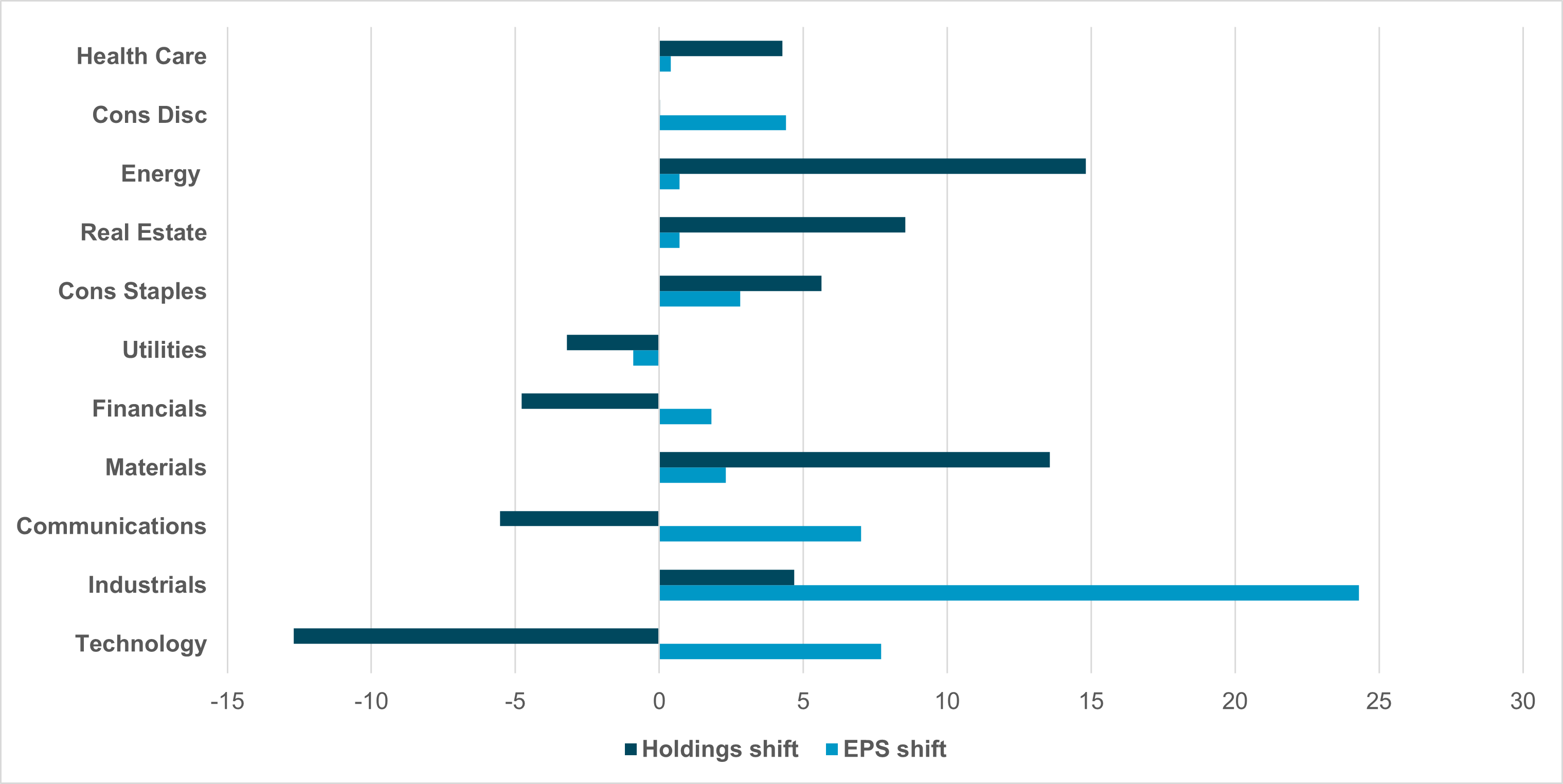

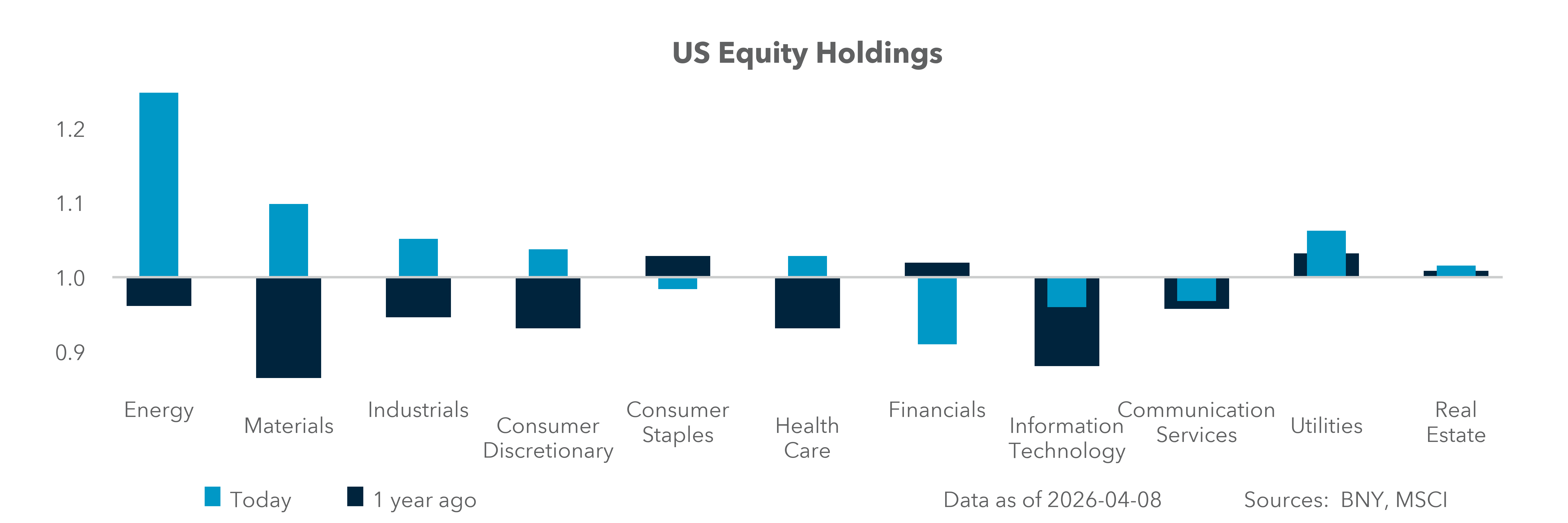

EXHIBIT #1: EARNINGS EXPECTATIONS VS. U.S. EQUITY HOLDINGS – CHANGE IN Q1

Source: BNY, FactSet

Q1 reporting will focus more on outlooks than results. The consensus earnings growth is 13%, but the forecast, varying from 9% to 19%, is wide. Early corporate guidance has also been notable, with 59 companies issuing positive guidance – the most since 2022. Revisions to earnings growth expectations are up 0.4% since December 31. Revenue growth is also expected to increase 0.4% q/q, 9.2% y/y, as profit margins are forecast up 9.7% y/y, led by Technology at 27.5%, Communications at 12.5%, and Financials at 10%, while Health Care is expected to improve significantly, from -4.4% to +6%.

Key drivers for Q1 expansion are 1) AI monetization, as technology hype translates into cost savings and efficiency; 2) positive operating leverage, which will be watched given expectations for stronger revenue growth outstripping costs; and 3) tax relief from the One Big Beautiful Bill Act (OBBBA), with $200bn expected to be reflected in Q1 earnings.

Q1 negatives will be wrapped around supply-chain and energy shocks from March, along with USD gains. While 60% of the S&P 500 is domestically focused, the sectors most vulnerable to dollar moves are IT, Materials, and Communications.

Our take

Three notable divergent moves in holdings relative to earnings expectations will be key to how investors react to EPS beats. iFlow data show that Technology, Communications Services and Financials have all seen a significant shift down in holdings – a rotation that began before the Middle East conflict and was clearly part of the broader 2026 shift away from dominant growth themes. Energy’s rise has been linked more directly to the war and may prove most sensitive to any resolution or further disruption around the Strait of Hormuz. Real Estate, Materials and Health Care look more dependent on underlying earnings.

Forward look

The decline in IT and Communications Services holdings reflects price moves since October among the big tech companies dominating the S&P 500. The S&P 500’s 12m-forward P/E has dropped to 19.8 from 22 since January 1, a notable compression given the index is down just 0.6% on the year. The trailing 12m P/E of 26.2 may be the more instructive reference. Investors could rotate from value to growth, with beats rewarded more asymmetrically than misses in the weeks ahead.

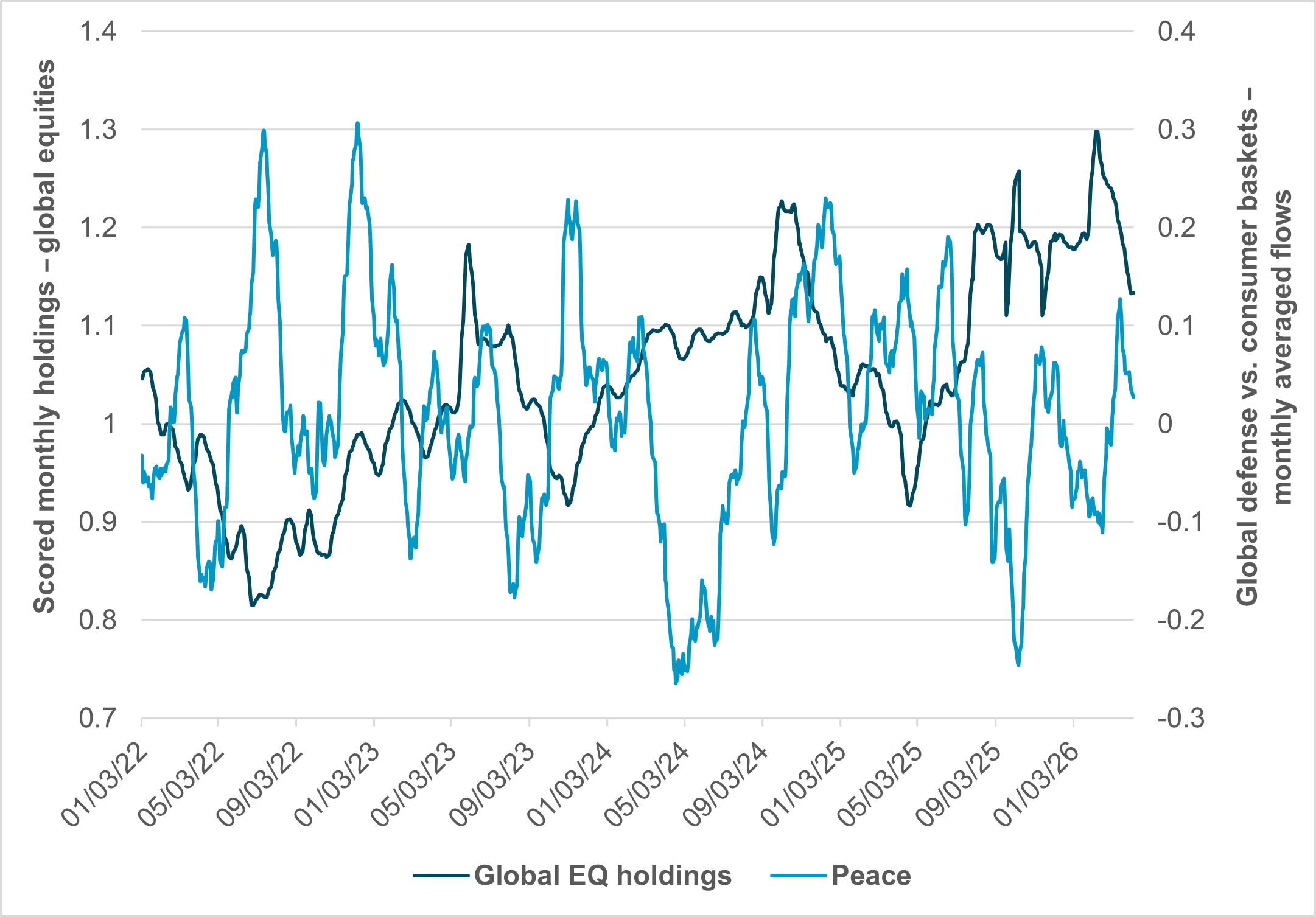

EXHIBIT #2: IFLOW EQUITY “PEACE” FLOWS AGAINST OVERALL GLOBAL HOLDINGS

Source: BNY

Our take

The war with Iran did not send investors into defense shares as much as into energy stocks. In fact, the selling of Financials, Consumer Discretionary and IT stands out in the quarter more than much else. The lesson for investors has been to remain nimble, given significant volatility and ongoing uncertainty about the conflict’s duration and damage to global supply chains. Notably, safe havens in energy and materials outstripped defense stocks – a preference that flow history confirms: a global basket of defense and aerospace sectors versus Consumer Staples suggests positioning is driven more by margins than by expectations of new demand.

Forward look

Looking at the early days of the Russia-Ukraine conflict in 2022, the lessons about any peace index start with expectations around conflict duration – our flows did not turn toward defense stocks until three months in, and even then, broader concerns about equities mattered more than any rotation trade. Investors in Q2 will be watching for energy and other supply-chain shocks, but also for AI rotation trades, with helium and energy supply pressure on semiconductor prices as consequential as any geopolitical speculation.

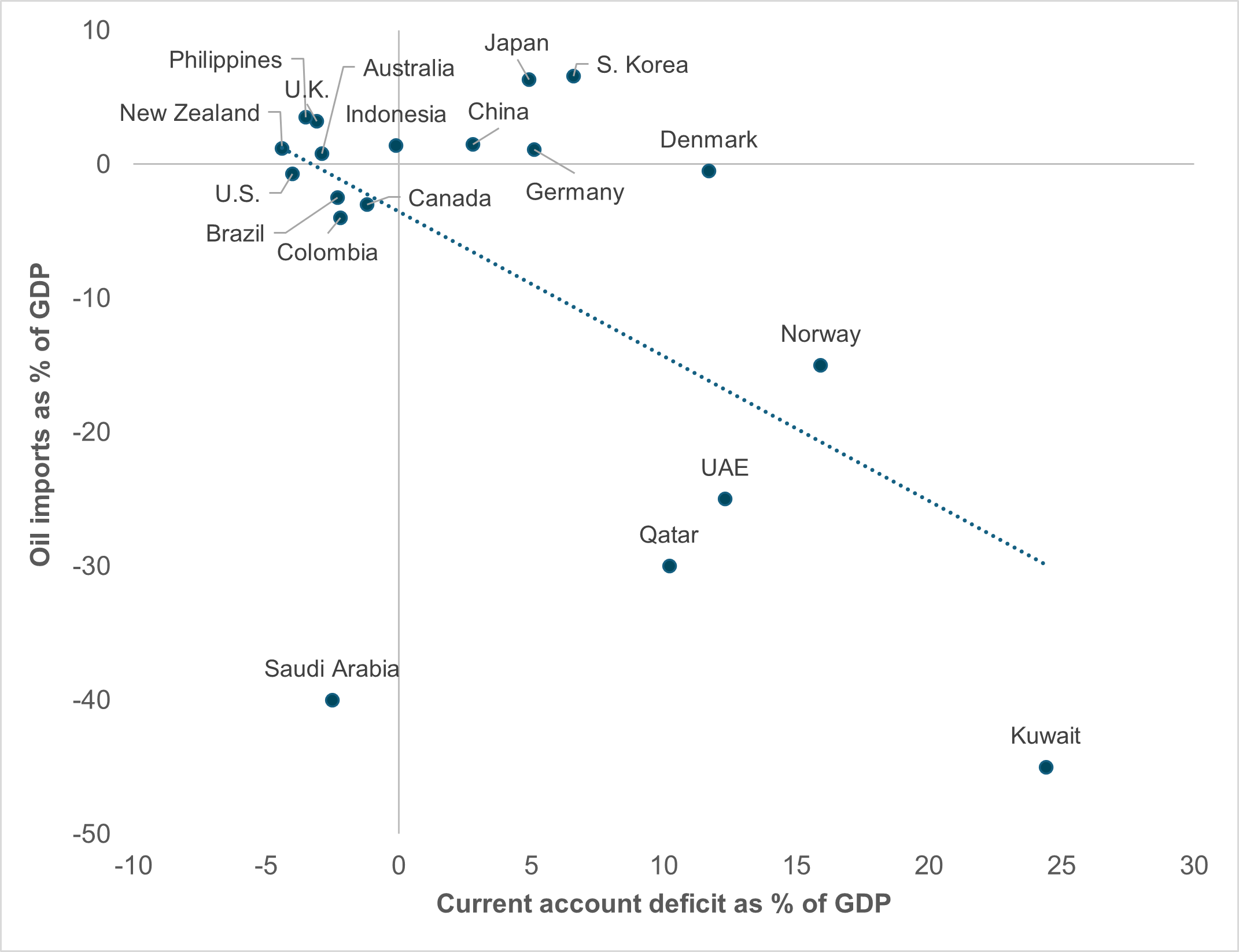

EXHIBIT #3: OIL AND CURRENT ACCOUNTS BY COUNTRY

Source: BNY, Bloomberg

Our take

Oil exporters in the GCC have seen oil prices rise but exports drop with the closure of the Strait of Hormuz. The March shortfall in global oil output is estimated at 8mbd – 8% less than needed – leaving pricing high and the second-order effects of petrochemical prices and fuels worrisome. Q1 earnings and Q2 outlooks for global companies will hinge on exposure to this supply-chain shock and how the resulting inflation will be absorbed or passed through – a dynamic that interest rate moves will complicate further. Nations that are both import-dependent and reliant on foreign capital are most exposed heading into Q2, with asset markets likely to reflect both growth and inflation pressures. The U.K. and the Philippines are standout examples. For U.S. companies, revenue exposure to nations above the trend line will be watched closely.

Forward look

Nations that need to offset the cost of oil imports – like Japan, South Korea, China and Germany – have surpluses to cushion some of the drag on growth, but this will require either new fiscal commitments and borrowing or selling out of some assets. Either way, rate markets will be a key factor in interpreting Q1 earnings and Q2 outlooks. Stock holdings by cross-border investors in the U.S. show much the same rotation pressures as we saw in Exhibit #1, but there are two sectors that stand out in new holdings: Consumer Staples and Energy. Cross-border holdings in Q1 Energy jumped 22%, while Consumer Staples rose 10%. Investors are clearly looking at risk through more than just an earnings lens as they forecast growth slowdowns and search for safe cash flows ahead.

The earnings season is likely to be defined less by reported results and more by forward guidance, particularly as macro uncertainty and sector rotations intensify. Equity markets appear increasingly sensitive to outlook revisions, with asymmetric reactions favoring companies that can demonstrate durable growth amid volatility. AI-driven efficiency gains and margin expansion remain key structural tailwinds, supporting an equity-biased stance, particularly in sectors with strong operating leverage. However, rising energy costs, supply chain disruptions, and interest rate pressures introduce crosscurrents that could challenge earnings durability into Q2. Portfolio positioning suggests investors are already hedging through increased exposure to energy and defensive cash flow sectors, while reducing allocations to prior market leaders. For equity investors, the opportunity lies in selectively adding to high-quality growth franchises on weakness, while maintaining exposure to sectors benefiting from inflation pass-through and geopolitical tailwinds. Active management and sector rotation will remain critical in navigating this evolving landscape.