Coming into 2025, the United States economy and global markets were strong with solid labor markets, easing inflation and a stock market boom fueling consumer spending. So far this year, markets have shown continuous change across the global landscape with shifting policy, tariff expectations and international relations driving higher volatility across asset classes. Stock performance in the first quarter was weak for both passive and active investors. U.S. equity markets sold off significantly against bounce backs in Europe and Asia. Positions flipped from short to long EU shares, while U.S. longs flipped to short holdings. Rate cut expectations for the Federal Open Market Committee (FOMC) bounced around during the first half of 2025, with calls for no cuts to more than six. Additional noise from persistent structural deficits and lack of fiscal reform led to the U.S. downgrade from Moody’s (the last of the three agency downgrades), though market reaction was muted. Many investors are questioning the U.S. exceptionalism mantra that characterized markets for over a decade.

Consumer and business sentiment data remain weak, but have yet to reflect recent trade developments. The University of Michigan’s consumer sentiment index is near historical lows1 and small business optimism2 has weakened to its lowest since last October. Investor sentiment dropped to near the weakest in history after the initial tariff announcement on April 2, but has since improved to levels before the trade escalation. CEO confidence fell sharply for several months from the post-election high in January, but was unchanged in April, suggesting the downturn has likely stabilized.3 Overall, while sentiment was impacted by higher policy uncertainty, markets are pricing in a stabilization and sentiment improvement — the extent of which will depend on continued policy clarity and a focus on tax cuts and deregulation.

Our Take

The effective tariff rate has potentially settled to ~13%, which our experts think could represent the target terminal tariff rate of the U.S. administration. The U.S. Court of International Trade (USCIT) ruling last week has created additional uncertainty around final tariff rates, but may not ultimately change the course of tariffs given the alternative pathways to increase trade duties. Still, tariffs remain higher than anticipated and continue to be a drag on economic outlook. U.S. growth is seen as materially slowing from 2024 levels to ~1%, and inflation is expected to pick up to ~3.5%. Additionally, the sustainability of U.S.-China sanctions represents a concern for global growth and inflation, with iFlow data indicating outflows from both economies since January as investors seek alternatives. Market recovery hinges on the speed of potential U.S. tariff deals, with the current 90-day pause in 25% average tariffs providing only temporary relief.

Equities

Given the impact on confidence and freezing of investment plans, our experts' base case remains a non-recessionary slowdown with weak 2025 real GDP growth. Our latest estimate is a 25% chance of recession risk, down from 40% before the China tariff rollbacks. The promise of upcoming trade deals has driven an equity rally from the year-to-date low. Our experts anticipate 2025 earnings to hold up, particularly after a remarkably strong first-quarter earnings season, ending the year with 9% growth. Earnings expectations for 2026 are likely to stabilize with clearer tariff rates and can support S&P 500® Index (S&P 500) levels of $6,100-$6,400 in the next 6 to 12 months.

Lingering risks, including government debt and higher rates, could lead to a renewed pick up in volatility depending on policy developments. While the U.S. has generally underperformed other markets year-to-date (lagging the most since 2017), our experts believe U.S. strategic outperformance will resume.

Rates and U.S. Bonds

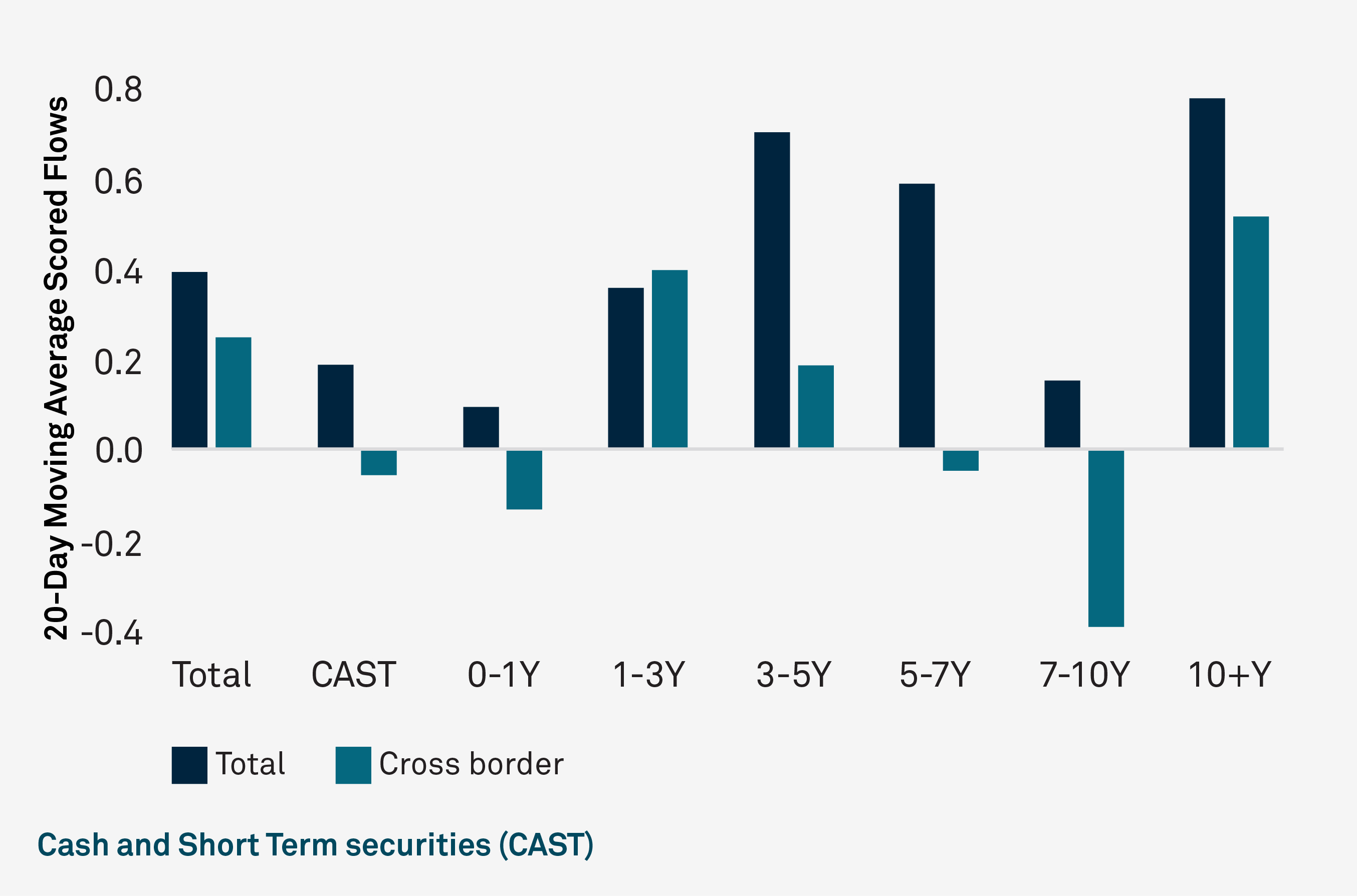

The recent run-up in bond yields and U.S. dollar (USD) weakness from mid-April to mid-May indicate a significant shift in safe-haven perceptions, with U.S. assets no longer commanding their traditional haven status during risk-off environments. BNY’s iFlow data shows foreign investors are reducing exposure to U.S. assets and the dollar, redirecting capital flows toward Eurozone and Japanese government bonds. Post-Liberation Day selling has affected U.S. Treasuries across maturities, alongside broader fixed-income products (Figure 1). Despite financial press speculation, fears of a U.S. Treasury basis trade unwind appear misplaced, as our securities lending data shows this hedge fund strategy remains robust. While U.S. Treasury liquidity faced challenges in early April, trading desk metrics confirm conditions have since recovered. Central bank policy remains on hold, with the Federal Reserve discouraging the idea of a "Powell put" while focusing on containing inflation expectations.

FIGURE 1: TERM STRUCTURE OF U.S. TREASURY FLOWS

Sources: BNY, WM/Refinitiv, Bloomberg. Data as of 5/19/25. Charts provided for illustrative purposes only.

Credit

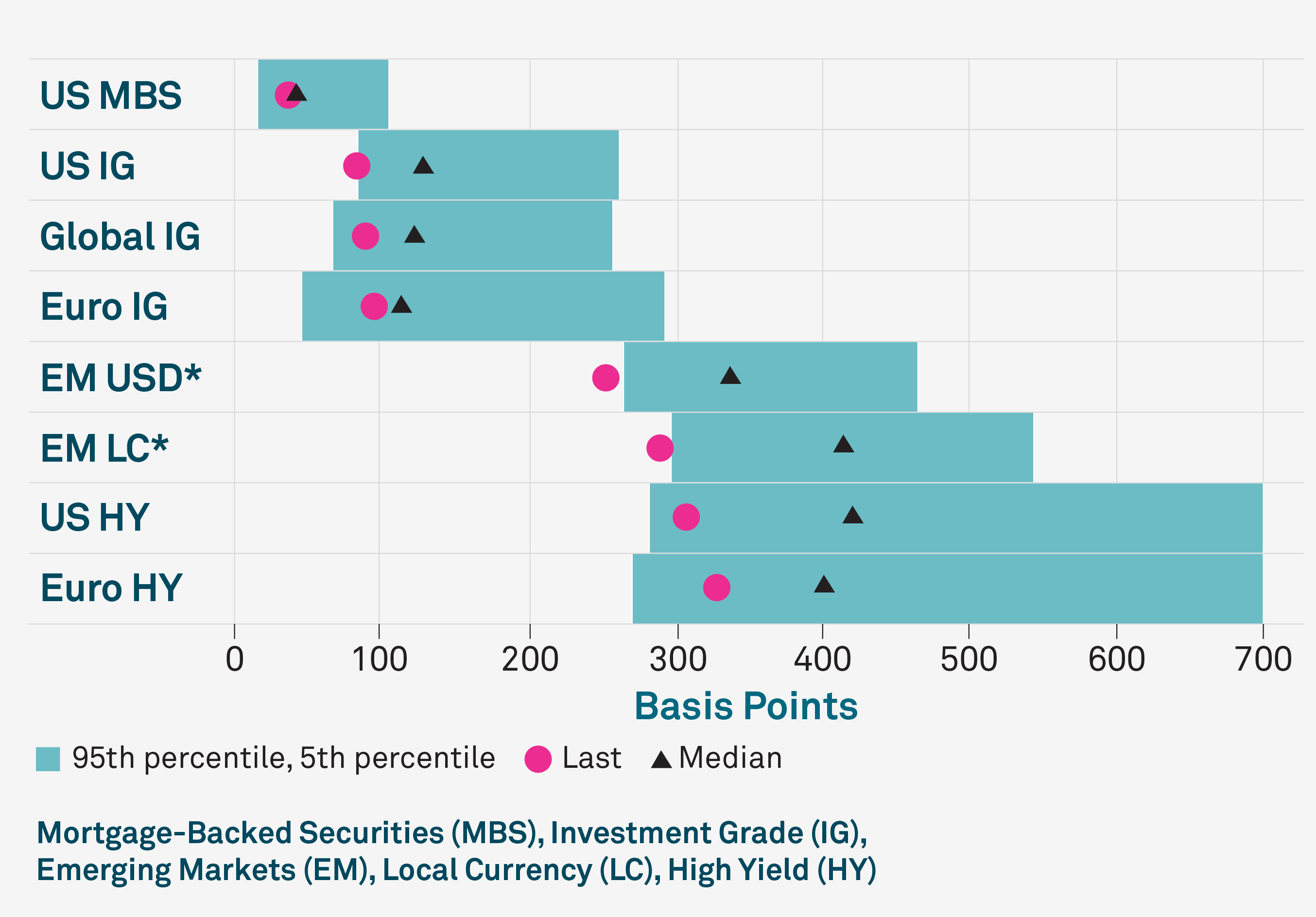

With recent trade policy developments, credit spreads have retraced most of the widening seen since mid-February (Figure 2), heading back to near-historic lows. In the short term, risk appetite may remain supportive, driven by several tailwinds, including resilience in activity data and potentially some improvement in forward-looking sentiment. Additionally, the reduced risk of a U.S.-China decoupling curtails the likelihood of recession, the worst-case scenario for credit investors, and our experts expect other technical factors, such as strong credit demand, to remain supportive.

However, the stagflationary impulse from trade policy remains a concern. Based on our experts’ U.S. outlook, downward pressure on growth and upward pressure on costs and prices is expected. Our experts anticipate the hard data to roll over from the summer as front-loading unwinds and the rise in inflation dampens spending. Though volatility may be expected in the second half of the year, with the risk premium somewhat rising, this can be managed via careful active selection of quality names, international diversification and seeking out relative value opportunities, which will require staying nimble.

FIGURE 2: GLOBAL CREDIT SPREADS

Sources: BNY Investment Strategy and Macrobond. Data as of 5/21/2025. 95th percentile of HY spreads is not shown. *EM debt is shown as a spread vs maturity matched U.S. Treasury yields. Credit spreads referes to the difference in yield between two debt instruments with the same maturity but different credit ratings.

Foreign Exchange (FX)

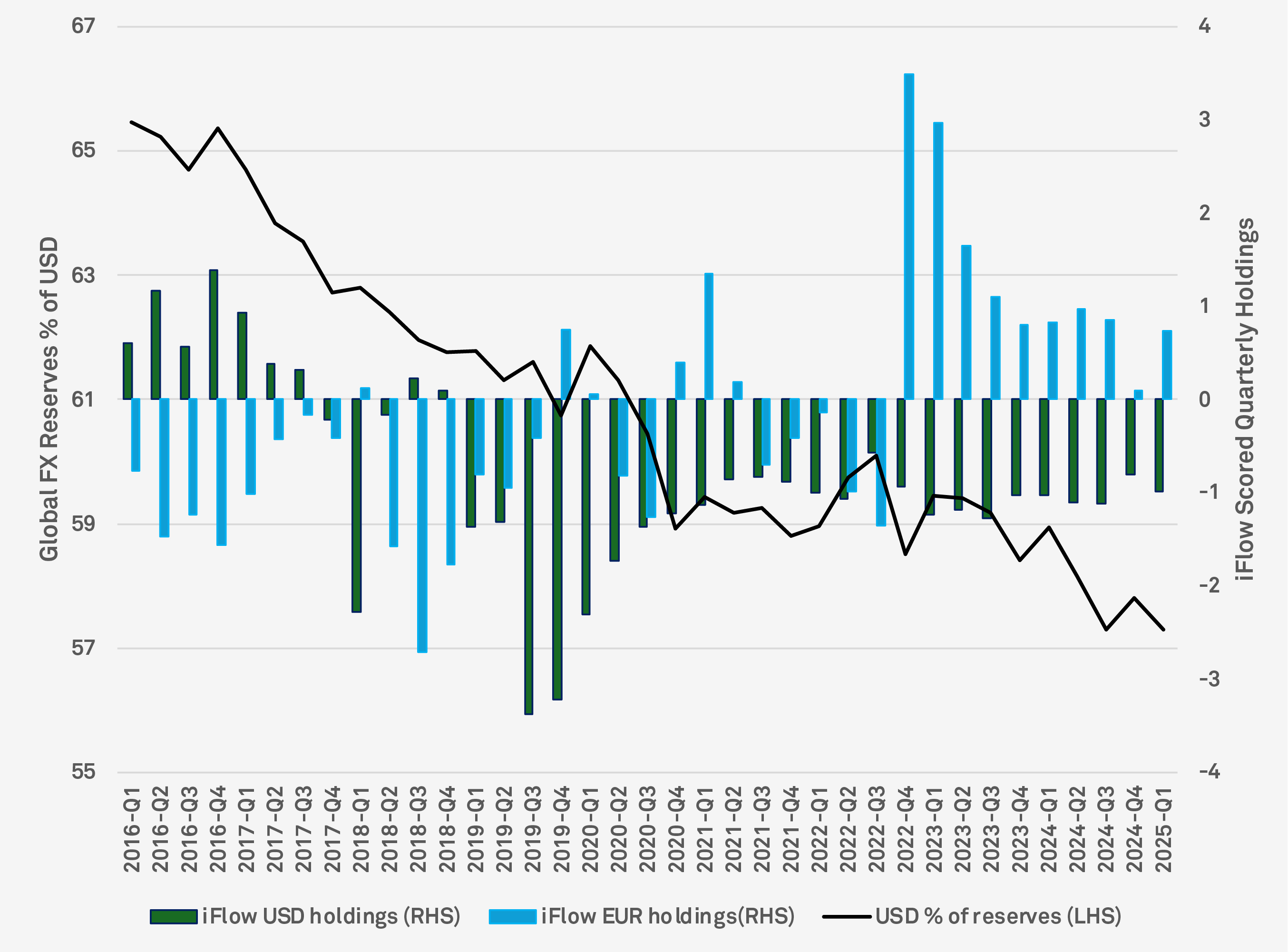

The debate surrounding the USD's status as the world’s reserve currency remains a focal point. Despite its continued dominance, accounting for more usage than all other FX reserve currencies combined, there is a discernible shift towards alternatives like gold and other currency baskets. Notably, the USD’s share of FX reserves has decreased from 65% in 1Q16 to 57% today, marking a 25-year low (Figure 3).

iFlow data reveals a significant reversal in euro (EUR) buying in 2025 , which was near zero at the end of 2024. This trend suggests that investor flows between EUR and USD are more closely tied to economic growth expectations than interest rates or prevailing trends. Despite this shift, the perception around U.S. exceptionalism is evident in dollar hedging and home bias from cross-border flows. FX reserve holdings are increasingly correlated with the volume of USD or EUR held abroad, underscoring the critical role of trade in shaping these dynamics.

The potential for further decline in USD holdings over the coming weeks, months and quarters is influenced by more than just U.S. tariff concerns; U.S. policy and budgetary concerns, the risk premium associated with holding bonds and the volatility of national assets all play a key role. Our experts’ near-term focus will be around U.S. fiscal spending and taxes. The value of the USD and the appetite of cross-border investors to hold U.S. assets have tracked U.S. two-year rates and the S&P 500, but while U.S. asset acquisition is gaining traction, it may no longer carry the label of exceptionalism.

Overall, the potential for an optimistic case exists, where the U.S. remains focused on trade negotiations and decreasing uncertainty, changes in tax and regulation take center stage, and greater policy stimulus from the rest of the world kicks in. One thing is certain: With the rapidly evolving market landscape, our experts think the ability to see through the noise will help investors successfully navigate market swings.

FIGURE 3: USD / EUR HOLDING TRENDS

Source: BNY and International Monetary Fund (IMF) Cofer data (as of 3/30/25), which tracks global FX reserves and is viewed as a link between FX and U.S. bonds and stocks.

Final Thoughts

Overall, we see the potential for an optimistic case, where the U.S. remains focused on trade negotiations and decreasing uncertainty, changes in tax and regulation take center stage, and greater policy stimulus from the rest of the world kicks in. One thing is certain: With the rapidly evolving market landscape, our experts think the ability to see through the noise will help investors successfully navigate market swings.

Bryan Besecker, Eric Hundahl, Alicia Levine, Bob Savage and John Velis contributed to this article.

1 Joanne Hsu, “Consumers Anticipate Rising Unemployment and Elevated Risks of Personal Job Loss,” University of Michigan Surveys of Consumers, May 2025, https://www.sca.isr.umich.edu/

2 William C. Dunkelberg, Holly Wade, “NFIB Small Business Economic Trends,” National Federation of Independent Business, April 2025, https://www.nfib.com/news/press-release/new-nfib-survey-small-business-optimism-declines-in-april/

3 Bloomberg Chief Executive Group, CEO Confidence Index.

iFlow® / FX MARKET COMMENTARY

The products and services described herein may contain or include certain “forecast” statements that may reflect possible future events based on current expectations. Forecast statements are neither historical facts nor assurances of future performance. Forecast statements typically include, and are not limited to, words such as “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “likely,” “may,” “plan,” “project,” “should,” “will,” or other similar terminology and should NOT be relied upon as accurate indications of future performance or events. Because forecast statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict.

iFlow® is a registered trademark of The Bank of New York Mellon Corporation under the laws of the United States of America and other countries. iFlow captures select data flows from the firm’s base of assets under custody, as well as from its trading activity with non-custody clients, on an anonymized and aggregated basis.

BNY

BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally. This material does not constitute a recommendation by BNY of any kind. The information herein is not intended to provide tax, legal, investment, accounting, financial or other professional advice on any matter, and should not be used or relied upon as such. The views expressed within this material are those of the contributors and not necessarily those of BNY. BNY has not independently verified the information contained in this material and makes no representation as to the accuracy, completeness, timeliness, merchantability or fitness for a specific purpose of the information provided in this material. BNY assumes no direct or consequential liability for any errors in or reliance upon this material.

This material may not be reproduced or disseminated in any form without the express prior written permission of BNY. BNY will not be responsible for updating any information contained within this material and opinions and information contained herein are subject to change without notice. Trademarks, service marks, logos and other intellectual property marks belong to their respective owners.

© 2025 The Bank of New York Mellon. All rights reserved. Member FDIC.

BNY Investments

All investments involve some level of risk, including loss of principal. Certain investments have specific or unique risks.

Equities are subject to market, market sector, market liquidity, issuer, and investment- style risks to varying degrees. Small and mid-sized company stocks tend to be more volatile and less liquid than larger company stocks as these companies are less established and have more volatile earnings histories. Investing in foreign- denominated and/or domiciled securities involves special risks, including changes in currency exchange rates, political, economic, and social instability, limited company information, differing auditing and legal standards, and less market liquidity. These risks are generally greater with emerging market countries. Real Estate security investments involve similar risks to those associated with direct investments in real estate, including falling property values due to increasing vacancies or declining rents resulting from economic, legal, political, or technological developments, lack of liquidity, limited diversification and sensitivity to certain economic factors such as interest rate changes and market recessions. Bonds are subject to interest rate, credit, liquidity, call and market risks, to varying degrees. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines. Municipal income may be subject to state and local taxes. Some income may be subject to the federal alternative minimum tax for certain investors. Capital gains, if any, are taxable.

FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS. FOR GENERAL PUBLIC DISTRIBUTION IN THE U.S. ONLY.

This material should not be considered as investment advice or a recommendation of any investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Any statements and opinions expressed are those of the author as at the date of publication, are subject to change as economic and market conditions dictate, and do not necessarily represent the views of BNY. The information has been provided as a general market commentary only and does not constitute legal, tax, accounting, other professional counsel or investment advice, is not predictive of future performance, and should not be construed as an offer to sell or a solicitation to buy any security or make an offer where otherwise unlawful. The information has been provided without taking into account the investment objective, financial situation or needs of any particular person. BNY is not responsible for any subsequent investment advice given based on the information supplied. This is not investment research or a research recommendation for regulatory purposes as it does not constitute substantive research or analysis. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations. Charts are provided for illustrative purposes only and are not indicative of the past or future performance of any BNY product. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance is no guarantee of future results. Information and opinions presented have been obtained or derived from sources which BNY believed to be reliable, but BNY makes no representation to its accuracy and completeness. BNY accepts no liability for loss arising from use of this material.

All investments involve risk including loss of principal.

Not for distribution to, or use by, any person or entity in any jurisdiction or country in which such distribution or use would be contrary to local law or regulation. This information may not be distributed or used for the purpose of offers or solicitations in any jurisdiction or in any circumstances in which such offers or solicitations are unlawful or not authorized, or where there would be, by virtue of such distribution, new or additional registration requirements. Persons into whose possession this information comes are required to inform themselves about and to observe any restrictions that apply to the distribution of this information in their jurisdiction.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: For Institutional, Professional, Qualified Investors and Qualified Clients. For General Public Distribution in the U.S. Only. • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorizsed and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorizsed financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • Singapore: BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

BNY COMPANY INFORMATION

BNY Investments is one of the world’s leading investment management organizations, encompassing BNY’s affiliated investment management firms and global distribution companies. BNY is the corporate brand of The Bank of New York Mellon Corporation and may also be used to reference the corporation as a whole and/or its various subsidiaries generally. • Mellon Investments Corporation (MIC) is a registered investment advisor and subsidiary of The Bank of New York Mellon Corporation. MIC is composed of two divisions: Mellon, which specializes in index management, and Dreyfus, which specializes in cash management and short duration strategies. • Insight Investment - Investment advisory services in North America are provided through two different investment advisers registered with the Securities and Exchange Commission (SEC) using the brand Insight Investment: Insight North America LLC (INA) and Insight Investment International Limited (IIIL). The North American investment advisers are associated with other global investment managers that also (individually and collectively) use the corporate brand Insight. Insight is a subsidiary of The Bank of New York Mellon Corporation. • Newton Investment Management - “Newton” and/or “Newton Investment Management” is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021, NIMJ was established in March 2023. NIM and NIMNA are registered with the Securities and Exchange Commission (SEC) in the United States of America as an investment adviser under the Investment Advisers Act of 1940. Newton is a subsidiary of The Bank of New York Mellon Corporation. • ARX is the brand used to describe the Brazilian investment capabilities of BNY Mellon ARX Investimentos Ltda. ARX is a subsidiary of The Bank of New York Mellon Corporation. • Walter Scott & Partners Limited (Walter Scott) is an investment management firm authorized and regulated by the Financial Conduct Authority, and a subsidiary of The Bank of New York Mellon Corporation. • Siguler Guff - The Bank of New York Mellon owns a 20% interest in Siguler Guff & Company, LP and certain related entities (including Siguler Guff Advisers LLC). • BNY Mellon Advisors, Inc. (BNY Advisors) is an investment adviser registered as such with the U.S. Securities and Exchange Commission (“SEC”) pursuant to the Investment Advisers Act of 1940, as amended. BNY Advisors is a subsidiary of The Bank of New York Mellon Corporation.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

©2025 THE BANK OF NEW YORK MELLON CORPORATION

BMAIAM-745169-2025-05-23 | BABR-744808-025-05-22 | GU-644-30 June 2026