Balancing growth, inflation and risk-free rates

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

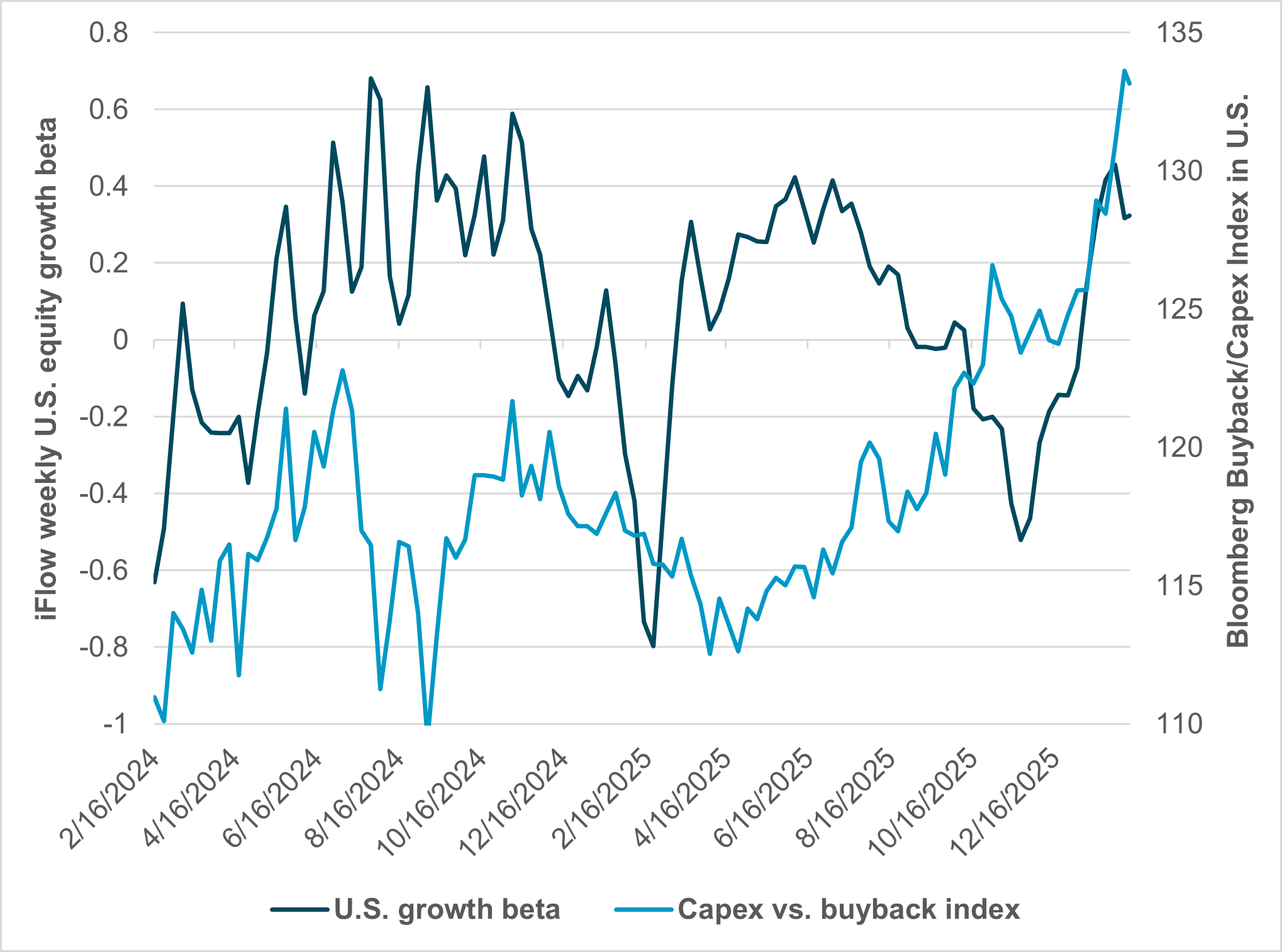

The relationship between debt issuance and stock performance has shifted in 2026. The low-rate regimes from 2010 to 2019 led to significant debt issuance and share buybacks, while R&D was notable in only some sectors, led by pharma and tech. Even in 2025, share buybacks accounted for 70% of spending, with R&D about 17%. Unlike previous cycles when debt was often used for “financial engineering” (buybacks), the 2026 issuance surge (estimated to be up 30%) is heavily linked to tangible growth investments in AI infrastructure. Some of this reflects the tax changes from 2025, while much of it reflects the faith in new technology driving productivity and future earnings. Capex only adds to value when it drives incremental returns above the cost of capital. Debt issuance in 2025 by big tech hyperscalers reached $165bn and is on target to more than double to $400bn in 2026.

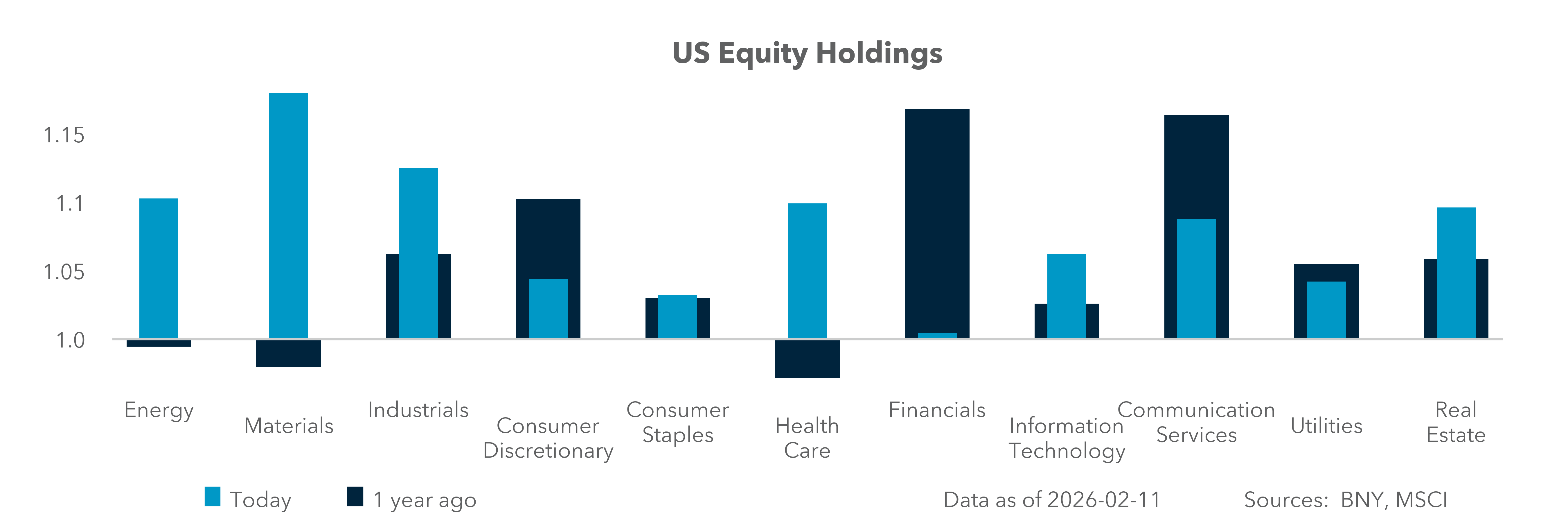

EXHIBIT #1: U.S. BUYBACK AND CAPEX INDEX RELATIVE TO IFLOW GROWTH BETA

Source: BNY, Bloomberg

Our take

Investors are leaning into growth in 2026, and hyperscalers are directing capex toward that demand. The balance of investment flows supporting growth beta is positive, but U.S. data appear to have peaked after the sharp spike in January economic data surprises. The preference for capex over buybacks reflects another factor, as investors are seeing a sector rotation out of tech toward materials and industrials and a broadening of U.S. earnings as a positive. Q4 earnings wind down after this week, but the issuance of new debt and more buybacks usually follow.

Forward look

There is a clear risk that investors will require growth evidence to support ongoing capex investments. How rates handle higher growth without expectations for more inflation will be a critical factor in the balancing act for pricing risk. The flow of money into capex rather than buybacks affects U.S. valuation and momentum, and those factors have been struggling. Rotation trades across U.S. sectors may be the next question to consider, with small caps winning out over tech mega-cap companies.

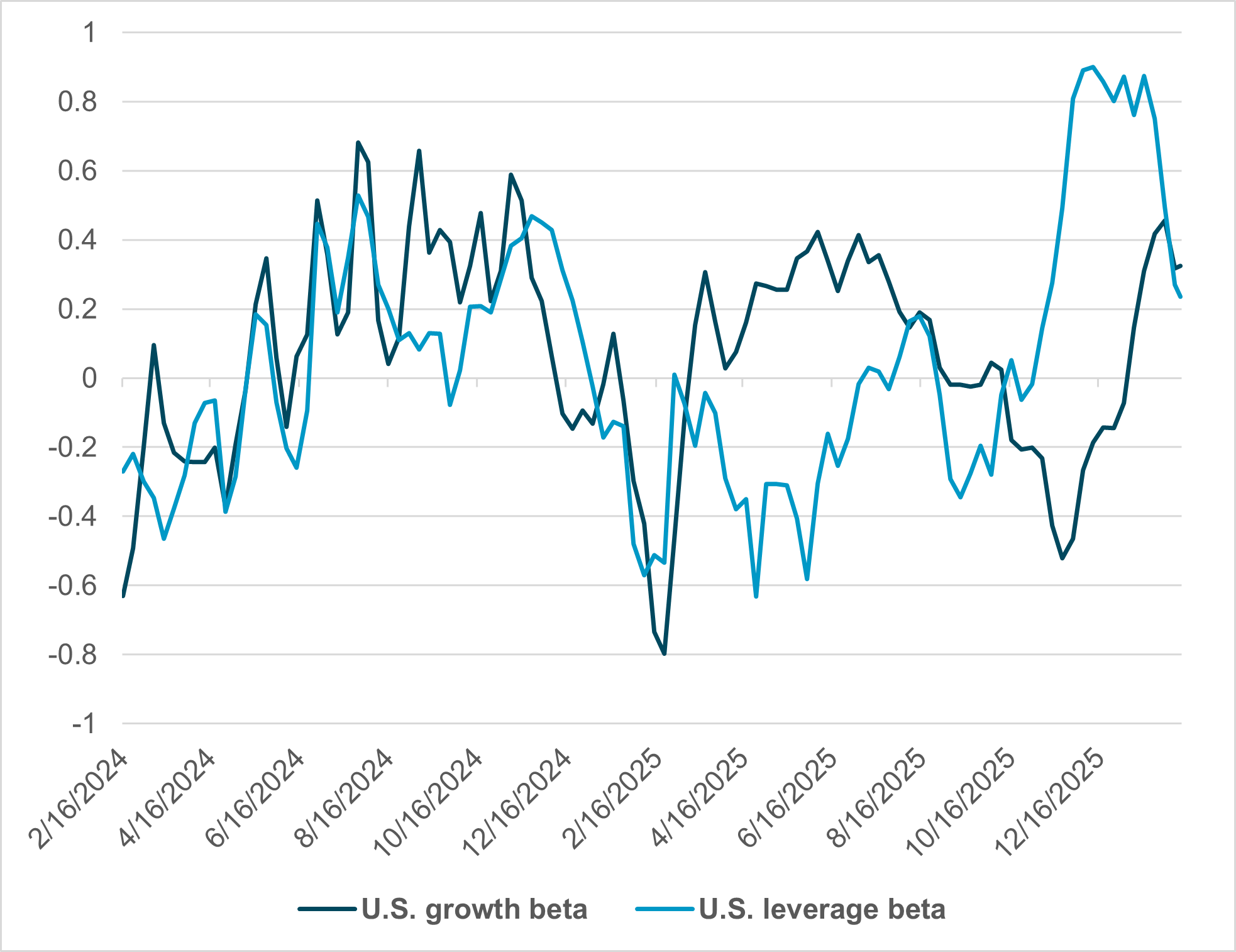

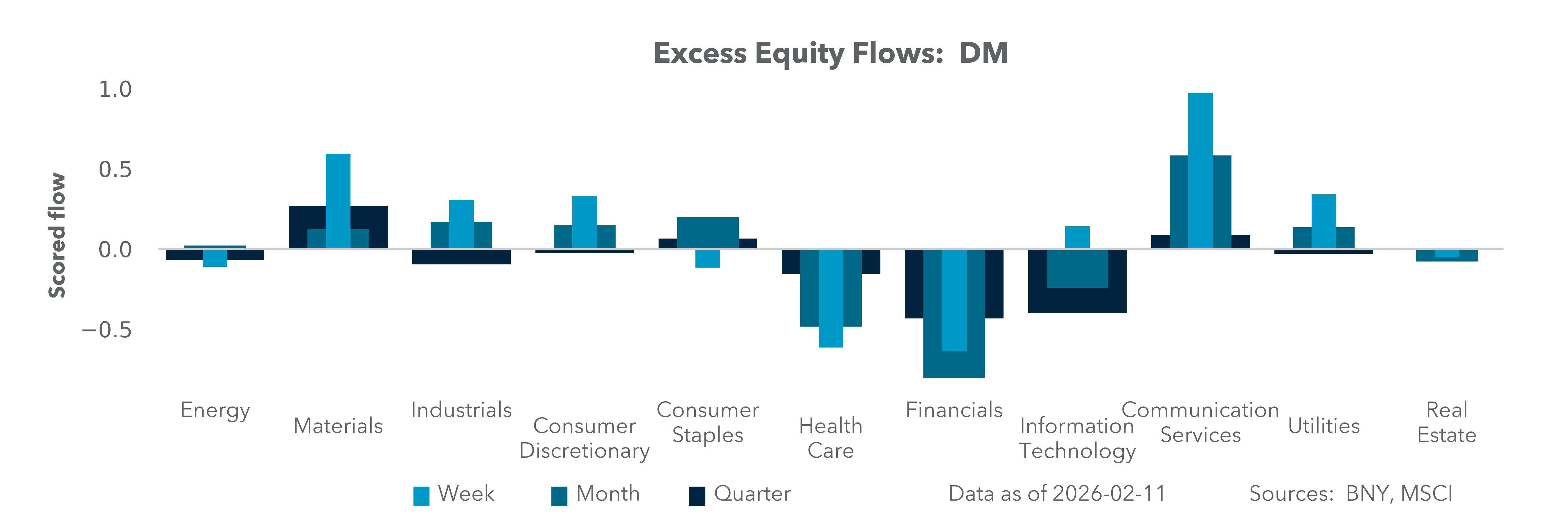

EXHIBIT #2: U.S. EQUITY BETA SHOWS GROWTH MOMENTUM STRONGER THAN LEVERAGE

Source: BNY, Bloomberg

Our take

The role of Fed rate cuts on U.S. equity markets stands out in our rising leverage beta from September to today. Growth in response to easing and the return of U.S. economic data followed in late November. Whether growth can continue to rise depends on better data. Economic surprises and Q4 earnings beats are no longer sufficient to maintain buying momentum.

Forward look

The peak in our equity leverage factor reflects growing doubts about the pace and size of future FOMC rate moves. Investors are unlikely to reward hyperscalers for their capex or other sectors using buybacks to support their shares. Markets price in two rate cuts but will be watching economic growth to keep the balancing act intact. The risk of lower growth and higher inflation drives investors to rethink safety and value models.

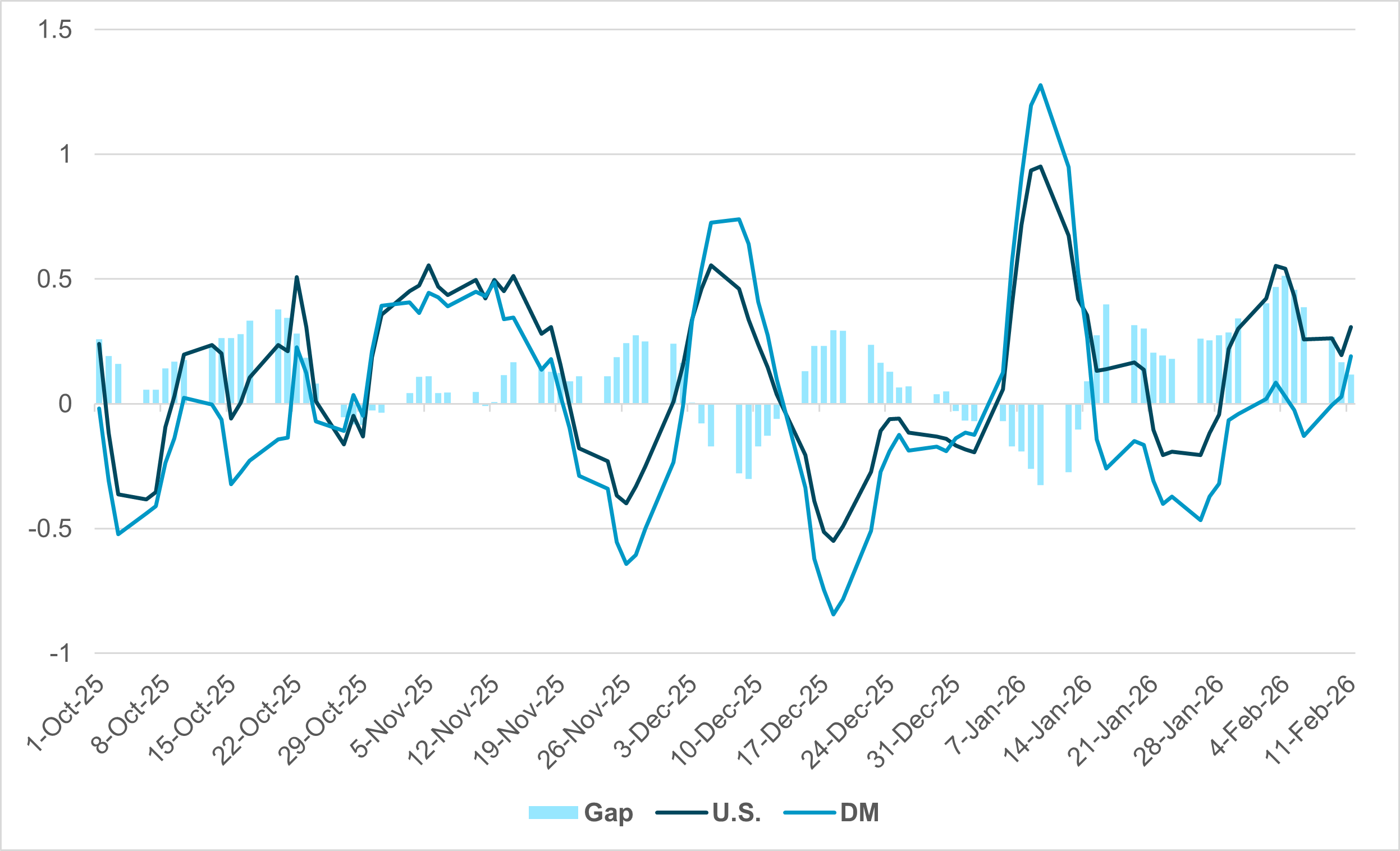

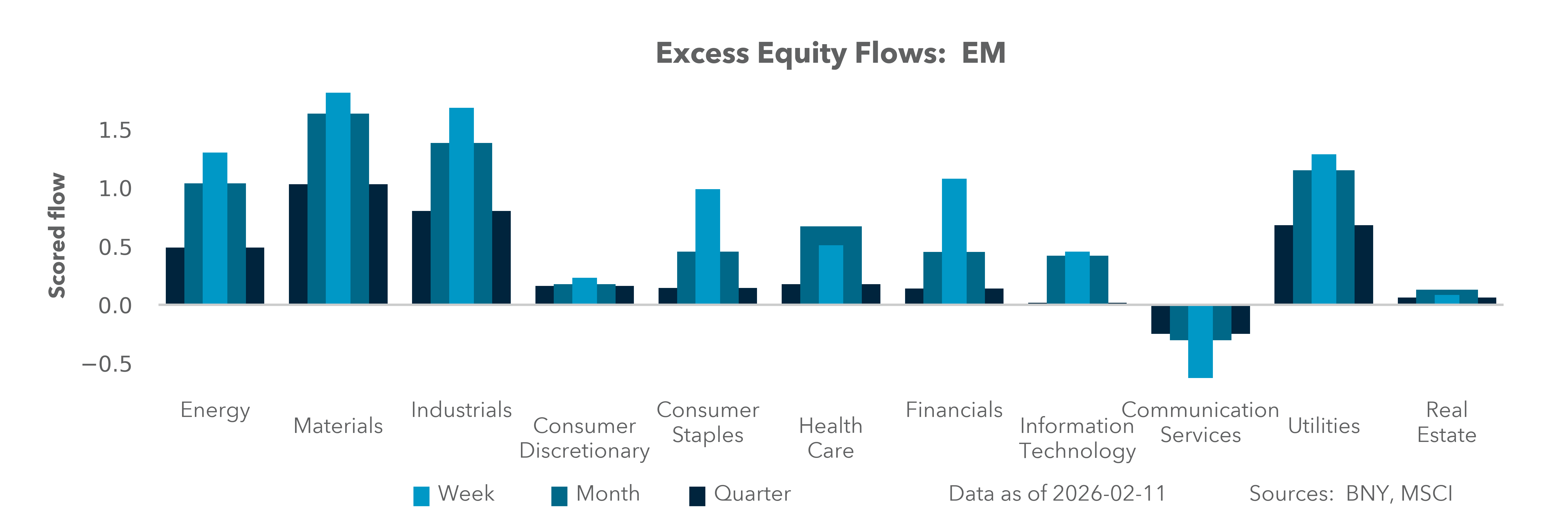

EXHIBIT #3: FLOWS INTO U.S. CREDIT STARTING TO OUTPACE REST OF THE WORLD

Source: BNY

Our take

Strong demand for issuance by U.S. tech companies has alleviated fears of material credit tightening, particularly as investors remain confident that affected companies can generate enough cash flow to service the debt. Alphabet led the focus last week with $32bn in debt, including a surprise 100-year GBP bond – an unprecedented issuance level. While we see a risk that other forms of borrowing will be crowded out, there is clear ongoing interest among asset allocators in adding exposure to U.S. credit, especially relative to peers in developed markets.

Forward look

Throughout much of the current economic cycle, credit’s global performance has been weak amid persistently elevated real and nominal government bond yields. Into the first half of 2025, however, global demand began to pick up as developed markets’ benchmark rates fell, signaling a more prolonged easing cycle. While cuts have not been as aggressive as previously expected, the direction of travel is clear. This is particularly true for the U.S., which helps support the credit market, especially if inflation is expected to run relatively “hot” and bring real yields for corporate borrowers down further. In contrast, real yields may stay elevated in other developed markets, which is affecting corporate credit performance: The gap between U.S. and developed-market issuers globally is the widest in several months. It will likely widen further if secondary demand for new tech-based issues remains resilient.

Looking ahead, the central question for equity investors is whether today’s surge in capex can translate into durable earnings growth sufficient to justify higher leverage and stretched valuations. Unlike prior cycles dominated by buybacks, 2026 places capital discipline under sharper scrutiny, as hyperscalers deploy unprecedented, longer-dated debt into AI infrastructure with uncertain payoffs. Markets are signaling conditional support: Credit flows remain robust and rates are easing at the margin, but equity momentum is no longer automatic.

With economic surprises fading and earnings season nearing completion, investors are likely to rotate toward sectors where capex generates visible cash-flow inflection not narrative-driven optionality. Rate expectations will be pivotal – growth must strengthen without reigniting inflation to preserve the current balance between risk appetite and valuation tolerance. If that balance falters, leadership may continue to broaden away from mega-cap tech toward cyclicals, small caps, and real-economy beneficiaries, reinforcing dispersion and rewarding selectivity over beta.